Broad-Based Asset Management Programs

National Asset Management Agency (NAMA)

Purpose

To stabilize the Irish banking sector and restore “the flow of credit […] while minimizing the risk to the taxpayer” (NAMA 2009, 1).

Key Terms

-

Launch DatesApril 7, 2009 (Announcement); December 21, 2009 (Start of operations); (First asset transfer took place between March 29, 2010 and May 10, 2010)

-

Wind-down DatesNAMA did not have an initial wind-down date, but current policy is that NAMA’s would close by the end of 2025

-

Size and Type of NPL ProblemThe government did not know the extent of the NPL problem in commercial loans until NAMA began asset purchases. NAMA purchased land and property development loans as well as any assets related to such loans (both commercial and residential)

-

Program SizeNot specified, but NAMA could issue up to €54 billion to purchase assets

-

Eligible InstitutionsAny credit institution could apply to NAMA, but the Finance Minister ultimately decided which applicants were eligible

-

UsageAssets with a face value of €74.4 billion purchased for €31.8 billion

-

OutcomesProjected surplus of over €4 billion at program termination

-

Ownership StructurePublic-private ownership (majority private)

-

Notable FeaturesExtensive legal authority (though committed to limit use), hedged risk of overvaluation with claw back mechanism, off-balance-sheet SPV structure

After the Irish property boom peaked in 2007, Ireland’s banks faced declining share prices and increasing liquidity pressures. When in the aftermath of the September 2008 collapse of Lehman Brothers, Ireland’s banks lost access to liquidity from abroad, it triggered a banking crisis in the country. In spite of various responses by the Irish government, the financial viability of Ireland’s banks (as well as the government’s fiscal position) continued to deteriorate in early 2009. The Irish government attributed the problem to impaired real estate assets sitting on bank balance sheets, which made it difficult for markets to believe that government’s upcoming capital injections would render the banks solvent. In response, the government created the National Asset Management Agency (NAMA), a majority privately owned asset management company (AMC), to remove these assets from the banks. The ownership structure was complex, being nominally privately owned so that NAMA would not appear on the government balance sheet. Most of the powers and benefits from ownership were structured so that they would accrue to the state. From its establishment under the NAMA Act on December 21, 2009, NAMA purchased assets with a face value of approximately €77.4 billion for €31.7 billion. As of December 31, 2018, it had disposed of all but €2.3 billion of these assets. NAMA was considered one of the best performing AMCs of the era and enjoyed an expansive legal mandate, but it was not sufficient to solve Ireland’s economic woes. Although NAMA was still operating as of 2019, it was projected to wind down by 2025 (having submitted a detailed wind-down plan by the end of 2021) and yield a profit of €4 billion.

|

GDP (SAAR, Nominal GDP in LCU converted to USD) |

$276.5 billion in 2008 $236.4 billion in 2009 $222.5 billion in 2010 |

|

GDP per capita (SAAR, Nominal GDP in LCU converted to USD) |

$61,263 in 2008 $52,105 in 2009 $48,715 in 2010. |

|

Sovereign credit rating (five-year senior debt)

|

As of Q4, 2008 Fitch: AAA Moody’s Aaa S&P: AAA

As of Q4, 2009: Fitch: AA- Moody’s: Aa1 (negative outlook) S&P: AA

As of Q4, 2010 Fitch: BBB+ Moody’s: Baa1 S&P: A*- |

|

Size of banking system

|

$470.0 billion in total assets in 2008 $ 42.7 billion in total assets in 2009 $ 373.4 billion in total assets in 2010 |

|

Size of banking system as a percentage of GDP |

169.94% in 2008 177.85% in 2009 167.84% in 2010 |

|

Size of banking system as a percentage of financial system |

100% in 2008 100% in 2009 100% in 2010 |

|

Five-bank concentration of banking system |

90.7% of total assets at the end of 2008 90.8% of total assets at the end of 2009 87.2% of total assets at the end of 2010 |

|

Foreign involvement in banking system |

36.0% of total banking assets in 2008 35.0% of total banking assets in 2009 35.0% of total banking assets in 2010 |

|

Government ownership of banking system |

0% at the end of 2008 7.27% at the end of 2009 20.69% at the end of 2010 |

|

Existence of deposit insurance |

In early 2008, 90% of deposits, with a maximum payout of $27,777.78 (€20,000) As of September 2008, $138,888.90 (€100,000) with no co-insurance In December 2008, unlimited In 2009, $138,888.90 (€100,000) with no co-insurance In 2010, $138,888.90 (€100,000) with no co-insurance |

|

Sources: Bloomberg; World Bank Global Financial Development Database; World Bank Deposit Insurance Dataset; IMF International Financial Statistics. |

In late 2008, uncertainty stemming from the Global Financial Crisis (GFC) burst the real estate bubble supporting Ireland’s economy and triggered a banking crisis. Between September 2008 and April 2009, the Irish government responded with blanket guarantees, bank recapitalizations, and bank nationalization, but the financial viability of the banks (as well as the government’s fiscal position) continued to deteriorate. Government analysts traced the credibility problem to the impaired real estate assets populating the balance sheets of Ireland’s largest banks. On April 7, 2009 the government recommended that Ireland establish a centralized, majority privately owned asset management company, the National Asset Management Agency (NAMA), to remove these assets from the balance sheets and persuade the market that its banks were adequately capitalized. NAMA would then manage and dispose of these assets, aiming to optimize returns for the Irish public.

Ireland established NAMA on December 21, 2009, under the National Asset Management Agency Act 2009. NAMA eventually purchased assets with a face value of approximately €74.4 billion for €31.8 billion by issuing government guaranteed securities. Although NAMA did not prevent Ireland from requiring an EU-IMF Programme that began in November 2010, NAMA disposed of all but €2.3 billion in remaining assets by the end of 2018 and projected that it would return over €4 billion in profit to the taxpayers by the anticipated end of its life in 2025.

The effectiveness of NAMA at stabilizing the Irish economy is uncertain. The consensus seems to be that NAMA was effective at performing the functions asset management companies are expected to perform. As a whole, NAMA was considered one of the more well-developed and commercially successful European asset management companies of the GFC era. Like the other interventions preceding Ireland’s eventual IMF-EU program, NAMA was not enough to solve Ireland’s financial problems. However, it was able to effectively carve out much of the toxic assets in Irish banks, making it possible to credibly recapitalize the banks. The problem was that Ireland did not have enough fiscal room to do this without an IMF-EU program. NAMA remained politically unpopular, having to grapple with the combination of a perceived transparency problem and early delays that further aggravated a sense of uncertainty.

Key Design Decisions

Part of a Package

1

The announcement and creation of NAMA in 2009 did not initially appear to be coordinated with other programs. By the time that NAMA was established, the government had nationalized ANGLO and also injected capital into ANGLO, AIB, and BOI (Cussen and Lucey 2011) (See Figure 8).

However, the Central Bank of Ireland knew that its March 2010 stress test would reveal significant losses. The stress test, known as the Prudential Capital Assessment Review (PCAR), projected the capital each bank would need by the end of 2012 to meet regulatory capital requirements (Honohan 2015; Honohan 2012; Honohan 2010; NAMA Frequently Asked Questions 2009, 10-11). This would theoretically make transparent to the public the size of banks’ losses. Based on the haircuts, the banks would raise more capital (via government capital injections or via the private sector).

However, the haircuts that came with NAMA’s asset valuations and purchases were larger than those projected by the stress tests, creating further uncertainty (Honohan 2015; Honohan 2012; Honohan 2010; NAMA Frequently Asked Questions 2009). NAMA was originally expected to cement confidence in the stress test projections and create market certainty as to the health of Ireland’s banks. These larger than expected haircuts did the opposite. Responding to the larger-than-expected haircuts problem, policymakers in 2010 injected at least €23 billion into Anglo Irish Bank, €0.35 billion into EBS, €2.3 billion into INBS, and €3.7 billion into Allied Irish Banks (See Figure 8). They hoped that the new capital could fill the larger-than-expected capital holes exposed by NAMA (Cussen and Lucey 2011, 83). The government had enough money on hand to fill the holes projected by the stress tests, but not the larger-than-expected ones exposed by NAMA. Therefore, the government had to seek a program from the troika (Honohan 2019).

