Bank Holidays & Fund Suspensions

United States: Reserve Primary Fund Suspension, 2008

Purpose

The SEC stated that the temporary suspension of redemption rights in the Primary Fund was necessary to protect the fund’s investors

Key Terms

-

Announcement DateSeptember 22, 2008

-

End DateDecember 9, 2014

-

Legal AuthoritySection 22(e)(3) of the Investment Company Act of 1940

-

AdministratorThe Securities and Exchange Commission

-

Communication and DisclosureThe SEC stated that it retroactively suspended redemption rights in the Primary Fund to protect the fund’s investors and alleged that the operators of the fund violated securities laws

-

Permitted WithdrawalsWithdrawals were not permitted for investors in the Primary Fund

-

Treatment of Depositors or InvestorsThe Primary Fund delayed payments by seven days for redemptions of more than $10,000 on September 17 and sought an SEC order to suspend redemption rights

-

OutcomesWhen the final distribution was made in December 2014, investors had recovered 99.1 cents per share held in the Primary Fund on September 15, 2008

-

Notable FeaturesThe SEC alleged that the Primary Fund operators violated securities laws by telling investors the fund still had a $1.00 NAV on September 15 and part of the day on September 16; A court overruled the fund’s plan to set aside $3.5 billion of investors’ funds to handle litigation costs, replacing it with a more modest $83.5 million expense fund

In 2008, the Reserve Primary Fund was the world’s third-largest money market fund with $62.5 billion in assets. Following Lehman Brothers’ bankruptcy filing on September 15, the Primary Fund’s $785 million position in Lehman debt securities was underwater, and the fund faced severe redemption pressures from investors. In just two days, redemption requests surpassed $40 billion. Owing to the fund’s inability to liquidate assets at or above par value in the frozen markets and the inability of its sponsor, the Reserve Management Company, Inc. (RMCI), to support investors, the Reserve announced on September 16 that the Primary Fund had “broken the buck” at 4pm that day, meaning that its net asset value per share had fallen under $0.995. Following RMCI’s recommendation, the Primary Fund delayed payments by seven days for redemptions of more than $10,000, and the Reserve requested the Securities and Exchange Commission (SEC) to allow the Primary Fund to suspend redemption rights for outstanding redeemable securities. On September 22, the SEC issued an order permitting the Primary Fund to temporarily suspend redemption rights with effect as of September 17. Following the suspension, the fund’s management company began liquidating the Primary Fund on September 29; however, the liquidation was marked by several legal challenges. The Primary Fund’s investors recovered about half their funds at the end of October 2008 and 79 cents for every dollar in early December; they waited two years for recoveries to reach 99 cents on the dollar and received a final distribution in December 2014 when recoveries ultimately reached 99.1 cents.

This case study is about the temporary suspension of redemption rights for Reserve Primary Fund investors following an order issued by the Securities and Exchange Commission (SEC). The module also briefly discusses related assistance provided to the Reserve U.S. Government Fund and other fund series managed by the Reserve Management Company, Inc. (RMCI).

In 2008, RMCI provided investment advisory services to five investment companies, offering 22 open-end portfolios (collectively, the Reserve Funds or the Reserve) and managing approximately $120 billion in assets. In the fall of 2008, the Reserve Primary Fund was the flagship Reserve fund and the world’s third-largest money market fund (MMF) with $62.5 billion in assets under management (AUM).

As of Sunday, September 14, 2008, the Primary Fund held commercial paper and medium-term notes issued by Lehman Brothers with a face value of $785 million, or about 1.26% of the Primary Fund’s total assets. Early in the morning of September 15, Lehman Brothers filed for bankruptcy. As a consequence of this announcement, the Primary Fund faced severe redemption pressures. At 10:10am on September 15, State Street Bank and Trust Company, the Primary Fund’s custodial bank, having funded approximately $10 billion in redemption requests through the Primary Fund’s overdraft account, stopped funding these requests and suspended the Primary Fund’s overdraft privileges. Although redemptions were no longer being paid out, by 3:45pm the next day, unfulfilled redemption requests surpassed $30 billion, bringing total redemptions to roughly two-thirds of the Primary Fund’s total AUM.

On September 16, the Reserve reported that the fund had marked down its Lehman holdings to zero, which caused the net asset value (NAV) of the Primary Fund to fall under $1.00 per share at 4pm. As a result, the Primary Fund became the second US-based MMF to ever break the buck, in other words, the second fund whose shares declined in value below $0.995 per share, the lowest point at which they could permissibly still be rounded to $1.00FIn 1994, Community Banker's U.S. Government Money Market Fund lost a large fraction of its investments in floating-rate securities and became the first US-based money market fund to break the buck when the portfolio’s market value declined due to a sharp increase in interest rates. That event did not create widespread panic at other money market funds (ICI 2012a). (Gardephe 2010; The Reserve 2008a). On September 16, the Reserve also announced a seven-calendar-day redemption delay. The Reserve Yield Plus Fund and the Reserve International Liquidity Fund, Ltd., two other Reserve Funds, also broke the buck that day (The Reserve 2008b). The Reserve Primary Fund was the only money market fund that held Lehman debt securities and did not have an affiliate with sufficient resources to support a $1.00 per share NAV (US GAO 2023).

Following the unprecedented run on the Reserve Primary Fund, the run spread to the other Reserve Funds and almost immediately to the entire money market fund industry (Shapiro 2012).

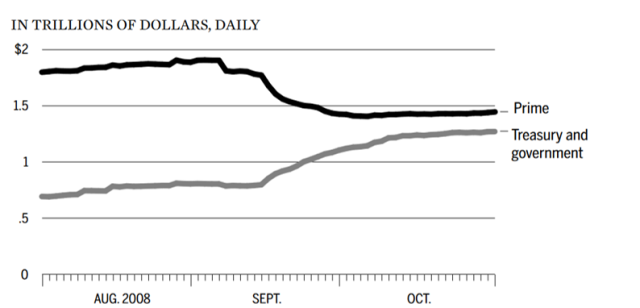

As indicated in Figure 1, between September 10 and October 1, $439 billion was redeemed from prime funds and $362 billion flowed into government-only funds (Bernanke 2015).

Figure 1: Investments in Money Market Funds, August–October 2008

Note: In a flight to safety, investors shifted from prime money market funds to government money market funds, which invest in Treasury and agency securities and repo backed by those securities.

Note: In a flight to safety, investors shifted from prime money market funds to government money market funds, which invest in Treasury and agency securities and repo backed by those securities.

Source: FCIC 2011.

Patrick McCabe, an economist at the Federal Reserve, states of the broader run on the MMFs: “It was overwhelmingly clear that we were staring into the abyss—that there wasn’t a bottom to this—as the outflows picked up steam on Wednesday and Thursday. The overwhelming sense was that this was a catastrophe that we were watching unfold” (FCIC 2011, 357). MMFs started hoarding cash and stopped rolling over commercial paper positions issued by companies, financial institutions, and local and state governments. The MMF industry held 40% of outstanding commercial paper in 2008, and during September 2008, the funds’ retreat from the markets caused the short-term credit markets to freeze (Shapiro 2012).

