Swap Lines

United States: FIMA Repo Facility, 2020

Purpose

To “help support the smooth functioning of the U.S. Treasury market by providing an alternative temporary source of U.S. dollars other than sales of securities in the open market” and “along with the U.S. dollar liquidity swap lines the Federal Reserve has established with other central banks, to help ease strains in global U.S. dollar funding markets” (FRB 2020e)

Key Terms

-

Participating PartiesFederal Reserve Bank of New York; Most central banks and international monetary authorities were eligible; approximately 30 signed up at the outset

-

Type of SwapRepurchase agreement facility for foreign and international monetary authorities

-

Currencies InvolvedUS dollars

-

Launch DatesAnnounced: March 31, 2020 Operational: April 6, 2020

-

End DateTwo extensions; made standing facility

-

Date of First UsageWeek ended April 8, 2020

-

Interest Rate and Fees25 bps over the Fed’s interest rate on excess reserves

-

Amount AuthorizedN/A

-

Peak Usage Amount and Date$1.4 billion; week ended May 13, 2022

-

Downstream Use/Application of Swap FundsBuilding precautionary dollar balances or passing dollar liquidity to domestic financial systems

-

OutcomesLow uptake, positive announcement effects

-

Notable FeaturesBroad eligibility; no disclosure of counterparties, individual transactions

On March 31, 2020, amidst historically severe strains in the US Treasury market and global dollar funding markets, the Federal Reserve announced the Foreign and International Monetary Authorities (FIMA) Repo Facility. The FIMA Repo Facility was designed to discourage foreign official Treasury sales and broadly improve foreign dollar funding markets—and ultimately the flow of credit in the United States. The facility provided renewable, overnight repurchase agreements (repos) to central banks and other international monetary authorities against Treasury collateral. This allowed approved central banks to access dollars for precautionary reasons or to pass to their domestic financial systems without engaging in further outright Treasury sales. The Fed priced the facility to serve as a backstop to private repo rates in a normally functioning market. The Fed created the facility to complement its dollar swap lines, which it had made available to 14 central banks. Unlike the swap lines, virtually every central bank in the world was eligible for the FIMA Repo Facility. At the facility’s outset, approximately 30 central banks signed up. However, usage was minimal; volume peaked at just $1.404 billion in May 2020. Despite low uptake, Federal Reserve Bank of New York (FRBNY) staff report the facility was welcomed by market participants and argue that the FIMA Repo Facility eased selling pressure in the Treasury market. Two FRBNY researchers also find evidence it eased foreign exchange stresses and helped restore Treasury holdings of foreign central banks that were outside the Fed’s dollar swaps network. After two extensions, the Fed announced in July 2021 that the FIMA Repo Facility would become permanent.

On March 31, 2020, amidst historically severe strains in the US Treasury market and global dollar funding markets as a result of the COVID-19 pandemic, the Federal Reserve announced the Foreign and International Monetary Authorities (FIMA) Repo Facility (Choi et al. 2022). The FIMA Repo Facility was a new lending facility—technically structured as a repurchase agreement (repo)—for central banks and other international monetary authorities to secure dollar liquidity against Treasury security holdings (FRB 2020e).

Most FIMA account holders—virtually all central banks, as well as international organizations such as the Bank for International Settlements—were eligible to apply for the facility (FRB 2020a). “FIMA account holders” describes foreign central banks and other foreign monetary authorities with custodial accounts at the Federal Reserve Bank of New York (FRBNY) (Choi et al. 2022, 102). The FRBNY services more than 200 foreign official and international institutions, providing them more than 550 deposit and custody accounts, and “foreign central banks and monetary authorities hold the vast majority of these accounts” (FRBNY n.d.a). Choi et al. (2022) further clarify that the FRBNY “maintains cash and custody accounts for nearly every central bank in the world and the FIMA Repo Facility adds to a suite of Federal Reserve dollar-based correspondent banking and custody services.”

Daleep Singh, who was head of the Markets Group at the FRBNY from February 2020 to February 2021, said in an interview with the Yale Program on Financial Stability (YPFS) that about 30 counterparties initially enrolled in the facility and that these counterparties represented about 75% of foreign official Treasury holdings FThe transcript cited here leaves some ambiguity about the “30 or so” number of initial enrollees used here and whether that count was exhaustive. Singh confirmed to YPFS in follow-up emails that this was indeed the approximate total of enrollees in about the first six months. (Singh 2022). The FIMA Repo Facility complemented the dollar swap lines that the Fed had expanded or made newly available to 14 leading central banks in response to foreign dollar funding stresses earlier in March (Hoffner 2023).

The FIMA Repo Facility’s broader eligibility assured dollar liquidity for central banks that didn’t have access to the swap lines but did have sufficient holdings of Treasuries. Prior to the rollout of the FIMA Repo Facility, some of the largest official sector holders of Treasuries were central banks, particularly China’s, that didn’t have access to the Fed’s swap lines (Singh 2022).

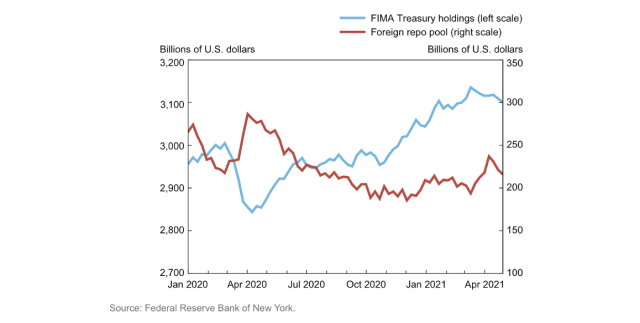

Despite the expanded dollar access that the swap lines provided, central banks were significant sellers of Treasuries in March and April, which contributed to the stress in the Treasury market. Foreign official holdings of Treasuries declined by $150 billion in March 2020 and an additional $70 billion in April, when the FIMA Repo Facility was also in place (Choi et al. 2022, 97).

