Market Support Programs

United States: Primary Dealer Credit Facility

Purpose

“Allow primary dealers to support smooth market functioning and facilitate the availability of credit to businesses and households” and “foster the functioning of financial markets more generally."

Key Terms

-

Launch DatesAuthorized: March 17, 2020 Announced: March 17, 2020

-

Operational DateMarch 20, 2020

-

End DateMarch 31, 2021

-

Legal AuthoritySection 13(3) of the Federal Reserve Act

-

Source(s) of FundingFederal Reserve

-

AdministratorFederal Reserve Bank of New York

-

Overall SizeAggregate amount of haircut-adjusted eligible collateral that each primary dealer could issue to the Fed

-

TermOvernight to 90-day maturity, renewable upon borrower’s election

-

Interest / Haircut RatePrimary credit rate (25 basis points)

-

CollateralOMO-acceptable collateral and investment-grade securities

-

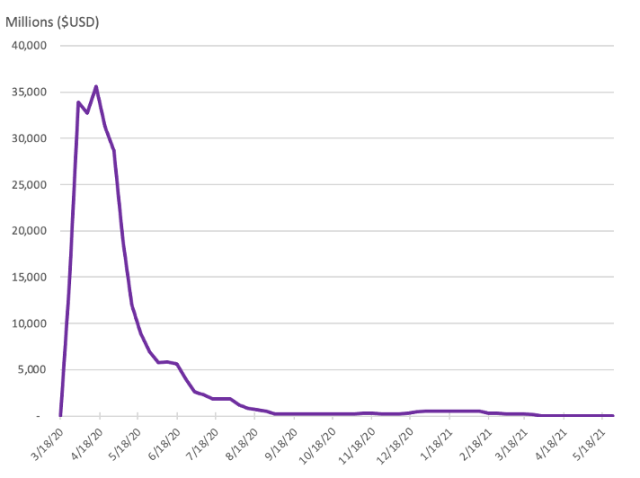

Peak Utilization$35.6 billion during the week of April 15, 2020

In March 2020, the uncertain outlook for the United States in the face of the COVID-19 pandemic prompted extremely high demand for cash and near-cash assets. Amid intense selling pressure from investors, securities dealers were unable to fully absorb the high volume of trade orders into their inventory due to balance sheet capacity and funding constraints. As dealer capacity declined and demand for liquidity continued rising, volatility spread to the critical and normally highly liquid market for US Treasury securities, prompting the Federal Reserve to increase open market operations (March 12) and begin historically large purchases of US Treasuries (March 16). On March 17, the Fed used its Section 13(3) emergency authority to establish the Primary Dealer Credit Facility (PDCF), modeled after a program that the Fed implemented in response to the Global Financial Crisis (GFC) in 2008. The PDCF lent to primary dealers at the primary credit rate for up to 90 days, collateralized by dealers’ inventory of securities. Compared to the 2008 PDCF, the 2020 PDCF accepted a narrower range of collateral, offered terms longer than overnight, and did not charge a penalty fee for frequent use. Use of the PDCF peaked at $35.6 billion in loans outstanding the week of April 15, 2020, then gradually decreased. The PDCF expired on March 31, 2021, after two extensions to its operating dates.

As the economic outlook turned negative in in the face of the COVID-19 pandemic, broad risk-off sentiment drove heavy investor demand for cash and other liquid assets. Amid a “dash-for-cash” in March 2020, nonbanksFNonbanks, particularly relative value hedge funds, sold roughly $90 billion in less-liquid Treasuries as they unwound basis trades (FSB 2020). (See Barth and Kahn (2020) for more information.) and foreign holders sold record amounts of less-liquid, long-dated Treasuries in favor of shorter-dated assets (TIC 2021; He, Nagel, and Song 2020, 3, 9).

At first, securities dealers who intermediate in short-term markets absorbed the increased trade flows, including the sales of Treasuries, but this reportedly expanded dealers’ balance sheets against the constraints imposed by regulatory or risk-management considerations, and by mid-March dealers became unable or unwilling to continue acting as market-makers (FRB 2020b; Duffie 2020; Chen et al. 2021). Without dealers providing liquidity, assets in dealer-intermediated markets traded at material discounts, and liquidity dried up in even the most liquid marketFMeanwhile, businesses and governments which normally issue commercial paper (CP) with multi-week maturity began issuing paper that matured on a daily basis (FRB 2020b). Money market mutual funds (MMFs) saw large outflows as investors demanded redemptions, and corporate debt markets stalled as nonfinancial corporations sought funding while facing credit downgrades (FSB 2020). (FRB 2020b; FRB and Goldberg 2020; Duffie 2020).

On March 12, the Fed responded by offering $1.5 trillion in repurchase agreements, or repos, in an effort to provide liquidity to dealers (FRBNY 2020a; Duffie 2020). Take-up was low, however, with market participants blaming balance-sheet constraints and an inability to efficiently distribute cash throughout the system (Timiraos and Verlaine 2020). Beginning on March 16, the Fed purchased $1 trillion in Treasuries over three weeks, partly as a means of freeing up balance sheet space by reducing dealer inventory (FSB 2020). Yet these purchases did not ease constraints as much as the Fed intended due to regulatory capital requirements and the fact that the Fed pays for these Treasuries with reserves, which the banking system must absorb (Duffie 2020).

As market conditions continued to deteriorate, the Fed announced on March 17 that it would use its emergency lending authorities under Section 13(3) to re-establish the Primary Dealer Credit Facility (PDCF), which lent to primary dealers with full recourse at the primary credit (discount window) rate for a term up to 90 days (FRB 2020m). The Fed lent against the dealer’s inventory of securities and applied haircuts based on the riskiness of the assets pledged as collateral, which was revalued daily by the clearing bank, Bank of New York Mellon (BNYM) (FRBNY 2020b).

The Fed established two “companion” facilities—the Commercial Paper Funding FacilityFFor more information on the CPFF, see Engbith (2021). (CPFF) on March 17 and the Money Market Mutual Fund Liquidity FacilityFMoney market mutual funds provide funding to dealers in the repo markets. For more information on the MMLF, see Mott (2021). (MMLF) on March 18—to help stabilize short-term funding marketsFAnother facility, the Secondary Market Corporate Credit Facility (SMCCF), helped stem the risk-off activity in corporate debt markets, which dealers intermediate, although dealer intermediation in these markets has declined in recent years (Kargar et al. 2020). (Clarida, Duygan-Bump, and Scotti 2021). On April 1, 2020, the Fed temporarily allowed bank holding companies to exempt reserves and Treasuries from their Supplementary Leverage Ratio Rule (SLR) calculations to further ease constraints on dealer balance sheets (FRB 2020h).

