Account Guarantee Programs

United States: Transaction Account Guarantee Program

Purpose

To “strengthen confidence and encourage liquidity in the banking system” (FDIC 2008h)

Key Terms

-

Launch DatesAnnouncement: Oct. 14, 2008; Authorization: Oct. 13, 2008; Operation: Oct. 14, 2008;

-

End DateOriginally Dec. 31, 2009; later extended to Dec. 31, 2010, with a replacement guarantee provided by Dodd-Frank extending to Dec. 31, 2012

-

Eligible InstitutionsAll FDIC-insured institutions automatically enrolled

-

Eligible AccountsOriginally, NIBTAs. Later extended to NOWs and IOLTAs

-

FeesOriginally, a flat annualized rate of 10 bps on quarter-end balances of eligible deposits over $250,000; later a risk-based annualized rate of 15 bps to 25 bps on quarter-end balances of eligible deposits over $250,000

-

Size of GuaranteeUnlimited

-

CoverageAt its peak, more than $834 billion in deposits

-

Outcomes$1.5 billion in losses on bank failures as of Dec. 31, 2018; $1.2 billion in fees collected

-

Notable FeaturesAutomatic enrollment with nonreversible opt-out: All FDIC-insured institutions were automatically enrolled with the nonreversible option to opt out of the TAGP; Change in fee structure: Originally, the FDIC charged a flat-rate fee, but it later moved to a risk-based fee, both to phase the program out and to cover losses associated with the program

The collapse of Lehman Brothers in September 2008 led many uninsured depositors to withdraw their funds from US banks that they perceived as troubled. To reassure depositors, the Federal Deposit Insurance Corporation (FDIC), on October 14, 2008, guaranteed certain debt and deposits through its Temporary Liquidity Guarantee Program (TLGP). The Temporary Account Guarantee Program (TAGP) was one component of the TLGP. Through the TAGP, the FDIC provided unlimited insurance to noninterest-bearing transaction accounts (NIBTAs) and other low-interest-bearing accounts. On October 3, 2008, the US Congress had increased the limit on insured deposits to $250,000. By guaranteeing these accounts in full, the FDIC hoped to calm depositors and forestall potential bank runs. All FDIC-insured institutions were automatically enrolled in the TAGP, free of charge, with the option to opt out after 30 days. After 30 days, banks were charged a flat-rate fee to stay in the program. Eighty-six percent of banks remained in the TAGP after 30 days. The FDIC extended the TAGP twice through December 31, 2010. The Dodd-Frank Act replaced the TAGP with a similar program that expired on December 31, 2012, which the FDIC administered. Through 2010, the TAGP collected $1.2 billion in fees. The FDIC absorbed $1.5 billion in losses from the failure of banks covered by the TAGP.

In the wake of Lehman Brothers’s bankruptcy on September 15, 2008, uncertainty about the value of mortgage-backed assets and the consequences for financial institutions’ balance sheets led to significant deposit withdrawals, even from healthy banks, and runs on short-term funding markets (Krimminger 2018). The government response had three main components. The Treasury Department injected capital into ailing banks, the Federal Reserve indirectly purchased commercial paper through an off-balance sheet legal entity, and the Federal Deposit Insurance Corporation (FDIC) guaranteed bank debt and deposits through its Temporary Liquidity Guarantee Program (TLGP) (FDIC 2017). For the FDIC to set up the TLGP under the laws in force at the time, the Treasury Secretary had to determine there was a systemic risk, with the concurrence of the FDIC Board, the Federal Reserve Board, and the President (FDICIA 1991, Article 141[g(i)]).

The TLGP was composed of the Debt Guarantee Program (DGP), which guaranteed banks’ unsecured debt, and the Transaction Account Guarantee Program (TAGP) (FDIC 2019; Katz 2020). The TAGP, which is the focus of this case study, was meant to reestablish confidence in banks and prevent bank runs (FDIC 2019). To do so, the TAGP guaranteed in full all noninterest-bearing transaction accounts (NIBTAs). The US Congress, on October 3, 2008, had increased the limit on insured deposits to $250,000 (EESA 2008, Article 136[a(1)]). The FDIC noted that these accounts were mainly used by businesses in payment processing (FDIC 2008h; FDIC 2017). Because these accounts were often over the $250,000 cap, bankers and the FDIC worried they were susceptible to runs (FDIC 2008h; FDIC 2017). The FDIC later expanded the coverage to low-interest negotiable order of withdrawal (NOW) accounts and Interest on Lawyers Trust Accounts (IOLTAs) (FDIC 2019).

For the TAGP, the FDIC guaranteed accounts using fees collected from participating institutions, rather than from its existing Deposit Insurance Fund (DIF) (FDIC 2008a; FDIC 2008e). If the fees were unable to cover bank defaults, the FDIC planned to levy a special assessment fee on the banking industry to cover the difference (FDIC 2008d).