On September 22, 2008, the SEC issued an order permitting the Reserve to suspend the redemption rights for outstanding redeemable securities and postpone payment for shares that had been submitted for redemption but had not yet been paid in the Primary Fund and the U.S. Government Fund, with effect as of September 17, 2008. The SEC stated that the order was “necessary for the protection of their security holders” (SEC 2008a, 2). The order permitted the Primary Fund to “suspend redemptions and payment of redemption proceeds, until the markets are liquid to a degree that enables each fund to liquidate portfolio securities without impairing the net asset value of each fund, or until the Commission rescinds the order,” according to a frequently-asked-questions statement the SEC later released (SEC 2008d, 1). The fund would create a plan for the orderly liquidation of assets that would be supervised by the SEC, and the fund also represented that it would keep appropriate records of the events.

On October 24, 2008, the SEC issued a second order suspending redemption rights and permitting delayed payment to allow for orderly liquidations in several other Reserve Funds, with effect from October 8, 2008 (SEC 2008b).

On September 30, the board of trustees of the Reserve Funds voted to liquidate the Reserve U.S. Government Fund (The Reserve 2008f). On November 20, 2008, the US Treasury Department entered into an agreement to accept the Reserve U.S. Government Fund into its temporary guarantee program for Money Market Funds, announced on September 19, 2008, although the fund was not originally eligible. The Treasury agreed to serve as a buyer of last resort for the fund’s securities, if the fund was unable to liquidate portfolio securities at or above amortized cost within 45 days, so that shareholders in the fund would recover their entire investment (US Treasury 2008b).

On December 3, the Primary Fund’s board approved a plan of liquidation and distribution of assets that would have distributed up to 91.72 cents per share, while setting aside $3.5 billion in a special reserve to cover any legal expenses and judgments against the fund filed by investors. On May 5, 2009, the SEC filed an action to the United States District Court for the Southern District of New York (USDC–SDNY) to prohibit the Primary Fund from enacting that proposal since it did not consider the plan “fair and equitable.” The SEC objected that the plan would “effectively halt all further distributions to any investors in order to fund an enormous ‘Special Reserve’ to benefit the Fund’s Trustees and individuals other than investors” (SEC 2009b, 3). The SEC also objected that the plan would have allowed investors who redeemed early to receive all of their money back; the SEC instead proposed a pro rata distribution plan treating all investors equally. It also proposed replacing the special reserve with a far smaller expense fund of $83.5 million to cover fund management fees and expenses. Seventy-five investors in the Primary Fund submitted comments on this revised pro rata distribution plan. Investors who represented more than 75% of the Primary Fund’s remaining assets either supported or did not have any objections to the SEC’s distribution plan (Gardephe 2009a). The objections of the shareholders representing the remaining 25% of assets are described in Key Design Decision No. 9, Verification of Solvency. A court later ruled in support of the SEC’s plan.

By July 16, 2010, investors in the Primary Fund recovered 99% of their investments, and they ultimately recovered approximately 99.1 cents on the dollar, after RMCI received approval from a federal court in September 2014 to make the final distribution (Primary Fund-In Liquidation 2014a). A timeline of events related to the suspension of redemption rights for the Reserve Primary Fund is shown in Figure 2.

Figure 2: Timeline of Important Events—Reserve Funds

Source: Author’s analysis.

Steven Shafran, a senior US Treasury official at the time, notes that by allowing some investors (the first $10 billion before State Street stopped honoring requests) to redeem at par on the morning of September 15, 2008, the fund concentrated the Lehman loss onto the remaining investors who had not redeemed fast enough. He highlights that in the overnight cash market, investors were not rewarded for their patience and investors fled to safety (Shafran 2020).

Then–Federal Reserve Bank of New York President Timothy Geithner points out that although the Lehman paper represented only 1.2% of the Primary Fund’s AUM, it was enough to spark a run since the Primary Fund had no capital buffers to absorb losses (Geithner 2014, 195).

A paper analyzes sponsor support provided to 14 other MMFs that held Lehman debt and points out that the extent of sponsor support was limited to the Lehman exposure of each of these funds. The paper goes on to say that the ultimate cause of the Primary Fund’s downfall was the lack of sponsor support that could have provided nonmarket liquidity (Akay, Griffiths, and Winters 2015).

Key Design Decisions

Purpose

1

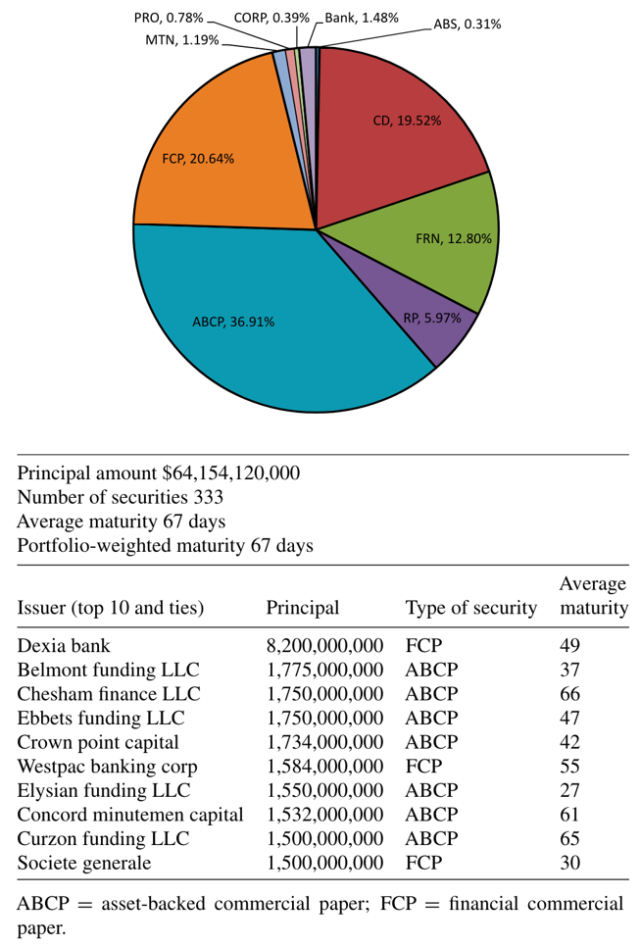

The Reserve Primary Fund, the flagship Reserve fund, increased its commercial paper holdings from 1% of the fund’s assets in July 2007 to nearly 60% of assets a year later. When the Primary Fund increased commercial paper holdings—including Lehman debt—its gross yield increased rapidly relative to that of its peers, and the fund’s assets jumped from $30 billion in July 2007 to $67 billion in July 2008; virtually all of the asset growth was commercial paper (McCabe 2010). By September 2008, the Primary Fund was the world’s third-largest money market fund and had $62.5 billion in assets under management (The Reserve 2008h). In September 2008, approximately 21% of the Primary Fund’s assets were held in financial commercial paper, including debt issued by Lehman Brothers.FFigure 5 in the Appendix provides a detailed breakdown of the Reserve Primary Fund’s portfolio.The Primary Fund faced severe redemption pressures following Lehman Brothers’ bankruptcy filing, since the fund held $785 million (1.2% of the Primary Fund’s total AUM) of unsecured commercial paper and medium-term notes issued by Lehman (The Reserve 2008k). Without capital support from an affiliate, any loss greater than 0.5% of a fund’s assets would have been sufficient to cause the fund to break the buck, that is, to report a net asset value below $0.995 per share, the lowest point at which they could permissibly be rounded to $1.00 (ICI 2009).