It is also important to note that these capital injections were not required for these domestic banks to participate in NAMA. Nor was participation in NAMA required for banks to be recapitalized (National Asset Management Agency Act 2009, Revised 2018). However, recapitalization was certainly mandatory for the participating banks because of their performance in the stress tests (Honohan 2015; Honohan 2012; Honohan 2010; NAMA Frequently Asked Questions 2009). For foreign-owned banks in Ireland, the government requested that they be recapitalized using funds from their parent companies before requesting funding from the government for recapitalization (Cerruti and Neyens 2016). That being said, none of the foreign-owned banks in Ireland requested government funding or applied to NAMA.

It is also important to note that these capital injections were not required for these domestic banks to participate in NAMA. Nor was participation in NAMA required for banks to be recapitalized (National Asset Management Agency Act 2009, Revised 2018). However, recapitalization was certainly mandatory for the participating banks because of their performance in the stress tests (Honohan 2015; Honohan 2012; Honohan 2010; NAMA Frequently Asked Questions 2009). For foreign-owned banks in Ireland, the government requested that they be recapitalized using funds from their parent companies before requesting funding from the government for recapitalization (Cerruti and Neyens 2016). That being said, none of the foreign-owned banks in Ireland requested government funding or applied to NAMA.

Legal Authority

2

After the April 7, 2009, announcement of NAMA, the government drafted the NAMA Act to grant NAMA any authority “necessary for, or incidental to, the achievement of its purposes and the performance of its functions.” The government introduced a draft version of the NAMA Bill on July 30, 2009, which was revised and eventually became the NAMA Act when the Taoiseach (Ireland’s prime minister) signed it into law on November 22, 2009, in spite of substantial public opposition (National Asset Management Agency Act 2009).

The NAMA Act had to comply with European state aid rules (Cahill and O’Donnell 2010). NAMA would constitute state aid. Therefore, NAMA could only be compatible with the EU’s internal market if it met the criteria for EC state aid rules for asset relief measures. These criteria were established in the Communication from the Commission on the Treatment of Impaired Assets in the Community Banking Sector of February 25, 2009 (better known as the Impaired Asset Communication and the IAC) (Communication from the Commission 2009; Cas and Peresa 2016).

These criteria pertained to the following aspects of the program:

- “Transparency and disclosure requirements;”

- “burden sharing between the State, shareholders and creditors;”

- “aligning incentives for beneficiaries with public policy objectives;”

- “principles for designing asset-relief measures in terms of eligibility, valuation and management of impaired assets;” and

- “the relationship between asset relief, other government support measures and the restructuring of banks” (Communication from the Commission 2009).

The EC found NAMA to be consistent with State aid criteria. The EC approved the establishment of NAMA on February 26, 2010. It then required NAMA to submit each of NAMA’s asset transfers (and the corresponding valuation) to the EC for review (Cas and Peresa 2016; Martin 2010).

Special Powers

1

NAMA was seen as having a broad legal mandate (Cas and Peresa 2016). The Minister for Finance also buttressed NAMA’s authority with a bevy of statutory amendments between 2009 and 2013 (NAMA Amendments 2019). As a result, NAMA was protected from a variety of types of liability and had special rights during legal proceedings, reflecting policymakers’ concern that “litigation might hinder the achievement of NAMA’s objectives” (Carroll and Dodd 2012; National Asset Management Agency Act 2009, Revised 2018)

These rights and protections included, but were not limited to the following examples:

- If an asset acquired by NAMA were secured by a charge, then NAMA could redeem or discharge any charges on an acquired asset that were senior to NAMA’s, rendering NAMA the senior creditor (National Asset Management Agency Act 2009, Revised 2018);

- NAMA could void certain transactions that “hinder the acquisition or impair the value of an eligible bank asset”;

- For certain claims, the NAMA Act restricted the remedies available for damages and also restricted the power of the courts to “grant injunctive relief”;

- NAMA could join certain legal proceedings “in lieu of or in addition to” the participating banks (Carroll and Dodd 2012).

NAMA also had the power to issue directions to participating institutions to deal with any unacquired portion of an asset that NAMA had acquired from said institution in any way specified by NAMA. Participating institutions were required to obey these directions and “dealing with” could mean the participant giving NAMA title to an asset in situations where NAMA acquired a derivative that captured the proceeds of said asset (National Asset Management Agency Act 2009, Revised 2018).

NAMA had the power to access information on its borrowers from tax authorities as well as any necessary information on its acquired assets from the government’s Land Registry (National Asset Management Agency Act 2009, Revised 2018; Cerruti and Neyens 2016). The NAMA Act provided NAMA with the “compulsory right of purchase”, the right to petition the Court for vesting orders, and the ability to appoint a statutory receiver to a participant’s assets (Cerruti and Neyens 2016). All three of these powers allowed NAMA to increase its control over the relevant asset (and potentially its underlying property) (Property Registration Authority 2014). The first two of these powers aimed to help NAMA in its effort to avoid fire sales. The compulsory right of purchase was similar to the eminent domain powers enjoyed by authorities in the United States; it made it less costly in time and money to acquire distressed assets. The vesting order right made it possible for NAMA to convert its security interest in underlying collateral into outright ownership (Carroll and Dodd 2012; McNulty 1912). As part of EC state aid proceedings, Ireland committed to consult with the EC before using its “compulsory right of purchase” power; however, it did not need to consult with the EC in situations involving ransom strips of land—that is, land needed to access an adjacent property from a public highway (Martin 2010). The EC also required the Irish authorities to commit that NAMA wouldn’t use its vesting order power in the context of a syndicated loan without the agreement of the other syndicate members.FThe EC asked Ireland to restrict NAMA’s use of several other powers that it understood to be “potentially more distortive” of competition (Martin 2010).

The power to appoint a statutory receiver allowed NAMA to appoint a receiver to take possession of the collateral securing its assets; this was an unprecedented power within Irish creditor-debtor law. This power became NAMA’s favored tool for pursuing uncooperative debtors (Carroll and Dodd 2012). According to NAMA officials, NAMA needed this power because Irish insolvency law at the time was extremely outdated; bankruptcy under existing laws could take as long as 12 years. Legislators were already debating bankruptcy reforms that included features like the power to appoint a statutory receiver. While these reforms would not happen until 2012, some of the features made their way into the NAMA Act 2009 (Susan McDermott and Jamie Bourke of NAMA, Zoom discussion with author, February 26, 2021).

Mandate

1

NAMA’s initial mandate was to realize the aims of the NAMA Act by acquiring eligible bank assets from participating institutions, “as is appropriate,” dealing with such acquired assets “expeditiously,” and enhancing or protecting the value of the assets in the interest of the government (gov.ie 2019). To this end, NAMA’s commercial mandate was to obtain the best achievable financial return for the government, taking the three following parameters into account: (1) The amount of money the Irish government paid to acquire and manage the assets, (2) NAMA’s cost of capital and operating costs, and (3) any other factor that NAMA thinks is relevant to realizing its purpose (National Asset Management Agency Act 2009, Revised 2018).

NAMA’s mandate did evolve over time. As Ireland’s economic health deteriorated in the second half of 2010, NAMA began to emphasize its role in the restructuring of the banking system (NAMA Second Progress Report 2018). After NAMA’s asset disposals then accelerated and its portfolio shrank, NAMA’s mandate gradually shifted to one focused on the development of affordable housing in Ireland (Dodd 2012; O’Dwyer 2016; NAMA Progress Report 2014). This related to one of the aims of the NAMA Act, which was to “contribute to the social and economic development of the state” (Susan McDermott and Jamie Bourke of NAMA, Zoom discussion with author, February 26, 2021).

Communication

1

NAMA officials appeared on radio programs to explain the organization’s activities and supplied anonymous as well as official information to newspapers (Carswell 2010; Irish Independent 2012).FNAMA officials were bound by a Code of Conduct and by the Official Secrets Act 1963 that kept them from providing confidential information through external sources (NAMA Annual Report 2010). NAMA did not have a constituency in the banking or property development industry, with its Chairman stating in the 2010 Annual Report that “I do not believe that any other State Agency has come into being with a potential client base—those in banking and property development—whose enthusiasm for it was so lukewarm” (NAMA Annual Report 2010).