The COVID-era PDCF was modeled on a 2008 GFC predecessor that was established in response to repo-market stress driven by concerns about dealer exposure to subprime mortgages (Yang 2020; Martin and McLaughlin 2020). The 2008 PDCF accepted a greater variety of collateral than the 2020 PDCF, extended credit only overnight, and charged regular users of the facility a frequency-based fee (Yang 2020; Martin and McLaughlin 2020).

Lending through the pandemic-era PDCF began on March 20, 2020, and peaked three weeks later at $35.6 billion (see Figure 1). For context, the 2008 PDCF reported $130 billion in loans outstanding at the height of its useFNote that a greater range of collateral was eligible for the 2008 PDCF than the 2020 PDCF. Additionally, in March 2020, only $340 billion in privately issued securities were financed in the tri-party repo market, compared to $600 billion in August 2008 (Martin and McLaughlin 2020). (Yang 2020). Initially scheduled to expire on September 30, 2020, with other emergency lending facilities, the Fed and Treasury extended the operating window of the PDCF to December 31, 2020, and then again to March 31, 2021 (FRB 2020l; FRB 2020k). The facility shed its final holdings the week of April 21, 2021 (FRB 2020q). In its May 9, 2021, report to Congress, the Fed reported that, as of April 30, 2021, all loans had been repaid, no losses were realized on the PDCF, and the Federal Reserve Bank of New York had received interest, fees, and other revenue on the PDCF of $12.8 million (FRB 2021a).

Figure 1: Loans Outstanding at the PDCF

Source: Federal Reserve H.4.1 Statistical Release.

Source: Federal Reserve H.4.1 Statistical Release.

The PDCF extended 356 loans to 21 primary dealers totaling $132 billion against $149 billion worth of collateral (FRB 2022). The median borrowing term was 14 days (FRB 2022). 35% of loans had terms greater than 84 days, while 22% of loans were overnight (FRB 2022).

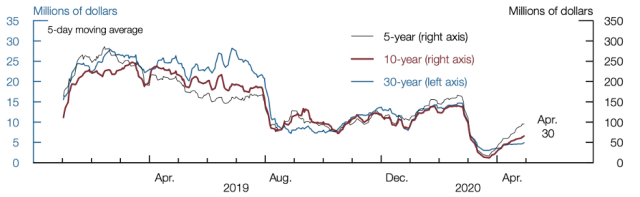

By offering more favorable rates than dealers could find in the markets, the PDCF provided a backstop for dealers to finance their inventory of securities, thus allowing dealers to resume their intermediation and smooth market functioning (Martin and McLaughlin 2020; Pozsar 2020). The PDCF became operational on March 20, 2020, and saw immediate and sustained utilization through the end of April 2020 (Martin and McLaughlin 2020; FRB 2020b). In mid-April, when investors’ demand for liquidity across multiple asset classes rose again, the higher order volume once again “clogged” the balance sheets of dealers, limiting their ability to warehouse investor trade flows and causing the price of liquidity to rise (FRB and Goldberg 2020; Duffie 2020). By May, the Fed found that dislocations in the market for US Treasury securities had subsided, and measures of market functioning—such as market depth, bid-ask spreads, and divergence of similar-maturity yields—had improved (FRB 2020b) (see Figure 2).

Figure 2: Treasury Market Depth

Source: FRB 2020.

Amid widespread turmoil such as in March 2020, evaluating any individual crisis-time intervention on its own terms can be a challenge. This is especially true of the PDCF, which the Fed established during a month that saw several efforts designed to alleviate constraints on dealers, provide access to liquidity, and improve Treasury market functioning. Efforts included expanded repo operations, historically large purchases of Treasuries, and dollar swap lines with foreign central banks,FThe rapid increase in supply was due to foreign investors (central banks and investors in tax havens) selling about $300 billion in Treasuries, mutual funds selling roughly $15 billion, and net issuance of $150 billion by the U.S. Treasury Department (He, Nagel, and Song 2020, 3). Foreign official institutions, including central banks, sold roughly $60 billion in Treasuries in March 2020, due in part to emerging market economies raising USD cash to satisfy funding needs and intervene in foreign exchange markets (TIC 2021; FSB 2020, 30). Dollar swap lines established by the Fed helped relieve this pressure on the US Treasury market and the dealers who intermediate it. as well as the launch of companion facilities in interrelated markets: the CPFF for commercial paper (CP), the MMLF for money market mutual funds invested in commercial paper and municipal securities, and the Secondary Market Corporate Credit Facility for corporate debt (FRB 2020b).

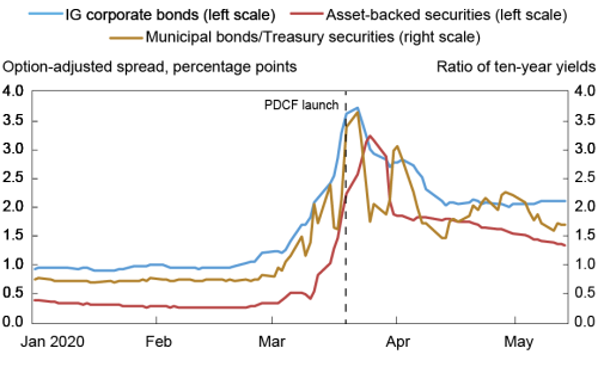

Utilization of the PDCF, CPFF, and MMLF peaked quickly after launch and, considered together, these interventions appear to have had a beneficial effect on dealers, with indicators of market functioning improving after their announcements (FRB 2020b) (see Figure 3). Following the announcement of the CPFF on March 17, issuance of CP soon returned to normal multi-week maturity (Chen et al. 2021; FRB 2020b). Carlson and Macchiavelli (2021) show that the PDCF enhanced the ability of primary dealers to provide intermediation services, specifically by facilitating the issuance of CP and negotiable certificates of deposit (CD). They also show that CP and CD issuers benefited indirectly from the PDCF, as the facility enabled issuers to issue more securities at lower cost when the CP or CD that was issued was pledged as collateral to the PDCF by a dealer (Carlson and Macchiavelli 2021).

Figure 3: Spreads Since PDCF Launch

Source: Chen et al. 2021.

In the corporate debt market, the combined announcements of the PDCF and Primary and Secondary Market Corporate Credit Facilities appear to have reversed the “dash for cash,” and investor demand for liquidity—and the cost to dealers for supplying it—quickly receded (Kargar et al. 2020, 4; Chen et al. 2021). Moreover, dealers’ apparent reluctance to absorb corporate debt appears to have changed around the dates corresponding to the Fed’s announcement of the Primary Dealer Credit Facility (March 17) and the Primary and Secondary Market Corporate Credit Facilities (March 23) (Kargar et al. 2020, 16) (see Figure 4). O’Hara and Zhou (2021) found that almost immediately after the announcement of the PDCF, dealers reverted to accumulating inventories, and transaction costs for investment-grade securities fell, even for large trading quantities (“block trades”) which become very expensive in illiquid markets (O’Hara and Zhou 2020; Martin and McLaughlin 2020).