Confronted with Lehman’s failure, the fund’s board pursued several options before suspending redemptions on September 16. First, in a conference call at 9:30 in the morning on September 15, the board decided on the advice of KPMG, its accounting firm, and outside legal counsel to change the accounting method for the Primary Fund from amortized cost to fair value, to reflect the impact of the Lehman bankruptcy on the NAV per share.FThe Primary Fund calculated its NAV on an approximately hourly basis. The board also concluded that it was not in the best interest of the Primary Fund shareholders to liquidate the Lehman debt at fire sale prices amidst the credit market turmoil and near freeze of trading. Although the fund’s chief investment officer advised the board that there was indicative pricing in the market for the Lehman paper between 45% and 80% of par, the board decided to value the Lehman paper at 80% of par, the high end of that range. At that level, the value of the Primary Fund shares fell to $0.9975, just above the level required to allow the fund to maintain a NAV per share of $1.00 (SEC 2009a).

But extraordinary redemption requests during trading on September 15 forced the board to meet again at 1pm to consider further options. Under normal conditions, investors would receive payment for their redeemed shares from State Street within an hour of submitting the redemption request. At 10:10am on September 15, State Street, having received approximately $10 billion in redemptions, stopped funding redemption requests and suspended the Primary Fund’s overdraft privileges. By 1pm, redemption requests totaled $16.5 billion (Gardephe 2009a). Given the unprecedented market illiquidity, Bruce Bent Sr., the chairman of RMCI and the Primary Fund, notified the board that the fund would not be able to liquidate assets at par value to meet redemptions but would likely have to do so at “fire sale prices” (The Reserve 2008k, 2). In other words, the fair value of assets at current market prices was below par, implying that without some kind of support from its sponsors, the fund would have to break the buck. To avoid breaking the buck, the board authorized management to enter into a credit support agreement with RMCI. It also authorized management to file the required notice with the SEC about the support agreement.

By September 16, 2008, redemptions at the Primary Fund exceeded $40 billion. The fund never entered into a credit support agreement with RMCI; the SEC later determined that RMCI had misrepresented its willingness to provide credit support to the fund. Later on September 16, the board notified the SEC and issued a press release announcing that it had written off the entire value of the Lehman debt and that the fund had therefore broken the buck (SEC 2009a; The Reserve 2008b).

At one point during the run, the Primary Fund asked the Federal Reserve Bank of New York for help to avoid breaking the buck; however, the New York Fed declined, since it did not think it could stop the run. The Fed did not have the legal authority to guarantee MMFs and protect their investors from losses, and Donald Kohn, then vice chair of the Fed, characterized the Primary Fund’s request for aid from the Fed as a “ridiculous request” (Geithner 2014, 195). However, within days, the Treasury rather than the Fed had found the authority to guarantee MMF investors, and the Fed, under Kohn’s leadership, had launched its own broad-based program to lend to banks for the purpose of buying commercial paper from MMFs, described in Key Design Decisions No. 2, Part of a Package (Logan, Nelson, and Parkinson 2020).

The Reserve Funds submitted an application to the SEC to suspend redemption rights for the Primary Fund and U.S. Government Fund securities and postpone payment for shares that had requested redemption but which had not been paid; research has been unable to locate the application or determine the date on which it was sent (SEC 2008a, 1). On September 22, 2008, the SEC issued an exemptive order permitting the funds to temporarily suspend redemption rights and postpone payment for shares redeemed but not paid (SEC 2008a, 2). This SEC order was applied retrospectively beginning September 17, 2008 (SEC 2008a, 2). The SEC stated that the order was necessary for the protection of the investors and it would stay in effect until the markets were “liquid to a degree that enable[d] each Fund to liquidate portfolio securities without impairing the net asset value of each or until revoked by the commission” (SEC 2008a, 2).

Part of a Package

1

Money market funds experienced a broad run by investors following the news of the Primary Fund’s breaking the buck. Marcin Kacperczyk and Philipp Schnabl estimate about $172 billion in MMF redemptions within three days. Kacperczyk and Schnabl also estimate that the total value of commercial paper outstanding fell by 15%, from approximately $1.8 trillion to $1.4 trillion, within a month of the Primary Fund’s announcement (2010).

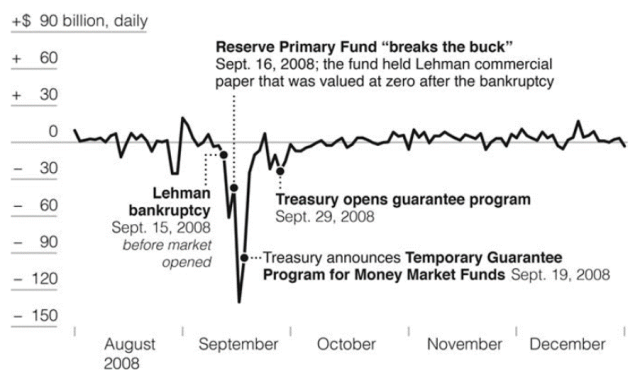

On September 19, the US Department of the Treasury announced the Temporary Guarantee Program for Money Market Funds to arrest the run on the MMFs, and it became operational on September 29 (Shapiro 2012). The temporary guarantee program was open to all MMFs regulated under Rule 2a-7 of the Investment Company Act of 1940 with a NAV of at least $0.995 as of September 19, 2008. For a quarterly fee, the Treasury would guarantee the share price of any eligible money market mutual fund that applied and paid for the programFThe guarantee was funded by the then–$50 billion Exchange Stabilization Fund. For more details on the temporary guarantee program, see Vergara (2022). (US Treasury 2008a). Figure 3 charts daily money market fund flows between August and December 2008.

Figure 3: Prime Institutional Money Market Fund Flows

Source: YPFS and Brookings Institution.

Source: YPFS and Brookings Institution.

The Primary Fund was not eligible for the guarantee program. However, other Reserve Funds were, according to the Reserve. In November, the Treasury entered into an agreement with the Reserve U.S. Government fund (which otherwise was not eligible) to allow the fund to participate in the temporary guarantee programFThe Reserve announced that the Primary II Fund, Reserve Liquid Performance Money Market Fund, and Treasury and Repo Fund, were also eligible to participate in the temporary guarantee program; however, it is not clear if these funds participated in the program (The Reserve 2008j). Wilson (2020) claims to have obtained, through FOIA, a list of all fund managers that received a guarantee, and Reserve is not on it. (US Treasury 2008b). The agreement stated that the Reserve U.S. Government Fund had 45 days to sell assets at or above their amortized cost, and the Treasury's Exchange Stabilization Fund would purchase any remaining securities after this period at amortized cost, up to an amount required to ensure that each shareholder received $1 per share. The Reserve U.S. Government Fund did not create any taxpayer losses through the temporary guarantee program (Henriques 2008).

The Treasury’s temporary guarantee program ended a year after it was announced, on September 18, 2009, and generated $1.2 billion in fee revenue. At its peak usage, the program guaranteed 366 MMF management companies and 1,486 individual funds. The guarantee gave fund managers the ability to protect investors if they were unable to maintain the value of a fund’s holdings above $0.995 and were forced to liquidate. Ultimately, no funds were forced into liquidation during the time the program was active.

