Bank Holidays & Fund Suspensions

United States: National Bank Holiday, 1933

Purpose

To provide “a period of respite . . . with a view to preventing further hoarding of coin, bullion or currency or speculation in foreign exchange” (Roosevelt 1933a, 2)

Key Terms

-

Announcement DateMarch 6, 1933

-

End DateMarch 15, 1933

-

Legal AuthoritySection 5(b) of the Trading with the Enemy Act of 1917

-

AdministratorUS executive branch and Treasury Department

-

Communication and DisclosureThe president communicated that all banks that reopened were viable, no matter when they opened

-

Permitted WithdrawalsDepositors were permitted small withdrawals for essential use; for example, savings banks allowed $10 withdrawals to meet urgent personal needs

-

Treatment of Depositors or InvestorsDepositors could withdraw small sums for needs such as food, medicine, and other daily essential transactions

-

Outcomes90% of the country’s banking resources became available by the general resumption of business on March 15, 1933

-

Notable FeaturesThe Fed issued an emergency currency that was little used; various abortive proposals for clearinghouse certificates and other temporary currencies stoked confusion during the holiday; Government authorities were liberal in their evaluations of banks’ solvency, with the promise that the government would cover any losses to the Federal Reserve; despite the federal government’s push for uniformity, state authorities’ approaches to bank reopenings varied significantly

By mid-February 1933, the United States was in the depths of the Great Depression and the banking system faced sustained depositor runs and currency hoarding. On February 14, the governor of Michigan declared a holiday for all banks and trusts in the state. There followed a wave of declared bank holidays and bank runs across the country. The public withdrew $1.8 billion in gold and currency from banks in February and early March, with nearly two-thirds of those withdrawals occurring in the week ended Friday, March 3. By that date, 25 of 48 states had implemented bank holidays or restricted withdrawals. The Federal Reserve Board, concerned about the dwindling cash and gold reserves at the Federal Reserve Banks, voted to implement a nationwide bank holiday early in the morning on Saturday, March 4, the day of President Franklin D. Roosevelt’s inauguration. Fed and US Treasury officials persuaded the governors of remaining states to close their banks before business opened that day. Roosevelt declared a national bank holiday on March 6, his third day in office, to place a uniform set of restrictions on banks and buy some time to plan for their reopening. On March 9, Congress passed the Emergency Banking Act. The next day, President Roosevelt issued an executive order dictating the reopening procedure. Banks applied for licenses to reopen from the Treasury and state authorities. On March 13, 1933, the 12 Reserve Banks and viable banks in those cities reopened, followed by viable banks in cities with clearinghouse branches on March 14, and a general reopening of remaining viable banks on March 15. By the end of March, $1.2 billion, or two-thirds of the decline in deposits since the beginning of February, had returned to the banking system.

This case study is about the nationwide bank holiday instituted in the United States in March 1993 during the Great Depression, “a unique event in American financial history” (Silber 2009, 21). Appendix A gives a detailed description of the statewide holiday in Michigan that preceded the national holiday.

In the early 1930s, the US banking system was under extreme economic stress, manifesting in domestic runs to hoard currency and massive foreign withdrawals of gold. Despite efforts by the Hoover administration and incoming Roosevelt administration, by mid-February 1933, after runs in various states during which customers withdrew more than 20% of all deposits, the banking system was on the brink of total collapse. On February 14, 1933, the governor of Michigan declared a bank holiday, followed by the governor of Maryland on February 25 (Awalt 1969; Hoover 1933; Jaremski, Richardson, and Vossmeyer 2023; Silber 2009).

Many other states and municipalities declared their own bank holidays or withdrawal restrictions the following week, as bank runs spread nationwide. By Friday, March 3, the last day of Herbert Hoover’s presidency, 18 states had declared bank holidays; this number increased by 10, to 28 states, over the following two days. Additionally, by March 3, seven states and the District of Columbia had restricted bank withdrawals, and four had taken other precautionary steps, according to the Associated Press (CFC 1933a; CFC 1933b). These holidays were not mandatory in most states, and many states allowed depositors to withdraw up to 5% of their funds.FThe nature of these state-level holidays varied, with only 28 states enacting total shutdowns of their banking systems that mirrored the national holiday that would follow (CFC 1933a; Wicker 1996). The Federal Reserve System’s gold reserves fell $200 million on March 2 and 3, reaching their legal limit (Awalt 1969; CFC 1933a; Jaremski, Richardson, and Vossmeyer 2023; NYT 1933a; NYT 1933d; Silber 2009; St. Louis Fed 2021; Wicker 1996).

Early on the morning of Saturday, March 4, the Federal Reserve Board, concerned about the dwindling cash and gold reserves at the Federal Reserve Banks, voted to implement a nationwide bank holiday that day, but Hoover declined to approve the measure “in the last few hours of this administration” (Meltzer 2003, 388). To achieve the same outcome, Fed and Treasury officials urged the governors of New York and other key banking states to close their banks on Saturday morning, before business opened on March 4, and most complied. Once New York Governor Herbert Lehman had proclaimed a holiday, early that morning, the Federal Reserve Bank of New York announced that it would observe the holiday and suspended gold payments and banking transactions. The other Reserve Banks also closed soon after. Thus, on March 4, the day that Franklin D. Roosevelt assumed the office of the presidency, virtually every bank in the country was subject to a bank holiday or operating under some restrictions imposed by state authorities or the Office of the Comptroller of the Currency (OCC)FA congressional joint resolution on February 25, 1933, empowered the Comptroller to exercise for national banks the same powers that state officials exercised over state banks. This resolution also gave the comptroller special regulatory authority over banks in Washington, DC, for a period of six months (US Government 1933). (Awalt 1969; NYT 1933c; Rockoff 1993; St. Louis Fed 2021; US Government 1933).

After taking office, the Roosevelt administration immediately began work on restoring confidence in the banking system. Several members of the Treasury Department, OCC, and Federal Reserve carried over from the Hoover administration and had previously recommended the declaration of a national bank holiday, using the legal authority of the World War I–era Trading with the Enemy Act. President Roosevelt announced Proclamation 2039, declaring a national bank holiday, late on the evening of Sunday, March 5, 1933, having been convinced of its necessity by Treasury Secretary William Woodin and its constitutionality by Attorney General Homer Stille Cummings (Awalt 1969; Roosevelt 1933a; Roosevelt 1934).

Proclamation 2039 declared a four-day bank holiday lasting through March 9, 1933, during which time all bank transactions were suspended. This included paying out deposits, making loans, discounting paper, and dealing in foreign exchange. Unlike many state bank holidays announced in the previous weeks, it was mandatory and initially did not allow small deposit withdrawals. However, the national holiday allowed for case-specific exemptions for necessities. Also, similar to many state bank holidays, banks were authorized to receive deposits into special trust accounts from which depositors could withdraw funds without restriction (Roosevelt 1933a; Wicker 1996).

Proclamation 2039 also provided for the issuance of clearinghouse certificates. Clearinghouses—which were associations of banks in major cities—had issued these certificates in US banking panics since the late 19th century as a transferrable liability capable of serving as a payment substitute, before the creation of the Federal Reserve (Fulmer 2022c).FThe use of clearinghouse certificates (CLCs) in banking panics between 1873 and 1914 is documented across several YPFS case studies (Fulmer 2022b; Fulmer 2022c). But they would prove unnecessary in the 1933 crisis, as the Fed now had several tools to provide liquidity to banks and others in a crisis (Fed 1934; Fulmer 2022c; Roosevelt 1934).

Immediately following the declaration of the national holiday, the president, Treasury secretary, attorney general, Comptroller, and the Fed (together, Executive Branch), set about expanding upon legislation that had been prepared at the end of the Hoover administration, which would enable the orderly reopening of banks following the holiday. Congress passed the Emergency Banking Act (EBA) on March 9, 1933, and the president signed the legislation on the same day. The EBA validated the declaration of the banking holiday, empowered the Reconstruction Finance Corporation (RFC) to purchase preferred stock in banks, allowed the Fed to issue currency against all bank assets, and gave the Comptroller the power to appoint conservators for banks as an alternative to liquidation (Boston Fed 1996; Greene 2013; Roosevelt 1934).