Figure 4: Change in Dealer Inventory of Corporate Debt

Source: Kargar et al. 2020.

Nevertheless, standing facilities can be subject to stigma, which market participants speculate may have limited the effectiveness of the PDCF (Ennis and Price 2020; Armantier, Lee, and Sarkar 2015).

Key Design Decisions

Purpose

1

On March 17, 2020, the Fed announced that it had authorized the Federal Reserve Bank of New York (FRBNY) to extend collateralized credit to primary dealers for a term of up to 90 days (FRB 2020m). The stated purpose of the PDCF was to support the credit needs of American households and businesses by fostering the functioning of financial markets more generally and to expand the ability of primary dealers to gain access to term funding (FRB 2020i).

Specifically, by allowing primary dealers to borrow against a variety of assets on their balance sheets, the PDCF intended to reduce the costs associated with holding inventory and intermediating transactions between customers (Kargar et al. 2020; FRB 2020b). The Fed expected the PDCF would add liquidity to the market for US Treasuries in particular, as unprecedented sales volumes in March overwhelmed the capacity of dealers to intermediate in that market (FRB 2020b).

Part of a Package

1

The PDCF worked in concert with other backstop facilities designed to provide targeted liquidity to specific financial entities; namely, the Commercial Paper Funding Facility (CPFF), announced several hours before the PDCF, and the Money Market Mutual Fund Liquidity Facility (MMLF), announced on March 18 (Boyarchenko, Kovner, and Shachar 2020; FSB 2020). The Fed also intervened in the dealer-intermediated secondary market for corporate bonds through the Secondary Market Corporate Credit Facility (SMCCF) (FSB 2020; Kargar et al. 2020).

Legal Authority

1

The Federal Reserve Board authorized the PDCF by invoking its authority under Section 13(3) of the Federal Reserve Act (FRB 2020m). Section 13(3) of the Federal Reserve Act permits the Fed, in “unusual and exigent circumstances,” to “discount for any participant in any program or facility with broad-based eligibility” (FRB 2017, Sec. 13(3)(a)). The invocation of Section 13(3) allows the Fed to provide liquidity more broadly than its monetary policy and discount window authorities allow. Under Section 13(3), the Fed could extend collateralized credit to primary dealers (FRB 2020m). The PDCF received the unanimous approval of the five members of the Fed Board of Governors and the treasury secretaryFThe Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 required Treasury pre-approval for the establishment of programs like the PDCF; this stipulation did not exist for the GFC-era PDCF (CRS 2020). (FRB 2020m; Mnuchin 2020).

The PDCF was based on counterparty relationships already in place between primary dealers and the New York Fed because of the latter’s role in conducting open market operations (OMOs) (FRBNY, n.d.b).

Governance

1

Pursuant to Section 13(3) of the Federal Reserve Act, the Fed submitted reports to Congress every 30 days including “the [aggregate] value of collateral, the amount of fees and other items of value received; and the expected or final cost to the taxpayer” (FRB 2020e, 29–30). The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) required the Board to publish these reports on its website within seven days of them being submitted to Congress; although the PDCF was not funded by the CARES Act, the Board published the relevant reports anyway (FRB 2020e).

The Government Accountability Office (GAO) published a report examining the Fed’s overall response to the COVID-19 pandemic, as well as two reports on the Fed’s emergency lending facilities. The reports did not include recommendations specific to the PDCF (GAO 2020a).

Reserve Bank Operations and Payment Systems (RBOPS), a division of the Federal Reserve Board that oversees the policies and operations of the Reserve Banks, conducted a three-phase review of Fed facilities (GAO 2020b). In the first phase, RBOPS assisted with the launch of the facility (GAO 2020b). In the second phase, conducted no later than 45 days after the Board authorized the facility, RBOPS focused its oversight of each facility on four areas: (1) compliance, governance, and risk management; (2) credit and collateral; (3) processes and controls; and (4) accounting and reporting (GAO 2020b). The third phase of RBOPS’s review consisted of monitoring the Fed’s facilities (GAO 2020b). RBOPS communicated any control or design gaps it identified, as well as recommendations for remediation, to Reserve Bank management (GAO 2020b). RBOPS identified unspecified gaps in the design of controls for the PDCF (GAO 2020b).

Administration

1

The Federal Reserve Bank of New York (FRBNY) administered the PDCF. FRBNY was uniquely positioned to operate the PDCF because the facility relies on the relationships and infrastructure built for its dealer trading counterparties who assist the FOMC in implementing monetary policy (FRBNY, n.d.b). FRBNY also administered the GFC-era PDCF with operational assistance from the Federal Reserve Banks of Atlanta and Chicago (GAO 2011).

Dealers typically fund themselves in the tri-party repo market which involves a clearing bank that acts as an intermediary and handles the administrative details between the two partiesFFor a full discussion of the tri-party repo market, see Copeland, et al. (2012). For more information on the role clearing banks play in tri-party repo, see Paddrik et al (2021) and Kahn and Olson (2021). (Duffie 2020; Paddrik, Ramírez, and McCormick 2021). For the PDCF, Bank of New York Mellon (BNYM) executed the custody and arrangement of funding on behalf of the New York Fed (FRBNY 2020b). In 2019 BNYM became the predominant clearing bank in the tri-party repo market for US government securities, providing much of the collateral valuation, margining, management services, transaction settlement, and custodial services (Paddrik, Ramírez, and McCormick 2021).

Communication

1

The Fed established the PDCF to provide primary dealers with access to term funding as part of a larger effort to support financial market functioning and the credit needs of US households and businesses more broadly (FRB 2020m). Throughout the duration of the facility, the Fed reiterated the role of the PDCF in helping dealers resume their market intermediation and smooth market functioning (Martin and McLaughlin 2020; FRB 2020k; FRB 2020l).

Similarly, the Fed created the 2008 PDCF to provide liquidity to primary dealers when troubles at Bear Stearns negatively affected the market for triparty repurchase agreements (Yang 2020; Martin and McLaughlin 2020).

The Fed made regular press releases accompanying decisions on the terms and rules related to the PDCF.

Disclosure

1

Section 13(3), as amended by the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank Act), requires the Fed to present Congress with two types of reports: 1) one submitted within a week after authorizing any loan, providing the justification for the exercise and detailed information on the recipients and the amounts of each transaction; and 2) a monthly update “regarding the value of collateral, the amount of fees and other items of value received; and the expected or final cost to the taxpayer” (FRB 2017). In compliance with the second type of required report, the Fed provided monthly reports to Congress with details on the PDCF including the aggregate amounts borrowed, interest rate charged, and value of pledged collateral, as well as the overall costs, revenues, and fees (FRB 2020i). These reports included more detailed aggregate data on the PDCF’s outstanding loans than were included in the Fed’s weekly release of its balance sheet data (FRB 2020c).