Singh (2022) said of these foreign, official sector Treasury sales that “not all of that was used to defend their currencies; a lot of it was just essentially ‘cash under the mattress.’”

Evidence that many of these sales were precautionary can be seen in the juxtaposition of FIMA account holders’ Treasury holdings versus their assets in the Fed’s “foreign repo pool”—a reverse repo product that FIMA customers use to deposit their cash overnight; see Figure 1 (Choi et al. 2022).

Figure 1: FIMA Treasury Holdings and the Fed’s Foreign Repo Pool

Source: Choi et al.

The FRBNY later reported that the surge in the foreign repo pool balance “was primarily driven by a shift in FIMA customers’ preference toward liquid, safe holdings amid a highly uncertain period of increased volatility, dollar funding pressures, and Treasury market stress” (FRBNY 2021, 43).

The Fed created the FIMA Repo Facility to discourage foreign official Treasury sales and broadly improve foreign dollar funding markets—and ultimately the flow of credit in the United States. The FIMA Repo Facility provided renewable, overnight repos to foreign and international monetary authorities against Treasury collateral (FRB 2020a). This allowed these foreign central banks to build their dollar balances for precautionary reasons or to pass dollar liquidity to their domestic financial systems without engaging in further outright Treasury sales (Choi et al. 2022).

The Fed priced the facility higher than private repo rates in a normally functioning market to encourage its use only in times of stress. The repos charged the Fed’s administered interest rate on excess reserves plus 25 basis points (bps) (FRB 2020a). Thus, throughout 2020, the facility had an all-in interest cost of 35 bps (FRB 2021b). Because the repos were against Treasury securities, the Fed faced no foreign exchange risk (FRB 2020a). It managed its price risk via haircuts on collateral consistent with those at its discount window, which were between 1% and 8% depending on the type and term of the Treasury security (FRB 2020a; FRS 2020).

Singh (2022) said he believed that after the FIMA Repo Facility was in place, swap lines and FIMA repo access provided liquidity to countries holding “well over 80%” of the official holdings of Treasury securities. The FRBNY said that FIMA account holders that had enrolled in the facility “represented a broad range of global regions, economic sizes, and levels of economic development, and accounted for a large share of foreign official ownership of outstanding U.S. Treasury securities” (FRBNY 2021, 16). Borrowings from the FIMA Repo Facility were limited by the haircut-adjusted market value of an eligible borrower’s Treasury collateral (FRB 2020a). The Foreign Currency Subcommittee of the Fed’s Federal Open Market Committee (FOMC) also could set limits on a per-counterparty, per-day basis; the Fed didn’t release information about any limits it may have set (Choi et al. 2022, 104; FOMC 2020d; Goldberg and Ravazzolo 2021b, 2).

Weekly reported outstanding FIMA Repo Facility volume peaked at $1.404 billion on May 13, 2020 (FRB 2022b). The FRBNY described usage of the facility in 2020 as “minimal” and largely reflecting “small-value exercises that took place as part of operational onboarding of approved account holders” (FRBNY 2021).

When the Fed announced the FIMA Repo Facility on March 31, 2020, it said the facility would be in place for at least six months (FRB 2020e). After two six-month extensions, the Fed announced on July 28, 2021, that the FIMA Repo Facility would become permanent; the Fed established the standing facility with an initial interest rate of 25 bps and a per-counterparty limit of $60 billion (FRB 2020g; FRB 2020h; FRB 2021a).

A report from four authors at the FRBNY finds that the FIMA Repo Facility “eased pressure on foreign official institutions to sell Treasury securities for precautionary reasons” despite limited uptake. “Nevertheless, central banks’ increased confidence in their ability to raise dollar liquidity through the facility likely contributed to a strong return to Treasury investments by the second week of April 2020.” They also note that feedback from market participants was positive on the establishment of the FIMA Repo Facility (Choi et al. 2022, 101–2, 106).

Goldberg and Ravazzolo (of the FRBNY) also separately find that foreign exchange swap spreads began to normalize later for countries without access to swaps lines—but started to after the establishment of the FIMA Repo Facility. They similarly find that, after falling earlier in the pandemic, Treasury holdings of those central banks with access to the FIMA Repo Facility, but without swap line access, began to normalize after the introduction of the FIMA repos (Goldberg and Ravazzolo 2021a).

Key Design Decisions

Purpose

1

The FIMA Repo Facility was a repurchase agreement facility for foreign and international monetary authorities that provided dollar reserves in exchange for US Treasury securities collateral. The Fed intended the facility to stanch the flow of Treasury sales from the foreign official sector and to complement Fed swap lines in supporting dollar funding markets (FRB 2020a; FRB 2020e). The facility was available to virtually any central bank in the world, while the Fed made swap lines available to only 14 central banks (Hoffner 2023).