On the same day, March 9, President Roosevelt issued Proclamation 2040, which extended the banking holiday “in full force and effect until further proclamation by the President” (Roosevelt 1933b). On March 10, he issued Executive Order 6073, which stated that banks that were members of the Federal Reserve System—including all nationally chartered banks and state-chartered member banks—needed to apply to the Treasury secretary for licenses to reopen. The order designated the Federal Reserve as an agent of the Treasury secretary for receiving applications for licenses. The order also dictated that state authorities were empowered to accept applications for reopening from state-chartered banks that were not members of the Federal Reserve System. The Executive Branch reopening plan dictated that banks would be reopened in stages, but that all banks that reopened would be capable of satisfying all customer claims with new currency. President Roosevelt communicated the reopening plan to the public via radio address on March 12, 1933, the first of his now famous “fireside chats” (Roosevelt 1933c). The public generally responded positively to the announcement of the holiday and the president’s “fireside chat” explanation of the reopening procedure. Upon resumption of banking services, deposits reentered the banking system at a rapid pace (Jabaily 2013; Kennedy 2014; Roosevelt 1933d; Silber 2009).

On March 13, 1933, the Federal Reserve Banks began transacting with banks and viable banks in the 12 cities with Fed branches reopened. On March 14, viable banks in the 250 cities with clearinghouses reopened, and a general reopening took place on March 15. The general reopening on March 15 meant that viable banks controlling 90% of the country’s banking resources had resumed operations. By the end of March, 72% of US banks had resumed normal operations (Greene 2013; Jabaily 2013; Kennedy 2014). A timeline of events related to the national bank holiday is shown in Figure 1.

Figure 1: Timeline of Events Related to the National Bank Holiday of 1933

Sources: Author’s analysis.

Sources: Author’s analysis.

The Michigan state bank holiday had nationwide repercussions—draining reserves from other states, as Michigan depositors rushed to take out the 5% of funds they were allowed, and leading depositors in other states to hoard gold and currency in the expectation that they could be next (Awalt 1969). State officials declared bank holidays and withdrawal limitations as a means of preventing depositors from shifting funds to other states without moratoriums, creating a “doom loop” of sorts (Wicker 1996, 127–28). A New York Times editorial on March 4 opined that the immediate cause of the “hoarding mania” that gripped the nation was the “numerous decrees postponing bank payments to depositors” (NYT 1933b, 12). By the time of his inauguration, President Roosevelt had no other option but to declare a national bank holiday.

William Silber of New York University notes that, while FDR “did not invent the bank holiday,” since every state had declared a holiday or other restrictions by the time of his March 5 proclamation, the president’s action was crucial because it “turned a maze of state restrictions into a uniform national policy (Silber 2009, 22). “This action was the first key step to resolving the banking crisis: It shifted the responsibility for the integrity of the payment system to the federal government, where it belonged” (Silber 2009, 22-23).

State governments and the business community quickly rallied behind the president and the bank holiday. The chief executive officer of General Motors, among the largest US companies at the time, stated that his company “stood ready to accept whatever losses may result” from the banking holiday (Kennedy 2014, 160). Former President Hoover also immediately urged support for the bank holiday, and a conference of governors passed resolutions of confidence in the president (Kennedy 2014).

In his memoir recounting the first year of his administration, Roosevelt says that he considered the “prompt co-operation and vigorous action” by Congress in the passing of the EBA to have been the most important factor in reassuring the US public (Roosevelt 1934, 18). He says that once depositors regained access to their deposits upon the bank reopening the week of March 13, 1933, “the most critical part of the banking emergency was over” (Roosevelt 1934, 34). However, he makes clear that the core of the emergency could be fixed only through a long series of laws aimed at reorganization and measured control of the US economic structure (Roosevelt 1934).

An article in the Commercial & Financial Chronicle on Saturday, March 11, commented on the unprecedented expansion of the president’s powers under the Emergency Banking Act. The article expressed confidence in the president’s decisive nature during his tenure and stated that the expansion of powers was necessary given the situation. The article also expressed that the president had the confidence of the entire nation and that he would use the powers to bring about a return to normal procedures as soon as possible (CFC 1933b).

In an article discussing the effectiveness of the bank holiday, Silber states that the EBA, and the Federal Reserve’s willingness to provide unlimited amounts of currency with indemnification from the federal government, effectively constituted 100% implicit deposit insurance for reopened banks. He concludes that this implicit guarantee, alongside decisive use of authority by the Executive Branch to create substantive policy solutions that backed up forceful rhetoric, contributed to the reestablishment of confidence and credibility. Joseph Mason of Drexel University notes that by October 1933, it became clear that a number of reopened banks could not qualify as solvent (and thereby access newly created Federal Deposit Insurance Corporation [FDIC] coverage) without being recapitalized. Therefore, the Reconstruction Finance Corporation’s preferred stock purchase program became an important tool for ensuring that the number and condition of capital deficient banks was not exposed (Mason 2000; Silber 2009).

A paper by Jaremski, Richardson, and Vossmeyer (2023) finds that despite efforts to avoid stigma in the bank reopening process, banks that reopened in March did take in more deposits than those that opened later in the process. Despite this evidence of depositor response to signaling by regulators, this did not significantly slow the broader recovery effort. The authors assert that the lesson of the bank holiday is that bank stigma can be overcome through supportive policies such as those that accompanied the reopening period (Jaremski, Richardson, and Vossmeyer 2023).

Conti-Brown and Vanatta (2021) emphasize that the Roosevelt administration’s commitment to closing insolvent banks helped legitimize the claim that all banks that reopened were viable. They state that this legitimacy laid the foundation for an expansion of the US bank supervisory apparatus. President Hoover’s policy had largely been a refusal to close banks, which the authors assert was an endorsement of all of the banks and therefore none of the banks. Before the crisis, the role of bank supervision was only to keep banks from failing. After the holiday, in which authorities designated viable and nonviable banks, the authors assert that bank supervision began a transition into a “decisive bureaucratic power” (Conti-Brown and Vanatta 2021, 113). As such, the authors state that this broader supervisory discretion over the US banking system became the force behind the US dollar (Conti-Brown and Vanatta 2021).

Key Design Decisions

Purpose

1

Amid the economic uncertainty of the Great Depression, the US banking system was experiencing sustained runs in 1933. On February 14, 1933, the governor of Michigan declared a statewide bank holiday, beginning a series of widespread state bank holidays throughout the country (St. Louis Fed 2021).

Over two business days on March 2 and 3, the Federal Reserve System lost $200 million in gold and $150 million in currency.FAppendix B shows the weekly deterioration of deposits in the banking system and the subsequent recovery (Jaremski, Richardson, and Vossmeyer 2023). On March 3, the Federal Reserve Board suspended the requirement that Federal Reserve Banks hold at least 40% of currency in gold. While the system’s reserves were above 40% overall, the New York Fed’s were at 24% (Awalt 1969; Fed 1934).

Early on the morning of Saturday, March 4, the Federal Reserve Board considered three options to address the dwindling cash and gold reserves at the Reserve Banks: declaring a nationwide bank holiday, suspending specie payments, or suspending banks’ reserve requirements. The Board decided to recommend a bank holiday. However, Hoover declined to approve the measure “in the last few hours of this administration” (Meltzer 2003, 388). To achieve the same outcome, Fed and Treasury officials urged the governors of New York and other key banking states to close their banks on Saturday morning, before business opened on March 4, and most complied. All 12 reserve banks also closed (Awalt 1969; Boston Fed 1996; Rockoff 1993).

Thus, a de facto national bank holiday was already in place on the day that the Roosevelt administration began. However, the terms varied between mandatory and voluntary, and many, but not all, states allowed depositors to withdraw up to 5% of their money. This feature had not prevented many depositors from withdrawing as much as they could, creating a liquidity drain for Federal Reserve Banks in their districts (Awalt 1969; Boston Fed 1996; Wicker 1996).

The purpose of a national bank holiday was to impose a uniform set of restrictions on all banks and allow for the development of adequate means of handling the national emergency (US Government 1933). As the Fed noted in its 1933 annual report: “An important purpose of this action was to attack the problem of bank failures comprehensively by reviewing at one time the condition of all banks and reopening only such banks as could meet all demands upon them. This procedure was intended both to assure more equitable treatment as between the depositors who were making withdrawals and those who were not, and to restore confidence in the banking situation as a whole” (Fed 1934, 10).

Joint consultations between existing Treasury and Federal Reserve officials and incoming members resulted in three immediate action items for the new president:

- (a) Use the Trading with the Enemy Act of 1917 to declare a national bank holiday.

- (b) Call a special session of Congress to validate and extend the holiday and pass new legislation for bank reopening.