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) required the Fed to publish monthly reports to the public about programs supported by CARES Act funds within seven days of delivering them to Congress (116th US Congress 2020). Although the PDCF was not supported by CARES Act funds, the Fed released the required congressional PDCF reports to the public anyway (FRB 2020e).

The Fed did not publicly disclose disaggregated details about PDCF transactions, unlike some of the other emergency lending facilitiesFSee the Main Street Lending Programs by Kelly (2021) and the Primary Market Corporate Credit Facility and Secondary Market Corporate Credit Facility by Leonard (2021). (FRB 2020f). As allowed in the Dodd-Frank Act, the Fed chair requested a delay in the release of confidential treatment of borrower-identifying information for the PDCF, MMLF, and CPFF to avoid adversely affecting these facilities’ participants (GAO 2020b). The Fed was cognizant of the possibility that market participants would view a firm’s use of these facilities as a sign of liquidity stress, which could cause a run on the institution (GAO 2020b). However, Section 11(s) of the Federal Reserve Act, as amended by the Dodd-Frank Act, requires the Fed to disclose detailed transaction-level data within one year after the termination date of any credit facility; for the PDCF, this deadline was March 31, 2022 (FRB 2020j, 12; FRB, n.d.a, sec. 11[s][2][A]).

SPV Involvement

1

The PDCF was not operated through an SPV.

Program Size

1

The amount of funding that any primary dealer could borrow under the PDCF was limited only by the amount of margin-adjusted eligible collateral that a primary dealer could present to the clearing bank (FRB 2020n).

Use of the PDCF peaked at $35.6 billion the week of April 15 (FRB 2020q). For context, broker-dealers held about $3.5 trillion in assets in Q4 2019 (FRB 2020b). As of August 2021, primary dealers funded an average of $600 billion in daily trade volume while non-primary dealers funded $71 billion (Paddrik, Ramírez, and McCormick 2021).

Source(s) of Funding

1

The PDCF functioned as a loan facility for primary dealers, similar to the way the Federal Reserve’s discount window provides a backup source of funding to depository institutions. Credit extended by the Federal Reserve through the PDCF was collateralized (FRBNY 2020c).

The Fed recorded PDCF loans as assets on its balance sheet (Hoops and Kurtzman 2021). As dealers paid back loans, the Fed extinguished the reserves (FRB 2020c).

Eligible Institutions

1

The PDCF utilized the New York Fed’s existing operational relationships with primary dealers and the tri-party repo system that is used for OMOs. Primary dealers are trading counterparties of the New York Fed in its implementation of monetary policy. The PDCF extended 356 individual loans to 21 primary dealers (see Figure 5) (FRB 2022).

Figure 5: Cumulative Loan Amounts Extended to PDCF Borrowers

|

Borrower |

Cumulative Loan Amount ($thousands) |

Loans Extended |

|

Amherst Pierpont Securities LLC |

418,500 |

86 |

|

Bank of Nova Scotia, New York Agency |

70,000 |

3 |

|

Barclays Capital Inc. |

3,361,000 |

11 |

|

BMO Capital Markets Corp. |

2,833,000 |

8 |

|

BNP Paribas Securities Corp. |

14,400,000 |

7 |

|

BofA Securities, Inc. |

50 |

1 |

|

Cantor Fitzgerald & Co. |

4,500,000 |

74 |

|

Citigroup Global Markets Inc. |

6,500,000 |

5 |

|

Deutsche Bank Securities Inc. |

11,189,187 |

51 |

|

Goldman Sachs & Co. LLC |

4,700,000 |

3 |

|

J.P. Morgan Securities LLC |

60,350,000 |

29 |

|

Jefferies LLC |

767,706 |

19 |

|

Mizuho Securities USA LLC |

250,000 |

1 |

|

Morgan Stanley & Co. LLC |

500,000 |

1 |

|

NatWest Markets Securities Inc. |

570,000 |

3 |

|

Nomura Securities International, Inc. |

2,335,000 |

15 |

|

RBC Capital Markets, LLC |

8,168,000 |

7 |

|

Société Générale, New York Branch |

51,000 |

2 |

|

TD Securities (USA) LLC |

4,550,000 |

6 |

|

UBS Securities LLC |

3,412,000 |

20 |

|

Wells Fargo Securities, LLC |

3,775,000 |

4 |

|

Total |

132,700,443 |

356 |

Source: FRB 2022.

Securities dealers play a critical role in short-term markets by marketing, underwriting, and transacting in a range of securities; using their balance sheets to make markets; and providing liquidity by buying and selling securities from their own holdings (FRB 2020b). Large dealers, most of whom are subsidiaries of bank holding companies,FBecause dealer subsidiaries are just one business line to which large banks allocate capital, liquidity, and risk, dealers were further constrained in March 2020 by demands to hold greater margin collateral, loan requests from bank customers, and requests for heightened levels of intermediation in other assets (Duffie 2020). use short-term secured funding markets to fund their inventory of securitiesFDealers also source funding from banks and other dealers (FRB 2020b). (FRB 2020b). Primary dealers are heavily reliant on short-term lending markets in their role as securities market makers, but, unlike banks, cannot access the discount window (FRBNY 2020b).

Use of the GFC-era PDCF was restricted to the 20 primary dealers at the time, but included the London-based affiliates of four primary dealers. Ultimately, 18 primary dealers tapped the 2008 PDCF (Yang 2020).

Auction or Standing Facility

1

The PDCF was a standing facility (FRB 2020j). Under the PDCF, dealers contacted BNYM with their funding needs, normally by 2:00pm ET, and BNYM would verify that eligible collateral had been pledged. BNYM then notified FRBNY when a sufficient amount of eligible, margin-adjusted collateral had been assigned to FRBNY’s tri-party account, at which point FRBNY transferred the amount of the loan to BNYM for credit to the primary dealer, normally around 5:00pm ET on the same day (FRB 2020n).

Loan or Purchase

1

The extension of credit under the PDCF depended on the New York Fed’s relationships and processes established as part of the primary dealer system. To mitigate risk, the Fed applied haircuts and had a clearing bank value the collateral at the least available value and revalue it daily (FRBNY 2020b). Loans to primary dealers under the PDCF were made “with recourse beyond the collateral to the broker-dealer entity itself,” assuring the Fed’s protection in the event of a borrower default (FRBNY 2020b). Dealers were permitted to prepay PDCF loans (FRBNY 2020b).

Eligible Collateral or Assets

1

The PDCF accepted all collateral eligible for OMOs: US Treasury, agency, and agency mortgage-backed securities (FRBNY 2020b). The PDCF also accepted non-OMO-eligible collateral, including equity securities, money market instruments, and investment-grade municipal and corporate securities (see Figures 6 and 7) (FRBNY 2020c).

Figure 6: Securities Pledged to the PDCF, by Type

Source: FRB 2022.