Part of a Package

1

To ease conditions in global dollar markets, the Fed expanded and eased the terms of its swap network (Hoffner 2023). On March 15, 2020, the Fed eased the terms of its standing, uncapped swap lines with five other advanced economy central banks FThe five central banks were the Bank of Canada, Bank of England, Bank of Japan, European Central Bank, and Swiss National Bank. From the Fed’s press release: “These central banks have agreed to lower the pricing on the standing U.S. dollar liquidity swap arrangements by 25 basis points, so that the new rate will be the U.S. dollar overnight index swap (OIS) rate plus 25 basis points. To increase the swap lines’ effectiveness in providing term liquidity, the foreign central banks with regular U.S. dollar liquidity operations have also agreed to begin offering U.S. dollars weekly in each jurisdiction with an 84-day maturity, in addition to the 1-week maturity operations currently offered” (FRB 2020b). (FRB 2020b).On March 19, the Fed extended swap lines to nine additional central banks FFrom the Fed’s press release: “These new facilities will support the provision of U.S. dollar liquidity in amounts up to $60 billion each for the Reserve Bank of Australia, the Banco Central do Brasil, the Bank of Korea, the Banco de Mexico, the Monetary Authority of Singapore, and the Sveriges Riksbank and $30 billion each for the Danmarks Nationalbank, the Norges Bank, and the Reserve Bank of New Zealand” (FRB 2020c). (FRB 2020c). The Fed had set up similar swap lines during the Global Financial Crisis of 2007–2009 with the same 14 central banks (French 2023).

To ease the impact of global Treasury sales, the Fed increasingly expanded its direct Treasury purchases and also eased large bank holding companies’ capital requirements for Treasury securities (YPFS 2022). On March 23, the Fed uncapped its outright purchases of Treasury securities, promising to purchase the amounts needed to support market functioning and effective transmission of monetary policy (FRB 2020d). On April 1, the Fed temporarily exempted Treasury securities from the supplementary leverage ratio (SLR) requirement that applies to large banks. This exemption allowed large bank holding companies to not hold capital against their holdings of Treasuries. The SLR easing, like the FIMA Repo Facility, aimed to improve liquidity conditions in the market for Treasury securities (FRB 2020f).

Legal Authority

1

Section 14 of the Federal Reserve Act covers open market operations. Section 14(2)(e) provides the authority for a Reserve Bank “to open and maintain banking accounts for such foreign correspondents or agencies, or for foreign banks or bankers, or for foreign states.” This authority was the basis of the prior creation of the FIMA accounts (US Congress n.d.b; Potter 2017). The Board’s Regulation N authorizes the Reserve Banks to do business with these accounts “to effectuate the conduct of open market operations” subject to the directives of the FOMC (FRB 1962; Potter 2017).

The Fed’s monetary policy committee, the FOMC, authorized the FIMA Repo Facility by notation vote on March 31, 2020 (FOMC 2020e; FRB 2022a). The FOMC did so by amending the standing Authorization for Domestic Open Market Operations (FOMC 2020a; FOMC 2020c; FOMC 2020e).

In the Authorization for Domestic Open Market Operations, the FIMA Repo Facility is not classified under “Open Market Operations,” but is instead authorized under “Transactions with Customer Accounts.” This section authorizes such transactions “to ensure the effective conduct of open market operations, while assisting in the provision of short-term investments or other authorized services for foreign central bank and international accounts,” and authorizes the transactions “when undertaken on terms comparable to those available in the open market” (FOMC 2020c).

Governance

1

The FOMC authorized its Foreign Currency Subcommittee to approve changes to the FIMA Repo Facility’s eligibility, rate, term, and counterparty limits (FOMC 2020d). The Foreign Currency Subcommittee consisted of the FOMC chair and vice chair (typically the FRBNY president) as well as the Fed Board vice chair (FOMC 2020b; FRB 2023).

The Fed reported outstanding and weekly average volumes in its weekly “H.4.1” disclosure report of its balance sheet (Fed n.d.; FRB 2020a).

Section 11(s) of the Federal Reserve Act requires the Fed to release transaction-level data on its Section 14 open market operations with no more than an eight-quarter lag, but only for transactions with nongovernmental counterparties (US Congress n.d.a; US Congress n.d.b). Moreover, as noted in Key Design Decision No. 3, Legal Authority, the FIMA Repo Facility is not classified under “Open Market Operations” in the FOMC’s Authorization for Domestic Open Market Operations but is instead authorized under “Transactions with Customer Accounts” (FOMC 2020c). Although the Fed discloses its central bank swap transactions in real time, it does not disclose FIMA Repo Facility transactions even with a lag (FRBNY n.d.b; FRBNY n.d.c).

In a written response to a question from a member of the Financial Services Committee of the US House of Representatives about the Fed having not disclosed information about individual usage of the FIMA Repo Facility, Fed Chair Jerome Powell wrote that the Fed “does not disclose information regarding accounts and specific services provided to individual account holders, which is in line with international central banking norms and is consistent with the terms on accounts that foreign central banks establish for the Federal Reserve” (FSC 2020, 80).

Administration

1

The FRBNY managed the FIMA Repo Facility operations. The FRBNY services more than 200 foreign official and international institutions, providing them more than 550 deposit and custody accounts (FRBNY n.d.a). Most of these institutions are central banks and other international monetary authorities (see Key Design Decision No. 7, Eligible Institutions).

Additionally, Singh (2022) told YPFS that the FRBNY “went out to 30 counterparties and basically explained to them the modalities of the facility and that we welcomed their participation. It was up to those counterparties as to whether they’d apply, and I think almost all of them did so.” The FOMC also authorized its Foreign Currency Subcommittee to change the FIMA Repo Facility’s rate, term, and counterparty limits (FOMC 2020d).