According to NAMA officials, the organization’s messaging evolved as the institution’s work evolved. When NAMA was first proposed, the Irish government did not promote NAMA as a guaranteed cure for the economy’s woes and very much presented the NAMA scheme as a work in progress. Government officials communicated that the potentially large (and uncertain) cost of NAMA’s purchases and the make-up of Ireland’s sovereign bond holders could have negative impact on Ireland’s fiscal situation. However, it seemed to hedge those concerns by stating that “The income streams from the NAMA assets will mitigate the cost to the Exchequer of servicing the additional debt and the proceeds from their eventual sale will accrue to NAMA and the Exchequer (Houses of the Oireachtas May 2009).”

Several other key themes echoed throughout NAMA’s communications. One was that NAMA was not a bailout for developers or a bad bank. Government statements referred to NAMA as an “asset management agency” rather than as a “bad bank,” with the Taoiseach claiming that NAMA “is not a bad bank model […] because it obviously takes in all loans, including performing loans.” The word “bailout” only seemed to appear when NAMA was being discussed in the Oireachtas or in simplified NAMA documents (which may have been aimed at the general public) like the three-page “The National Asset Management Agency: A Brief Guide” (NAMA Brief Guide 2010; Houses of the Oireachtas May 2009a).

From 2013, as NAMA’s asset sales accelerated, messaging shifted toward emphasizing the organization’s ability to meet its strategic objectives (Susan McDermott and Jamie Bourke of NAMA, Zoom discussion with author, February 26, 2021). Around this time, NAMA started talking more about its social and economic contributions. NAMA’s focus on its social and economic contributions became more dominant as the organization took on more of a role as a housing developer in the mid-to-late 2010s (Dodd 2012; O’Dwyer 2016).

Although NAMA publicly emphasized its commitment to transparency early on in its life, references to transparency (beyond transparency in its procurement process) in official communications were less common in annual reports released after 2010 (NAMA Annual Report 2010; NAMA Annual Report 2012; NAMA Annual Report 2013; NAMA Annual Report 2018). That being said, NAMA states that it has been fully transparent within the constraints put on it by Irish laws and confidentiality rules (Susan McDermott and Jamie Bourke of NAMA, Zoom discussion with author, February 26, 2021).

Another theme in NAMA’s communications is best expressed by the statement “NAMA is not the problem, it is merely cleaning up a problem that was created by others.” Officials tended to describe what NAMA would do using nonfinancial terms like “cleansing” and “crystallising” losses. NAMA would act in a commercial manner, but would not hesitate to put pressure on the banks and borrowers. For example, NAMA asserted that it would only be providing funding to developers “where it will make commercial sense” and criticized the banks by stating that NAMA’s operations had “revealed a troubling picture of poor loan documentation, of assets not properly legally secured and of inadequate stress-testing of borrowers and loans—all born of a mindless scramble to funnel lending into one sector at considerable pace and of a reckless abandonment of basic principles of credit risk and prudent lending” (McDonagh 2010).

Ownership Structure

1

If NAMA’s assets ended up on the government’s balance sheet some policymakers believed that there would be an increased possibility that “Irish […] [deficit] levels could be artificially distorted as a result of loan foreclosures” on loans with collateral located in Ireland. Eurostat regulations mandated that NAMA’s assets needed to have majority private ownership to not be on the government balance sheet and enjoy a government guarantee at the same time (Cussen and Lucey 2011).

To fulfill this requirement, NAMA conducted most of its operations through an Irish SPV created by NAMA called National Asset Management Agency Investment Ltd. (Called NAMAIL or the Invest Co.). Invest Co. was a public-private partnership with initial capital of €100 million. Three sets of private investors (Irish Life & Permanent, New Ireland Assurance (Bank of Ireland Group), and “a group of clients of Allied Irish Banks’ Investment Managers”) held a 51% stake and NAMA held a 49% stake with veto power over strategic decisions (Martin 2010; Cas and Peresa 2016). Beneath this SPV were three Section 110 SPVs, which enjoyed special tax status (allowing for only a nominal tax burden), and two conventional Irish SPVs (See Figure 4) (NAMA Acquisition of Bank Assets 2010; NAMA Second Progress Report 2018). NAMA wanted to reduce the tax liability of its subsidiaries because NAMA’s exemption from “income tax, corporation tax and capital gains tax” under Section 214 of the NAMA Act did not apply to subsidiaries.FSuch maneuvers were common in Irish finance at the time, though this would change with legal reforms in 2016. Although the NAMA Act did not allow NAMA itself to downstream its own tax-exempt status to its subsidiaries, Irish corporate law, with its treatment of Section 110 SPVs, allowed NAMA to decrease its tax burden in line with other Irish corporations of the time.

Invest Co. created (and owned a 100% stake in) a Section 110 SPV called National Asset Management Ltd. (also known as the Master SPV). The Master SPV then owned a subsidiary Section 110 SPV called National Asset Management Group Services Ltd. (the Intermediate Co.). The Intermediate Co. owned three functional subsidiaries: a Section 110 SPV known as National Asset Loan Management Ltd. (the Acquirer Co.), a conventional Irish SPV known as National Asset Property Management Ltd. (the Property Co.), and a conventional Irish SPV known as National Asset Management Services Ltd. (the Management Services Co.) (NAMA Acquisition of Bank Assets 2010).

Together, the companies functioned as follows: The Acquirer Co. directly received the assets that NAMA bought, which included any income from interest on the loans, and initiated enforcement proceedings against the borrowers of the loans as needed. As the Acquirer Co. could not “carry on any activities ancillary to holding and managing the loans,” it sold the properties it acquired to the Property Co. for zero consideration upfront. The Property Co. then managed these properties and used its property management profits to pay corporation taxes. The Property Co. would eventually dispose of the assets and pay the resulting proceeds to the Acquirer Co. as delayed consideration. The Acquirer Co.’s after tax proceeds then flowed back up through the other SPVs to the Master SPV, which paid a performance-based dividend to Invest Co.’s private investors and then paid any remaining surplus to NAMA. Finally, NAMA paid the surplus it received from the Master SPV to the Exchequer (NAMA Acquisition of Bank Assets 2010).

In order to limit the benefits and potential losses for NAMA’s private-sector shareholders, NAMA placed a cap on their possible annual return or loss to 10% above or below the yield on the 10-year Irish government bond yield, with remaining profits (losses) going to NAMA (Braakman and Forster 2011).

Meanwhile, the Management Services Co. handled the expenses, tax administration, and financial operations of these companies (Carroll and Dodd 2012).

This private ownership legal structure was based on a French program called Société de Financement de l’Économie Française (SFEF). SFEF used a majority privately owned vehicle to issue government guaranteed debts and lend the proceeds to French financial institutions in need of liquidity. NAMA chose to follow this structure, because it initially fit well with Eurostat accounting guidelines. These guidelines allowed majority-private interventions like SFEF and NAMA to avoid being counted as part of the public debt (Cussen and Lucey 2011).

The Eurostat regulation also required that NAMAIL be “of a temporary duration,” “created solely to deal with the financial crisis,” and not be “expected to incur losses” (Cussen and Lucey 2011). By 2016, these Eurostat rules changed, placing asset management companies like NAMA on the government balance sheet if the company’s funding structure had a government guarantee, even if the AMC were privately owned (Cas and Peresa 2016). However, it is not clear how much a difference the changed Eurostat rules would have made to NAMA’s operations. Ratings companies classified NAMA as part of the Irish sovereign’s balance sheet and the Irish government had to enter an EC-IMF program at the end of 2010 regardless (European Commission 2019a; Cullinan and Beers 2010).

NAMA’s SPV structure and use of profit participation loan (PPL) agreements initially also allowed NAMA to pay almost no taxes. Under such agreements, the Section 110 SPVs would pay interest on the PPLs dependent on its profitability. However, due to a number of changes in the tax law in 2016, NAMA restructured the Acquirer Co. into a “regular trading company” when the PPL tax deduction was restricted (NAMA Second Progress Report 2018).