- (c) Summon bank leadership from several major cities (New York City, Chicago, Philadelphia, Baltimore, and Richmond) for immediate consultation (Kennedy 2014).

On March 5, 1933, an assembly of bankers from the major cities advised that a holiday was necessary. The incoming president rejected the suggestion of federal deposit insurance, as Fed officials had the week before. Before declaring the holiday, Roosevelt required that the Treasury secretary have emergency legislation ready for passage through Congress by March 9. Having been convinced of the legality of using the Trading with the Enemy Act by his attorney general, Roosevelt decided that the national bank holiday was indeed necessary (Awalt 1969; Kennedy 2014; Roosevelt 1934). He was “fully convinced that the drastic action of closing the banks was necessary in order to prevent complete chaos on Monday morning” (Roosevelt 1934, 4).

Late on the evening of March 5, Roosevelt issued Proclamation 2039, declaring a national bank holiday through March 9. It suspended all banking activity and banned the exportation of gold outside the country. The objective then became implementing a plan to reopen banks as soon as possible while ensuring that only viable banks commenced business again (Roosevelt 1933a; Roosevelt 1934; Silber 2009).

Part of a Package

1

Discouraging Hoarding

The presidential proclamations prohibited buying or selling gold in any form other than jewelry, and this prohibition lasted until 1974. In his radio address on March 12, 1933, President Roosevelt characterized the hoarding of currency as an “exceedingly unfashionable pastime” (Roosevelt 1933c, 3). The Treasury Department requested a list from the Federal Reserve of large gold withdrawals that had not been returned by the start of the phased reopening on March 13. Various states took legal efforts to further discourage hoarding following the resumption of bank operations. For example, Kansas lawmakers passed a resolution to publicly disclose the names of individuals who drew any amount larger than $500 when banks reopened. The New York Times reported that $200 million in gold returned to the banking system by the close of business on Friday, March 10, as depositors feared fines or imprisonment (Boston Fed 1996; NYT 1933j; NYT 1933l).

Promoting Liquidity

During the holiday, checks served as an important means of payment alongside the small withdrawals permitted for essential use; retailers and service providers also accepted money orders, credit, and even nontradable goods as payment (Kennedy 2014).

At first, a popular idea among Treasury officials and other advisers in both administrations was to encourage clearinghouses to issue clearinghouse certificates as an alternative to currency during and after the bank holiday. President Roosevelt included the idea in Proclamation 2039 on March 5, and in several cities, clearinghouses rapidly began to print such certificates and banks made arrangements to pledge the required assets. Some jurisdictions went further. On March 7, the New York Times reported that New York Governor Herbert Lehman had signed state legislation authorizing the creation of a corporation that would issue a statewide scrip, arguing that no city-based clearinghouse could provide the banking needs of the whole state (NYT 1933h). In a separate article, the Times reported that Treasury officials supported local clearinghouse certificates and had dismissed the idea of a national government scrip, possibly issued through the Reconstruction Finance Corporation. The Treasury approved Lehman’s plan on March 7 and withdrew that approval on March 8 (CFC 1933b; NYT 1933h).

The Treasury was still working toward some kind of national plan. On March 7, 1933, the Treasury secretary issued Regulation No. 12, authorizing the 250 clearinghouses in the country to issue certificates against sound bank assets, but only with explicit Treasury approval before March 10, and with the further condition that the Treasury could revoke permission if the secretary had announced a comprehensive national plan before then (Greene 2013; Kennedy 2014; US Government 1933).

Federal Reserve officials didn’t see a need for either clearinghouse certificates or a new form of scrip. Certificates had solved a problem in pre-Fed financial crises by making sure banks could obtain currency, but with the Fed in operation, any bank with assets could obtain currency. Federal Reserve Board Governor Eugene Meyer and New York Fed President George Harrison both regarded certificates “as an exercise in utter futility,” according to Meyer’s biographer (Pusey 1974, 233). And any national scrip, they believed, should be issued by the Fed (Pusey 1974).

On Wednesday, March 8, the Times reported that officials were leaning toward a Fed-issued currency, Federal Reserve bank notes, which could be based on any sound assets possessed by banks rather than gold, which backed the existing currency. Meanwhile, the Times also reported that the public debate over various currency plans “brought questions from perplexed citizens . . . The result is that an atmosphere of immense confusion and doubt hung over the entire administration, as viewed from the outside” (Krock 1933, 1). The president proposed to the Treasury secretary that all government securities, of any maturity, be immediately convertible into cash at par. Treasury and Fed officials were alarmed at the inflationary implications. Instead, they proposed authorization for the Fed to lend to individuals or corporations using government securities as collateral (see Key Design Decision No. 12, Regulatory Changes) (Fed 1934; Kennedy 2014).

On March 9, the Emergency Banking Act authorized both the proposal for Fed lending to nonfinancial entities on government collateral and the issuance of Federal Reserve bank notes as emergency currency. The New York Times compared the emergency currency to a currency briefly used in a 1914 banking crisis under the Aldrich-Vreeland Act, which was also backed by bank assets. Unlike the 1914 currency, however, the Federal Reserve bank notes represented liabilities of the Fed itself. The Fed preferred this option because it was not inflationary—no reserves were created. The availability of Federal Reserve bank notes meant that clearinghouse certificates would simply not be needed, the Fed later noted in its 1933 annual report (Fed 1934; Fulmer 2022a; Goldenweiser 1951).

The president told the Fed to issue currency liberally and that he would request that Congress cover any losses (see Key Design Decision No. 9, Verification of Solvency). In combination with President Roosevelt’s forceful communication, this created an implicit deposit guarantee for banks that reopened following the holiday. Despite this implicit guarantee, President Roosevelt expressed skepticism about formal deposit insurance until the end of May 1933, although many bankers and politicians promoted the idea from the early days of the crisis (Fed 1933a; Jaremski, Richardson, and Vossmeyer 2023; NYT 1933g; Silber 2009).

Ultimately, some cities reported limited issuance of clearinghouse certificates and scrip backed by bank deposits. Once banks began to reopen, the usage of Federal Reserve bank notes was also minimal, as depositors rushed to return cash and gold to their banks; the emergency currency may have provided a positive psychological impact. Usage grew slowly over the course of 1933 and peaked at $213 million in December 1933. The Fed’s new lending authorities were also little used (Fed 1934; CFC 1933c; CFC 1934).

Restructuring and Liquidating Banks

Section 304 of the Emergency Banking Act empowered the Reconstruction Finance Corporation to purchase directly or make loans secured by preferred stock in any national bank, state bank, or trust company that requested such support, if the Treasury secretary concurred and the president approved. The RFC was created by the Reconstruction Finance Corporation Act (RFC Act) in January 1932 to provide secured emergency lending to financial institutions that did not have access to the Federal Reserve’s discount window, given the impact of the Great Depression on credit availability (Leonard 2022; US Congress 1933a).

The RFC Act dictated that the RFC could not have more than three times its capital stock outstanding in any forms of obligations, and this was increased to 6.6 times in July 1932. As such, the RFC’s capital stock of $500 million enabled it to issue government-guaranteed debt for up to $3.3 billion in assistance. The RFC had $1.2 billion in notes outstanding at the end of the first financial quarter of 1933 (Lawson 2021; US Congress 1932; US Treasury 1959).

Uptake of RFC capital injections was initially slow, but by year-end 1933, RFC aid totaled one-third of the total capital in the US banking system. Ultimately, the RFC provided $1.2 billion in capital injections to 7,400 financial institutions (Lawson 2021). Full accounts of the work of the RFC during the Great Depression can be found in two Yale Program on Financial Stability case studies (Lawson 2021; Leonard 2022).

Following the general reopening of viable banks, the Comptroller oversaw restructuring efforts for national banks that did not qualify for immediate reopening but could be made viable with government support.FState authorities appointed conservators for state banks (Kennedy 2014, 195). This restructuring required the doubling in size of the office of the Comptroller. An executive order issued on March 18, 1933, gave state authorities the power to appoint conservators for state-chartered banks (See Key Design Decision No. 9, Verification of Solvency) (Awalt 1969; Greene 2013; Kennedy 2014; US Government 1933).

Nonbank Institutions

At the state level, authorities invoked clauses directing savings banks to require 60- or 90-day notice for withdrawals. For example, heads of New York–based savings banks met and agreed to invoke a 60-day notice for withdrawals, and the New Haven Clearing Association voted to invoke a clause requiring 90 days’ notice for deposits greater than $100 (CFC 1933b).