On October 14, 2008, all FDIC-insured banks were automatically enrolled in the TAGP for 30 days, free of charge (FDIC 2008a). To remain in the program after the TAGP’s first 30 days, banks were required to pay quarterly an annualized fee of 10 basis points on deposits exceeding $250,000 (FDIC 2009b). The FDIC later increased the fees and put in place a risk-based fee system fee, partly to limit losses associated with the program (FDIC 2009b). Banks could opt out of the program if they wished (FDIC 2008a). However, all decisions to opt out were final (Krimminger 2020).FThe FDIC made one exemption to this rule. In the case of a merger of two eligible entities, the post-merger institution had a “a one-time option to revoke a prior decision to opt-out” (FDIC 2010a). Moreover, all banks were required to disclose to their customers whether they were participating in the TAGP (FDIC 2010a). After the first 30 days, more than 7,100 banks and thrifts, equivalent to 86% of eligible institutions, remained in the TAGP (Davison 2019). Over time, some of these institutions opted out of the TAGP (Shapiro and Dowson 2012).

The FDIC gave the TAGP a deadline of December 31, 2009 (FDIC 2019). However, policymakers extended the TAGP twice—in August 2009 and again in April 2010—because they feared that eliminating the TAGP would disrupt the banking system (FDIC 2009a; FDIC 2010c; Davison 2019). The TAGP expired on December 31, 2010 (FDIC 2019). After the TAGP expired, the Dodd-Frank Act replaced it with unlimited deposit insurance on NIBTAs and IOLTAs, but not NOWs, representing $1.4 trillion in NIBTAs above the basic coverage limit of $250,000 per account (FDIC 2019; Dodd-Frank Act 2010; FDIC 2010d; FDIC 2015; FDIC 2012). The FDIC administered this coverage, which was “separate from, and in addition to, the insurance coverage provided for a depositor’s other accounts held at an FDIC-insured bank” (FDIC 2011). Under the Dodd-Frank Act, the FDIC used its existing DIF to back the unlimited guarantee after the TAGP expired (FDIC 2011). Those protections expired on December 31, 2012 (FDIC 2019; FDIC 2010d; Dodd-Frank Act 2010).

At its peak, the TAGP covered over $834 billion in deposits (Davison 2019; Cave 2011). During its time of operation, the TAGP collected $1.2 billion in fees (FDIC 2019). At year-end 2012, the FDIC estimated $2.1 billion in losses because of bank failures the guarantee covered (FDIC 2019). Through further collections on its receiverships, though, the FDIC’s cumulative losses on the program declined to $1.5 billion by year-end 2017 (FDIC 2019). In contrast, the DGP ran a surplus. Combining the two programs, the TLGP overall recorded a net $9.3 billion surplus (FDIC 2019).

According to the Government Accountability Office (GAO), banks, especially small banks, indicated that the TAGP had been “helpful in stemming [deposit] outflows” (GAO 2010). Some academics and the FDIC said that the TAGP increased the flow of deposits into NIBTAs, given that these accounts were viewed as insured, safe accounts (Shapiro and Dowson 2012; FDIC 2017). In the FDIC’s view, the program provided banks with an additional source of funding and stabilized deposit funding (FDIC 2017). The TAGP also helped reduce the FDIC’s administrative costs in resolving banks, as the broad insurance coverage meant it did not have to identify which deposits were insured and which were not (FDIC 2017).

Architects of the TAGP credited its success to the program’s design and communication. They said that the TAGP received less criticism than other programs because the TAGP simply expanded depositor protections (Krimminger 2020). They argued that these protections were both widely understood and popular, and that the program’s costs were clearly denoted and equitably priced (Krimminger 2020). The program’s architects also argued that it had credibility because the public thought the FDIC was apolitical (Krimminger 2020).

Perhaps the greatest criticism of the TLGP was that the FDIC did not have the legal authority to establish it (Krimminger 2020; Davison 2019). The laws in place at the time required the FDIC to resolve failed banks using the method that it believed would result in the least cost to taxpayers, unless it identified an overriding systemic risk (FDICIA 1991, Article 141[g(i)]). To establish the TLGP, the FDIC got a determination from the Treasury Secretary that there was a systemic risk, with the concurrence of the FDIC Board, the Federal Reserve Board, and the president (FDICIA 1991, Article 141[g(i)]). However, it was not clear whether this systemic risk exception could be applied to the financial system as a whole, as opposed to a single failing bank (USC 2006, Article 4[a]; Krimminger 2020). The GAO in 2010 found that “there is some support for the agencies’ position,” but wrote that “the statutory requirements may require clarification” (GAO 2010). The Dodd-Frank Act, passed in 2010, prohibited the FDIC from creating a future TAGP and created restrictions on the creation of a future DGP (Davison 2019). During the COVID-19 pandemic, Congress temporarily restored the FDIC’s power to institute a program like the TAGP, although the FDIC did not do so (McNamara 2020; CARES Act 2020).

According to the GAO, the TAGP raised moral hazard concerns (GAO 2010). By providing unlimited insurance on NIBTAs, critics held, the TAGP “weaken[ed] incentives for newly protected, larger depositors to monitor their banks, and in turn banks [could] engage in riskier activities” (GAO 2010). The International Association of Deposit Insurers (IADI) further echoed this concern in their examination of deposit insurance, writing that poorly designed deposit insurance could “lead to greater risk-taking by banks than might otherwise be the case” (IADI 2014). This led some to argue that the TAGP’s unlimited guarantees ultimately constituted a “threat to the nation’s long-term financial stability” (Shapiro and Dowson 2012) and increased the likelihood of future banking crises (Demirgüç-Kunt and Detragiache 2002).