Governance/Administration

2

NAMA was structured as a statutory corporation (not a bank) and was governed using a nine-person Board. The composition of NAMA’s Board was as follows:

- Seven members appointed by the Minister for Finance

- Two ex-officio members appointed by the Minister for Finance

- The CEO of NAMA (appointed by the Minister for Finance in consultation with the Chief Executive of the NTMA)

- The Chief Executive of the NTMA (National Asset Management Agency Act 2009, Revised 2018)

Additionally, NAMA was subject to various anti-corruption acts and a number of other anti-corruption related provisions. The NAMA Act made lobbying NAMA, defined broadly, a legal offence (Carroll and Dodd 2012; National Asset Management Agency Act 2009, Revised 2018). This provision also penalized people who believed that they received a communication that constituted lobbying under the NAMA Act, but did not report the details of the communication to the Garda (police) promptly. The NAMA Act also contained provisions that appeared to protect whistle-blowers (National Asset Management Agency Act 2009, Revised 2018).

NAMA was provided with staff, “human resources, IT and market risk analysis” servicesFOver time, NAMA developed an extensive IT interface that included a public database of “NAMA-related properties in receivership in Ireland, Northern Ireland and Great Britain.” (See NAMA Annual Report 2018). by its parent, the National Treasury Management Agency (NTMA) (Cas and Peresa 2016).FNTMA was “reimbursed by NAMA for the costs of these services.” (See Cas and Peresa 2016). Although the NTMA was the organization in charge of issuing and managing Irish government debt, it was not formally part of the Ministry of Finance. (See Linehan 2012). As a result, NTMA did not have to be staffed by civil servants (although its chief was to be appointed by the Minister for Finance) and could pay its employees a salary that was similar to those in the private sector while cutting down the amount of bureaucracy required for decision-making (as well as hiring). The NTMA was also the institution in charge of managing the national pension fund. NAMA expected to have around 100 employees (Connolly 2017, 1-2), but grew to a size of up to 380 employees with specialist skills in property, banking, finance, law, and related disciplines (Williams 2014). This number does not include the roughly 500 people at the five participating banks who managed NAMA’s €13 billion exposure to smaller debtors (About NAMA 2014). For staff and contractors involved in asset management, NAMA drew on “many former development companies and former banking interests” (Williams 2014). Until around 2014, NAMA’s staff enjoyed bonuses linked to employee performance (Cerruti and Neyens 2016). A change in this policy, and NAMA’s March 2012 reorganization from asset purchase and valuation to asset management, caused NAMA to lose critical staff (NAMA Annual Report 2012). Anticipating NAMA’s eventual winding-down, NAMA implemented a voluntary redundancy program in 2015, which NAMA’s Chief Executive described as “helpful to date in stemming the volume of staff departures at a time when an uncontrolled exodus would have been seriously damaging to our business.” Nevertheless, NAMA did not appear to have remedies for retaining “specialist staff,” which NAMA believed could be easily poached by the recovering private sector (NAMA Annual Report 2015).

Discussions with NAMA staff revealed that though NAMA could pay market rates, its positions were largely for contractors (Susan McDermott and Jamie Bourke of NAMA, Zoom discussion with author, February 26, 2021). As an organization with a limited lifetime, employees could not be certain that these contracts would always be renewed. Therefore, some employees started to leave as the market improved, reasoning that NAMA could not offer enough job security.

NAMA had significant accountability to the Minister for Finance, the Oireachtas, and the EC. As for the two former groups, NAMA had to do several things. It had to submit annual reports to the Minister for Finance, keep accounts in a form specified by the Minister for Finance, and produce quarterly reports for the Minister for Finance (that would then be passed on to the Oireachtas). It also had to produce reports at the behest of the Minister for Finance, submit to audit by the Comptroller and Auditor General, and be accountable to the legislative Dail Eireann Committee of Public Accounts (PAC) (Carroll and Dodd 2012). NAMA’s Chairperson and CEO were required to report to other committees in the Oireachtas that had been appointed to “examine matters related to NAMA” (National Asset Management Agency Act 2009, Revised 2018). Although NAMA was required to “act in a transparent manner in carrying out its functions,” it only had to do so to the extent that it was “consistent with proper and efficient and effective discharge” of its functions (Carroll and Dodd 2012). As for the EC, NAMA had to report to the EC every six months on its participating banks’ restructuring plans and the functioning of the program. NAMA also had to report to EC’s and the Republic of Ireland’s competition authorities each year on the “use of NAMA’s post acquisition powers” (Martin 2010).

Operationally, NAMA enjoyed a significant amount of independence because the Minister for Finance only appeared to intervene in NAMA on a limited basis (Carroll and Dodd 2012).FHowever, University College Dublin economist Karl Whelan argued that the Minister for Finance strained NAMA’s independence when he ordered that NAMA acquire a loan facility between IBRC and the Central Bank of Ireland. This order aimed to limit the damage of IBRC’s special liquidation in April 2012 (See NAMA Second Progress Report 2018). (See Whelan 2012). However, the Minister for Finance was able to control NAMA using several tools. Under the NAMA Act, the Minister for Finance could issue binding written guidelines and directions to NAMA. NAMA would have to “have regard to any guidelines issued by” the Minister for Finance and be required to comply with written directions from the Minister for Finance “concerning the achievement of the purposes of this Act” (National Asset Management Agency Act 2009, Revised 2018). The Minister could also determine which organizations could participate in NAMA, which assets would count as eligible assets, and have the final say over whether a “particular asset may be acquired.” They also had the final say on the “total value of a portfolio of assets to be acquired from a participating institution” in cases where the participants filed a dispute with NAMA (Carroll and Dodd 2012). The structure of NAMA’s Board, in which seven of its nine members and NAMA’s CEO were appointed by the Minister for Finance, also granted the Minister for Finance a significant amount of power over the organization (National Asset Management Agency Act 2009, Revised 2018).

In practice, as of 2019, the Minister for Finance issued six directions and twelve statutory instruments under the NAMA Act (National Asset Management Agency Act 2009, Revised 2018). The Minister for Finance also issued four directions under the IBRC Act in 2013 (Carroll and Dodd 2012).

There were only three events where the Minister for Finance used its powers to issue directions and statutory instruments under the NAMA Act to become visibly involved in NAMA’s day-to-day operations. The first was when the Minister for Finance put forward two statutory instruments and a direction requiring NAMA to expedite its asset acquisition process (eliminating the tranche system) (Lenihan 2010; S.I. No. 504 2010; S.I. No. 505 2010). The others were two operations related to the IBRC; one of the directions under the NAMA Act and all four directions under the IBRC Act ordered NAMA to support the special liquidation of IBRC in various capacities (Legislation).

Program Size

1

There was no cap on the face value of the assets NAMA would purchase, but the NAMA Act allowed the organization to issue up to €54 billion in debt securities for the purchase of assets before asking the government for permission to spend additional funds (Carroll and Dodd 2012). This number was arrived at by estimating the long-term value of the assets expected to be eligible for transfer to NAMA. €47 billion of this figure represented the then-current market value of the assets. They determined the remaining €7 billion by applying a number of statutory uplift factors (related to the expected default rate, the proportion of performing loans, etc.) (NAMA Business Plan 2009).

Ultimately, NAMA spent €31.8 billion to acquire assets with a face value of €74.4 billion.

Funding Source

2

NAMA ultimately funded its asset purchases by issuing €30.2 billion in state-guaranteed senior bonds usable as collateral in the Eurosystem and €1.6 billion in subordinated bonds. Minister for Finance Brian Lenihan said that the purpose of these subordinated bonds was that they “put […] the bank at risk if NAMA were to lose money […] without giving them an upside in relation to its gains” (Houses of the Oireachtas September 2009).

The terms of the senior bonds included (but were not limited to) the following (NAMA 2011):FThis information is from the March 1, 2011, circular, but the 2011 issuance was in substantially the same form as the 2010 issuance (with exception of the fact that the 2011 issuance “may be physically settled at maturity at the option of the Issuer upon not less than 20 business days’ notice to holders by issuing a new Note on the same terms as the existing Note,” while the 2010 issuance could be “physically settled at maturity at the option of the Issuer upon not less than 10 business days’ notice. (See NAMA 2011.)