Legal Authority

1

Section 5(b) of the Trading with the Enemy Act of 1917 provided the authority for the national bank holiday. President Roosevelt used this authority to issue Proclamation 2039 declaring the national bank holiday beginning on March 6, 1933 (Roosevelt 1933a). Section 5(b) gave the president two major powers during times of war that related to the announcement of the bank holiday:

- (a) To prevent the offshoring of the nation’s gold, and

- (b) To uniformly prohibit or exercise greater control over transactions at all US banks (US Congress 1933b).

There had been some question among the attorney general and other officials in the Hoover administration about the strength of the authority under the Trading with the Enemy Act as a basis for a nationwide bank holiday. Hoover did not want to declare a holiday without assurances from Roosevelt that he would convene a special session of Congress to pass emergency legislation. However, once in charge, Roosevelt’s administration reconciled any issues and relied on the law (Awalt 1969).

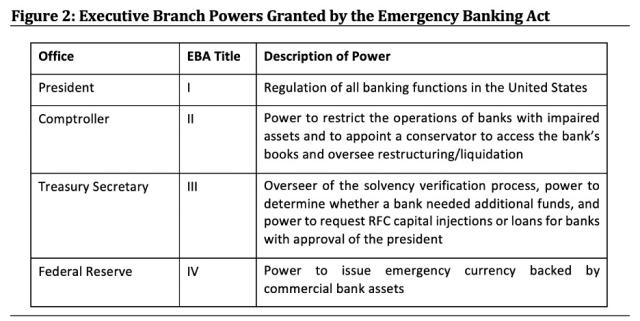

The Emergency Banking Act of 1933 provided the authority for the bank reopening process. Passed on March 9, the EBA retroactively approved the bank holiday and granted new powers to the president and other members of the Executive Branch. The main impact of the Emergency Banking Act was to bring the banking system under the authority of the Executive Branch via the Treasury secretary (Greene 2013; US Congress 1933a). The specific powers delegated to each part of the Executive Branch are shown in Figure 2.

Source: Greene 2013.

Source: Greene 2013.

Proclamation 2040 extended the bank holiday indefinitely until further executive action. Executive Order 6073 established the Federal Reserve System as agents capable of acting on behalf of the Treasury secretary and dictated that all Federal Reserve System member banks needed to apply for licenses from the Treasury Department in order to reopen. The Treasury secretary issued several regulations that dictated the terms of limited banking services during the holiday and guided the reopening process (Roosevelt 1933b; Roosevelt 1933d; US Government 1933).

Administration

1

The president worked with the Treasury secretary, Comptroller of the Currency, attorney general, and Federal Reserve officials to administer the bank holiday as well as to develop and implement the bank reopening plan. The departing Treasury secretary, Ogden Mills, from the Hoover administration, informed William Woodin, the Treasury secretary of the incoming Roosevelt administration, of prior discussions regarding a possible bank holiday the night before the presidential inauguration. Additionally, the Treasury undersecretary and acting Comptroller of the Currency carried over in their roles, as well as the staff of the Federal Reserve Board, providing important continuity in the midst of the crisis (Greene 2013; Kennedy 2014; Roosevelt 1934).

The president declared the national holiday and authorized the Treasury secretary to regulate what limited banking services were offered during the holiday period (See Key Design Decision No. 7, Details of Suspension, Gates, or Fees). The president’s Executive Order 6073 empowered the Treasury secretary to oversee the reopening process, with the support of the Federal Reserve. The Federal Reserve made emergency currency backed by commercial bank assets available to banks to support the reopening process. The Comptroller oversaw the restructuring of banks that could not open immediately but could be made viable with government support (Greene 2013; Kennedy 2014; Roosevelt 1933a; Roosevelt 1933d).FFigure 2 in Key Design Decision No. 3, Legal Authority, provides an applicable breakdown of powers within the Executive Branch.

In terms of reopening procedures, nationally chartered banks and state-chartered banks that were members of the Federal Reserve System were required to apply for licenses from the Treasury department (see Key Design Decision No. 9, Verification of Solvency). Executive Order 6073 established Federal Reserve branches as agents of the Treasury Department to receive and evaluate license applications (Roosevelt 1933d).

State-chartered banks that were not members of the Federal Reserve System received their reopening licenses from state-level authorities (See Key Design Decision No. 9, Verification of Solvency). State authorities operated independently but were instructed to allow these banks to open on the same schedule as the nationally chartered banks. An outcome of their independence was that some of these state-chartered nonmember banks opened with restrictions on deposit withdrawals or provision of loans. Approximately half of US state authorities permitted reopening under restriction and 1,685 state banks were permitted to reopen under restriction in March (Awalt 1969; Jaremski, Richardson, and Vossmeyer 2023; Roosevelt 1933c).

Governance

1

Roosevelt’s Proclamation 2039, based on the authority of the Trading with the Enemy Act of 1917, established federal control over all banks such that a consistent nationwide solution could be developed. The passage of the EBA by Congress confirmed that control and provided necessary expanded powers over the financial system to the president and the Executive Branch.FMany members of Congress did not even have a chance to read the legislation before it came time to vote (Greene 2013). All Federal Reserve member banks fell under the licensing jurisdiction of the Treasury secretary. The secretary then delegated authority for reopening nationally chartered banks to the Comptroller and authority over state-chartered member banks to their respective Federal Reserve Bank, under a common framework setting the terms for reopening. Nonmember state banks were under the purview of state supervisory agencies (Roosevelt 1934; Wicker 1996).

Having been empowered to issue currency against stable assets instead of gold, Federal Reserve Banks were required to report the amount of new currency as well as the amount and type of collateral held, pursuant to a regulation outlined by the Treasury secretary on March 12 (Fed 1933a; US Government 1933).

Communication

1

The governor of Michigan’s declaration of a statewide bank holiday on February 14, 1933, led to a nationwide contagion effect. Governors attempted to reassure the public but found limited success (Silber 2009).FSee Appendix B for a graph documenting the change in deposits in the banking system over time.

President Roosevelt convened a conference of governors and other local officials from most of the states on March 6, 1933.FThis meeting had been scheduled nearly a month before March 5 to cover a range of issues but became entirely about the bank holiday (NYT 1933f). At the meeting, Roosevelt and the state governors discussed modes of relief for constituents as measures were taken to relieve the banking situation. The president delivered a statement to the conference of state officials emphasizing the importance of a uniform, national solution through cooperation among the federal government and the states. Newspaper reporting published on March 6, 1933, suggested that state legislators and citizens in major banking states, such as Pennsylvania and New York, were still looking to local decisions at the start of the national bank holiday. Roosevelt addressed this issue at the end of his statement to the governors, stating: “One State is doing it one way and another State is doing it another way . . . But as yet we have no national policy for all of this. I believe we can have one, and ought to have one” (Roosevelt 1934, 12). Following the meeting, a committee of the governors issued a resolution expressing confidence in the president and committing to joint cooperation (NYT 1933e; NYT 1933f; NYT 1933i; Roosevelt 1934; Warn 1933).

Public statements supporting the bank holiday by members of the administration, business leaders, and former president Hoover himself all contributed to the restoration of confidence among the US public. On the day that the holiday was announced, Treasury Secretary Woodin stated, “We are at the bottom now. We are not going any lower,” while asserting that the United States would remain on the gold standard (Kennedy 2014, 160). However, the New York Times reported on March 8 that there was confusion among major New York bankers about the issuance of currency and the extent to which limited banking functions had been permitted. These confusions stemmed from a misunderstanding about the impact of a proclamation by the governor on regulations dictated by the Treasury secretary, which authorized limited use of currency and scrip. Governor Lehman issued a clarifying statement, saying that his proclamation did not restrict any functions that had been permitted by the Treasury secretary. On March 9, 1933, President Roosevelt sent a message to Congress requesting immediate legislative measures in order to support the reopening of sound banks (Fed 1933b; Kennedy 2014; Krock 1933).

Some critics contended that banks should have been reopened immediately following the passage of the Emergency Banking Act. Roosevelt addressed these concerns in a radio address on Sunday, March 12. Roosevelt’s March 12, 1933, radio address was heard by an estimated 60 million listeners, nearly half of the country’s population.FThe total population of the United States in 1933 was 126 million people (per USAfacts.org). The address outlined the phased reopening plan and emphasized that all banks that opened were viable, even if they did not open on the first day of eligibility. In this first “fireside chat,” Roosevelt said, “I can assure you that it is safer to keep your money in a reopened bank than under the mattress” (Roosevelt 1933c). The public generally responded positively to the communications regarding the holiday. Upon reopening of the banks, the public immediately returned gold and currency to the banking system (see Key Design Decision No. 8, Treatment of Depositors or Investors) (Fed 1933a; Kennedy 2014; Roosevelt 1933c; Silber 2009).