Banks themselves expressed concerns about the TAGP’s design. Opt-outs from the TAGP were final (FDIC 2010b). This program design choice led to criticism, as some institutions that had opted out wished to rejoin the program (FDIC 2010b). Originally, commentators noted that these institutions opted out under the assumption that the TAGP was temporary (FDIC 2010b). However, these institutions later sought to rejoin the program because they feared that institutions that remained in the program would have a competitive advantage (FDIC 2010b). In response to these concerns, the FDIC responded that allowing institutions to opt back into the program would have been “inconsistent” with the program’s goals (FDIC 2010b). The FDIC also added that only three institutions had expressed a desire to rejoin the program, that reinstatement would be costly, and that the potential confusion of such a decision counted against permitting reinstatements (FDIC 2010b).

Key Design Decisions

Purpose

1

Following the collapse of Lehman Brothers, economic conditions deteriorated, with even healthy banks facing significant depositor withdrawals (Krimminger 2018). Given these conditions, the government created the TAGP to reestablish confidence in banks and prevent bank runs by guaranteeing NIBTAs, IOLTAs, and NOWs (FDIC 2019). The FDIC sought to insure these accounts in full as these accounts were used in businesses payment processing, were often over the $250,000 limit, and were susceptible to runs (FDIC 2008h; FDIC 2017).

The FDIC also wanted to avoid a disadvantage for American banks that competed with banks in European and Asian countries that had already introduced similar guarantees (FDIC 2008a).

Part of a Package

1

On October 3, 2008, the US Congress had increased the limit on insured deposits to $250,000 (EESA 2008, Article 136[a(1)]). On October 14, 2008, the FDIC announced the TLGP, with the DGP guaranteeing bank debt and the TAGP insuring certain deposit accounts.

The Treasury and Federal Reserve announced other financial programs at the same press conference as the FDIC’s TLGP announcement on October 14, 2008. The Treasury announced the Capital Purchase Program (CPP), which provided eligible institutions with capital (US Treasury n.d.; Lawson and Kulam 2021). The Federal Reserve Board announced the Commercial Paper Funding Facility (CPFF), which sought to improve market liquidity by purchasing commercial paper from issuers (Federal Reserve n.d.; Wiggins 2020).

Legal Authority

1

The TAGP and DGP were established pursuant to the Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA) (FDICIA 1991, Article 141[g(i)]). Policymakers used FDICIA’s “systemic risk exception,” which allowed the FDIC to adopt an approach to resolving a bank that was not “the least cost[ly]” to taxpayers but “avoid[ed] or mitigate[d the] adverse effects” of the least costly resolution method (USC 2006, article 4[a(i)]). The systemic risk exception was invoked upon a determination by the secretary of Treasury, in consultation with the president, the FDIC’s board of directors, and the Federal Reserve Board of Governors (FDIC 2008e; USC 2006, article 4[g(i)]). Unless the systemic risk exception was invoked, the FDIC was required to aid troubled institutions in a way that minimized costs to the DIF.

The use of the systemic risk exception prompted legal questions. Among these, it was an open legal question as to whether the exception could be applied to the financial system as a whole, as opposed to a single bank (USC 2006; Krimminger 2020). The GAO in 2010 found that “there is some support for the agencies’ position,” but wrote that “the statutory requirements may require clarification” (GAO 2010). The Dodd-Frank Act passed by Congress in 2010 prohibited the FDIC from creating a future TAGP (Davison 2019) and created restrictions on a future DGP. During the COVID-19 pandemic, Congress temporarily restored the FDIC’s power to institute a program like the TAGP (McNamara 2020; CARES Act 2020).

Administration

1

The FDIC directly oversaw the TAGP because the program extended its function in insuring deposits (FDIC 2019).

To enroll in the TAGP, institutions needed to provide the FDIC with information about eligible accounts—that is, the amount of existing deposits that exceeded $250,000 in TAGP-eligible accounts (FDIC 2008c; FDIC 2008f). The FDIC used this information to determine the fees that an institution would pay to participate (FDIC 2009a). The FDIC also required all eligible institutions to disclose to customers whether they were participating in the TAGP, including through lobby notices and website notices (FDIC 2010a).

Governance

1

Since the TAGP was established using the systemic risk exception, the FDICIA required the GAO to review the FDIC’s determination (FDICIA 1991, article 141[g(iv)]; GAO 2010). The GAO ultimately recommended that Congress consider regulatory reform and changes to the FDICIA to ensure adequate oversight and market discipline (GAO 2010). Under the Dodd-Frank Act, the FDIC continued to provide unlimited insurance on NIBTAs and IOLTAs accounts, with minor changes (FDIC 2019; FDIC 2010d; FDIC 2015; Dodd-Frank Act 2010, Article 343).

Communication

1

On October 14, 2008, the FDIC announced the TAGP, which was part of the TLGP (FDIC 2019). Policymakers said they created the TLGP “to strengthen confidence and encourage liquidity in the banking system” (FDIC 2008h). Officials wanted the TAGP to address the lack of stability and confidence in banks—especially small banks—that could have faced runs (FDIC 2019; FDIC 2008a).