The Fed also created two broad-based programs to provide liquidity to MMFs that were still experiencing runs. On September 19, 2008, the Federal Reserve launched the Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility “to assist money funds that hold such paper in meeting demands for redemptions by investors and [to] foster liquidity in the [asset-backed commercial paper] ABCP markets and broader money markets” (Fed 2008, 1). Through the AMLF, the Federal Reserve extended nonrecourse loans at the primary credit rate to US depository institutions and bank holding companies to finance their purchases of high-quality ABCP from money market mutual funds.

During the first two weeks of operation, the Federal Reserve’s AMLF loaned $150 billion to banks to purchase ABCP from MMMFs (the equivalent of 21% of all outstanding ABCP); however, its usage declined over time as redemption pressures waned and markets improved (Wiggins 2020a). Kacperczyk and Schnabl (2010) highlight that this was the first time in history that the Fed purchased commercial paper directly, and by January 2009, the Fed was the single largest purchaser of commercial paper, owning $357 billion, or 22.4% of the market, through its various lending facilities.

On October 21, 2008, the Fed also announced the Money Market Investor Funding Facility, which was “intended to provide liquidity to U.S. money market mutual funds and certain other money market investors, thereby increasing their ability to meet redemption requests and hence their willingness to invest in money market instruments, particularly term money market instruments” (Fed 2020, 5). The MMIFF would loan up to $540 billion to a series of special purpose vehicles (SPVs) that would use the funds to purchase certificates of deposit, bank notes, and commercial paper from eligible money market investors (Wiggins 2020b).

The Federal Reserve’s MMIFF expired on October 30, 2009, and was not used. Collectively, the Fed and Treasury’s programs immediately slowed the run on MMFs, but any evaluation must consider the coexistence of the other programs targeting the same problem.

Legal Authority

1

The Fund had to seek SEC approval at various stages in 2008 and 2009.

First, on September 15, because the Lehman debt exceeded more than 0.5% of the Primary Fund’s total assets, the fund had to provide the SEC with a plan to handle the Lehman securities, as stipulated under Rule 2a-7 of the Investment Company Act of 1940FUnder Rule 2a-7, since the Lehman debt exceeded more than 0.5% of the Primary Fund’s total assets the fund’s board had to determine whether it was in the best interest of the fund to dispose of the Lehman debt and notify the SEC promptly of its decision (The Reserve 2008k, 1). (SEC 2010).

Second, some sources suggest that on September 16, the Reserve Funds filed an application with the SEC for permission to suspend redemptions and postpone payments to investors, under Section 22(e) of the Investment Company Act of 1940. This section of the law provides, in part, that,

No registered investment company shall suspend the right of redemption, or postpone the date of payment or satisfaction upon redemption of any redeemable security in accordance with its terms for more than seven days after the tender of such security to the company or its agent designated for that purpose for redemption, except . . .

(3) for such other periods as the Commission may by order permit for the protection of security holders of the company” (US Congress 2023, 64–65) (author’s emphasis)

On September 22, 2008, the SEC issued a temporary order pursuant to Section 22(e)(3), with effect as of September 17, permitting the Primary Fund and the Reserve U.S. Government Fund to temporarily suspend redemptions of outstanding shares and postpone payment for shares that had already been submitted for redemption but not yet paid, until market liquidity improved so that the funds could sell their assets without impairing each fund’s NAV or until the SEC rescinded the order (SEC 2008a).

In December 2008, the SEC’s approval was again required after the closure of the fund for the fund’s proposed plan to disburse remaining funds to shareholders. As noted in Key Design Decision No. 5, Governance, the SEC did not approve of the fund’s proposed plan and brought a court action under Section 21(d)(5) of the Securities and Exchange Act of 1934 to substitute a different plan that it proposed.

Section 21(d)(5) of the Securities and Exchange Act of 1934 states that “[i]n any action or proceeding brought or instituted by the Commission under any provision of the securities laws, the Commission may seek, and any Federal court may grant, any equitable relief that may be appropriate or necessary for the benefit of investors” (SEC 2009b, 5).

Further, under Section 25(c) of the Investment Company Act, the USDC–SDNY had the authority to “enjoin the consummation of any plan of reorganization of [a] registered investment company upon proceedings instituted by the Commission . . . [where] such a plan is not fair and equitable to all security holders” (SEC 2009b, 5). The court approved the SEC’s plan of distribution.

Administration

1

Under Section 22(e) of the Investment Company Act of 1940, the Primary Fund was permitted to postpone payment for redemptions for up to seven days (SEC 2008c). The Primary Fund added a supplement to its prospectus on September 17, 2008, announcing that redemption payments would be no later than seven calendar days after the redemption request was receivedFIn its prospectus as of September 28, 2007, the Primary Fund had outlined that it might suspend redemptions for more than seven days if trading were suspended on the New York Stock Exchange, an emergency ere declared by the SEC, or if otherwise permitted by SEC order (The Reserve 2007). (The Reserve 2007).

The Reserve Funds was organized as a Massachusetts business trust, and under Article 9 Section 4(b) of the declaration governing the trust, either the trustees or the shareholders were authorized to liquidate the fund (The Reserve 2008l). After redemptions were frozen in the Primary Fund, while the liquidation of the fund was being decided on and administered, RMCI started posting the complete portfolio of the fund with a one-day lag (The Reserve 2008g).

Governance

1

The SEC approved the fund’s application to suspend redemptions and postpone payments on September 22. On September 29, 2008, the Primary Fund’s board voted to liquidate the fund and distribute its assets to shareholders (The Reserve 2008d).

On December 3, 2008, the Primary Fund’s board approved a plan of liquidation and distribution of assets that would have distributed up to 91.72 cents per share, subject to provisions made for a special reserve. Under the special reserve proposal, the fund also would have set aside $3.5 billion for costs and damages related to more than 20 lawsuits filed against the operators of the Primary Fund after September 15 (The Reserve 2009).

On May 5, 2009, the SEC filed an action with a US District Court, pursuant to Section 25© of the Investment Company Act, to prohibit the Primary Fund from enacting its plan for distributing funds to investors in the liquidation. The SEC criticized the proposed diversion of funds to the $3.5 billion special reserve. The SEC also said that the fund’s decision to redeem some investors’ claims on September 15 at a $1.00 NAV disadvantaged other investors who tried to redeem later, and the plan was therefore not “fair and equitable” to investors (SEC 2009b, 6). The SEC took issue with the way the fund had valued the Lehman assets and calculated its NAV. Since the SEC considered the fund’s NAV calculations and communications to have been flawed, the SEC proposed a distribution plan that paid all shareholders the same pro rata amount regardless of when they had submitted their redemption request. Some shareholders were expecting to receive a NAV of $1.00, since they had received redemption confirmations for a $1.00 NAV, and filed objections to the SEC’s pro rata distribution plan (SEC 2009b). (See Key Design Decisions No. 8, Treatment of Depositors or Investors, and No. 9, Verification of Solvency.)

On November 25, 2009, Judge Paul Gardephe of USDC–SDNY issued an order enjoining the Primary Fund’s liquidation plan and approving the SEC’s proposed pro rata distribution plan. Judge Paul Gardephe’s order also reduced the amount set aside in the expense fund to $83.5 million (Gardephe 2009b).