As noted in Key Design Decision No. 4, Governance, the Fed did not disclose specific recipient eligibility or participation, nor did it disclose any individual transaction details. Singh (2022) noted that the Fed’s counterparties could disclose their access/use of the FIMA Repo Facility if they so chose; see Key Design Decision No. 6, Communication.

Communication

1

The Fed consistently communicated the FIMA Repo Facility as meant to support market functioning—particularly in the Treasury market and foreign dollar funding markets—and thereby supporting the flow of credit domestically (FRB 2020e; FRB 2020g; FRB 2020h). It also regularly referred to the facility as a backstop (FRB 2020g; FRB 2020h; FRB 2022a).

The Fed did not publicly communicate about who applied, received eligibility, or drew on the FIMA Repo Facility (FSC 2020, 80; Singh 2022). FRBNY’s Singh said that “if those countries wanted to, they could have announced their participation, but we didn’t announce it for fear of creating a stigma effect” (Singh 2022).

The central banks of Chile, Colombia, Ghana, Indonesia, Sri Lanka, and Hong Kong announced they had received access to the facility in 2020 FThe Financial Markets Committee—a committee of central bankers and financial sector participants—of Bank Negara Malaysia (BNM, the central bank of Malaysia) wrote in its April 9, 2020, meeting minutes that BNM “informed that it has access to the Federal Reserve’s FIMA repo facility” (BNM 2020). However, it’s unclear if BNM had officially been accepted and/or applied to the facility yet given its recent opening and the potentially required operational hurdles noted in Key Design Decision No. 7, Eligible Institutions. (BCCh 2020; BI 2020; BOG 2020; BR 2020; CBSL 2020; HKMA 2020b). Sweden and South Korea announced FIMA access shortly before their temporary swap lines with the Fed expired (Riksbank 2021; Roh 2021). (See Key Design Decision No. 16, Exit Strategy.)

Eligible Institutions

1

Virtually all central banks, as well as international organizations such as the Bank for International Settlements, were eligible to apply for the FIMA Repo Facility.

The FRBNY services more than 200 foreign official and international institutions, providing them more than 550 deposit and custody accounts. It also says that “foreign central banks and monetary authorities hold the vast majority of these accounts” (FRBNY n.d.a). “FIMA account holders” describes foreign central banks and other foreign monetary authorities with custodial accounts at the FRBNY (Choi et al. 2022, 102). Choi et al. (Choi et al. 2022) says that the FRBNY “maintains cash and custody accounts for nearly every central bank in the world and the FIMA Repo Facility adds to a suite of Federal Reserve dollar-based correspondent banking and custody services.”

New York Times Fed reporter Jeanna Smialek later reports in a book that the Fed “allowed roughly 170 central banks and foreign entities” with FRBNY accounts “potential access” to FIMA repos (Smialek 2023, 198). The Fed’s “frequently asked questions” (FAQs) released alongside the FIMA Repo Facility rollout said, “Most FIMA account holders [. . .] will be eligible to apply to use the facility,” but that account holders’ applications to the Repo Facility still needed to be approved by the FOMC Foreign Currency Subcommittee (FRB 2020a).

Additionally, Singh (2022) shared with YPFS that the FRBNY “went out to 30 counterparties and basically explained to them the modalities of the facility and that we welcomed their participation.” He said that approximately 30 counterparties enrolled in the facility in its early days and that these counterparties represented “about 75%” of foreign official holdings of Treasury securities.

Prior to the rollout of the FIMA Repo Facility, Singh said, some of the material official sector holders of Treasuries were countries that didn’t have access to the Fed’s expanded network of swap lines—particularly China, then one of the largest foreign holders of Treasuries (US Treasury 2021). And it wasn’t just China, Singh said—“There were other countries with large Treasury holdings, too, that just weren’t able to access swap lines for a variety of reasons.” The FRBNY said in its 2020 annual report on open market operations that FIMA account holders that had enrolled in the facility “represented a broad range of global regions, economic sizes, and levels of economic development, and accounted for a large share of foreign official ownership of outstanding U.S. Treasury securities” (FRBNY 2021, 16).

A press release from Chile suggested the Fed also required potential counterparties to meet certain operational requirements. Banco Central de Chile reported receiving access to the FIMA Repo Facility only after executing the Fed’s functional requirements (BCCh 2020).

Size

1

Borrowings on the FIMA Repo Facility were limited by the haircut-adjusted market value of eligible borrowers’ Treasury collateral (FRB 2020a). The Foreign Currency Subcommittee of the FOMC also could set per-counterparty, per-day limits FThe directive cited here follows the first extension of the facility in July 2020. There does not appear to be a publicly available implementation directive from immediately following the facility’s authorization and initiation. A footnote in the minutes to the Fed’s July meeting suggests the July directive is an update of the March iteration (FOMC 2020f). (FOMC 2020d). Choi et al. (Choi et al. 2022, 104) clarifies that per-counterparty limits were to be set and communicated on a bilateral basis. Bank Indonesia—the central bank of Indonesia—announced in April 2020 that it had secured a $60 billion FIMA repo line (BI 2020). Bank of Ghana announced a $1 billion FIMA repo line in May 2020 (BOG 2020). The Hong Kong Monetary Authority (HKMA) US Dollar Liquidity Facility—a back-to-back facility funded by the FIMA Repo Facility (see Decision No. 10, Downstream Use of Borrowed Funds)—provided for up to $10 billion, though the HKMA said the facility’s terms were subject to revision (HKMA 2020b). When the Fed made the FIMA permanent, it set a per-counterparty limit of $60 billion on all counterparties, with these limits subject to change by the Subcommittee (FOMC 2021).

