Market Support Programs

United Kingdom: Covid Corporate Financing Facility

Purpose

“…[T]o support companies which are fundamentally strong, but have been affected by a short-term funding squeeze. This will act as a vehicle to support corporates who would ordinarily seek market-based finance for their working capital, but find themselves unable to access financial markets in this uncertain operating environment” (Sunak 2020, 1)

Key Terms

-

Launch DatesMarch 17, 2020

-

Operational DateMarch 23, 2020

-

End DatePurchases: March 23, 2021 Expected maturity of holdings: March 2022

-

Legal AuthorityFinancial Services Act 2012, Part 4

-

Source(s) of FundingCentral bank reserves

-

AdministratorBank of England; Her Majesty’s Treasury

-

Overall SizeUnlimited

-

Eligible Collateral (or Purchased Assets)Sterling-denominated commercial paper with maturity between one week and 12 months

-

Peak UtilizationGBP 20.5 billion on May 20, 2020

During the COVID-19 crisis, sterling-denominated money markets froze, and otherwise-healthy companies were shut out of short-term, wholesale funding markets. To unfreeze these markets, the UK government announced a series of corporate funding measures. One of the measures was the Covid Corporate Financing Facility (CCFF), which enabled the Bank of England (BoE), acting on behalf of Her Majesty’s Treasury’s, to purchase commercial paper (CP) on primary and secondary markets from eligible dealers. The purpose of the CCFF was to provide stopgap wholesale funding to large, financially healthy firms while preserving British banks’ capacity to serve small and medium-sized companies. Under the facility, BoE created central bank reserves to buy standard CP with maturities between one week and 12 months. While BoE did not set any purchase limits, it assigned limits to individual issuers based on their credit ratings. Eligible issuers included financially healthy companies that made a material contribution to the UK economy. Eligible dealers were identified on a case-by-case basis, and all counterparties required authorization to transact with BoE under the Financial Services and Markets Act 2000. BoE conducted the CCFF in bilateral transactions and priced CP at a spread above an overnight index swap reference rate. Participating issuers were required to restrict dividends, capital distributions, and senior executive pay. Issuers were permitted to repurchase their securities prior to maturity. BoE began purchasing securities on March 23, 2020, and finished all purchases on March 22, 2021, though BoE continues to hold securities in the CCFF into March 2022. Scholars have not yet formally evaluated the CCFF.

During the early stages of the COVID-19 crisis, the United Kingdom (UK) money market experienced intensifying outflows and spreads spiked sharply (Hauser 2020). Sterling-denominated money markets froze, which deprived otherwise healthy companies of access to their normal short-term funding markets and left them with few funding options to cover salaries, rent, and taxes. In response, the Bank of England (BoE) and Her Majesty’s Treasury (HMT) created the Covid Corporate Financing Facility (CCFF) to provide funding to large, highly rated UK firms while preserving UK banks’ capacity to serve companies with worse financial outlooks, including small and medium-sized companies (Bailey 2020; BoE/HMT 2020a). As a temporary emergency measure, the CCFF was meant to offer stopgap funding to firms that were unable to finance themselves through short-term wholesale markets (Sunak 2020).