The FDIC also said that the TAGP was fully industry-funded and did not rely on its existing DIF (FDIC 2008a). Architects of the TAGP credited the program’s success to this factor, along with the FDIC’s reputation as an apolitical institution that had a long-standing reputation as an advocate for depositors, one which had long provided account guarantees and thereby did not gain a new function (Krimminger 2020).

Size of Guarantee

1

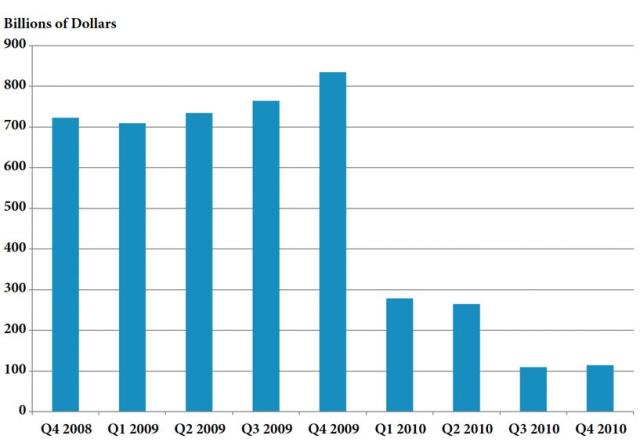

The TAGP covered all eligible accounts with an unlimited guarantee (FDIC 2019). At its peak, on December 31, 2009, the TAGP covered over $834 billion in deposits (Davison 2019; Cave 2011; CRS 2018). Figure 1 illustrates the total amounts that the TAGP guaranteed from 2008 to 2010. Usage declined significantly in 2010 when the FDIC raised its fees from a flat 10 basis points per quarter to a risk-based range of 15 to 25 basis points per quarter. Some large banks exited the TAGP due to these fees, but 93% of institutions enrolled at year-end 2009, or 6,400 institutions, remained enrolled in the TAGP through June 30, 2010 (FDIC 2017; Shapiro and Dowson 2012).

In the Dodd-Frank Act of 2010, Congress replaced the TAGP with unlimited deposit insurance on NIBTAs and IOLTAs (but not NOW accounts) from the end of 2010 to the end of 2012 (FDIC 2019; Dodd-Frank Act 2010; FDIC 2010d; FDIC 2015). The FDIC administered this program as well (FDIC 2011).

At the end of 2011, the FDIC guaranteed $1.4 trillion in NIBTAs above the basic coverage limit of $250,000 per account under the Dodd-Frank mandate, more than the TAGP had guaranteed in 2008 through 2010 (Figure 1) (FDIC 2012).

Figure 1: Amounts Guaranteed by the TAGP in USD, 2008–2010

Source: FDIC 2017.

Source: FDIC 2017.

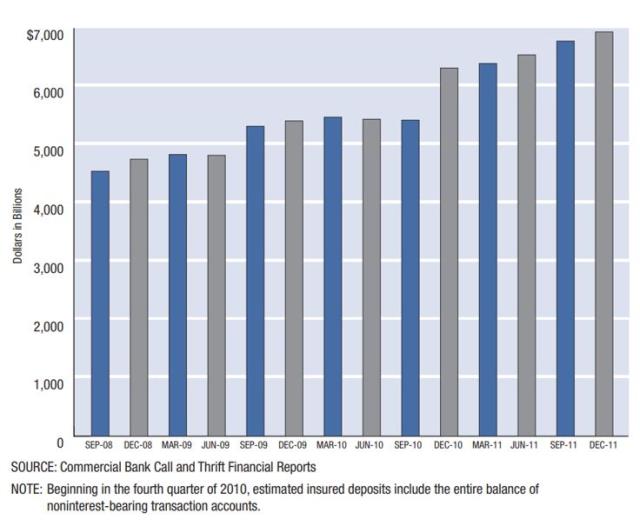

Figure 2 illustrates the impact of the TAGP, and later the Dodd-Frank Act, on DIF-insured deposits (FDIC 2012). Deposit accounts grew steadily from September 2008 to year-end 2011.

Figure 2: Estimated DIF-Insured Deposits

Source: FDIC 2012.

Source: FDIC 2012.

Source and Size of Funding

1

The FDIC funded the TAGP through the fees charged to banks that participated in the program (FDIC 2019; FDIC 2008a). These fees allowed the FDIC to fund the TAGP without using the DIF—the FDIC’s fund for insuring banks in non-crisis times—or taxpayer funds; instead, the TAGP relied on “direct user fees included as part of a bank's regular insurance premium” (FDIC 2008a). The TAGP collected $1.2 billion in fee revenue over 2009 and 2010 (FDIC 2019). Through its life, the TAGP ran a cumulative deficit of $300 million (FDIC 2019). To cover this shortfall, the FDIC utilized funds collected through the DGP (FDIC 2019). If the fees were unable to cover bank defaults, the FDIC planned to cover the difference with a special assessment fee—a fee charged to the banking industry to cover losses: in this case, those associated with the use of the systemic risk exemption (FDIC 2008d).