Source: FRB 2022.

In March 2020, high demand for liquidity and unusual selling pressure caused dislocations in the US Treasuries market, which is critical to overall financial market functioning and the transmission of monetary policy (TIC 2021; He, Nagel, and Song 2020; Brainard 2018). Primary dealers also act as market markers for other fixed-income securities, equity securities, and other securities in markets that experienced dislocations. The terms of the PDCF were designed to accommodate this variety, accepting investment-grade corporate debt securities, international agency securities, commercial paper, municipal securities, mortgage-backed securities, asset-backed securities, and equity securities (excluding ETFs, unit investment trusts, mutual funds, rights, and warrants) (FRBNY 2020c). Only US-dollar denominated collateral was accepted (FRB 2020n). Unlike the discount window, the PDCF accepted equity securities as collateral for loans and did not accept foreign-exchange denominated assets or whole loans (FRBNY 2020b; FRB 2021b). In addition, credit under the PDCF was extended in the form of a repurchase agreement transaction (FRBNY 2020b).

Figure 7: Securities Ratings

Source: FRB 2022.

Source: FRB 2022.

Obligations issued by the borrower or its affiliates were not eligible (FRBNY 2020b). Most of the assets financed in the PDCF were experiencing volatility and pressure in March 2020, including corporate and municipal debt, asset-backed securities, and commercial paper (Martin and McLaughlin 2020).

The 2008 PDCF defined “eligible collateral” as all collateral eligible for pledge under tri-party repurchase agreements. As a result, the 2008 program included some noninvestment-grade securities and whole loans that the 2020 PDCF did not accept (Yang 2020).

Loan Amounts (or Purchase Price)

1

FRBNY extended a principal amount equal to the value of the collateral pledged to secure the advance less a risk-adjusted haircut; there were no other restrictions on primary dealers’ use of the facility (FRB 2020j). In the event collateral was downgraded, the primary dealer would need to replace the security with eligible collateral to maintain full collateralization or terminate the loan (FRBNY 2020b).

Haircuts

1

Haircuts assigned to OMO-eligible collateral were equivalent to haircuts under open market operations (FRBNY 2020c). For collateral not eligible for OMO, haircuts were assigned according to the asset’s risk (FRBNY 2020c). BNYM valued the collateral according to a collateral schedule sent from FRBNY to primary dealers and BNYM (see Appendix); this was designed to be similar to the margin schedule for lending to commercial banks at the discount windowFFor most eligible collateral, the haircut applied at the PDCF aligns to the haircut applied to the longest-dated tenor of that collateral type at the discount window (FRB 2021b; FRBNY 2020c). (FRB 2020n). The Fed stated that the collateral schedule could be adjusted “as conditions warrant and upon further analysis” (FRBNY 2020b).

The 2008 PDCF also assigned haircuts to OMO-eligible collateral that were equivalent to haircuts under the OMOs. Haircuts for non-OMO eligible collateral were determined by the asset’s risk and generally higher than under OMO standards (Yang 2020).

Interest Rate

1

The interest rate for the loan was based on the primary credit (discount window) rate offered to depository institutions at the time the loan was originated. On March 15, the Fed announced it would lower the primary credit rate by 50 basis points to 25 basis points (the upper bound of the federal funds rate). Reducing the spread between the primary credit rate and the general level of overnight interest rates was intended “to help encourage more active use of the window by depository institutions to meet unexpected funding needs” (FRB 2020o; FRB 2020a). From the facility’s launch in March 2020 to its expiration a year later, the primary credit rate remained at 25 basis points (FRB 2020n).

Under normal conditions, the primary credit rate exceeds the overnight repo rate for most eligible securities (FRBNY, n.d.a). As a result, the PDCF was not an especially attractive means of financing an inventory of securities in normal market conditions (GAO 2020b). The Fed set the rate for the PDCF according to the principles of penalty rates in Regulation AFThe 2015 amendment to Regulation A calls for the Fed to charge a “penalty rate” on all lending through 13(3) emergency lending facilities (FRB 2015).; namely, that the rate “is a premium to the market rate in normal circumstances” but “affords liquidity in unusual and exigent circumstances” (FRB 2015; 12 CFR, n.d.; GAO 2020b, 12; COC 2020, 33). Fed officials told the Government Accountability Office that charging such a rate ensured “the facilities would experience limited participation when credit is available in the marketplace and increased participation when markets declined and there was a shortage of credit” (GAO 2020b, 12). The PDCF was designed to be self-liquidating, meaning dealers were incentivized to use the PDCF only as a backstop, not as a primary funding source once markets returned to normal (GAO 2020b).

The GFC-era PDCF also charged the primary credit rate; throughout the duration of the facility this represented a 25 basis point premium to the upper limit of the fed funds rate (Yang 2020, 13).

Fees

1

The PDCF did not charge borrowers a frequency-based fee, but primary dealers did pay normal tri-party fees to BNYM (FRBNY 2020b).

In contrast, the GFC-era PDCF charged a frequency-based penalty fee on primary dealers that accessed the facility on more than 30 days out of any 120 days. The fee was later revised based on use of the facility for more than 45 business days out of the preceding 180 business days (Yang 2020).

Term

1

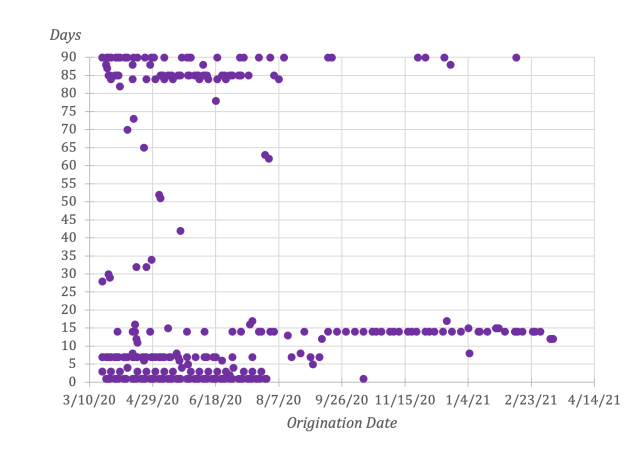

The PDCF offered credit for up to a 90-day term. This brought the facility’s terms in line with changes to the discount window, which, as of March 15, 2020, also allowed depository institutions to obtain secured liquidity for up to 90 days (FRBNY 2020b; FRB 2020a). The median term of the borrowing of the COVID-era PDCF was 14 days, and most borrowing was longer than overnight (see Figure 8) (FRB 2022; Martin and McLaughlin 2020). As the remaining maturity of the loan declined, the primary dealer could choose to prepay the loan and request a new loan up to 90 days (FRBNY 2020b).

The GFC-era PDCF only offered overnight loans (Yang 2020).

Figure 8: Duration of PDCF Loans by Origination Date

Source: FRB 2022.