Weekly reported outstanding FIMA Repo volume peaked at $1.404 billion on May 13, 2020 (FRB 2022b). Consistent with the timing of that peak, the HKMA reported a draw for $1.400 billion on its facility funded by the FIMA Repo Facility (HKMA 2020b; HKMA 2020c). The FRBNY described usage of the facility in 2020 as “minimal” and largely reflecting “small-value exercises that took place as part of operational onboarding of approved account holders” (FRBNY 2021).

Process for Utilizing the Swap Agreement

1

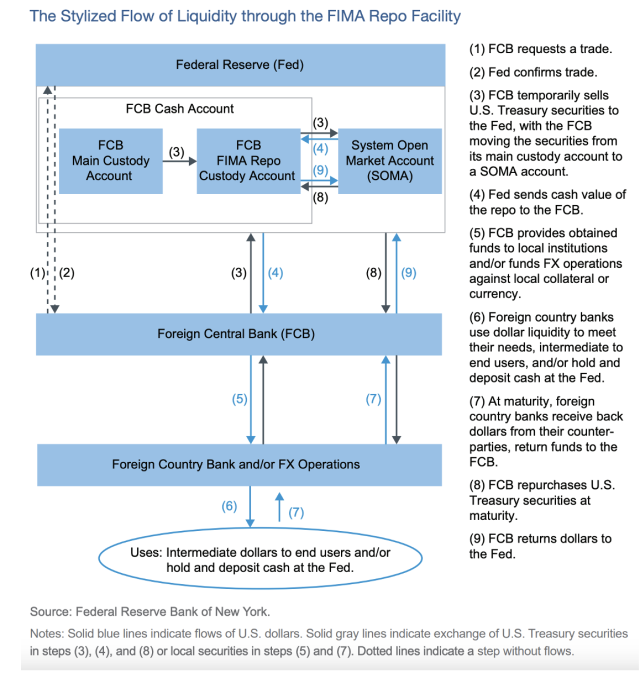

A FIMA account holder could apply to the Repo Facility for access. Once approved by the FOMC’s Foreign Currency Subcommittee, the FIMA account holder could draw on the facility by sending a trade request to the FRBNY. If the trade requested conformed to the repo facility’s terms, the FRBNY would send back a trade confirmation. Then, the FIMA account holder would sell the required Treasury collateral in a repo transaction to the Fed and the collateral would move from the FIMA account holder’s custody account to the Fed’s portfolio account. After the collateral landed, the Fed would send the haircut-adjusted cash value of the securities to the account holder. The Fed itself, rather than the tri-party repo system (provided by Bank of New York Mellon in the US) or an outside vendor, was responsible for post-trade clearing, settlement, and collateral management (Choi et al. 2022, 102). Using the Fed’s systems rather than a private market participant’s may be beneficial for maintaining confidentiality of borrower activity (Potter 2017). For a graphic outline of this process, see Figure 2 in the Appendix.

Downstream Use of Borrowed Funds

1

The FIMA Repo Facility borrowers could make the dollars available to institutions in their jurisdictions or hold them as precautionary balances (Choi et al. 2022; FOMC 2020e). FRBNY’s Singh noted of the foreign central bank Treasury sales that preceded the FIMA Repo Facility’s rollout that “not all of that was used to defend their currencies; a lot of it was just essentially ‘cash under the mattress’” (Singh 2022). The Fed intended this dollar access to help stanch outright sales of Treasury securities by foreign holders and, more broadly, ease strains in global dollar funding markets (FOMC 2020e).

The Hong Kong Monetary Authority set up a dollar auction facility that was funded by dollars it sourced from the FIMA Repo Facility. It provided for seven-day dollar repos at a rate set by auction but not lower than the rate the Fed charged on FIMA (HKMA 2020a).

Duration of Swap Draws

1

FIMA repos matured overnight but could be rolled over as needed (FRB 2020a). The HKMA used the funds from the FIMA Repo Facility to offer US dollar liquidity to banks in its jurisdiction on a seven-day basis—as noted in Key Design Decision No. 10, Downstream Use of Borrowed Funds.

Rates and Fees

1

FIMA repos charged 25 bps over the Fed’s administered interest rate on excess reserves (FRB 2020a). Throughout 2020, the all-in interest rate for a FIMA repo was thus 35 bps (FRB 2021b). No fees applied to participation in the FIMA Repo Facility.

The Fed said that this rate was generally above private market repo rates that prevail in normal times, intending for the facility to be used in periods of market stress (FRB 2020a). A report from Credit Suisse notes that 35 bps represented a premium over the rate the Fed charged on its domestic repo facilities, which cost primary dealers only the interest rate on excess reserves. Thus, at the margin, the rate differential may have encouraged dealer intermediation relative to direct participation in the FIMA Repo Facility—and thus limited private sector balance sheet relief (Pozsar 2020).

Balance Sheet Protection

1

The FIMA Repo Facility did not pose any foreign exchange risk as it swapped dollars for US Treasuries. Price risk was managed via collateral haircuts that aligned with those applied at the Fed’s discount window (FRB 2020a). These haircuts varied between 1% and 8% of the security’s market price depending on the Treasury security’s type and term to maturity (FRS 2020). Collateral was revalued daily for haircut purposes (Choi et al. 2022, 102).