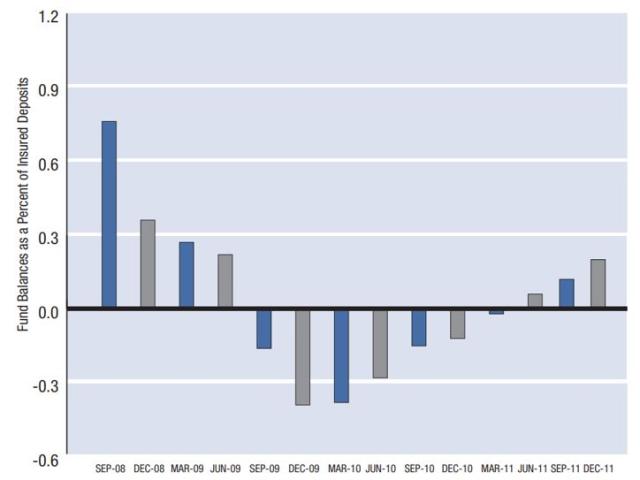

After the TAGP expired at the end of 2010, the Dodd-Frank Act replaced it with unlimited deposit insurance on NIBTAs and IOLTAs from the fourth quarter of 2010 until the end of 2012 (FDIC 2019; Dodd-Frank Act 2010; FDIC 2010d; FDIC 2015). The FDIC used its existing DIF to cover this commitment (FDIC 2011). However, the DIF was technically insolvent, with a negative balance for seven quarters from September 2009 to March 2011, after paying billions of dollars of depositors at failed banks during the GFC. The FDIC, in its 2011 annual report, set a goal of building the DIF to 1.35% of estimated insured deposits by 2020, as Congress had required in the Dodd-Frank Act (FDIC 2012). Its long-run goal for the ratio is 2%. Figure 3 illustrates the FDIC DIF reserve ratio.

Figure 3: DIF Reserve Ratios

Source: FDIC 2012.

Source: FDIC 2012.

Eligible Institutions

1

All FDIC-insured institutions were eligible for the TAGP (FDIC 2008a). On October 14, 2008, all FDIC-insured institutions were automatically enrolled in the TAGP (FDIC 2008a). These institutions could, after the first 30 days, opt out of the program (FDIC 2008a). All decisions to opt out of the TAGP were final (FDIC 2010a; Davison 2019; Krimminger 2020). The FDIC made one exemption to the finality of opting out. In the case of a merger of two eligible entities, the post-merger institution had a “a one-time option to revoke a prior decision to opt-out” (FDIC 2010a).

After the first 30 days, more than 7,100 banks and thrifts, equivalent to 86% of eligible institutions, remained in the TAGP (Davison 2019). At year-end 2008, the TAGP insured $684 billion (FDIC 2009c). By the first quarter of 2010, 80% of eligible institutions remained in the TAGP (Shapiro and Dowson 2012). By the program’s termination in 2010, 74% of eligible institutions remained enrolled in the program (Shapiro and Dowson 2012).

Some institutions criticized the rule that opt-out decisions were final (FDIC 2010b). A small number of institutions opted out under the assumption that the TAGP was temporary but later sought to rejoin the program, fearing that they were at a competitive disadvantage (FDIC 2010b). The FDIC responded that allowing institutions to opt back into the program would have been “inconsistent” with the program’s goals (FDIC 2010b). Moreover, the FDIC added that only three institutions had expressed a desire to rejoin the program, that the costs of implementing a reinstatement program would be high, and that the potential confusion of such a decision counted against permitting reinstatements (FDIC 2010b).

The FDIC required institutions to post notices about their participation in the TAGP (FDIC 2010a). Institution that opted out effective July 2010, for example, had to post the following notice: “Beginning July 1, 2010 [Institution Name] will no longer participate in the FDIC's Transaction Account Guarantee Program. Thus, after June 30, 2010, funds held in noninterest-bearing transaction accounts will no longer be guaranteed in full under the Transaction Account Guarantee Program but will be insured up to $250,000 under the FDIC's general deposit insurance rules” (FDIC 2010a).

Eligible Accounts

1

The TAGP was originally meant to cover NIBTAs, providing them with unlimited insurance beyond the $250,000 limit (FDIC 2008a). This was intended to calm depositors, eliminating the incentive to withdraw their money from otherwise safe banks, given that assets above $250,000 were not previously insured (FDIC 2008a; FDIC 2008h; FDIC 2017).

At its inception, the TAGP only covered NIBTAs, given that these accounts did not bear any interest (FDIC 2008g). In November 2008, upon receiving feedback from depositors and FDIC-insured institutions, the FDIC decided to extend the TAGP to cover NOW accounts that bore low interest rates and IOLTAs (FDIC 2019; FDIC 2008g; FDIC 2008i). Comments sent to the FDIC regarding NOWs and IOLTAs highlighted that the interest accrued from both were de minimis; further, regarding IOLTAs, several comments discussed how lawyers would be inclined to run from IOLTAs to NIBTAs because of the guarantee (FDIC 2008g).

The FDIC originally guaranteed NOW accounts where the participating institutions maintained an interest “rate no higher than 0.5 percent; this maximum was lowered to 0.25 percent as part of the second extension of the program” (FDIC 2017).