- Principal and Interest guaranteed by The Minister for Finance of Ireland

- Maximum Amount Outstanding: €51,300,000,000

- Currency: Euro, Sterling, or U.S. Dollars

- Issue Date: March 26, 2010 (Carroll and Dodd 2012)

- Maturity: March 1, 2011 (it is uncertain whether all the senior debt would be rolled over annually)

- Interest Rate (paid semi-annually on March 1 and September 1):

- For Euro-denominated Notes: six-month Euribor

- For Dollar-denominated Notes: six-month LIBOR

- For Sterling-denominated Notes: six-month LIBOR (NAMA 2011)

The architects of the senior bonds appear not to have anticipated that the six-month Euribor rate might decrease to the extent that the bonds bore a negative interest rate. If the notes carried a negative interest rate, they could not be used as collateral with the ECB and this would therefore make it more difficult for their holders to fulfill “their regulatory liquidity requirements.”FThat being said, negative rates were not a common occurrence, let alone perceived as a likely occurrence when these senior bonds were designed (Liu and Anderson 2013). When the six-month Euribor rate declined to 4.9 basis points in late July 2015, the Minister for Finance began to worry that a negative interest rate was a significant possibility. In response, the Minister directed NAMA to “take appropriate steps to ensure that in the event that the 6[-]month Euribor is negative a negative rate will not apply to the Notes.” He continued, writing that NAMA was “to ensure that these notes remain eligible as collateral for Eurosystem monetary policy operations” in so far as was possible (Noonan 2015).

The terms of the subordinated bonds included (but were not limited to) the following (NAMA 2010):

- Aggregate Nominal Amount and Issue Price: 5% of the total acquisition value of the acquired portfolio of each participating institution (€1.6 billion)

- Currency: Euro

- Issue Date: March 26, 2010

- Interest Rate: 10-year Irish Government bonds rate as of March 26, 2010 (the first issue date), plus 75 basis points, paid annually starting March 1, 2011, if the Board of the Issuer determines the Issuer is “achieving objectives” related to NAMA’s financial performanceFUntil NAMA achieved these objectives, the subordinated bonds would serve as a loss-bearing liability held by participants. (Carroll and Dodd 2012; NAMA Annual Report 2018).

- First Call Date: March 1, 2020

- Term: Perpetual

NAMA funded its day-to-day operations through government borrowing and €51 million in equity provided by the various private organizations investing in NAMA’s SPV (Martin 2010; Cas and Peresa 2016). In practice, NAMA was able to sustain itself using funds generated by its operations after it repaid €299 million in loans from the Central Fund by February 2011 (NAMA Annual Report 2011; McDonagh 2013). NAMA originally expected to issue commercial paper, but this proved difficult amidst Ireland’s deteriorating financial conditions (Martin 2010; Cas and Peresa 2016).

NAMA enjoyed a loss-sharing clawback provision under the NAMA Act. Under this provision, if NAMA ended up with a loss, NAMA could impose a tax on its participants to make up the loss. The EC pointed to this tool as one of NAMA’s two “risk-sharing-mechanisms.” However, the feature was controversial during NAMA’s design (Martin 2010). NAMA’s (pre-establishment) interim CEO Brendan McDonagh and the future Minister for Finance Brian Lenihan argued against the measure during debates on Peter Bacon’s initial NAMA proposal. According to them, “the appropriate place to impose the levy would be finance legislation rather than the NAMA legislation [because] it might have an effect on the valuation of the assets to be transferred” as the clawback essentially represented “an unpriced option in terms of what the clawback would be in the future” (Houses of the Oireachtas May 2009b). Although similar loss-sharing features might have been controversial when put forward in other countries, legislators adopted the provision in response to “voters’ anger over the rising cost of the bank bailout and simultaneous fiscal tightening,” and the provision ceased to be particularly newsworthy soon after (Gumuchian 2010).

Eligible Institutions

3

Once NAMA was established (on December 21, 2009) “[a]ny credit institution, including Irish subsidiaries of foreign credit institutions,” that wished to participate had 60 days (until February 19, 2010) to apply. All five applicants were Irish banks and their subsidiaries that were covered by the Irish government’s blanket guarantee (Martin 2010). NAMA started collecting information from some of these banks in mid-2009, as there were already public expectations that certain troubled banks (like ANGLO) would apply (NAMA Acquisition of Bank Assets 2010).

Before NAMA began, the government requested that foreign banks subsidiaries in Ireland be recapitalized using funds from their parent companies before requesting funding from the government; however, this became a moot point because no foreign bank subsidiaries applied to participate in NAMA and a similar requirement did not exist for the other domestic banks (Cerruti and Neyens 2016).

Within three months of receiving an application, the Minister, after consultation with the Governor of the Central Bank and Regulatory Authority, would determine if an applicant could participate based on three factors (Martin 2010; National Asset Management Agency Act 2009, Revised 2018):

- Systemic importance of the applicant, which was determined using a standardized rubric (Martin 2010, 37; NAMA Acquisition of Bank Assets 2010);

- Available Ministry of Finance resources and the financial position of the applicant;

- Compliance with NAMA Act obligations, which included but what were not limited to:

- Including all of its subsidiaries in its application to the Minister for Finance;

- Providing any “information, explanation, books, documents and records that the Minister” required;

- Certifying in “utmost good faith […] all matters and circumstances […] that might materially affect […] the Minister’s decision” on an institution’s application; and

- Limiting a number of business actions (like dealing with eligible assets outside the ordinary course of business) it could take without “prior written approval of NAMA” before NAMA acquired the eligible assets (National Asset Management Agency Act 2009, Revised 2018).

Although the initial proposals for an asset management company had recommended that the program be mandatory, the government opted for a voluntary approach (National Asset Management Agency Act 2009, Revised 2018). This was because the various recapitalization undertaken by the government had already resulted in significant public ownership of the Irish banking system. The government had stakes in ANGLO, AIB, and BOI at the time of NAMA’s establishment (Cerruti and Neyens 2016).

Ireland’s Financial Regulator and the Minister for Finance could require participants to produce any such report they considered necessary for monitoring compliance. After consultations with the Governor of the Central Bank and the Financial Regulator, the Minister for Finance could require participants to produce Restructuring Plans and/or business plans by a certain time. With approval from the Minister for Finance, the Financial Regulator could also issue directions to participants that would restrict balance sheet growth, the ability of participants to conduct mergers or acquisitions, or require balance sheet reduction, so long as the purpose of the direction was to achieve the purposes of the NAMA Act (National Asset Management Agency Act 2009, Revised 2018).

It is important to understand that the Irish government already had significant control over the country’s large banks by the time that NAMA began operating. The government had significant stakes in all of NAMA’s participants by the end of 2010 (See Figure 8) (Palcic and Reeves 2011).

Ireland’s Financial Regulator and the Minister for Finance could require participants to produce any such report they considered necessary for monitoring compliance. After consultations with the Governor of the Central Bank and the Financial Regulator, the Minister for Finance could require participants to produce Restructuring Plans and/or business plans by a certain time. With approval from the Minister for Finance, the Financial Regulator could also issue directions to participants that would restrict balance sheet growth, the ability of participants to conduct mergers or acquisitions, or require balance sheet reduction, so long as the purpose of the direction was to achieve the purposes of the NAMA Act (National Asset Management Agency Act 2009, Revised 2018).

It is important to understand that the Irish government already had significant control over the country’s large banks by the time that NAMA began operating. The government had significant stakes in all of NAMA’s participants by the end of 2010 (See Figure 8) (Palcic and Reeves 2011).

Eligible Assets

1

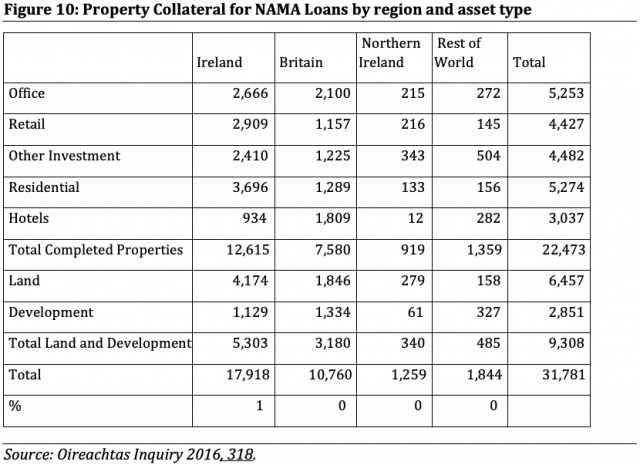

Any “bank asset” designated by the Minister for Finance was an eligible asset for purchase by NAMA. In the NAMA Act, the term could broadly include any “security related to a credit facility” as well as any credit facility. But the Minister for Finance ultimately defined eligible bank assets more narrowly as “all loans issued for the purchase, exploitation or development of land as well as loans either secured or guaranteed by land;” related commercial loans; and other financial contracts relating to acquired loans (Martin 2010; NAMA Acquisition of Bank Assets 2010; Oireachtas Inquiry 2016). NAMA had full discretion to decide which assets it would purchase from participating banks (Carroll and Dodd 2012; NAMA Annual Report 2018). For efficiency reasons, all transferred loans from AIB, Anglo Irish Bank, and Bank of Ireland had to be at least €5 million; NAMA’s Board later increased the figure to €20 million for assets held by AIB and Bank of Ireland (Oireachtas Inquiry 2016). The government expected eligible assets to be highly concentrated among a small number of large real estate developers (Martin 2010).