Details of Holidays, Suspensions, or Gates

1

Proclamation 2039 announced a four-day suspension of all transactions at all banking institutions, lasting from Monday, March 6, through Thursday, March 9, 1933. The president always intended to extend the holiday as necessary, considering an indefinite holiday to be unwise (Kennedy 2014; Roosevelt 1933a).“Banking institutions” included the following types of firms:

- (a) Banks;

- (b) Federal Reserve Banks;

- (c) National banking associations;

- (d) Trust companies

- (e) Savings banks;

- (f) Building and loan associations;

- (g) Credit unions; and

- (h) All other businesses receiving deposits, making loans, or discounting paper (Roosevelt 1933a).

The legal authority used for the proclamation stipulated that any violations of the banking holiday were punishable by a fine of up to $10,000 ($238,000 when adjusted for inflationFInflation data found via usinflationcalculator.com.) or imprisonment for up to 10 years (Roosevelt 1933a).

For the duration of the holiday, however, the Treasury secretary was empowered to permit the performance of banking functions on an ad hoc basis with the approval of the president. The Treasury secretary also had the power to permit or require the issuance of clearinghouse certificates or other claims against assets of banks and the power to authorize the creation of special trust accounts in banking institutions, which could receive new deposits that were withdrawable on demand (Roosevelt 1933a).

On March 9, Congress passed the Emergency Banking Act, which granted the president and the Executive Branch full authority over all banking functions. On the same day, President Roosevelt issued Proclamation 2040, which extended the bank holiday pending further executive action. By March 15, 10 days after the announcement of the national holiday, banks representing 90% of the country’s banking resources had resumed operations (Greene 2013; Jabaily 2013; Roosevelt 1933b; US Congress 1933a).

The national bank holiday provided a uniform set of rules that was lacking across the individual state holidays by transferring power over bank reopening to the Executive Branch; the Treasury then delegated reopening responsibility back to state and federal authorities under a common framework. The problems with the various state holidays were that they not only lacked consistency at their inception, but their rules changed independently. Such waffling had spooked depositors in nearby states and influenced run dynamics (Wicker 1996).

However, the decision to revert to state bank authorities to decide whether to reopen state-chartered banks that were not members of the Federal Reserve System resulted in “wide differences in availability of banking facilities in the country” (Meltzer 2003, 423). Some states immediately reopened all state-chartered banks on March 13; others were more selective (see Key Design Decisions No. 8, Treatment of Depositors or Investors, and No. 9, Verification of Solvency).

Treatment of Depositors or Investors

1

Beginning on March 7, 1933, the Treasury secretary used his expanded authority to allow banks to provide limited, essential services. In Treasury Regulation No. 10, the secretary announced that any state or national bank would be permitted to exercise the usual banking functions “as shall be absolutely necessary to meet the needs of its community for food, medicine, other necessities of life, for the relief of distress, for the payment of usual salaries and wages, for necessary current expenditures for the purpose of maintaining employment, and for other similar essential purposes”FThe full text of Treasury regulations and other statements during March 1933 are published in US Government (1933, 11–14), starting on page 11.(US Government 1933, 12). The Treasury secretary mandated that all precautions be taken to prevent hoarding and unnecessary withdrawals. Savings banks allowed a maximum $10 withdrawal to meet “urgent personal needs,” and commercial banks opened to make change (Kennedy 2014, 162).

A March 10 amendment to Treasury Regulation No. 10 permitted the Federal Reserve Banks to make advances to national banks and state-chartered banks that were members of the Federal Reserve System to “meet the needs of their respective communities” consistent with the regulation. It also authorized Reserve Banks to make advances to “individuals, partnerships, and corporations to meet their immediate pay roll requirements” March 12, 1933 (US Government 1933, 16). This measure excluded state-chartered banks that were not members of the Federal Reserve System; Congress later directed the Fed to expand lending to nonmember banks (see Key Design Decision No. 12, Regulatory Changes).

In the 5% of banks that were permanently closed and liquidated, authorities prioritized depositors while taking care to ensure that no creditor received preferential treatment (Kennedy 2014).

After the government received complaints, the RFC ensured that depositors received immediate access to their funds from banks in liquidation. The RFC expanded its lending operation, issuing loans to insolvent institutions against their good assets such that the banks could pay their depositors (Kennedy 2014).

Verification of Solvency

1

President Roosevelt laid out the terms for the reopening process with Executive Order 6073. He stated that the precondition for a bank reopening was that its soundness be verified to the satisfaction of the government. In order to comply with this executive order, nationally chartered banks and state-charted banks that were members of the Federal Reserve System needed to apply for a license from the Treasury Department, while state banks were required to apply to their respective state superintendent of banks (NYT 1933k; Roosevelt 1933d).

Ogden Mills, Treasury secretary in the Hoover administration, had created a reopening plan that became the foundation of the plan that the Roosevelt administration implemented. The Mills plan called for dividing banks into three categories:

- (a) Assets equal to deposits and ready for unrestricted reopening,

- (b) Obviously insolvent and requiring supervised liquidation, and

- (c) Eligible for reopening after restructuring (Kennedy 2014).

The Mills plan was largely adopted by the Roosevelt administration and Mills’s former assistant, Undersecretary Arthur Ballantine, who transitioned to the new administration and was in charge of implementation. Authorities also determined to reopen banks that met the (a) criteria in three stages (Kennedy 2014; Roosevelt 1933c). President Roosevelt justified this decision in his radio address, saying, “Your Government does not intend that the history of the past few years shall be repeated. We do not want and will not have another epidemic of bank failures” (Roosevelt 1933c, 2).

Owing to time constraints, the information used for verification was in most cases the bank examiner’s previous reports, which were conducted twice a year for national banksFState examiners faced even more dated information, with all bank reports being precrisis and some being nearly a full year old (Kennedy 2014). and which may have been outdated especially given the significant challenges the system faced. Other considerations such as geographical distribution and politics also played some role, and some weak banks were opened early (Jaremski, Richardson, and Vossmeyer 2023; Kennedy 2014).

There was a general tendency toward forbearance among the Federal Reserve authorities that the Treasury secretary and Comptroller sought to dispel. The minutes of the Federal Reserve board meeting held on March 11, 1933, reported that Federal Reserve officials had expressed concerns about the planned method of valuation. Valuing bank assets at fire sale liquidation prices would prevent immediate reopening of many banks that otherwise may have been eligible if their assets were valued on a fair going-concern basis. Having received a letter from the Treasury secretary emphasizing this point, President Roosevelt stated that valuation mistakes would be inevitable and that the Federal Reserve would likely face losses on its lending to banks. He continued that given the increased scope of the Federal Reserve System under the EBA, he would ask Congress to cover any losses Federal Reserve Banks suffered. He also expressed confidence that Congress would grant such a request (Awalt 1969; Fed 1933a).

Among the banks that required licenses from the Treasury secretary, state banks that were part of the Federal Reserve System applied to their district Federal Reserve branch and national banks applied to the Comptroller. The Treasury secretary adopted the phased reopening process, wherein banks in Federal Reserve Bank cities opened on Monday (March 13), banks in clearinghouse cities on Tuesday (March 14), and a general opening followed on Wednesday (March 15). The Treasury secretary worried that a staggered opening would cause more skepticism than a general opening.FThe fireside chat on March 12 helped to calm these fears, as President Roosevelt emphasized banks that reopened would be viable, no matter the date of their reopening (see Key Design Decision No. 6, Communication and Disclosure) (Roosevelt 1933c). The Treasury secretary requested that the Comptroller’s chief national bank examiner in each district submit a list of national banks based on criteria that were dictated by Treasury officials over telephone. Comptroller officials reviewed the recommendations along the same criteria and reconciled any differences found. Federal Reserve officials conducted the same process, and if the three examining parties disagreed on a particular recommendation, the Treasury secretary then made a final decision (Fed 1933a; Kennedy 2014).