Other Conditions

1

There were no other restrictions on PDCF participants.

Regulatory Relief

1

Although the Fed and other financial regulators provided relief from regulation around this time, no regulatory changes were made to specifically accommodate participants in the PDCF.

International Cooperation

1

The Fed did not coordinate with other jurisdictions when designing or operating the PDCF.

Duration

1

The PDCF began extending credit on March 20, 2020, and was designed to continue for “at least six months, or longer if conditions warrant” (FRBNY 2020b). On July 28, the Fed announced that it would extend several 13(3) emergency lending facilities, including the PDCF, through December 31, 2020 (FRB 2020k). On November 30, the Fed announced a further extension of the PDCF to March 31, 2021, along with three other 13(3) programs: the Commercial Paper Funding Facility (CPFF), the Money Market Mutual Fund Liquidity Facility (MMLF), and the Paycheck Protection Program Liquidity Facility (PPPLF) (FRB 2020l). When announcing both extensions, the Fed acknowledged that “financial markets have stabilized significantly,” but pointed to “the presence and extent of volatility and illiquidity in financial markets” and “the price and availability of credit in the market . . . as compared to normal market conditions” as justification for their continued operations (FRB 2020d; FRB 2020g).

The PDCF, along with the CPFF and MMLF, expired on March 31, 2021, while the Fed continued to invoke its 13(3) authorities to operate the PPPLF. All loans made by FRBNY through the PDCF were repaid by April 30, 2021 (FRB 2021a).

Key Program Documents

-

(FRB 2020j) Federal Reserve Board (FRB). May 26, 2020. “Money Market Mutual Fund Liquidity Facility FAQs.”

FAQs for the MMLF.

-

(FRB 2020n) Federal Reserve Board of Governors (FRB). March 17, 2020. “Term Sheet for Primary Dealer Credit Facility (PDCF).”

General term sheet for the 2020 PDCF.

-

(FRB 2020q) Federal Reserve Board of Governors (FRB). April 16, 2020. “FRB: H.4.1 Release—Factors Affecting Reserve Balances—April 16, 2020.”

Weekly release detailing Fed balance sheet.

-

(FRBNY 2016) Federal Reserve Bank of New York (FRBNY). November 9, 2016. “Policy on Counterparties for Market Operations.”

FRBNY policy outlining eligible counterparties and requirements for market operations.

-

(FRBNY 2020b) Federal Reserve Bank of New York (FRBNY). March 17, 2020. “FAQs: Primary Dealer Credit Facility.”

FAQs for the 2020 PDCF.

-

(FRBNY 2020c) Federal Reserve Bank of New York (FRBNY). April 9, 2020. “Primary Dealer Credit Facility: Collateral Schedule.”

List of securities eligible for the PDCF.

-

(FRBNY, n.d.a) Federal Reserve Bank of New York (FRBNY). No date. “Markets Data Dashboard.” Accessed October 19, 2021.

Dashboard displaying FRBNY’s markets data.

-

(FRBNY, n.d.b) Federal Reserve Bank of New York. No date. “Primary Dealers – Current List, Expectations, and Eligibility.” Accessed August 30, 2021.

List of primary dealers.

-

(TIC 2021) U.S. Department of the Treasury (TIC). June 2021. “Net Purchases of U.S. Treasury Bonds & Notes by Major Foreign Sector.”

Treasury International capital flows data.

-

(12 CFR, n.d.) Federal Reserve Board of Governors (12 CFR). No date. “12 CFR § 201.4 - Availability and Terms of Credit.” Cornell Law School. Accessed August 9, 2021.

Code of Federal Regulations section describing regulations for emergency lending.

-

(116th US Congress 2020) 116th US Congress. March 27, 2020. Public Law 116-136: The Coronavirus Aid, Relief, and Economic Security Act (The “CARES Act”). 116-136.

Economic stimulus bill passed in response to the COVID-19 pandemic.

-

(FRB 2017) Board of Governors of the Federal Reserve System (FRB). February 13, 2017. Federal Reserve Act, Section 13. Power of Federal Reserve Banks.

Excerpt from the Federal Reserve Act describing the powers of the Federal Reserve Banks.

-

(FRB, n.d.a) Federal Reserve Board of Governors (FRB). No date. “Section 11 of the Federal Reserve Act.” Federal Reserve Board of Governors.

Section of the Federal Reserve Act including disclosure requirements.

-

(FRB, n.d.b) Federal Reserve Board of Governors (FRB). No date. 12 CFR § 201.4 Availability and Terms of Credit. Accessed August 27, 2021.

Extensions of credit by Federal Reserve Banks (Regulation A).

-

(FRB 2015) Federal Reserve Board of Governors (FRB). November 30, 2015. “Federal Reserve Board Approves Final Rule Specifying Its Procedures for Emergency Lending under Section 13(3) of the Federal Reserve Act.” Board of Governors of the Federal Reserve System.

Final rule specifying the Fed’s procedures for emergency lending under Section 13(3) of the Federal Reserve Act.

-

(FRB 2020h) Board of Governors of the Federal Reserve System (FRB). April 1, 2020. “Regulatory Capital Rule: Temporary Exclusion of U.S. Treasury Securities and Deposits at Federal Reserve Banks from the Supplementary Leverage Ratio,” April, 35.

Rule allowing banks to exclude US Treasuries and deposits from a regulatory capital ratio.

-

(Timiraos and Verlaine 2020) Nick Timiraos and Julia-Ambra Verlaine. March 13, 2020. “Federal Reserve Accelerates Treasury Purchases to Address Market Strains.” Wall Street Journal, sec. Markets.

WSJ article noting the Fed’s increased purchases of US Treasuries in response to the COVID-19 pandemic.

-

(Brainard 2018) Lael Brainard. December 3, 2018. “Speech by Governor Brainard on the Structure of the Treasury Market.” Board of Governors of the Federal Reserve System.

Speech by Federal Reserve Governor on the structure and functioning of the market for US Treasuries.

-

(FRB 2020a) Federal Reserve Board of Governors (FRB). March 15, 2020. “Federal Reserve Actions to Support the Flow of Credit to Households and Businesses.” Federal Reserve Board.

Press release describing Federal Reserve actions in response to the COVID-19 pandemic.

-

(FRB 2020k) Federal Reserve Board (FRB). July 28, 2020. “Federal Reserve Board Announces an Extension through December 31 of Its Lending Facilities That Were Scheduled to Expire on or around September 30.”

Press release announcing an extension to several Fed facilities through the end of 2020.

-

(FRB 2020l) Federal Reserve Board (FRB). November 30, 2020. “Federal Reserve Board announces extension through March 31, 2021, for several of its lending facilities that were generally scheduled to expire on or around December 31.” Board of Governors of the Federal Reserve System.

Press release announcing an extension of several Fed facilities beyond the end of 2022.