When NAMA acquired the loans, their breakdown by region and asset type was as follows:

Acquisition - Mechanics

1

Once the panel of loan-value experts arrived at a valuation, NAMA grouped the loans based on their shared relationships with a given borrower (rather than by bank) and sorted them into tranches for transfer. Each additional tranche contained a larger number of borrowers and smaller positions (the author of this piece hypothesizes that NAMA’s designers carved up the assets into tranches because they anticipated that the scale of documentation processing required to value all of the assets at once dramatically outstripped NAMA’s administrative capacity).FThe 2010-02-26 European Commission state aid decision said that “It is [was] anticipated that the first tranche will include the 10-15 largest borrower exposures across all participating institutions” (Martin 2010). NAMA determined a transfer schedule for each tranche and provided it to the relevant participants. The transfer schedule included the assets that NAMA would acquire from the relevant participant and the consideration price NAMA would pay, which would be “the lower of the amount owed by the borrower and the loan’s long-term economic value” (NAMA Acquisition of Bank Assets 2010).

NAMA’s original intention was to value and purchase the first tranche immediately, which would contain the largest exposures, and then do the same for a new tranche every 30 days until an expected completion date of June or July 2010 (Houses of the Oireachtas October 2009; Houses of the Oireachtas November 2009). However, these 30-day and mid-year goals proved overly optimistic. Although NAMA aimed to finish purchasing its assets by the end of 2010, NAMA ultimately had to revise this end date several times between 2009 and 2011 (NAMA Acquisition of Bank Assets 2010) because of issues in its participants that included multiple management information systems (MIS), poor data management infrastructure, paper records, “unreliable key performance metrics,” and “[p]oor data collection capacity” (Oireachtas Inquiry 2016).

On September 30, 2010, the Minister for Finance requested that NAMA finish transferring assets as soon as possible and announced that “all remaining NAMA transfers should be completed in one single tranche for each of the participating banks” (NAMA Acquisition of Bank Assets 2010). The Minister for Finance then issued a direction and two statutory instruments on October 22, 2010, which incorporated this goal into NAMA’s governing documents. The direction and one of these statutory instruments added an additional function (and processes for fulfilling said function) to NAMA: take “all necessary steps to acquire” eligible bank assets from participants” as expeditiously as possible” (National Asset Management Agency Act 2009, Revised 2018). The other statutory instrument amended the March 3, 2010, statutory instrument dealing with the calculation of the “Long-Term Economic Value of property and Bank Assets” (S.I. No. 504 2010). After consulting with NAMA’s Board and the EC, the Minister for Finance also requested that NAMA table its acquisition of loans from AIB and BOI where the borrower’s exposure was less than €20 million, shrinking the number of eligible assets that NAMA intended to acquire to around €73.4 billion (NAMA Acquisition of Bank Assets 2010). On November 28, 2010, however, Ireland’s Financial Regulator issued a statement reversing course: NAMA would now acquire all of AIB and BOI’s exposures (including those less than €5 million) (PCAR 2011). The Financial Regulator’s statement was codified in the National Asset Management Agency (Amendment) Bill 2011, but the Bill was never passed, and the reversal was never implemented (Carroll and Dodd 2012).

NAMA accordingly began an accelerated transfer of most of the assets in its remaining tranches (three through nine) between October and December 2010 (NAMA Annual Report 2011; NAMA Progress Report 2014). NAMA would use the new valuation process “for purposes of expedited acquisitions” to calculate the amount of consideration NAMA would give to participants during this accelerated transfer (S.I. No. 504 2010).FIn NAMA’s 2011 Annual Report, its CEO noted that “we had little information on the underlying collateral from the participating institutions” when they acquired the assets in tranches three through nine (See NAMA Annual Report 2011, 12). This leveraged sampling rather than loan-by-loan valuations (Honohan 2019). In the process, NAMA acquired these assets, it would conduct more detailed due diligence, produce a final long-term economic value for the assets, and revise its consideration cost accordingly (S.I. No. 504 2010).FAfter adjustments, NAMA realized its final valuation was around €0.5 billion more than its provisional valuation and paid the banks the difference (See NAMA Progress Report 2014). NAMA would not finish purchasing the remaining €3.4 billion in assets and conducting due diligence on assets purchased after the fourth tranche until March 2012 (European Commission 2014). By that point, NAMA had purchased a total of €74.4 billion in assets for €31.7 billion, leaving the participants with an average haircut of 57% (Oireachtas Inquiry 2016). The EC officially approved these transfers on July 29, 2014 (European Commission 2014).

Acquisition - Pricing

2

NAMA’s valuation procedures were intended to clarify the value of its assets while limiting the damage that the resulting haircuts would impose on its participants by paying the long term economic value for the assets (which would be higher than the current market value) (Carroll and Dodd 2012). The Irish government began collecting information for due diligence and constructing valuation processes by May 2009, months before the NAMA Act passed or NAMA was formally established (NAMA Acquisition of Bank Assets 2010). The NAMA Act allowed for NAMA to purchase assets at the current market value or at any price between the current market value and the long-term economic value so long as NAMA consulted with the Minister for Finance. However, all of NAMA’s valuations and acquisitions ultimately took place at long-term economic value. NAMA defined long-term economic value for asset as “the value, as determined by NAMA, that it can reasonably be expected to attain in a stable financial system when the crisis conditions prevailing at the passing of the Act are ameliorated.”FThe term asset, rather than loan, is sometimes used because NAMA also acquired some derivatives. It defined long-term economic value for property as “the value, as determined by NAMA, that it can reasonably be expected to attain in a stable financial system when the crisis conditions prevailing at the passing of the Act are ameliorated and in which a future price or yield of the property is consistent with the reasonable expectation having regard to the long-term historical average.” NAMA defined the “long-term” as between January 1, 1985 and December 31, 2005, indicating that NAMA placed the Irish property market as only having been overvalued starting January 1, 2006 (Carroll and Dodd 2012). NAMA constructed the long-term economic value by observing the current market value of the asset and the assets’ collateral as of November 30, 2009 (rather than the current market value at the time of the purchase), applying an uplift factor based on the projected increase in the collateral’s value and a discount based on “the extent to which a participating bank has secured its legal right to realise the underlying security” to a discounted cash flow (DCF) valuation methodology approved by the EC (NAMA Acquisition of Bank Assets 2010).FThe EC did not specifically require the use of DCF. The 2009 IAC instead merely stated that “the Commission would consider a transfer value reflecting the underlying long-term economic value of the assets on the basis of underlying cash flows and broader time horizons as an acceptable benchmark indicating compatibility of the aid amount as the minimum necessary” (See Martin 2010). Additionally, the EC noted that NAMA’s DCF approach and the calculation of long-term economic value was appropriate “to the extent that the discount rate and in particular the margin added to the risk-free rate is viewed as adequate” (Martin 2010).

The actual valuation process, which took place loan-by-loan until the Irish government received permission from the EC to simplify it in mid to late 2010, was arduous (Honohan 2019, 219). This was because the EC worried NAMA would be used to provide illegal state aid to Irish banks (i.e. that NAMA would inflate valuations to the point where NAMA’s purchases worked like a stealth recapitalization) (Honohan 2019).