State banks that were not members of the Federal Reserve System fell outside the procedure for national banks, leading to confusion regarding who should assess their soundness. The EBA had amended the Federal Reserve Act of 1913 to make such banks eligible for liquidity assistance from the Federal Reserve—although only against government securities as collateral—but members of Congress and state governors were hesitant to vest further licensing power with the Treasury secretary. Authorities ultimately decided that state officials would be empowered to license state banks outside the Federal Reserve System, along the same guidelines as those outlined in Roosevelt’s Executive Order 6073 (Kennedy 2014; Roosevelt 1933d).FAwalt says that many officials considered this to be a mistake, but that it was impossible for national authorities to handle the state banks given their limited information availability and time (Awalt 1969).Figure 3 provides a breakdown of the distribution of reopening authorities.

Source: Kennedy 2014.

Source: Kennedy 2014.

On March 11, the Treasury secretary authorized financial institutions to transact with the Federal Reserve and stated that all Federal Reserve branches—as well as other federal financial agencies, including federal land banks, intermediate credit banks, Federal Home Loan Banks, regional agricultural credit corporations, and the RFC—would reopen on March 13, 1933 (Fed 1933a).FThese institutions did not require a verification process.

On March 13, the Federal Reserve System and viable banks in the 12 Federal Reserve branch cities opened to the public. On March 14, viable banks in the 250 cities with recognized clearinghouses were permitted to open, and on March 15, all other viable banks that had been verified to be sound reopened (Greene 2013).

For banks that required liquidation, the EBA empowered the Comptroller of the Currency to appoint a conservator to oversee the bank’s liquidation proceedings. An executive order issued on March 18, 1933, granted state authorities the power to appoint conservators to banks under their supervision that had not reopened. Following the appointment of a conservator, all banks, state and national, required a license directly from the Treasury secretary in order to reopen (US Congress 1933a; US Government 1933).

The licensing process featured some instances of regulatory arbitrage. Specifically, several state banks in Texas withdrew from the Federal Reserve System to receive reopening licenses from the state bank superintendent. That said, 237 state banks entered into membership in the Federal Reserve System. The Federal Reserve’s 1933 annual report reported a net reduction in its membership of 293, driven largely by bank liquidations (Fed 1934; Kennedy 2014).

Other Conditions

1

Research did not reveal any other conditions associated with the national holiday.

Exit Strategy

1

Following the passage of the EBA, President Roosevelt issued an executive order dictating the bank reopening procedure. The following day, the president released a statement to the press that outlined the reopening procedure in greater detail (Kennedy 2014; NYT 1933k; Roosevelt 1933d).

A March 10 amendment to Treasury Regulation No. 10 permitted the Federal Reserve Banks to make advances to member banks to “meet the needs of their respective communities”; it also authorized Reserve Banks to make advances to “individuals, partnerships, and corporations to meet their immediate pay roll requirements” (US Government 1933, 16). The March 8, 1933, edition of the New York Times reported the opening of major banks in New York for limited operations (See Key Design Decision No. 6, Communication and Disclosure). The government stated that no bank was permitted to open until its soundness had been verified to the government’s satisfaction (see Key Design Decision No. 9, Verification of Solvency). Before receiving this verification, banks opened only on a restricted basis in order to satisfy essential needs of the public, as defined and allowed by the Treasury secretary (Kennedy 2014; Krock 1933; NYT 1933k).

The Bureau of Engraving and Printing worked 24-hour shifts for several days to print new Federal Reserve bank notes, which were shipped to Federal Reserve branches in preparation for the phased reopening. That said, the extra currency proved to be more useful psychologically than economically. Usage turned out to be minimal after gold and reserves flowed back into the system upon reopening. Though authorities were left with more notes than they needed, the more inflationary monetary policy was favored by several congressmen, who encouraged the extension of the note program (CFC 1933c; CFC 1934; NYT 1933k).

Having completed their evaluations, government authorities had successfully grouped banks into three categories (see Key Design Decision No. 9, Verification of Solvency). Approximately 50% of the country’s banks were approved to fully reopen by March 15, 1933, enabling public access to 90% of the country’s banking resources. An additional 25% were approved to open partially, paying out a percentage of deposits, and 20% were barred from paying out deposits but would be preserved through restructuring.FThe partially opened and restructured banks were both placed under conservators, meaning that 45% of the country’s banks entered conservatorship (Kennedy 2014, 187). The remaining 5% of banks were deemed insolvent and permanently closed. By the end of March, 5,387 of 6,694 Federal Reserve member banks and 7,654 of 11,435 state-chartered banks had fully reopened. In total, of the 17,000 commercial banks in existence before the holiday, 12,000 survived (Boston Fed 1996; Kennedy 2014; Todd 1992).

Regulatory Changes

1

During the March 1933 crisis, the Fed expanded access to its lending facilities to state-chartered banks that were not members of the Federal Reserve System. The Fed had traditionally opposed lending to such banks because they had not put up the capital for Fed membership and were not subject to Fed oversight (Sastry 2018).

In the 1932 Emergency Relief and Construction Act, Congress had added Section 13(3) to the Federal Reserve Act to allow Federal Reserve Banks, with Federal Reserve Board approval, to lend at a penalty rate to “individuals, partnerships, and corporations” based on any collateral that the Reserve Bank concluded was “secured to [its] satisfaction” (Sastry 2018, 23). Such lending could occur only under “unusual and exigent circumstances.” However, despite the broad language of Section 13(3), the Fed had excluded state-chartered nonmember banks from its coverage.

During the 1933 bank holiday, Title IV of the Emergency Banking Act added Section 13(13) to the Federal Reserve Act. This section allowed a Federal Reserve Bank to lend to “individuals, partnerships, and corporations” based on collateral “secured by direct obligations of the United States,” without a determination of unusual or exigent circumstances and without approval of the Federal Reserve Board (US Congress 1933a, tit. 4). In contrast to its interpretation of Section 13(3), the Fed agreed to lend to state-chartered nonmember banks under the new Section 13(13) authority, since these advances were backed by government securities (Sastry 2018).

However, the Fed was under pressure in March 1933 from the Treasury and state bankers to broaden access to nonmember banks against a broader range of collateral. After some discussion among the Fed, Treasury, and others, Congress voted on March 24 to amend the EBA to allow state-chartered nonmember banks access to the Fed’s discount window on the same basis as member banks for a period of one year (Sastry 2018).

Title I of the EBA increased the power of the Executive Branch to affect monetary policy, independent of the Federal Reserve. In combination with Title IV, the Executive Branch used the power to briefly take the United States off the gold standard by authorizing the Federal Reserve to issue currency backed by bank assets. Despite this move, authorities publicly said that the US remained on the gold standard. The government partially restored the gold standard with the Gold Standard Act of 1934, which persisted until the US ended dollar convertibility to gold in 1971 (Greene 2013; Kennedy 2014; US Congress 1933a).

Congress passed the Glass-Steagall Banking Act of 1933 on June 16, 1933. This legislation comprehensively reformed the US banking system, creating more formal separation between commercial banking activities and speculative investment activities. The new legislation also created the Federal Open Market Committee of the Federal Reserve to set monetary policy and the Federal Deposit Insurance Corporation to insure bank deposits. The FDIC began providing coverage for up to $2,500 per depositor on January 1, 1934 (Boston Fed 1996).

Key Program Documents

-

(Jabaily 2013) Jabaily, Robert. 2013. “Bank Holiday of 1933.” Federal Reserve History, November 22, 2013.

Article summarizing the national bank holiday of 1933.

-

(Jones 1951) Jones, Jesse H. 1951. Fifty Billion Dollars: My Thirteen Years with the RFC, 1932–1945. New York: Macmillan.

Memoir recounting the activities and operations of the RFC, which the government established in 1932 to provide financing to railroads, financial institutions, and corporations.

-

(St. Louis Fed 2021) Federal Reserve Bank of St. Louis (St. Louis Fed). 2021. “Uncurrent Events: The Bank Holiday of 1933.” Inside FRASER (blog), May 12, 2021.

Summary of the lead-up to the bank holiday of 1933.

-

(Fed 1933a) Board of Governors of the Federal Reserve System (Fed). 1933a. “Meeting Minutes of the Federal Reserve Board.” March 11, 1933.

Meeting minutes from the Federal Reserve Board meeting of March 11, 1933.

-

(History Grand Rapids 1933) History Grand Rapids. 1933. “Gov. William Comstock’s Proclamation of a Bank Holiday.” Grand Rapids Historical Commission, February 14, 1933.