-

(FRB 2020m) Federal Reserve Board of Governors (FRB). March 17, 2020. “Federal Reserve Board announces establishment of a Primary Dealer Credit Facility (PDCF) to support the credit needs of households and businesses.” Board of Governors of the Federal Reserve System.

Announcement of PDCF.

-

(FRB 2020o) Federal Reserve Board of Governors (FRB). March 21, 2020. “Actions of the Board, Its Staff, and the Federal Reserve Banks; Applications and Reports Received, No. 12, March 21, 2020.”

H.2 release of Board of Governors deliberations.

-

(FRB 2022) Federal Reserve Board of Governors (FRB). March 31, 2022. “Disclosures Regarding the Emergency Lending Response to COVID-19, Pursuant to Section 11(s) of the Federal Reserve Act.”

Borrower data for the PDCF and other COVID-era Fed facilities.

-

(FRBNY 2020a) Federal Reserve Bank of New York (FRBNY). March 12, 2020. “Statement Regarding Treasury Reserve Management Purchases and Repurchase Operations.”

Press release announcing adjustments to repo operation schedules to address temporary disruptions in Treasury financing markets.

-

(Mnuchin 2020) Mnuchin, Steven T. March 17, 2020. “Statement from Secretary Steven T. Mnuchin on the Establishment of a Primary Dealer Credit Facility.” U.S. Department of the Treasury.

Statement from US Treasury Secretary Steven T. Mnuchin announcing the establishment of the PDCF.

-

(Steven Mnuchin 2020) Steven Mnuchin. July 28, 2020. “Statement from Secretary Steven T. Mnuchin on the Extension of Facilities Authorized Under Section 13(3) of the Federal Reserve Act.” U.S. Department of the Treasury.

Statement from US Treasury Secretary Steven T. Mnuchin announcing the extension of the PDCF.

-

(COC 2020) Congressional Oversight Commission (COC). October 15, 2020. “The Fifth Report of the Congressional Oversight Commission.”

Official government oversight report detailing the findings of the COC regarding lending facilities established under the CARES Act.

-

(CRS 2020) Congressional Research Service, Marc (CRS). March 27, 2020. “Federal Reserve: Emergency Lending (Updated March 27, 2020),” March, 40.

Official government report assessing early actions taken in response to COVID-19 in the context of lessons learned from 2008.

-

(FRB 2020b) Board of Governors of the Federal Reserve System (FRB). May 2020. “Financial Stability Report (May 2020).” Financial Stability Report.

Official government assessment describing early evaluations of the monetary policy actions taken and facilities established in response to COVID-19.

-

(FRB 2021a) Board of Governors of the Federal Reserve System (FRB). May 9, 2021. “Periodic Report: Update on Outstanding Lending Facilities Authorized by the Board under Section 13(3) of the Federal Reserve Act (May 9, 2021).” Yale Program on Financial Stability Resource Library.

Official government report summarizing the updated usage of the emergency lending facilities established in response to the COVID-19 pandemic.

-

(FRB 2021b) Federal Reserve Board (FRB). July 1, 2021. “Discount Window Margins and Collateral Guidelines.”

Federal Reserve website listing discount window collateral information.

-

(FRB 2020c) Federal Reserve Board of Governors (FRB). April 9, 2020. “FRB: H.4.1 Release—Factors Affecting Reserve Balances—April 9, 2020.” H.4.1.

Weekly release detailing Fed balance sheet.

-

(FRB 2020d) Federal Reserve Board of Governors (FRB). July 31, 2020. “Periodic Report: Update on Outstanding Lending Facilities Authorized by the Board under Section 13(3) of the Federal Reserve Act (July 31, 2020).”

Official government report summarizing the updated usage of the emergency lending facilities established in response to the COVID-19 pandemic.

-

(FRB 2020e) Federal Reserve Board of Governors (FRB). August 2020. “Report on the Federal Reserve’s Balance Sheet (August 2020).”

Fed report summarizing operational developments for each of the COVID-19 Section 13(3) lending facilities.

-

(FRB 2020f) Federal Reserve Board of Governors (FRB). October 7, 2020. “Periodic Report: Update on Outstanding Lending Facilities Authorized by the Board under Section 13(3) of the Federal Reserve Act (October 7, 2020).”

Official government report summarizing the updated usage of the emergency lending facilities established in response to the COVID-19 pandemic.

-

(FRB 2020g) Federal Reserve Board of Governors (FRB). December 3, 2020. “Periodic Report: Update on Outstanding Lending Facilities Authorized by the Board under Section 13(3) of the Federal Reserve Act (December 3, 2020).”

Official government report summarizing the updated usage of the emergency lending facilities established in response to the COVID-19 pandemic.

-

(FRB 2020i) Federal Reserve Board (FRB). March 18, 2020. “Periodic Report: Update on Outstanding Lending Facilities Authorized by the Board under Section 13(3) of the Federal Reserve Act (March 25, 2020).”

Official government report summarizing the updated usage of the emergency lending facilities established in response to the COVID-19 pandemic.

-

(FRB 2020p) Federal Reserve Board of Governors (FRB). March 25, 2020. “Report to Congress Pursuant to Section 13(3) of the Federal Reserve Act: Primary Dealer Credit Facility.”

Official government report summarizing the updated usage of the emergency lending facilities established in response to the COVID-19 pandemic; excerpt of the PDCF.

-

(FSB 2020) Financial Stability Board (FSB). November 17, 2020. “Holistic Review of the March Market Turmoil.”

Report on the effect of the COVID-19 pandemic on global markets.

-

(GAO 2011) Government Accountability Office (GAO). October 4, 2011. “Federal Reserve System: Opportunities Exist to Strengthen Policies and Processes for Managing Emergency Assistance.” GAO-12-122T.

GAO report detailing the design and oversight of the Federal Reserve’s 13(3) facilities and recommending improvements.

-

(GAO 2020a) Government Accountability Office (GAO). November 30, 2020. “Urgent Actions Needed to Better Ensure an Effective Federal Response.” GAO-21-191. COVID-19.

GAO report containing recommendation that Fed strengthen procedures for lending to high-risk borrowers.

-

(GAO 2020b) Government Accountability Office (GAO). December 10, 2020. “Use of CARES Act-Supported Programs Has Been Limited and Flow of Credit Has Generally Improved.” Federal Reserve Lending Programs GAO-21-180. Report to Congressional Committees.

Government oversight report discussing Federal Reserve emergency lending facilities.

-

(Armantier, Lee, and Sarkar 2015) Armantier, Olivier, Helene Lee, and Asani Sarkar. August 10, 2015. “History of Discount Window Stigma.” Liberty Street Economics (blog).

Blogpost examining the history of discount window stigma.