Other Restrictions

1

There do not appear to have been any restrictions on the use of borrowed FIMA Repo Facility funds, nor additional restrictions on participation in the facility.

Other Options

1

Other options available to the Fed included expanding swap lines to more central bank counterparties or counteracting the foreign central banks’ Treasury sales with additional outright purchases of those securities. (See also, Key Design Decision No. 2, Part of a Package).

FRBNY’s Singh said of expanding the Fed’s network of swap lines that China and some other countries “weren’t able to access swap lines for a variety of reasons” (Singh 2022). Indeed, Smialek (2023) reports of the motivation for the FIMA repos that the Fed “needed to devise a way to shuttle dollars to governments with which it could not take the geopolitically cozy step of establishing a swap line.” Furthermore, the FIMA Repo Facility could accomplish this provision of dollar liquidity “through an existing New York Fed relationship. That made it boring instead of eyebrow raising from a political standpoint” (Smialek 2023, 197–98).

Singh (2022) said of the option for the Fed to simply buy more Treasuries instead of implementing the FIMA Repo Facility: “Of course, we could counteract those Treasury sales with asset purchases, but we’d already committed to trillions of dollars of asset purchases by that point. We didn’t want to make that number even higher.”

Exit Strategy

1

When announced on March 31, 2020, the FIMA Repo Facility was to open on April 6 and be in place for at least six months (FRB 2020e). On July 29, 2020, the FOMC extended the facility to March 31, 2021 (FRB 2020g). On December 16, 2020, the FOMC extended the facility to September 30, 2021 (FRB 2020h). In both cases, the Fed announced extensions of its swap lines with other central banks in the same press release.

On July 28, 2021, the FOMC announced that the FIMA Repo Facility would become permanent, with a per-counterparty limit of $60 billion (FRB 2021a). On the same day, the FOMC announced its new Standing Repo Facility, which allows primary dealers and banks to obtain funds from the Fed against U.S. Treasuries, agency debt, and agency mortgage-backed securities. The FOMC said that the interest rate on the Standing FIMA Repo Facility would equal the minimum bid rate for the Standing Repo Facility, then at 25 bps, unless the Foreign Currency Subcommittee set a different rate (FOMC 2021).

Closely following the Fed announcement, the Hong Kong Monetary Authority announced that it would also convert its domestic dollar liquidity facility into a standing arrangement on the same terms (HKMA 2021).

The Fed’s standing dollar swap lines with the original five advanced-economy central banks remain in place. However, the Fed allowed the temporary dollar swap lines with the other nine central banks to expire on December 31, 2021 (Hoffner 2023). Sweden and South Korea, both of which were recipients of the temporary swap lines, announced their FIMA access in December 2021 (Roh 2021; Riksbank 2021).

Key Program Documents

-

(FRB 2020a) Federal Reserve Board of Governors (FRB). 2020a. “FIMA Repo Facility FAQs.” March 31, 2020.

Document listing FIMA repo FAQs.

-

(FRB 2022a) Federal Reserve Board of Governors (FRB). 2022a. “FIMA Repo Facility FAQs (Updated).” March 24, 2022.

Updated FIMA repo facility FAQs.

-

(FRB 2023) Federal Reserve Board of Governors (FRB). 2023. “Federal Open Market Committee.” 2023.

Landing page for the FOMC.

-

(FRBNY n.d.a) Federal Reserve Bank of New York (FRBNY). n.d.a. “Central Bank & International Account Services.” Accessed December 6, 2022.

Site detailing the New York Fed’s account services for foreign official and international institutions.

-

(HKMA 2020a) Hong Kong Monetary Authority (HKMA). 2020a. “US Dollar Liquidity Facility–Summary of Terms.” April 22, 2020.

Annex document describing HKMA dollar facility terms.

-

(FOMC 2020a) Federal Open Market Committee (FOMC). 2020a. “Authorization for Domestic Open Market Operations.” January 28, 2020.

Directive authorizing reserve bank open market operations, as amended effective 1/28/2020.

-

(FOMC 2020b) Federal Open Market Committee (FOMC). 2020b. “Federal Open Market Committee Rules and Authorizations (January 2020).” January 28, 2020.

Annual pamphlet containing FOMC rules and authorizations.

-

(FOMC 2020c) Federal Open Market Committee (FOMC). 2020c. “Authorization for Domestic Open Market Operations.” March 31, 2020.

Directive authorizing reserve bank open market operations, as amended effective 3/31/2020.

-

(FOMC 2020d) Federal Open Market Committee (FOMC). 2020d. “FIMA Desk Resolution.” July 28, 2020.

Resolution prescribing the FRBNY’s FIMA operations.

-

(FOMC 2021) Federal Open Market Committee (FOMC). 2021. “Standing FIMA Repurchase Agreement Resolution.” July 27, 2021.

Resolution prescribing the FRBNY’s FIMA operations.

-

(FRB 1962) Federal Reserve Board of Governors (FRB). 1962. “12 CFR § 214.5–Accounts with Foreign Banks.” Regulation N, February 22, 1962.

Board regulation outlining authorities related to foreign accounts.

-

(US Congress n.d.a) US Congress. n.d.a. Section 11 of the Federal Reserve Act.

Section of the Federal Reserve Act including disclosure requirements.

-

(US Congress n.d.b) US Congress. n.d.b. Section 14 of the Federal Reserve Act.

Section of the Federal Reserve Act describing open market operation authorities.