Fees

2

The TAGP began with a flat-rate fee of 10 basis points, which was charged to a bank’s end-of-quarter balances that exceeded $250,000 (FDIC 2008h; GAO 2010). Effective January 2, 2010, the FDIC increased these fees and moved to a risk-based rate in an effort to balance the losses associated with the TAGP (FDIC 2009b). These risk-based fees were 15, 20, or 25 basis points, depending on the FDIC’s determination of the risk of each participating institution (FDIC 2009a; GAO 2010). These determinations were made using the FDIC’s risk-based premium system, which considers a bank’s size, capital adequacy, asset quality, management, earnings, liquidity, and sensitivity (CAMELS) (FDIC 2009a; FDIC 2017).

FDIC officials stated that, if the fees from the TAGP were insufficient to cover guarantee-associated losses, they planned to impose a special assessment fee (FDIC 2008d). Such a fee would be levied on the banking industry to cover the difference (FDIC 2008d). Ultimately, no special assessment fee was imposed, as profits from the DGP covered the TAGP’s losses (FDIC 2019).

Process for Exercising Guarantee

1

In the case where a bank was to fail, the FDIC would act as the bank’s insurer and receiver (FDIC 2020). As the bank’s insurer, the FDIC would first pay depositors the amount of their insured account (FDIC 2020). The FDIC would also cover any interest that had accrued, through the date of default (FDIC 2020). As the bank’s receiver, the FDIC would then liquidate the failed bank’s assets, which would reimburse the TAGP (FDIC 2020). This exercise guarantee process was akin to that for non-crisis time (FDIC 2008g).

Other Restrictions

1

Participating institutions faced no conditions on executive compensation or dividends. The FDIC said it would seek, through its supervisory oversight, to “prevent rapid growth or excessive risk-taking” by participating institutions (FDIC 2008b).

Duration

1

Originally, the TAGP was meant to last just over a year, until December 31, 2009 (FDIC 2019). However, the TAGP was extended twice—in August 2009 and again in April 2010—due to fears that eliminating the TAGP would disrupt the banking system (FDIC 2009a; FDIC 2010c; Davison 2019). The TAGP was allowed to expire on December 31, 2010 (FDIC 2019).

The Dodd-Frank Act, though, required the FDIC to continue to provide unlimited insurance on NIBTAs and IOLTAs accounts, with minor changes (FDIC 2019; FDIC 2010d; Dodd-Frank Act 2010, Article 343; FDIC 2015). The FDIC administered this coverage, which was “separate from, and in addition to, the insurance coverage provided for a depositor’s other accounts held at an FDIC-insured bank” (FDIC 2011). These deposits, under the Dodd-Frank Act, were covered under the DIF (FDIC 2011). The protections provided under the Dodd-Frank Act extended until December 31, 2012 (FDIC 2019; FDIC 2010d; Dodd-Frank Act 2010).

Key Program Documents

-

(FDIC 2008a) Federal Deposit Insurance Corporation (FDIC). 2008a. “Statement by Federal Deposit Insurance Corporation Chairman Sheila Bair; U.S. Treasury, Federal Reserve, FDIC Joint Press Conference.” Press release, October 14, 2008.

Press release of statements by FDIC chairwoman Sheila Bair on the Temporary Liquidity Guarantee Program.

-

(FDIC 2008b) Federal Deposit Insurance Corporation (FDIC). 2008b. “Temporary Liquidity Guarantee Program: FDIC Announces Temporary Program to Encourage Liquidity and Confidence in the Banking System.” Financial Institution Letter 103-2008, October 15, 2008. Federal Deposit Insurance Corporation.

Document explaining the purpose and conditions of the Temporary Liquidity Guarantee Program.

-

(FDIC 2017) Federal Deposit Insurance Corporation (FDIC). 2017. Crisis and Response: An FDIC History, 2008–2013. Washington, DC: Federal Deposit Insurance Corporation.

Book describing the FDIC’s actions in the GFC.

-

(FDIC 2019) Federal Deposit Insurance Corporation (FDIC). 2019. “Temporary Liquidity Guarantee Program,” updated February 19, 2019 .

Web page detailing the features of the Temporary Liquidity Guarantee Program and its results.

-

(Federal Reserve n.d.) Federal Reserve Bank of New York (Federal Reserve). n.d. “Commercial Paper Funding Facility,” accessed November 11, 2021.

Web page explaining the purpose of the Federal Reserve’s Commercial Paper Funding Facility.

-

(Krimminger 2020) Krimminger, Michael H. 2020. “The Temporary Liquidity Guarantee Program.” In First Responders: Inside the U.S. Strategy for Fighting the 2007–2009 Global Financial Crisis, edited by Ben S. Bernanke, Timothy F. Geithner, and Henry M. Paulson, Jr., with J. Nellie Liang, 226–53. New Haven: Yale University Press.

Book chapter examining the TLGP and its efficacy.

-

(McNamara 2020) McNamara, Christian. 2020. “Senate Bill Temporarily Restores Treasury, FDIC Guarantee Authority Eliminated Post-GFC.” Yale School of Management (blog), March 27, 2020.

Blog entry that discusses temporary powers granted to financial government agencies due to the COVID-19 pandemic.

-

(US Treasury n.d.) US Department of the Treasury (US Treasury). n.d. “Capital Purchase Program Overview,” accessed November 11, 2021.

Web page explaining the Department of the Treasury’s Capital Purchase Program.

-

(FDIC 2008c) Federal Deposit Insurance Corporation (FDIC). 2008c. “FDIC Temporary Liquidity Guarantee Program Election Form,” October 14, 2008.