Communication

1

Some funds that held Lehman debt, such as the Evergreen fund, issued statements that they would draw on available credit support from their sponsors, if necessary, to support the $1.00 NAV. The Primary Fund had no such agreements to draw upon to support its NAV, and despite representations by RMCI that it would provide credit support and board approval for the same, no such agreements were ever entered into (SEC 2009a).

Before announcing that the Primary Fund broke the buck and receiving the SEC’s exemptive order permitting suspension of redemptions and postponement of payments, RMCI, Resrv Partners, and the Bents engaged in active communications aimed at stopping the run on the Primary Fund and related funds. The SEC later sued such parties alleging among other things that these statements were materially false:

Over a two-day period in September [15–16] 2008, after the news of Lehman Brothers’ bankruptcy filing roiled the US financial markets, Defendants engaged in a systematic campaign to deceive the investing public into believing that the Primary Fund – their flagship money market fund – was safe and secure despite its substantial Lehman holdings. That campaign involved both the knowing dissemination of false information to the Primary Fund's Board of Trustees, investors, and rating agencies and, in the case of certain Defendants, the knowing concealment of the true effect of the Lehman holdings on the Fund. (SEC 2009a, 2)

The defendants issued press releases and newsletters, and their employees engaged in numerous telephone calls and meetings that disseminated inaccurate information regarding the NAV, impact of Lehman securities, redemption rates, overdraft protection, liquidity, and the availability of credit support to the Primary Fund board, shareholders, rating agencies, media, and general public.

Following the SEC’s order on September 22, 2008, the Reserve issued a press release clarifying that the order was “intended to allow us to fulfill all outstanding redemption orders and ensure an orderly sale process that [sought] to obtain best pricing for the interest of shareholders and integrity of the funds’ NAVs” (The Reserve 2008c, 1). By September 29, the Primary Fund’s board had voted to liquidate the entire fund and distribute functionally all its assets to shareholders; those shareholders who had not yet submitted a redemption request would be involuntarily redeemed (The Reserve 2008d).

Beginning on September 19, the Treasury and the Federal Reserve launched a number of programs to stem the run on the MMF industry. The Treasury stated that “maintaining confidence in the money-market fund industry is critical to protecting the integrity and stability of the global financial system” (Newman 2008, 1). See Key Design Decision No. 2, Part of a Package.

Details of Holidays, Suspensions, or Gates

1

The Primary Fund calculated its NAV on an approximately hourly basis per its prospectus. Generally, the fund transferred redemption payments to its shareholders within an hour of receiving redemption requests, via its custodial bank, State Street Bank. State Street Bank paid redeeming shareholders by applying the redemption amounts against RMCI’s overdraft account. However, after State Street suspended the Primary Fund’s overdraft privileges, the fund announced a seven-day delay in transmitting proceeds of redemptions in excess of $10,000 (The Reserve 2008a). It isn’t clear from the sources we consulted whether the fund continued to honor redemptions under $10,000 after the SEC’s September 22 ruling.

Treatment of Depositors or Investors

1

Bent II had stated in an email on September 14, 2008, to RMCI’s director of marketing that providing a line of credit to the Primary Fund and supporting the $1.00 NAV was “not an option for us” (SEC 2009a, 15). However, on September 15, Bent II emailed the director of sales and marketing that RMCI would provide credit support to the Primary Fund and that it was waiting for final SEC approval to support the fund. The SEC later stated that RMCI never requested approval for credit support. Bent II also disseminated similar false statements regarding credit support to representatives at Moody’s and Standard & Poor’s and authorized the dissemination of these false statements to clients on a need basis. In some cases, based on the false information disseminated, prospective investors were assured that the Primary Fund would not break the buck, and purchases of new shares in the fund were processed until September 16.

On the evening of September 15, it appeared that the plan to slow redemption activity by convincing investors that the Primary Fund's NAV was safe had been successful: “The client base reacted positively to this news and the redemption activity slowed greatly” (SEC 2009a, 26). However, total redemption requests in the Primary Fund surpassed $20 billion by close of business September 15, 2008, but nearly half remained unfunded. The other half were largely funded through an overdraft account at the fund’s custodial bank (The Reserve 2008l). By September 16, 2008, redemption requests at the Primary Fund exceeded $40 billion.

On September 17, the Reserve published NAVs for several funds including the Primary Fund and stated that all redemption requests received for the fund before 3pm on September 16 would be redeemed at an NAV of $1.00. The SEC would later assert that at the time the Reserve Funds made the statement, its management knew it was false and was unfair to shareholders. The SEC’s enforcement action is described in further detail in Key Design Decision No. 10, Other Conditions. On September 30, 2008, the board of trustees of the Reserve Funds announced that the first distribution to the fund’s investors would occur around October 13, 2008 (The Reserve 2008e). However, the initial distribution was delayed until October 30, 2008, due to technical challenges arising out of using a NAV under $1.00, among other issues (The Reserve 2008h).

On October 2, 2008, the Reserve announced that it would post the complete portfolios of the Primary Fund and the U.S. Government Fund with a one-day lag to better inform the funds’ investors (The Reserve 2008g). Ultimately, under the approved plan of distribution, all distributions were made pro rata, including the interim distributions made before the final liquidation plan was approved (The Reserve 2008l).

TD Ameritrade and Ameriprise Financial said that they would reimburse their clients for up to a 3% loss in the Primary Fund (Anand and Scannell 2012). Some investors in the Primary Fund were therefore able to recover their entire investment since TD Ameritrade and Ameriprise Financial agreed to mitigate potential losses.

The Primary Fund’s investors eventually regained access to most of their money through eight distributions that occurred after September 15, 2008, with the final distribution taking place on December 9, 2014. Figure 4 shows the asset distribution schedule. The final recoveries for the fund’s shareholders amounted to 99.1 cents on the dollar (Primary Fund-In Liquidation 2014a).

Figure 4: Asset Distribution Schedule for the Primary Fund

Sources: Primary Fund-In Liquidation 2014a; 2014b; The Reserve 2008e; The Reserve 2008l; The Reserve 2010a; The Reserve 2010b.

When Bruce Bent and his partner Henry B. R. Brown launched the first MMF in 1970, they developed the funds to provide investors with immediate liquidity and safety of principal invested amounts. Money market funds are subject to stringent regulations to ensure their safety and liquidity. Mary L. Shapiro, then-chair of the SEC, has said that although investors ultimately lost only one penny per share, the real damage was caused by the loss of liquidity promised by the Reserve Primary Fund. Investors in the Primary Fund who temporarily lost access to liquidity could have been unable for months to make mortgage payments, pay employees’ salaries, or fund their businesses (Shapiro 2012).

Shareholders in the Primary Fund also filed a class action lawsuit against the operators of the fund (Church 2013). As part of a court-approved settlement, they were awarded $55 million in January 2014 (Primary Fund In Liquidation 2014).

Verification of Solvency

1

One of the reasons the SEC alleged that the operators of the Primary Fund were liable for federal securities law violations was the discrepancy in the fund’s NAV calculation for September 15 and 16, 2008. The Reserve later admitted that the fund’s NAV calculation was wrong, blaming an “administrative error” on September 16, 2008, and should have indicated that the fund broke the buck when its NAV reached $0.9944 at 11am on September 16, earlier than previously stated (SEC n.d., 5). The Reserve explained that this error occurred because the fair-value markdown to Lehman securities was not taken into consideration on September 16, and the Primary Fund’s assets were overstated by approximately $170 million (The Reserve 2008i). When the SEC submitted its pro rata distribution plan for the Primary Fund’s assets on May 5, 2009, it stated that the fund’s NAV calculations from those days were “hopelessly and irreparably compromised by inaccurate and incomplete information” (SEC 2009b, 2).