-

(Roh 2021) Roh, Joori. 2021. “S.Korea c.Bank to Join Federal Reserve’s FIMA Repo Facility.” Reuters, December 23, 2021.

Article reporting Bank of Korea announcement.

-

(BCCh 2020) Banco Central de Chile (BCCh). 2020. “International Financing Lines with Central Banks.” Press release, June 24, 2020.

Central Bank of Chile press release announcing FIMA access (in Spanish).

-

(BI 2020) Bank Indonesia (BI). 2020. “Latest Developments in the Economy and BI Steps in Facing COVID-19.” Press release, April 7, 2020.

Bank Indonesia announcement of FIMA repo line (in Indonesian).

-

(BOG 2020) Bank of Ghana (BOG). 2020. “Monetary Policy Committee Press Release.” Press release, May 15, 2020.

Press release from Ghana’s central bank describing monetary developments, including a FIMA agreement.

-

(BR 2020) Banco de la República (BR). 2020. “Banco de La República Gets Access to Repos with the Federal Reserve.” Press release, April 20, 2020.

Central Bank of Colombia press release announcing FIMA access.

-

(CBSL 2020) Central Bank of Sri Lanka (CBSL). 2020. “The Central Bank Clarifies Its Repurchase Agreement with the Federal Reserve Bank, New York.” Press release, July 24, 2020.

Press release announcing FIMA access.

-

(FRB 2020b) Federal Reserve Board of Governors (FRB). 2020b. “Coordinated Central Bank Action to Enhance the Provision of U.S. Dollar Liquidity.” Press release, March 15, 2020.

Press release announcing expansion of standing swaps.

-

(FRB 2020c) Federal Reserve Board of Governors (FRB). 2020c. “Federal Reserve Announces the Establishment of Temporary U.S. Dollar Liquidity Arrangements with Other Central Banks.” Press release, March 19, 2020.

Press release announcing 10 new temporary swaps.

-

(FRB 2020d) Federal Reserve Board of Governors (FRB). 2020d. “Federal Reserve Announces Extensive New Measures to Support the Economy.” Press release, March 23, 2020.

Press release announcing Fed’s expanded Treasury purchases, among other measures.

-

(FRB 2020e) Federal Reserve Board of Governors (FRB). 2020e. “Federal Reserve Announces Establishment of a Temporary FIMA Repo Facility to Help Support the Smooth Functioning of Financial Markets.” Press release, March 31, 2020.

Press release announcing creation of the FIMA Repo Facility.

-

(FRB 2020f) Federal Reserve Board of Governors (FRB). 2020f. “Federal Reserve Board Announces Temporary Change to Its Supplementary Leverage Ratio Rule to Ease Strains in the Treasury Market Resulting from the Coronavirus and Increase Banking Organizations’ Ability to Provide Credit to Households and Businesses.” Press release, April 1, 2020.

Press release announcing the easing of banks’ SLR requirement.

-

(FRB 2020g) Federal Reserve Board of Governors (FRB). 2020g. “Federal Reserve Board Announces the Extensions of Its Temporary U.S. Dollar Liquidity Swap Lines and the Temporary Repurchase Agreement Facility for Foreign and International Monetary Authorities (FIMA Repo Facility) through March 31, 2021.” Press release, July 29, 2020.

Press release announcing first extension of the FIMA Repo Facility.

-

(FRB 2020h) Federal Reserve Board of Governors (FRB). 2020h. “Federal Reserve Announces the Extension of Its Temporary U.S. Dollar Liquidity Swap Lines and the Temporary Repurchase Agreement Facility for Foreign and International Monetary Authorities (FIMA Repo Facility) through September 30, 2021.” Press release, December 16, 2020.

Press release announcing second extension of the FIMA Repo Facility.

-

(FRB 2021a) Federal Reserve Board of Governors (FRB). 2021. “Statement Regarding Repurchase Agreement Arrangements.” Press release, July 28, 2021.

Press release announcing the conversion of the FIMA Repo facility to a standing facility.

-

(HKMA 2020b) Hong Kong Monetary Authority (HKMA). 2020b. “US Dollar Liquidity Facility.” Press release, April 22, 2020.

Hong Kong central bank release revealing its FIMA access.

-

(HKMA 2020c) Hong Kong Monetary Authority (HKMA). 2020c. “US Dollar Liquidity Facility Tender Result.” Press release, May 6, 2020.

Press release announcing results of FIMA-backed dollar tender.

-

(HKMA 2021) Hong Kong Monetary Authority (HKMA). 2021. “US Dollar Liquidity Facility.” Press release, July 30, 2021.

Press release describing new standing HKMA dollar facility tied to FIMA.

-

(Riksbank 2021) Sveriges Riksbank (Riksbank). 2021. “Riksbank Joins the Federal Reserve’s Repo Facility in USD.” Press release, December 20, 2021.

Press release announcing FIMA membership.

-

(Bertaut, von Beschwitz, and Curcuru 2021) Bertaut, Carol, Bastian von Beschwitz, and Stephanie Curcuru. 2021. “The International Role of the U.S. Dollar,” October 6, 2021.

Research note from Fed economists.

-

(BNM 2020) Bank Negara Malaysia (BNM). 2020. “Discussion Summary: Financial Markets Committee Meeting.” April 9, 2020.

Meeting minutes for the Bank Negara Malaysia’s Financial Markets Committee mentioning FIMA Repo Facility access.