Election form that eligible institutions were required to submit to signal their intent to participate in the TLGP.

-

(FDIC 2008d) Federal Deposit Insurance Corporation (FDIC). 2008d. “Technical Briefing on the Temporary Liquidity Guarantee Program.” Transcript of teleconference, October 14, 2008.

Transcript of technical briefing on the Temporary Liquidity Guarantee Program and its details.

-

(FDIC 2008e) Federal Deposit Insurance Corporation (FDIC). 2008e. “Temporary Liquidity Guarantee Program.” Federal Register 73, no. 210, October 29, 2008.

Interim rule announcing the Temporary Liquidity Guarantee Program.

-

(FDIC 2008f) Federal Deposit Insurance Corporation (FDIC). 2008f. “Temporary Liquidity Guarantee Program: Extension of Deadlines and Election Instructions.” Financial Institution Letter 125-2008, November 3, 2008.

Document highlighting deadlines associated with the Temporary Liquidity Guarantee Program and explaining how an institution could participate in the program.

-

(FDIC 2008g) Federal Deposit Insurance Corporation (FDIC). 2008g. “Temporary Liquidity Guarantee Program; Final Rule.” Federal Register 73, no. 229, November 26, 2008.

Document detailing the final rules that would govern the Temporary Liquidity Guarantee Program.

-

(FDIC 2009a) Federal Deposit Insurance Corporation (FDIC). 2009a. “Transaction Account Guarantee Extension: Third Quarter 2009.” Financial Institution Letter, 48-2009, August 27, 2009.

Document explaining the extension of the Transaction Account Guarantee Program to eligible institutions.

-

(FDIC 2009b) Federal Deposit Insurance Corporation (FDIC). 2009b. “Final Rule Regarding Limited Amendment of the Temporary Liquidity Guarantee Program to Extend the Transaction Account Guarantee Program with Modified Fee Structure.” Federal Register 74, no. 168, September 1, 2009.

Document explaining the extension of the Transaction Account Guarantee Program and its change to a risk-based fee.

-

(FDIC 2010a) Federal Deposit Insurance Corporation (FDIC). 2010a. “Temporary Liquidity Guarantee Program Frequently Asked Questions,” updated May 26, 2010.

Web page answering questions about the Temporary Liquidity Guarantee Program, along with its restrictions.

-

(FDIC 2010b) Federal Deposit Insurance Corporation (FDIC). 2010b. “Final Rule Regarding Amendment of the Temporary Liquidity Guarantee Program to Extend the Transaction Account Guarantee Program.” Federal Register 75, no. 123, June 28, 2010.

Document detailing the final rule regarding the Temporary Liquidity Guarantee Program, specifically the decision to extend the Transaction Account Guarantee Program.

-

(FDIC 2015) Federal Deposit Insurance Corporation (FDIC). 2015. “Temporary Liquidity Guarantee Program; Unlimited Deposit Insurance Coverage for Noninterest-Bearing Transaction Accounts.” Federal Register 80, no. 208, October 28, 2015.

Document explaining the alteration of the Transaction Account Guarantee Program under the Dodd-Frank Act.

-

(FDIC 2020) Federal Deposit Insurance Corporation (FDIC). 2020. “Deposit Insurance FAQs,” updated May 13, 2020.

Web page detailing the role of the FDIC and how the FDIC fulfills obligation if a bank fails.

-

(CARES Act 2020) Coronavirus Aid, Relief, and Economic Security Act (CARES Act). 2020. Public Law 116–136, 134 Stat. 291. March 27, 2020.

Economic stimulus bill passed in response to the COVID-19 pandemic.

-

(Dodd-Frank Act 2010) Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). 2010. Public Law 111–203, 124 Stat. 1376, July 21, 2010.

Legislation creating several reforms and amendments in the wake of the Global Financial Crisis.

-

(EESA 2008) Emergency Economic Stabilization Act of 2008 (EESA). Public Law 110–343, 122 Stat. 3765. October 3, 2008.

Law increasing the deposit insurance limit to $250,000.

-

(FDICIA 1991) Federal Deposit Insurance Corporation Improvement Act (FDICIA). 1991. Public Law 102–242, 105 Stat. 2236. December 19, 1991.

Law reforming the FDIC and providing for a systemic risk exemption.

-

(USC 2006) U.S. Congress (USC). 2006. “Corporation Monies.” 12 U.S.C. §1832.

Law setting out the FDIC’s systemic risk exemption.

-

(FDIC 2008h) Federal Deposit Insurance Corporation (FDIC). 2008h. “FDIC Announces Plan to Free Up Bank Liquidity: Creates New Program to Guarantee Bank Debt and Fully Insure Non-Interest Bearing Deposit Transaction Accounts.” Press release, October 14, 2008.

Press release announcing the FDIC’s Temporary Liquidity Guarantee Program and its goal of increasing confidence and liquidity.

-

(FDIC 2008i) Federal Deposit Insurance Corporation (FDIC). 2008i. “FDIC Board of Directors Approves TLGP Final Rule: Industry Funded Program Fully Backed by FDIC Guarantee; Will Promote Lending.” Press release, November 28, 2008.