Owing to the unreliability of the fund’s NAV calculation, the hierarchy of claims for unpaid shareholders who redeemed on September 15 and 16, 2008, and the NAV per share value of their redemptions were examined during legal proceedings. Some shareholders received confirmations that their redemption requests were received and would be paid out at the stable NAV of $1.00 per share, but the SEC stated that these confirmations were based on erroneous NAV calculations and did not create a contractual right to receive a $1.00 per share redemption. A few investors who redeemed early also claimed that they became unsecured creditors as opposed to shareholders when they received confirmation of redemptions requests. However, the SEC stated that this reasoning was flawed since all fund investors were creditors of the fund, regardless of their redemption activity.

The SEC also alleged that Bent II instructed the director of fund accounting to secretly record receivables transactions for the Yield Plus Fund and International Liquidity Fund totaling $17 million, to avoid disclosing that these funds had broken the buck before the Primary Fund. When the Primary Fund broke the buck, these transactions were reversed (SEC 2009a).

Other Conditions

1

The Reserve Primary Fund and Reserve U.S. Government Fund agreed to suspend sales in the funds when the SEC granted their application to suspend redemptions in the funds (SEC 2008a). Owing to the Reserve U.S. Government Fund’s agreement with the Treasury, the U.S. Government Fund’s advisers and trustees were required to waive their fees accrued after November 19, 2008, to the extent that fund shareholders did not receive distributions of $1.00 per share (US Treasury 2008b).

The SEC filed an enforcement action against RMCI, Resrv Partners, the Reserve Primary Fund, and the controlling persons of RMCI—Bruce Bent Sr. and Bruce Bent II—alleging several counts of securities law violations. The SEC provided evidence that the defendants published or authorized the dissemination of several false statements and concealed material facts from the board of trustees, investors, and rating agencies (See Key Design Decision No. 6, Communication and Disclosure). After a four-week civil trial at the USDC–SDNY, the Bents were cleared of the fraud charges; however, the court found Bent II liable for one claim of negligence (Grind and Steinberg 2012). Judge Paul Gardephe awarded $750,000 to the SEC, instead of the $130 million in damages the SEC sought (Raymond and Stempel 2013). Judge Gardephe also declined to order a permanent injunction from engaging in activities subject to securities law against the Reserve entities and Bruce Bent II.

Exit Strategy

1

The Primary Fund’s liquidation process took more than six years, and the fund was terminated in late December 2015 (Primary Fund In Liquidation 2015, 1).

Regulatory Changes

1

Following the Global Financial Crisis of 2007–2009, the SEC amended Rule 2a-7 of the Investment Company Act of 1940 to enhance the regulatory regime for MMFs and mitigate the systemic risk posed by MMFs (Shapiro 2009; Su 2020). These amendments were approved in January 2010 and provided adherence to strict levels of credit and interest rate risks, high diversification requirements, periodic stress testing, disclosing monthly portfolio information, three new liquidity requirements, and procedures to deal with money market funds that break the buck (ICI 2012b).

Following this amendment, the Investment Company Institute published a checklist for suspending redemptions and liquidating a MMF that outlines the major steps to follow before suspending redemptions (ICI 2011).

Also of note is that then-SEC Chair Shapiro highlights in her testimony on June 21, 2012, before the US Senate, that although the SEC amended regulations in 2010 to make MMFs more resilient, they remained susceptible to runs and posed systemic risks (2012).

Evidence gathered following the run on MMFs during the COVID-19 pandemic suggests that the SEC reforms adopted in 2010 and 2014 to strengthen MMFs were not effective at preventing runs and may have in fact contributed to the runs (US GAO 2023).

Key Program Documents

-

(Logan, Nelson, and Parkinson 2020) Logan, L., Nelson, W., & Parkinson, P. 2020. “The Fed’s Novel Lender-of-Last-Resort Programs.” In First Responders, ed. Bernanke et al., 81–112. New Haven: Yale Univ. Press.

Book chapter examining the Fed’s novel lending practices, including those designed for money market funds.

-

(Shafran 2020) Shafran, S.M. 2020. “Money Market Funds: Collapse, Run, and Guarantee.” In First Responders, ed. Bernanke et al., 193–207. New Haven: Yale Univ. Press.

Book chapter examining the Temporary Guarantee Program for Money Market Funds.

-

(Gardephe 2009a) Gardephe, Paul G. 2009a. Memorandum Opinion – In Re the Reserve Fund Securities and Derivative Legislation. November 25, 2009.

Court order permitting the suspension of redemptions in certain Reserve Fund mutual funds to permit their orderly liquidation.

-

(Gardephe 2009b) Gardephe, Paul G. 2009b. Order – In Re the Reserve Fund Securities and Derivative Legislation. November 25, 2009.

Court order requiring a liquidation plan for the Reserve Primary Fund’s assets and pro rata distribution.

-

(Gardephe 2010) Gardephe, Paul G. 2010. Memorandum Opinion and Order – In Re the Reserve Fund Securities and Derivative Legislation. February 24, 2010.

Court order permitting the suspension of redemptions in certain Reserve Fund mutual funds to permit their orderly liquidation.

-

(SEC 2008b) Securities and Exchange Commission (SEC). 2008b. Reserve Municipal Money-Market Trust, et al.; Notice of Application and Temporary Order. October 24, 2008.

SEC order permitting the suspension of redemptions in most of the Reserve Funds to permit their orderly liquidation.

-

(SEC 2009a) Securities and Exchange Commission (SEC). 2009a. SEC Enforcement Action Charging the Operators of the Reserve Primary Fund. May 5, 2009.

SEC enforcement action alleging that the operators of the Reserve Primary Fund violated securities law.

-

(SEC 2009b) Securities and Exchange Commission. 2009b. SEC’s Memo in Response to Objections to Its Application for Injunctive Relief and Approval of Proposed Distribution Plan. Aug. 21, 2009.

The SEC’s brief, including an Appendix reflecting an amended plan clarifying the term sheet previously submitted by the SEC.

-

(SEC 2010) Securities and Exchange Commission (SEC). 2010. Investment Company Act of 1940. Money Market Fund Reform, Final Rule, March 4, 2010.

Rules change to the Investment Company Act of 1940 describing notification regulations in the event of insolvency with respect to a portfolio security.

-

(US Congress 2023) US Congress. 2023. Investment Company Act of 1940. January 5, 2023.

Amendment to the Investment Company Act of 1940.

-

(SEC 2008a) Securities and Exchange Commission. 2008a. Order Temporarily Suspending Redemption and Postponing Payment for Investment Company Shares under Section 22(e)(3) of the Investment Company Act. Sept. 22, 2008.

SEC order permitting the suspension of redemptions in two Reserve Funds to permit their orderly liquidation.

-

(Akay, Griffiths, and Winters 2015) Akay, Ozgur, Mark Griffiths, and Drew Winters. 2015. “Reserve Primary: Fools Rush in Where Wise Men Fear to Tread!” Journal Of Investment Management 13, no. 1: 10–26, 2015.