-

(Choi et al. 2022) Choi, Mark, Linda S. Goldberg, Robert Lerman, and Fabiola Ravazzolo. 2022. “The Fed’s Central Bank Swap Lines and Fima Repo Facility.” Federal Reserve Bank of New York, Economic Policy Review 28, no. 1 (June): 93–113, June 2022.

Fed press release announcing the reinstatement of dollar liquidity swap lines with the ECB, BoC, BoE, and SNB.

-

(FOMC 2020e) Federal Open Market Committee (FOMC). 2020e. “Minutes of the Federal Open Market Committee, April 28–29, 2020.” May 20, 2020.

Minutes detailing the FOMC meeting of April 28-29, 2020.

-

(FOMC 2020f) Federal Open Market Committee (FOMC). 2020f. “Minutes of the Federal Open Market Committee, July 28–29, 2020.” August 19, 2020.

Minutes detailing the FOMC meeting of July 28-29, 2020.

-

(FRB n.d.) Federal Reserve Board of Governors (FRB). n.d. “Factors Affecting Reserve Balances–H.4.1–Release Dates.”

Weekly release detailing the Fed’s balance sheet.

-

(FRB 2021b) Federal Reserve Board of Governors (FRB). 2021. “Interest Rate on Excess Reserves (DISCONTINUED).” January 28, 2021.

FRED page sharing historical data on the Fed’s interest rate on excess reserves.

-

(FRB 2022b) Federal Reserve Board of Governors (FRB). 2022b. “Assets: Other: Repurchase Agreements–Foreign Official: Wednesday Level.” December 3, 2022.

FRED data listing foreign repo volume with the Fed.

-

(FRBNY n.d.b) Federal Reserve Bank of New York (FRBNY). n.d.b. “Central Bank Liquidity Swap Operations.”

Site disclosing details of central bank swap operations.

-

(FRBNY n.d.c) Federal Reserve Bank of New York (FRBNY). n.d.c. “Historical Transaction Data.”

Site releasing domestic open market, securities lending, and foreign currency operations.

-

(FRBNY 2021) Federal Reserve Bank of New York (FRBNY). 2021. “Open Market Operations during 2020.” May 24, 2021.

Annual FRBNY report describing the Fed’s market activity.

-

(FRS 2020) Federal Reserve System (FRS). 2020. “Discount Window Margins Effective July 1, 2019 to June 30, 2021.” July 8, 2020.

Chart outlining the Fed’s discount window collateral schedule.

-

(FSC 2020) Committee on Financial Services (FSC). 2020. “Monetary Policy and the State of the Economy.” Virtual hearing, June 17, 2020.

Transcript of congressional committee proceedings, including written responses.

-

(Potter 2017) Potter, Simon. 2017. “Keynote Remarks for the Commemoration of the Centennial of the Federal Reserve’s U.S. Dollar Account Services to the Global Official Sector.” Speech delivered at the Federal Reserve Bank of New York, New York, NY, December 20, 2017.

Speech from FRBNY official describing banking services provided to the foreign official sector.

-

(Pozsar 2020) Pozsar, Zoltan. 2020. “U.S. Dollar Libor and War Finance.” Credit Suisse, Global Money Notes No. 29, April 14, 2020.

Credit Suisse note discussing FIMA pricing.

-

(Singh 2023) Singh, Daleep. 2023. “Lessons Learned Interview by Steven Kelly, November 19, 2022.” Yale Program on Financial Stability Lessons Learned Oral History Project. Transcript.

Transcript of YPFS interview with Daleep Singh.

-

(Smialek 2023) Smialek, Jeanna. 2023. “Limitless: The Federal Reserve Takes on a New Age of Crisis.” New York: Alfred A. Knopf. February 28, 2023.

Book covering the Federal Reserve pandemic response.

-

(US Treasury 2021) US Department of the Treasury (US Treasury). 2021. “Major Foreign Holders of Treasury Securities.” June 15, 2021.

US Treasury’s Treasury International Capital (TIC) data describing foreign holdings of US Treasuries.

-

(YPFS 2022) Yale Program on Financial Stability (YPFS). 2022. “COVID-19 Financial Response Tracker Visualization (CFRTV).” 2022.

Database tracking financial responses to COVID-19.

-

(French 2023) French, Jack. 2023. “United States: Central Bank Swaps to 14 Countries, 2007–2009.” Journal of Financial Crises 5, no. 1.

Case study discussing 2008 Fed swap lines.

-

(Goldberg and Ravazzolo 2021a) Goldberg, Linda, and Fabiola Ravazzolo. 2021a. “Do the Fed’s International Dollar Liquidity Facilities Affect Offshore Dollar Funding Markets and Credit?” Federal Reserve Bank of New York, Liberty Street Economics, December 20, 2021.

Note discussing research findings.

-

(Goldberg and Ravazzolo 2021b) Goldberg, Linda, and Fabiola Ravazzolo. 2021b. “The Fed’s International Dollar Liquidity Facilities: New Evidence on Effects.” Federal Reserve Bank of New York Staff Report No. 997, December 20, 2021.

FRBNY staff research paper describing market impact of swaps and FIMA repos.

-

(Hoffner 2023) Hoffner, Benjamin. 2023. “United States: Central Bank Swaps to 14 Countries, 2020.” Journal of Financial Crises 5, no. 1.

Case study discussing 2020 Fed swap lines.

Figure 2: FIMA Repo Facility Execution Process

Source: Choi et al. (Choi et al. 2022, 103).

Taxonomy

Intervention Categories:

- Swap Lines

Countries and Regions:

- United States

Crises:

- COVID-19