Webpage archiving the proclamation issued by the governor of Michigan, declaring a statewide banking holiday.

-

(Roosevelt 1933a) Roosevelt, Franklin D. 1933a. “Proclamation 2039—Bank Holiday, March 6-9, 1933, Inclusive.” The American Presidency Project, March 6, 1933.

Presidential proclamation declaring the national bank holiday.

-

(Roosevelt 1933b) Roosevelt, Franklin D. 1933b. “Proclamation 2040—Continuing in Force the Bank Holiday Proclamation of March 6, 1933.” The American Presidency Project, March 9, 1933.

Presidential proclamation extending the national bank holiday.

-

(Roosevelt 1933c) Roosevelt, Franklin D. 1933c. “Fireside Chat 1: On the Banking Crisis.” UVA Miller Center, Presidential Speeches, March 12, 1933.

Radio address delivered on March 12, 1933, by Franklin D. Roosevelt, explaining the national bank holiday.

-

(US Government 1933) US Government. 1933. “Documents and Statements Pertaining to the Banking Emergency.” Part I, February 25–March 31, 1933.

Article containing all of the proclamations, legislation, executive orders, and Treasury regulations associated with the national bank holiday.

-

(Roosevelt 1933d) Roosevelt, Franklin D. 1933d. “Executive Order 6073—Reopening Banks.” The American Presidency Project, March 10, 1933.

Executive order establishing the protocol by which banks were to reopen following the national bank holiday.

-

(US Congress 1932) US Congress. 1932. Reconstruction Finance Corporation Act. H. R. 7360, 72nd Congress, Sess. I, January 22, 1932

January 1932 act creating the RFC.

-

(US Congress 1933a) US Congress. 1933a. Emergency Banking Act. H. R. 1491, 73rd Congress, Sess. I, March 9, 1933.

Act establishing provisions for exiting the 1933 bank holiday.

-

(US Congress 1933b) US Congress. 1933b. Trading with the Enemy Act. 50 U.S.C. Ch. 53.

Act establishing powers to limit economic activity with foreign adversaries during times of war.

-

(CFC 1933a) Commercial & Financial Chronicle (CFC). 1933a. “Financial Situation.” Commercial & Financial Chronical 136, no. 3532 (March 4).

Article reporting on the US financial situation on March 4, 1933.

-

(CFC 1933b) Commercial & Financial Chronicle (CFC). 1933b. “Financial Situation.” Commercial & Financial Chronicle 136, no. 3533 (March 11).

News article discussing the bank holiday and the legislation passed to facilitate banks’ reopenings.

-

(CFC 1933c) Commercial & Financial Chronicle (CFC). 1933c. “Financial Situation.” Commercial & Financial Chronicle 136, no. 3535 (March 25).

Article discussing the financial situation of the US on March 25, 1933, in the aftermath of the reopening of the banks.

-

(CFC 1934) Commercial & Financial Chronicle (CFC). 1934. “Financial Situation.” Commercial & Financial Chronicle 138, no. 3587 (March 24).

Article discussing the major financial stories in the US.

-

(Denny 1933) Denny, Harold N. 1933. “Michigan Holiday on Banks Is Ended.” New York Times, February 22, 1933.

News article reporting on the proclamation extending the bank holiday on a de facto basis.

-

(Krock 1933) Krock, Arthur. 1933. “Washington Leans to Emergency Currency; Roosevelt Studying 8-Point Bank Program; Banks Here to Furnish Cash for Vital Needs.” New York Times, March 8, 1933.

Article discussing public debates in Washington over the use of emergency currency.

-

(NYT 1933a) New York Times (NYT). 1933a. “Status of Banking Restrictions by States.” New York Times, March 3, 1933.

Article reporting the amount of allowed withdrawals in various states.

-

(NYT 1933b) New York Times (NYT). 1933b. “Hoarding and the ‘Moratorium.’” New York Times, March 4, 1933.

News article discussing the negative impacts of hoarding and efforts to discourage it.

-

(NYT 1933c) New York Times (NYT). 1933c. “Two-Day Holiday for Banks Here, Lehman’s Order.” New York Times, March 4, 1933.

News article reporting on the announcement of a bank holiday by the governor of New York.

-

(NYT 1933d) New York Times (NYT). 1933d. “Gold Drain Ended by Reserve Bank.” New York Times, March 5, 1933.

News article reporting on the massive outflow of gold from the Federal Reserve System and efforts to stop it.

-

(NYT 1933e) New York Times (NYT). 1933e. “Pennsylvania Awaits Decision at Capital.” New York Times, March 6, 1933.

News article reporting on the bank holiday decision in Pennsylvania.

-

(NYT 1933f) New York Times (NYT). 1933f. “Roosevelt Meets Governors Today.” New York Times, March 6, 1933.

News article reporting on a conference held among the president and state governors concerning the national bank holiday.

-

(NYT 1933g) New York Times (NYT). 1933g. “Glass Banking Bill Held in New Favor.” New York Times, March 7, 1933.

News article discussing the emergency and permanent legislative responses to the banking crisis.

-

(NYT 1933h) New York Times (NYT). 1933h. “Legislature Votes Lehman Wide Bank Powers; Creates a State Corporation to Issue Scrip; Woodin Authorizes New Checking Accounts.” New York Times, March 7, 1933.

Article discussing broad new powers for Governor Lehman and new authorizations from Treasury Secretary Woodin.

-

(NYT 1933i) New York Times (NYT). 1933i. “Roosevelt Sums Up Task to Governors.” New York Times, March 7, 1933.

News article reporting on the content of the meeting between the President and a conference of governors.

-

(NYT 1933j) New York Times (NYT). 1933j. “Kansas House Would List Hoarders.” New York Times, March 10, 1933.

News article reporting on the decision by Kansas legislators to publicly disclose the names of individuals who drew excess currency when banks reopened.

-

(NYT 1933k) New York Times (NYT). 1933k. “Banking Orders Issued.” New York Times, March 11, 1933.

News article discussing the reopening procedure for banks.

-

(NYT 1933l) New York Times (NYT). 1933l. “Gold Inflow Brings $20,000,000 in Day.” New York Times, March 11, 1933.

News article reporting the return of gold to the banking system during the nationwide holiday.

-

(Warn 1933) Warn, W.A. 1933. “Prepare in Albany to Act on Banks.” New York Times, March 6, 1933.

News article reporting on the New York legislative agenda changes in the wake of the banking situation.

-

(Awalt 1969) Awalt, Francis Gloyd. 1969. “Recollections of the Banking Crisis in 1933.” Business History Review 43, no. 3: 347–71.

Article by the former OCC director discussing the banking crisis of 1933.

-

(Boston Fed 1996) Federal Reserve Bank of Boston (Boston Fed). 1996. “Closed for the Holiday: The Bank Holiday of 1933.”

Article discussing the national closure of banks in March 1933.

-

(Fed 1933b) Board of Governors of the Federal Reserve System (Fed). 1933b. “Emergency Banking Legislation; Unified Banking—Opinion of Board’s Counsel; Annual Report of Bank of France.” Federal Reserve Bulletin 19, no. 3 (March).

Federal Reserve Bulletin for March 1933 reviewing the bank holiday.

-

(Fed 1934) Board of Governors of the Federal Reserve System (Fed). 1934. Annual Report. 1933.

Federal Reserve Board annual report for the year 1933.

-

(Goldenweiser 1951) Goldenweiser, E.A. 1951. American Monetary Policy. New York: McGraw-Hill Book Company.

Book discussing American monetary policy.

-

(Hoover 1933) Hoover, Herbert. 1933. Letter from Herbert Hoover to Franklin D. Roosevelt, February 18, 1933.

Letter from President Herbert Hoover to President-elect Franklin D Roosevelt, detailing the banking crisis.

-

(Pusey 1974) Pusey, Merlo J. 1974. Eugene Meyer. New York: Alfred A. Knopf.

Biography of Depression-era Federal Reserve Chair Eugene Meyer.

-

(Roosevelt 1934) Roosevelt, Franklin D. 1934. On Our Way. New York: John Day Company.

Memoir by Franklin D. Roosevelt on the first year of his administration.

-

(US Treasury 1959) US Department of the Treasury (US Treasury). 1959. “Final Report of the Reconstruction Finance Corporation.” May 6, 1959.

Legally mandated report summarizing and evaluating the RFC’s activities and operations.