NAMA’s creators integrated a valuation clawback provision (which the 2009 IAC mentioned as a potential tactic) (Communication from the Commission 2009) into the organization. If NAMA determined that it overpaid for an asset, NAMA could claw back the amount that it overpaid from the participants. The NAMA Act also provided for participants to claw back value from NAMA in cases of underpayment through a “Valuation Panel” procedure, but it is not clear whether these reverse clawbacks were widely used (Martin 2010; National Asset Management Agency Act 2009, Revised 2018). NAMA would determine that it overpaid by way of:

- EC decisions on proper loan valuation procedures;

- due diligence conducted after the expedited valuation and purchase of an asset;

- realization that it had made a mistake in applying its valuation procedures; or

the rectification of incorrect (or incomplete) information that NAMA received while initially valuing the assets (Carroll and Dodd 2012).

Management and Disposal

1

Once NAMA had acquired an asset, it effectively took the position of the participating institution who had originally held the assets. NAMA used this legal leverage (the ability to “take enforcement against borrowers in default”) to motivate borrowers to submit business plans to NAMA (Carroll and Dodd 2012). However, NAMA itself did not take direct ownership of much property (NAMA Management of Loans 2012). NAMA only directly owned €6 million worth of property and had not directly sold any of this type of property by the end of 2011.

If the borrower in question was a major borrower (as defined by NAMA), they submitted a “realistic business plan which set out their current assets and liabilities” to NAMA within three months of joining the scheme. Upon analyzing the business plan, NAMA then proposed (and negotiated) short term and long term repayment strategies with the borrower (Martin 2010; Williams 2014). NAMA ultimately developed five types of strategies:

- Full Restructuring: Borrower goes through a full refinancing with new terms and conditions.

- Partial Restructuring: Nearly the same as “Full Restructuring” but “did not result in new loan agreements.” Instead, they set down the terms for borrower compliance in “Connection management agreements (CMAs).”

- Support: Borrower received financial support from NAMA on the condition that it “implement a number of milestones in relation to debt reduction.”

- Consensual Disposal: Large scale asset sale by the borrower over a “relatively short-term horizon.”

- Enforcement: Although this was only deployed when the debtor was not cooperative or the debtor could not demonstrate viability, this strategy involved NAMA enforcing the debts using whatever legal powers it had at its disposal (NAMA Second Progress Report 2018).

If NAMA and the borrower could agree on a strategy, NAMA and the borrower collaborated on making the arrangement feasible, potentially involving, but not limited to, debt restructurings and write-offs that the borrower would present to NAMA in a “request for support.” If these negotiations failed (or if collaboration failed to make the agreement feasible), NAMA asked for full repayment from the borrower, threatening enforcement proceedings (Williams 2014).

If the borrower in question was not a major borrower, the participants would provide asset management services, but the credit decisions were made by NAMA and NAMA was represented in each of the banking units (Williams 2014). These borrowers would have the relevant participant submit information on their financial performance to NAMA. Then, NAMA would sort borrowers based on the “level of their exposure, […] creditworthiness and […] level of impairment,” and prioritize the larger and more impaired borrowers for assessment under the procedure for major borrowers “as a matter of urgency” (NAMA Business Plan 2009). During YPFS discussions with NAMA staff, they expressed a sentiment that, if they were to run NAMA again, they would leave less asset management responsibilities with participating institutions or work with other firms to provide those services (Susan McDermott and Jamie Bourke of NAMA, Zoom discussion with author, February 26, 2021). That being said, they noted that such a strategy might not have been viable in 2009 and 2010, as there were not as many credit and tax firms to provide such services in Ireland.

During NAMA’s 2011 due diligence and business plan assessment process, NAMA appeared to change its procedure for assessing the business plans of debtors managed by NAMA’s participants. Instead of only analyzing business plans at the debtor level, NAMA began to accept business plans at the “debtor connection, debtor or loan level depending on the individual characteristics of each case.” NAMA also changed this procedure by adopting a system, which NAMA called a “credit grading matrix,” for grading debtors on a combination of debtor performance and expectations of debtor recovery, although NAMA would not fully implement the system until 2012 (NAMA Annual Report 2012; NAMA Annual Report 2011).

On November 25, 2010, in line with NAMA’s attempt to expedite its asset purchases during late 2010, NAMA put forward a more “streamlined” version of its “Debtor Business Plan Requirements,” which replaced the original business plan for most debtors. The original, which NAMA described as requiring “detailed and comprehensive information,” was ultimately only used for “major debtors with complex corporate structures and whose loans transferred as part of the first three tranches” (NAMA Annual Report 2010; Debtor Business Plan Version 2 2010).

Ultimately, NAMA seemed to have a preference for disposing of its assets by sale “on the open market by private treaty, public auction, public tender and sealed bid” (private treaty is essentially the same as a private contract) (EBS 2017; Cas and Peresa 2016). NAMA frequently chose to package large numbers of related loans (typically after improving the underlying collateral) and selling them to large institutional investors (Cas and Peresa 2016).

Another feature of NAMA’s disposal strategy was how NAMA dealt with the potential conflict between NAMA’s purpose and NAMA’s functions (as outlined in the NAMA Act). While NAMA’s functions gave the organization a commercial primary mandate (to realize the best value for the assets), the purposes of the NAMA Act 2009 encompassed the stabilization of the banking system, improving liquidity, and contributing to social and economic development (National Asset Management Agency Act 2009, Revised 2018). In practice, this meant that NAMA would focus on its primary mandate. However, NAMA did conduct numerous operations related to social and economic development. This included a rent abatement program for tenants of NAMA borrowers and the demolition of “unfinished housing estates” (more popularly known as “ghost estates”). In response to the tight credit markets of 2012, NAMA created a vendor finance program for properties held by NAMA borrowers and receivers in Ireland and the UK. NAMA committed up to €2 billion over four years for the program in May 2012, which would fund up to 75% of the purchase of properties by making medium term loans to new investors (NAMA Second Progress Report 2018; Vendor Finance 2014). However, NAMA only provided €384 million under the facility by the end of 2016 (NAMA Second Progress Report 2018). NAMA looked to “Ireland’s exit from the Troika programme [the IMF program it entered in the last quarter of 2010], the recovery in the Irish economy in recent years, increased investment in Ireland by international investors and the wider availability of capital provided by international and debt providers,” as well as “the introduction of Irish REITs as an alternative investment mechanism” as an explanation of the limited demand for the program (Vendor Finance 2014).

In 2012, NAMA also introduced the Deferred Payment Initiative for residential property purchases (NAMA Second Progress Report 2018; NAMA Deferred Payment Initiative 2014). In the program, buyers would pay 80% of the price upfront and would pay no additional amount if “after five years, the value of the house has fallen by 20% or more relative to its original purchase price” (NAMA Deferred Payment Initiative 2014; NAMA Second Progress Report 2018). In cases where, after five years, “the value of the house has fallen by less than 20% or has increased, the amount ultimately payable will be the lesser of the value of the house or the original purchase price” (NAMA Deferred Payment Initiative 2014). The program stopped accepting participants in May 2014, having only assisted in the purchase of 103 properties (NAMA Second Progress Report 2018).

Timeframe

1

Once a loan moved onto NAMA’s balance sheet, NAMA began managing it and preparing for its exit. NAMA anticipated that it would conduct 7-10 years of asset management and then terminate itself. NAMA was not created with a sunset date; NAMA was to continue operating until its Board decided the organization should be wound down (Carroll and Dodd 2012). NAMA intended to recover about half of its investment through “partial or full restructurings, including by supporting debtors” and the “other half [of its investment] by disposals (consensual and enforced)” (Cas and Peresa 2016).

The EC broadly praised NAMA, stating that “By using a centralised asset protection scheme, banks effectively reduced the burden of legacy assets and strengthened their deleveraging and recapitalisation process.” It continued on to say that NAMA’s assets were “clearly defined, limited in size and relatively easy to sell,” which helped NAMA manage and dispose of its assets (European Commission 2015). Additionally, the European Commission noted that NAMA’s profitability also benefitted “from having part of its asset portfolio located in the UK and especially London, as this allowed for significant sales before 2013 as property prices in the UK market started recovering earlier (around 2010) (See Figure 11). NAMA then was able to add value to its properties and benefit from the Irish property market’s recovery beginning in 2013 (Cas and Peresa 2016).

Charles Enoch of the IMF lamented the impact of a “lack of a universally accepted methodology for the valuation of assets,” which he said, “led to a protracted process whereby bank book values were repeatedly discounted, prolonging uncertainty, delaying normalization of bank funding, and undermining the credibility of the process” (Enoch 2013).