Press release detailing the FDIC’s final rule on the Temporary Liquidity Guarantee Program.

-

(FDIC 2010c) Federal Deposit Insurance Corporation (FDIC). 2010c. “FDIC Board of Directors Approves Extension of Transaction Account Guarantee Program.” Press release, April 13, 2010.

Press release announcing the FDIC’s decision to extend the Transaction Account Guarantee Program until December 31, 2010.

-

(FDIC 2010d) Federal Deposit Insurance Corporation (FDIC). 2010d. “FDIC Approves Temporary Unlimited Deposit Insurance Coverage for Noninterest-Bearing Transaction Accounts.” Press release, November 9, 2010.

Press release announcing the FDIC’s final rule regarding deposit insurance, in compliance with the Dodd-Frank Act.

-

(Cave 2011) Cave, Jason C. 2011. “Statement of Jason C. Cave, Deputy Director for Complex Financial Institutions Monitoring, Office of Complex Financial Institutions, Federal Deposit Insurance Corporation on the Temporary Liquidity Guarantee Program, Congressional Oversight Panel, Washington, D.C. March 4, 2011.” Testimony before the Congressional Oversight Panel, March 4, 2011.

Congressional testimony given regarding the Temporary Liquidity Guarantee Program.

-

(CRS 2018) Congressional Research Service (CRS). 2018. “Costs of Government Interventions in Response to the Financial Crisis: A Retrospective,” updated September 12, 2018.

Report analyzing the effect of US government intervention in the Global Financial Crisis.

-

(FDIC 2009c) Federal Deposit Insurance Corporation (FDIC). 2009c. “Quarterly Banking Profile: Fourth Quarter 2008.” FDIC Quarterly 3, no. 1.

Quarterly report discussing the FDIC’s activities.

-

(FDIC 2011) Federal Deposit Insurance Corporation (FDIC). 2011. “Quarterly Banking Profile - Fourth Quarter 2010” FDIC Quarterly 5, no. 1.

Report discussing the FDIC’s activities, especially in light of the Dodd-Frank Act.

-

(FDIC 2012) Federal Deposit Insurance Corporation (FDIC). 2012. 2011 Annual Report.

Report detailing the FDIC’s annual activities for the year 2011.

-

(GAO 2010) Government Accountability Office (GAO). 2010. “Federal Deposit Insurance Act: Regulators’ Use of Systemic Risk Exception Raises Moral Hazard Concerns and Opportunities Exist to Clarify the Provision.” GAO 10–100, April 2010.

Government report examining the legal basis and the effects of the Temporary Liquidity Guarantee Program.

-

(Davison 2019) Davison, Lee. 2019. “The Temporary Liquidity Guarantee Program: A Systemwide Systemic Risk Exception.” Journal of Financial Crises 1, no. 2: 1–39.

Paper examining the Temporary Liquidity Guarantee Program and its effects.

-

(Demirgüç-Kunt and Detragiache 2002) Demirgüç-Kunt, Asli, and Enrica Detragiache. 2002. “Does Deposit Insurance Increase Banking System Stability? An Empirical Investigation.” Journal of Monetary Economics 49, no. 7: 1373–1406.

Journal article examining whether deposit insurance increases stability in the banking sector and whether private or public deposit insurance promotes greater stability.

-

(IADI 2014) International Association of Deposit Insurers (IADI). 2014. “Core Principles for Effective Deposit Insurance Systems.”

Report that presents the IADI’s principles for deposit insurance.

-

(Katz 2020) Katz, Justin. 2020. “The Debt Guarantee Program of the Temporary Liquidity Guarantee Program (U.S. GFC).” Journal of Financial Crises 2, no. 3: 546–75 .

Case study examining the Debt Guarantee Program, which was one aspect of the Temporary Liquidity Guarantee Program.

-

(Krimminger 2018) Krimminger, Michael H. 2018. “Responding to the Global Financial Crisis: What We Did and Why We Did It: The Temporary Liquidity Guarantee Program.” Preliminary discussion draft for the conference “Responding to the Global Financial Crisis: What We Did and Why We Did It,” Hutchins Center, Brookings Institution, Washington, DC, September 11–12, 2018.

Paper analyzing the Temporary Liquidity Guarantee Program, its design, its implementation, and its effects.

-

(Lawson and Kulam 2021) Lawson, Aidan, and Adam Kulam. 2021. “US Capital Purchase Program.” Journal of Financial Crises 3, no. 3: 821–90.

Case study analyzing the Department of the Treasury’s Capital Purchase Program.

-

(Shapiro and Dowson 2012) Shapiro, Robert J., and Doug A. Dowson. 2012. “The Financial Hazards and Risks Entailed in Extending Unlimited Federal Guarantees for Deposits in Transaction Accounts,” NDN Globalization Initiative paper, October 2012.

Academic paper examining the potential hazards of unlimited deposit insurance.

-

(Wiggins 2020) Wiggins, Rosalind. 2020. “The Commercial Paper Funding Facility (U.S. GFC).” Journal of Financial Crises 2, no. 3: 174–201.

Case study examining the Federal Reserve’s Commercial Paper Funding Facility.

Taxonomy

Intervention Categories:

- Account Guarantee Programs

Countries and Regions:

- United States

Crises:

- Global Financial Crisis