-

(Conti-Brown and Vanatta 2021) Conti-Brown, Peter, and Sean H. Vanatta. 2021. “The Logic and Legitimacy of Bank Supervision: The Case of the Bank Holiday of 1933.” Business History Review 95, no. 1: 87–120.

Article discussing banking supervision in the context of the bank holiday of 1933.

-

(Fulmer 2022a) Fulmer, Sean. 2022a. “United States: Aldrich-Vreeland Emergency Currency during the Crisis of 1914.” Journal of Financial Crises 4, no. 2: 1156–79.

YPFS case study on the Treasury Department’s role in issuing emergency currency during the Crisis of 1914.

-

(Fulmer 2022b) Fulmer, Sean. 2022b. “United States: New York Clearing House Association, the Crisis of 1914.” Journal of Financial Crises 4, no. 2: 1241–57.

YPFS case study of the New York Clearing House Association’s response to the outbreak of World War I through the issuance of clearinghouse loan certificates.

-

(Fulmer 2022c) Fulmer, Sean. 2022c. “United States: New York Clearing House Association, the Panic of 1873.” Journal of Financial Crises 4, no. 2: 1258–77.

YPFS case study on the NYCH’s issuance of CLCs during the Panic of 1873.

-

(Jaremski, Richardson, and Vossmeyer 2023) Jaremski, Matthew S., Gary Richardson, and Angela Vossmeyer. 2023. “Signals and Stigmas from Banking Interventions: Lessons from the Bank Holiday in 1933.” NBER Working Paper No. 31088, October 2023.

Working paper analyzing the signals sent by the government’s method for reopening banks following the 1933 bank holiday and the public’s response to these signals.

-

(Kennedy 2014) Kennedy, Susan Estabrook. 2014. The Banking Crisis of 1933. Lexington: University Press of Kentucky.

Book discussing the causes of and policy responses to the banking crisis of 1933.

-

(Lawson 2021) Lawson, Aidan. 2021. “US Reconstruction Finance Corporation: Preferred Stock Purchase Program.” Journal of Financial Crises 3, no. 3: 738–85.

YPFS case study discussing the broad-based capital injection program administered by the Reconstruction Finance Corporation.

-

(Leonard 2022) Leonard, Natalie. 2022. “United States: Reconstruction Finance Corporation, Emergency Lending to Financial Institutions, 1932–1933.” Journal of Financial Crises 4, no. 2: 1351–73.

YPFS case study on the broad-based emergency liquidity provided by the US Reconstruction Finance Corporation in the lead-up to the Great Depression.

-

(Mason 2000) Mason, Joseph R. 2000. “Reconstruction Finance Corporation Assistance to Financial Intermediaries and Commercial & Industrial Enterprise in the US, 1932-1937. ” Prepared for the World Bank Group, January 2000.

Academic study on effects of RFC lending.

-

(Meltzer 2003) Meltzer, Allan H. 2003. A History of the Federal Reserve, Volume 1: 1913–1951. Chicago: University of Chicago Press.

Book about the early history of the Federal Reserve System.

-

(Rockoff 1993) Rockoff, Hugh. 1993. “The Meaning of Money in the Great Depression.” National Bureau of Economic Research, Historical Working Paper No. 0052, December 1993.

Article discussing the decline in quality of money stock as a contributor to the severity of the Great Depression.

-

(Runkel 2022) Runkel, Corey N. 2022. “United States: New York Clearing House Association, the Panic of 1907.” Journal of Financial Crises 4, no. 2: 1322–50.

YPFS case study examining clearinghouse loan certificates issued during the Panic of 1907.

-

(Sastry 2018) Sastry, Parinitha. 2018. “The Political Origins of Section 13(3) of the Federal Reserve Act.” FRBNY Economic Policy Review 24, no. 1 (September): 1–33.

Article about the Federal Reserve’s emergency powers through Section 13(3) of the Federal Reserve Act, which bear some similarity to the Bank of England’s authorities during the Panic of 1866.

-

(Silber 2009) Silber, William L. 2009. “Why Did FDR’s Bank Holiday Succeed?” FRBNY Economic Policy Review 15, no. 1 (July): 19–30.

Article discussing the key policies that accompanied the bank holiday of 1933.

-

(Todd 1992) Todd, Walker F. 1992. “History of and Rationales for the Reconstruction Finance Corporation.” Federal Reserve Bank of Cleveland, Economic Review 28, no. 4: 22–35.

Academic article on the history of the RFC.

-

(Wicker 1996) Wicker, Elmus. 1996. The Banking Panics of the Great Depression. New York: Cambridge University Press.

Book discussing several instances of banking panic during the Great Depression, including the 1933 holiday.

-

(Wiggins et al., forthcoming) Wiggins, Rosalind Z., Owen Heaphy, Anmol Makhija, Stella Shaefer-Brown, Greg Feldberg, and Andrew Metrick. Forthcoming. “Survey of Bank Holidays and Fund Suspensions.” Journal of Financial Crises.

Survey of YPFS case studies examining bank holidays and mutual fund suspensions.

-

(Greene 2013) Greene, Stephen. 2013. “Emergency Banking Act of 1933.” Federal Reserve History, November 22, 2013.

Article summarizing the passage and impact of the Emergency Banking Act.

-

(US Congress 1934) US Congress. 1934. “Stock Exchange Practices.” Hearings before the US Senate Committee on Banking and Currency, 73rd Congress, Sess. II, January 5–23, 1934.

Transcript of testimony by the chief bank examiner of Michigan before the Senate Banking committee.

Appendix A: The Michigan Holiday (February 1933)

In February 1933, Detroit, Michigan, had two major banking groups, the Detroit Bankers Company Group and the Union Guardian Group (Ford Group). These groups were significant in that they owned all of the stock of major banks that provided services throughout the state. Also, as the name suggests, the Ford Group serviced the family and business interests of Henry Ford, the chief of Ford Motors and a major economic force in the state (Awalt 1969).

Michigan attracted large migration inflows in the early 20th century as workers sought jobs in the automobile industry. When credit conditions tightened, many of these workers elected to return to their more rural hometowns, where personal connections could support meager survival in a barter economy. Many of these individuals left small business credit lines and mortgages unpaid, sending massive losses to the Detroit banks that were their creditors and prompting deposit outflows that by early 1933 had accelerated into a run. The seizure of property by banks did little good as there was no market left for these assets. By February 1933, 72% of assets at Union Guardian Trust Company, a member of the Ford Group, were “immobilized” in this way (Kennedy 2014, 80). In testimony before the Senate Banking Committee, Michigan’s chief bank examiner attributed the failure of the Ford Group to three factors; (a) poor managerial decision-making; (b) heavy losses from the national economic slowdown; and (c) heavy losses on takeovers of Kean, Higbie & Co. and American State Bank (Jones 1951; Kennedy 2014; US Congress 1934).

To support liquidity in response to the ongoing run, authorities asked Henry Ford to subordinate some of his company’s deposits in the Ford Group. First National Bank, a member bank owned by the Detroit Bankers Company Group, had been forced to liquidate almost all of its liquid assets. Union Guardian Trust Company had already borrowed from the Reconstruction Finance Corporation (RFC) and from Ford himself. If Ford did not agree to subordinate his interests in Guardian Trust Company, the Ford Group as a whole would not be able to meet withdrawals. RFC authorities felt that Ford’s participation in the bailout was essential, as they otherwise could not legally provide support beyond the appraised value of the collateral at Guardian Trust. Having already loaned money to the group, Ford refused this new request. Ford believed that the RFC would not allow Guardian Trust to fail, in part because the RFC had provided a $90 billion loan to the Chicago-based Central Republic Trust Company in June 1932 under similar circumstances (Awalt 1969; St. Louis Fed 2021; Wicker 1996).

The regional and indeed national implications of the ongoing Detroit episode motivated President Herbert Hoover to arrange for Ford to meet with the secretary of Commerce and the undersecretary of the Treasury on February 13, 1933.FThis date, a Monday, was a legal and banking holiday in observance of Abraham Lincoln’s birthday, which had fallen on Sunday, February 12 (Awalt 1969). Despite the officials’ best efforts, Ford again refused to agree to the proposed plan of subordinating his company’s deposits. He further stated that in the event that Guardian Trust Company were to close, the following morning, he would withdraw $25 million in Ford deposits from First National Bank. By 4:30pm on February 13, it became clear that there was no hope of receiving Ford’s assistance in preserving Guardian Trust Company (Awalt 1969; St. Louis Fed 2021; Kennedy 2014).