A review of three GFC-era asset management companies (AMCs) by the EC billed NAMA as a success story. It pointed out NAMA as having been “the most advanced of the three” AMCs when it came to asset sales, but argued that this was related to NAMA’s macroeconomic situation and the fact that NAMA’s assets were homogeneous, yet spread across multiple real estate markets. The review also commended NAMA for its tendency to sell its loans as “large packages to institutional investors,” describing it as a tactic that helped NAMA enhance the value of its assets. The paper continues, writing that NAMA’s expansive legal powers improved its ability to conduct speedy asset disposals and “ensure income generation from rentals.” With the ability to accelerate disposals of its impaired assets, NAMA was able to help “develop a functioning secondary market for distressed assets by sending a price signal.” However, it also noted that NAMA may have been less successful if it “had acquired Irish residential mortgage loans” and NAMA’s practice of “adding value” to its assets could distort the commercial property market (Cas and Peresa 2016). A World Bank study asserts that NAMA’s success was underpinned by its homogenous asset mix; NAMA’s acquisition of residential mortgage loans would make the AMC’s portfolio less homogenous. The same study also partially attributes Spain’s AMC’s issues offloading its real estate assets to the organization’s holding a mix of small residential and large commercial assets. Acquiring residential mortgage loans would mimic this less desirable mix.

As for the issue of NAMA’s value-addition activities potentially distorting the “ordinary functioning of the commercial property market,” this mostly pertained to NAMA’s work pursuing new development projects (Cas and Peresa 2016). NAMA’s size alone also did give it influence over some of the commercial property markets in which it was involved (BBC 2011).

Additionally, it asserted that NAMA’s practice of “Combining original goals with additional socio-economic activities” could deter NAMA from its “primary mandate” as well as contribute to “conflicting objectives.” Perhaps most importantly, the paper noted that NAMA had to be accompanied by other initiatives to repair the financial sector. It went on to say that post-crisis regulatory changes would render the lessons to be learned from NAMA less relevant in future. As for the first point, NAMA’s actions were not able to prevent Ireland from continuing to suffer a “very high NPL ratio” and “subdued […] lending to the private sector” (Cas and Peresa 2016). NAMA’s own annual report from 2010 buttresses this point:

For a period, it perhaps had been reasonable to anticipate that NAMA on its own could have fixed the banking system, if the problem had been confined to the loan categories designated for NAMA. However, the sheer scale of the banks’ problems, which went far beyond the land and development and associated loans within NAMA’s mandate and which only emerged after NAMA’s work had begun, meant that [the] initial expectation was not realizable. (NAMA Annual Report 2010)

As for the second point, due to changes in the Eurostat rules, majority privately owned AMCs like NAMA are now formally included on the government balance sheet, thus making them difficult to implement when governments are financially constrained (Cas and Peresa 2016). However, credit rating agencies considered NAMA debt to be on the government balance sheet even during the organization’s early days anyways, which shows the limits of the strategy even before it was reined in by Eurostat (European Commission 2019a; Cullinan and Beers 2010).

The point of view of two analysts from the German Federal Statistical Office was that the “initial impact of its [NAMA’s] operations on general government’s deficit and debt” was effectively nil. This made NAMA “more advantageous […] in comparison to the German liquidation sub-agencies.” However they also believed this advantage would be “to a large extent reduced by later government payments” that happened when the Irish government had to inject capital into a number of the participating banks to keep them in compliance with “international equity standards” once the participating banks recognized NAMA’s haircuts on their balance sheets (Braakman and Forster 2011).

A 2015 paper from Professor Dirk Schoenmaker of Erasmus University Rotterdam also praised NAMA, writing that it “serves as an international example of successful management of bad assets” (Schoenmaker 2015). In stark contrast to a World Bank study authored by Caroline Cerruti and Ruth Neyens, Schoenmaker argued that NAMA’s decision to purchase assets at November 30, 2009, values was a prudent one.FThat being said, a 2013 debate in the Oireachtas suggests that NAMA maintained the November 30, 2009 reference date due to the “regimental” requirements of calculating EU state aid (McDonagh 2013a). He accepts NAMA’s view that the purchase date “protected the banks from any further deterioration of the Irish property market” that would’ve come as a result of the 25-30 percent decline in property values after November 30, 2009. However, he also lamented that the government did not implement a proposal to have NAMA acquire “smaller commercial real estate loans,” popularly known as “NAMA II.” Schoenmaker also stated that external asset management may have helped resolve Ireland’s stock of non-performing mortgages faster, “but the ECB made such schemes financially unattractive as it limited ECB funding to banks only, excluding resolution vehicles” like NAMA (Cerruti and Neyens 2016; Schoenmaker 2015).

A World Bank study authored by Caroline Cerruti and Ruth Neyens gave NAMA a mixed review (Cerruti and Neyens 2016). They praised NAMA’s asset management structure as “offering the benefits of creating economies of scale in administering workouts, expediting loan resolution with specific expertise, and breaking “crony capitalist” connections between banks and developers.” They noted that NAMA’s clear commercial mandate, transparency and independence, “efficiency in managing the assets,” and good property mix allowed for NAMA’s “strong performance,” but did not substantially focus on NAMA’s other mandates (such as its ability to promote social and economic development). They also complimented NAMA for following through on “two key principles […]: no fire sales and no hoarding,” and for professionalizing the Irish real estate market through its loan packaging program. However, they also argued that the uplift NAMA applied to assets when calculating their long-term economic value (ultimately an average of 8.3%) and the choice to value the assets as of November 30, 2009, caused NAMA to overpay for its assets (because property prices continued to fall after November 30, 2009). They note several other areas where NAMA could have improved. Specifically, they attribute NAMA’s loss of “critical staff” to NAMA’s failure to maintain its program of linking bonuses with performance. Similar to Schoenmaker, they also lament that NAMA’s lack of purview over non-land and non-development loans kept it from fully cleaning up the Irish banking system, but they do not go as far as to say that NAMA should have been involved with these other loans.

This perspective, in which NAMA was an effective program, but by no means a panacea for Ireland’s problems, is similarly reflected by the Deputy Governor of the Central Bank of Ireland in a September 22, 2017, speech (Sibley 2017). He stated that NAMA was part of the solution, but “was by no means the silver bullet some people may think for resolving Irish NPLs overall, as SME and mortgage loans remained a serious and growing problem.” As evidence, he pointed to the fact that NPLs “only peaked in Ireland in Q4 2013, with an NPL ratio of 31.8%, more than two years after loans were transferred to NAMA.” Patrick Honohan, the former head of Ireland’s central bank, also saw NAMA as an organization that could not have been expected to solve Ireland’s economic woes on its own. Even if NAMA (and/or the Irish government) had overcapitalized the banks and shrunk the haircuts that the AMC would apply, Honohan argued that “to have done so would simply have brought forward the melt-down that happened in the autumn” of 2010 (Honohan 2019). His belief was that the Irish government simply did not have the fiscal capacity to handle the problem at the point without official-sector support from abroad.

The government’s 2016 Report of the Joint Committee of Inquiry into the Banking Crisis (the Report) provided the opinions of NAMA’s external auditor, the Comptroller & Auditor General (C&AG). The C&AG argued that NAMA chose a poor way to operationalize its mandate to seek “the best achievable financial return,” deciding to measure it through NAMA’s ability to redeem debt instead of some kind of “expected or target rate of return”. The C&AG also criticized NAMA for its failure to realize its anticipated rental income in 2011 (Oireachtas Inquiry 2016). The C&AG noted that NAMA’s asset purchases “removed a considerable element of the prevailing uncertainty about the credit institutions’ financial position in the aftermath of the banking crisis” (Oireachtas Inquiry 2015).

The 2016 Report itself criticized the government for the one-year lag between NAMA’s 2009 announcement and NAMA’s first transfers, saying that the lag caused “considerable uncertainty and difficulty for some developers, as they were caught in a ‘no man’s land’ between their financial institutions and a NAMA not yet formally established.” It went on to note that NAMA had negative effects on a number of the property developers who were “borrowers” in the program. Although the report conceded that NAMA’s practice of acquiring good assets in addition to bad assets from the participants allowed NAMA “to get more value from individual borrowers,” it damaged the reputation of at least one borrower of a participating institution in the process (Oireachtas Inquiry 2016).