Paper analyzing the buildup of commercial paper holdings in the Primary Fund and listing reasons for the fund’s failure.

-

(Kacperczyk and Schnabl 2010) Kacperczyk, Marcin, and Philipp Schnabl. 2010. “When Safe Proved Risky: Commercial Paper during the Financial Crisis of 2007–2009.” Journal of Economic Perspectives 24, no. 1: 29–50, 2010.

Paper examining the role of commercial paper and money market funds during the Global Financial Crisis.

-

(McCabe 2010) “The Cross Section of Money Market Fund Risks and Financial Crises.” Fed Board, Finance and Economics Discussion Series, Paper No. 2010-51, September 12, 2010.

Paper examining the relationship between MMF risks and outcomes during the asset-backed commercial paper market issues in 2007 and the Global Financial Crisis.

-

(Vergara 2022) Vergara, Ezekiel. 2022. “United States: Temporary Guarantee Program for Money Market Funds.” Journal of Financial Crises 4, no. 2: 657–72.

YPFS case study examining the 2008 Temporary Guarantee Program for Money Market Funds.

-

(Wiggins 2020a) Wiggins, Rosalind Z. 2020a. “The Asset-Backed Commercial Paper Money Market Mutual Fund Liquidity Facility (AMLF).” Journal of Financial Crises 2, no. 3: 229–55, March.

YPFS case study examining the Asset-Backed Commercial Paper Money Market MutualFund Liquidity Facility (AMLF).

-

(Wiggins 2020b) Wiggins, Rosalind Z. 2020b. “Money Market Investor Funding Facility (U.S. GFC).” Journal of Financial Crises 2, no. 3: 257–79, October.

YPFS case study examining the Money Market Investor Funding Facility.

-

(Wiggins et al., forthcoming) Wiggins, Rosalind Z., Owen Heaphy, Stella Schaefer-Brown, Anmol Makhija, Greg Feldberg, and Andrew Metrick. Forthcoming. “Survey of Bank Holidays and Fund Suspensions.”

Survey of YPFS case studies examining bank holidays and fund suspensions.

-

(Wilson 2020) Wilson, Linus. 2020. “Broken Bucks: Money Funds That Took Taxpayer Guarantees in 2008.” Journal of Asset Management 21 no. 5: 375–92.

A paper that examines the characteristics of funds accepted into the US Treasury’s temporary guarantee of money market mutual funds.

-

(Anand and Scannell 2012) Anand, Shefali, and Kara Scannell. 2012. “Ameritrade to Make Clients Whole on Primary Fund.” Wall Street Journal, November 12, 2012.

News article discussing the outcome of the fraud charges the SEC filed against the operators of the Reserve Primary Fund.

-

(Church 2013) Church, Steven. 2013. “Reserve Primary Fund Settles Lawsuit for $54.9 Million.” Bloomberg, September 9, 2013.

News article discussing the settlement of a class action lawsuit in the Reserve Primary Fund case.

-

(Grind and Steinberg 2012) Grind, Kristen, and Julie Steinberg. 2012. “Reserve Primary Managers Cleared in SEC Fraud Case.” Wall Street Journal, November 12, 2012.

News article discussing the outcome of the fraud charges the SEC filed against the operators of the Reserve Primary Fund.

-

(Henriques 2008) Henriques, Diana B. 2008. “U.S. Treasury to Support a Frozen Money Fund.” New York Times, October 21, 2008.

Article discussing the US Treasury Department’s agreement to be the buyer of last resort for the Reserve US Government Fund.

-

(Newman 2008) Newman, Richard. 2008. “A Confidence Boost for Money Funds ; Treasury Backs up Assets, Fed Offers Aid.” The Record, September 20, 2008.

News article discussing the outcome of the fraud charges the SEC filed against the operators of Reserve Primary Fund.

-

(Raymond and Stempel 2013) Raymond, Nate, and Jonathan Stempel. 2013. “US Judge Awards $750,000 in Case of Money Fund That ‘Broke Buck.’” Reuters, September 30, 2013.

News article discussing fines RMCI, Resrv Partners, and Bruce Bent II had to pay following an SEC lawsuit.

-

(Fed 2008) Board of Governors of the Federal Reserve System (Fed). 2008. “Federal Reserve Board Announces Two Enhancements to Its Programs to Provide Liquidity to Markets.” Press release, September 19, 2008.

The Federal Reserve’s announcement of programs to aid the MMF industry.

-

(Primary Fund In Liquidation 2014) Primary Fund In Liquidation. 2014. “Additional Information Regarding Primary Fund In Liquidation.” Press release, January 23, 2014.

The Primary Fund-In Liquidation press release announcing court approval of settlement for class action litigation.

-

(Primary Fund In Liquidation 2015) Primary Fund In Liquidation. 2015. “Termination of Primary Fund In Liquidation.” Press release, November 4, 2015.

The Primary Fund-In Liquidation press release announcing its termination.

-

(Primary Fund-In Liquidation 2014a) Primary Fund-In Liquidation. 2014a. “Additional Information Regarding Primary Fund-In Liquidation: Federal Court Approves Final Distribution.” Press release, September 23, 2014.

The Primary Fund-In Liquidation press release announcing the final distribution to investors and total recoveries.

-

(Primary Fund-In Liquidation 2014b) “Fund Update—Final Distribution Set for December 9, 2014.” Press release, December 1, 2014.

The Primary Fund-In Liquidation press release announcing the date of the final distribution to investors.

-

(The Reserve 2008a) The Reserve. 2008a. “A Statement Regarding the Primary Fund.” Press release, September 16, 2008.

The Reserve press release announcing that following the bankruptcy of Lehman Brothers, the NAV of the Primary Fund series fell under one dollar per share.

-

(The Reserve 2008b) The Reserve. 2008b. “Fund NAVs for September 16, 2008.” Press release, September 17, 2008.

The Reserve press release announcing NAVs for three funds, including the Primary Fund.

-

(The Reserve 2008c) The Reserve. 2008c. “SEC Order Granted to Protect Interest of Reserve Shareholders.” Press release, September 23, 2008.

The Reserve press release clarifying the SEC order to suspend rights of redemption in the Primary Fund and US Government Fund series.

-

(The Reserve 2008d) The Reserve. 2008d. “Important Notice Regarding Reserve Primary Fund.” Press release, September 29, 2008.

The Reserve press release announcing the liquidation of the Primary Fund series.

-

(The Reserve 2008e) The Reserve. 2008e. “Timeframe for Initial Distribution Payment of Reserve Primary Fund.” Press release, September 30, 2008.

The Reserve press release clarifying the timeframe for the initial distribution of assets from the Primary Fund series.

-

(The Reserve 2008f) The Reserve. 2008f. “Important Notice Regarding US Government Fund.” Press release, October 1, 2008.

The Reserve press release announcing the liquidation of the U.S. Government Fund series.

-

(The Reserve 2008g) The Reserve. 2008g. “Important Notice to Reserve Fund Investors.” Press release, October 2, 2008.

The Reserve press release answering frequently asked questions regarding the Primary Fund and the US Government Fund.

-

(The Reserve 2008h) The Reserve. 2008h. “Reserve Primary Fund Disbursement Update.” Press release, October 15, 2008.