-

(Boyarchenko, Kovner, and Shachar 2020) Boyarchenko, Nina, Anna Kovner, and Or Shachar. July 2020. “It’s What You Say and What You Buy: A Holistic Evaluation of the Corporate Credit Facilities.” 935. Staff Reports.

Staff report on the CCFs.

-

(Carlson and Macchiavelli 2021) Carlson, Mark, and Marco Macchiavelli. June 21, 2021. “Primary Markets for Short-Term Debt and the Stabilizing Effects of the PDCF.”

FED Notes examining the effect of the 2020 PDCF on dealer-intermediated markets.

-

(Chen, Liu, Rubio, Sarkard, and Song 2021) Chen, Jiakai, Haoyang Liu, David Rubio, Asani Sarkard, and Zhaogang Song. March 24, 2021. “Did Dealers Fail to Make Markets during the Pandemic?” Liberty Street Economics (blog).

Blogpost examining the liquidity provided by dealers in several important financial markets during the COVID-19 pandemic.

-

(Clarida, Duygan-Bump, and Scotti 2021) Clarida, Richard H, Burcu Duygan-Bump, and Chiara Scotti. June 3, 2021. “The COVID-19 Crisis and the Federal Reserve’s Policy Response,” June.

Academic paper surveying the Fed’s emergency response to the COVID-19 crisis, and the impact of novel facilities on the flow of credit.

-

(Duffie 2020) Duffie, Darrell. June 2020. “Still the World’s Safe Haven? Redesigning the US Treasury Market After the COVID-19 Crisis.” Working Paper #62.

Policy paper analyzing dislocations in the US Treasury market during the COVID-19 pandemic, and considering possible improvements to the market.

-

(Ennis and Price 2020) Ennis, Huberto M, and David A Price. April 2020. “Understanding Discount Window Stigma.” Federal Reserve Bank of Richmond Economic Brief, no. No. 20-04 (April): 5.

Summary overview of discount window stigma.

-

(FRB Minneapolis 1988) Federal Reserve Bank of Minneapolis (FRB Minneapolis). August 1, 1988. “Discovering Open Market Operations.”

A history of open market operations.

-

(FRB and Goldberg 2020) Federal Reserve Board of Governors, and Jonathan Goldberg (FRB and Goldberg). July 17, 2020. “Dealer Inventory Constraints during the COVID-19 Pandemic: Evidence from the Treasury Market and Broader Implications.” FEDS Notes 2020 (2581).

Paper analyzing strains in the Treasury market amid a decline in broker-dealer inventory capacity during the COVID-19 pandemic.

-

(He, Nagel, and Song 2020) He, Zhiguo, Stefan Nagel, and Zhaogang Song. June 2020. “Treasury Inconvenience Yields during the COVID-19 Crisis.” National Bureau of Economic Research Working Paper Series, June, 62.

NBER paper analyzing Treasury yields during the COVID-19 pandemic.

-

(Hoops and Kurtzman 2021) Matthew Hoops, and Robert Kurtzman. July 30, 2021. “Accounting for COVID-19 Related Funding, Credit, Liquidity, and Loan Facilities in the Financial Accounts of the United States.” Board of Governors. Yale Program on Financial Stability Resource Library.

FEDS Note summarizing technical details on how the Fed’s emergency facilities were accounted for in the Financial Accounts of the United States.

-

(Kargar, Lester, Lindsay, Liu, Weill, and Zúñiga 2020) Kargar, Mahyar, Benjamin Lester, David Lindsay, Shuo Liu, Pierre-Oliver Weill, and Diego Zúñiga. 2020. “Corporate Bond Liquidity During the COVID-19 Crisis.” NBER Working Paper 27355.

Academic paper describing corporate bond liquidity throughout the COVID-19 crisis.

-

(O’Hara and Zhou 2020) O’Hara, Maureen, and Xing (Alex) Zhou. August 2020. “Anatomy of a Liquidity Crisis: Corporate Bonds in the COVID-19 Crisis.” SSRN Electronic Journal, August.

Academic paper detailing corporate bond reaction to COVID-19 shock.

-

(Paddrik, Ramírez, and McCormick 2021) Paddrik, Mark E., Carlos A. Ramírez, and Matthew J. McCormick. August 2, 2021. “The Dynamics of the U.S. Overnight Triparty Repo Market.”

Overview of the US overnight triparty market.

-

(Pozsar 2020) Pozsar, Zoltan. April 14, 2020. “Global Money Notes #29 – U.S. Dollar Libor and War Finance.”

Commentary from market participant on the efficacy of the PDCF.

-

(Yang 2020) Yang, Karen. October 10, 2020. “The Primary Dealer Credit Facility (PDCF) (US GFC),” October.

YPFS case study on the Fed’s 2008 PDCF established in response to the GFC.

Primary Dealer Credit Facility Collateral Schedule

Note: Margin percentages are calculated by dividing the value of the collateral pledged by the loan amount. REMICS refers to Real Estate Mortgage Investment Conduits. CMO refers to Collateralized Mortgage Obligations. CMBS refers to Commercial Mortgage-Backed Securities. *Direct obligations of the following federally related entities: Federal Agricultural Mortgage Corporation (Farmer Mac); Federal Farm Credit Banks Funding Corporation (Farm Credit System); Federal Home Loan Bank System; Federal Home Loan Mortgage Corporation (Freddie Mac); Federal National Mortgage Association (Fannie Mae); Financing Corporation (FICO); Resolution Funding Corporation (REFCO); Small Business Administration (SBA); Student Loan Marketing Association (SLMA); or Tennessee Valley Authority. **Excludes trust receipts. Agency refers to securities issued and/or fully guaranteed by the Government National Mortgage Association, Federal Home Loan Mortgage Corporation, Federal National Mortgage Association, or Farmers Agricultural Mortgage Corporation.

Note: Margin percentages are calculated by dividing the value of the collateral pledged by the loan amount. REMICS refers to Real Estate Mortgage Investment Conduits. CMO refers to Collateralized Mortgage Obligations. CMBS refers to Commercial Mortgage-Backed Securities. *Direct obligations of the following federally related entities: Federal Agricultural Mortgage Corporation (Farmer Mac); Federal Farm Credit Banks Funding Corporation (Farm Credit System); Federal Home Loan Bank System; Federal Home Loan Mortgage Corporation (Freddie Mac); Federal National Mortgage Association (Fannie Mae); Financing Corporation (FICO); Resolution Funding Corporation (REFCO); Small Business Administration (SBA); Student Loan Marketing Association (SLMA); or Tennessee Valley Authority. **Excludes trust receipts. Agency refers to securities issued and/or fully guaranteed by the Government National Mortgage Association, Federal Home Loan Mortgage Corporation, Federal National Mortgage Association, or Farmers Agricultural Mortgage Corporation.

Source: FRBNY 2020c.

Taxonomy

Intervention Categories:

- Market Support Programs

Countries and Regions:

- United States

Crises:

- COVID-19