The Reserve press release explaining the reason for a delay in the initial distribution of cash to investors on a pro rata basis.

-

(The Reserve 2008i) The Reserve. 2008i. “Important Notice Regarding Reserve Primary Fund’s Net Asset Value.” Press release, November 26, 2008.

The Reserve’s admission of discrepancy in the Primary Fund’s NAV calculation.

-

(The Reserve 2008j) The Reserve. 2008j. “Reserve Announces Participation of Some Funds in the Treasury Guarantee Program.” Press release, November 26, 2008.

The Reserve’s announcement of the temporary guarantee program participation eligibility for a few of its fund series.

-

(The Reserve 2009) The Reserve. 2009. “The Primary Fund: A Statement Regarding Special Reserve under the Plan of Liquidation.” Press release, February 26, 2009.

The Reserve press release announcing its plan of liquidation and distribution of assets for the Primary Fund, approved on December 3, 2008.

-

(The Reserve 2010a) The Reserve. 2010a. “Additional Information Regarding the Reserve Primary Fund.” Press release, May 27, 2010.

Reserve statement providing an update on asset distributions that occurred until January 29, 2010, and expenses accrued.

-

(The Reserve 2010b) The Reserve. 2010b. “Reserve Primary Fund to Distribute $215 Million.” Press release, July 15, 2010.

The Reserve press release announcing the seventh distribution to investors.

-

(US Treasury 2008a) US Department of the Treasury (US Treasury). 2008a. “Treasury Announces Temporary Guarantee Program for Money Market Funds.” Press release, September 29, 2008.

US Treasury press release announcing the opening of its Temporary Guarantee Program for Money Market Funds.

-

(US Treasury 2008b) US Department of the Treasury (US Treasury). 2008b. “Treasury Enters into Agreement to Assist the Reserve Fund’s US Government Money Market Fund.” Press release, November 20, 2008.

US Treasury Department announcement of liquidation agreements to support the Reserve US Government Fund.

-

(Bernanke 2015) Bernanke, Ben S. 2015. The Courage to Act: A Memoir of a Crisis and Its Aftermath. New York: W.W. Norton & Company.

Book describing the Bear Stearns crisis from the point of view of then–Federal Reserve Chairman Bernanke.

-

(FCIC 2011) Financial Crisis Inquiry Commission (FCIC). 2011. “The Financial Crisis Inquiry Report.” January 2011.

Final report of the National Commission on the Cause of the Financial and Economic Crisis in the United States.

-

(Geithner 2014) Geithner, Timothy F. 2014. Stress Test: Reflections on Financial Crises. New York: Crown Publishing Group.

Memoir describing former FRBNY President and Treasury Secretary Timothy Geithner’s reflections on the Global Financial Crisis.

-

(ICI 2009) Investment Company Institute (ICI). 2009. “Report of the Money Market Working Group.” March 17, 2009.

ICI money market working group report to the ICI’s board of governors including recommendations to make MMFs more resilient to extreme market conditions such as those encountered after the Primary Fund’s failure.

-

(ICI 2011) Investment Company Institute (ICI). 2011. “Checklist for Suspending Redemptions and Liquidating a Money Market Fund,” March 7, 2011.

A checklist for suspending redemptions and liquidating a money market fund following the SEC’s amendment to Rule 2a-7, following the Global Financial Crisis.

-

(ICI 2012a) Investment Company Institute (ICI). 2012a. “Money Market Funds in 2012: History of Money Market Funds.” February 13, 2012.

ICI note providing a brief history of money market funds.

-

(ICI 2012b) Investment Company Institute (ICI). 2012b. “History of Rule 2a‐7—The Evolution of Money Market Fund Regulation.” March 1, 2012.

ICI note providing a brief history of money market fund regulations.

-

(SEC n.d.) Securities and Exchange Commission (SEC). n.d. “Exhibit 5 - SEC’s Proposed Distribution Plan.”

Revised calculations for the Primary Fund’s NAV as of September 15–16, 2008.

-

(Shapiro 2009) Shapiro, L. Mary. 2009. “Speech by SEC Chairman: Statement at SEC Open Meeting.” Speech delivered at an open meeting of the SEC, Washington, DC, June 24, 2009.

Mary L Shapiro, then-SEC chair’s opening statements during a meeting considering rules to enhance the regulatory regime for money market mutual funds.

-

(Shapiro 2012) Shapiro, L. Mary. 2012. “Perspectives on Money Market Mutual Fund Reforms.” Testimony before the Committee on Banking, Housing, and Urban Affairs, US Senate, June 21, 2012.

Mary L Shapiro, then-SEC chair’s testimony before the Committee on Banking, Housing, and Urban Affairs of the United States Senate.

-

(Su 2020) Su, Eva. 2020. “Money Market Mutual Funds: A Financial Stability Case Study.” Congressional Research Service Report No. IF11320, March 24, 2020.

Congressional Research Service report examining the implications of money market fund runs on financial stability.

-

(The Reserve 2007) The Reserve. 2007. “Prospectus for the Primary Fund, US Government Fund, US Treasury Fund, and Reserve Liquid Performance Money Market Fund.” September 28, 2007.

Prospectus for four Reserve Funds and supplements to the prospectus.

-

(The Reserve 2008k) The Reserve. 2008k. “Minutes of the Joint Meeting of the Board of Trustees of the Reserve Fund.” September 15, 2008.

Minutes of the meeting of the board of trustees of the Reserve Fund discussing the impact of the Lehman bankruptcy on the Reserve Primary Fund.

-

(The Reserve 2008l) The Reserve. 2008l. “The Primary Fund: Plan of Liquidation and Distribution of Assets.” December 3, 2008.

A copy of the plan of liquidation and distribution of assets adopted by the board of the Primary Fund.

-

(US GAO 2023) US Government Accountability Office (US GAO). 2023. “Money Market Mutual Funds: Pandemic Revealed Unresolved Vulnerabilities.” Report No. GAO-23-105535, February 2023.

US GAO report to congressional committees on vulnerabilities in the money market mutual fund industry.

-

(Fed 2020) Board of Governors of the Federal Reserve System (Fed). 2020. “Credit and Liquidity Programs and the Balance Sheet.” March 24, 2020.

Webpage outlining lending facilities established by the Fed.

-

(SEC 2008c) Securities and Exchange Commission (SEC). 2008c. “Transcript of Recorded Telephone Conversations - Osnato Declaration Exhibit 29.” September 15, 2008.

Transcript of a phone conversation in which the effect of the Lehman bankruptcy is discussed.

-

(SEC 2008d) Securities and Exchange Commission (SEC). 2008d. “Division of Investment Management Responses to Frequently Asked Questions about the Reserve Fund and Money Market Funds.” October 1, 2008.

The SEC’s Division of Investment Management’s answers to a few frequently asked questions regarding the suspension of redemptions in the Reserve Primary Fund.

Figure 5: Reserve Primary Fund’s Portfolio Composition as of August 31, 2008

Source: Akay, Griffiths, and Winters 2015, 21.

Source: Akay, Griffiths, and Winters 2015, 21.

Taxonomy

Intervention Categories:

- Bank Holidays & Fund Suspensions

Countries and Regions:

- United States

Crises:

- Global Financial Crisis