BoE designed and operated the CCFF while HMT set the facility’s risk standards and indemnified any losses (Bailey 2020; BoE 2021f). Through the CCFF, BoE purchased commercial paper (CP) via bilateral transactions with eligible dealers on both primary and secondary markets (BoE 2021a). Eligible issuers included “non-financial companies that [made] a material contribution to the UK economy” (Bailey 2020, 1; BoE 2021a, 2). Issuers had to have a short-term investment-grade rating prior to the COVID-19 outbreak or “financial health equivalent to an investment grade rating” (Bailey 2020, 2). Eligible dealers were determined on a case-by-case basis, though as a minimum requirement, they needed authorization to transact with BoE by part 4a of the Financial Services and Markets Act 2000 (FSMA) (BoE 2021a). Eligible securities included sterling-denominated CP with maturities between one week and 12 months. The purchase price was set at a spread above an overnight index swap (OIS) reference rate, and the size of the spread depended on the eligible issuer’s underlying credit quality. Though there was no aggregate limit on the potential purchases under the CCFF, BoE could set a limit for an individual company’s issuance according to its credit rating (Bailey 2020; BoE 2021a). Participating issuers had to meet restrictions on dividends, capital distributions, and senior executive pay (BoE 2021a). The facility charged fees for secondary-market purchases, early repurchases of BoE’s CCFF holdings, and other miscellaneous costs. The facility was announced on March 17, 2020, became operational on March 23, 2020, accepted new counterparty applications until December 31, 2020, and finished buying CP entirely on March 22, 2021 (BoE 2021a; BoE/HMT 2020a; UK Gov 2020).

As of February 2022, there were no formal evaluations of the CCFF.

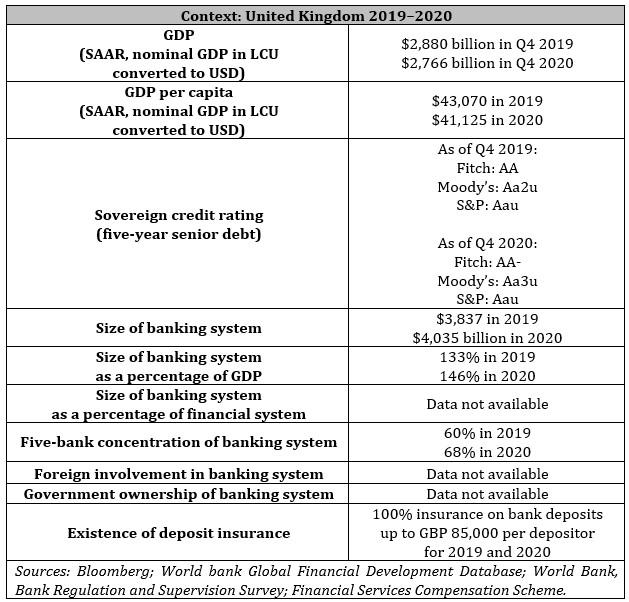

Through the CCFF, BoE lent about GBP 37 billion (USD 43 billion)FOn March 23, 2020, GBP 1 = USD 1.15 (Bloomberg). to 107 different companies and offered support to more than 200 businesses. It made all CCFF purchases on the primary market (BoE 2021d; BoE 2021e; BoE 2021f). As shown in Figure 1, weekly purchases peaked at about GBP 5.2 billion during the week of April 29, 2020 (BoE 2021e). Net amounts outstanding peaked at about GBP 20.5 billion during the week of May 20, 2020 (BoE 2021e). Approved borrowings stood at nearly GBP 10 billion at the beginning of April 2020, increased to GBP 80 billion by mid-July, and hovered between GBP 80 billion and GBP 85 billion through January 2021 (BoE 2021d). As a proportion of approved borrowings, the actual borrowings peaked on May 20, 2020, at 34%, before gradually trending downward to 14% by January 27, 2021. The UK’s industrial and transport and consumer and cyclical sectors together represented more than 70% of the CCFF’s primary issuers through January 2021.

Throughout the CCFF’s purchase window, HMT and BoE described the facility as a measure to sustain employment in the UK (HMT 2021a). In May 2020, BoE estimated that the companies potentially eligible for the CCFF could account for 28% of total turnover and 14% of aggregate employment in the UK (BoE FPC 2020a). Between March 2020 and March 2021, the CCFF provided more than GBP 34 billion to businesses responsible for 2.5 million jobs in the United Kingdom (HMT 2021b).

Figure 1: CCFF Commercial Paper Holdings (in GBP billions)

In a June 2020 speech, Andrew Hauser, BoE’s executive director of markets, said that the CCFF “deepen[ed] the CP market” because the sterling-denominated CP issuance under the CCFF was three times larger than before the COVID-19 crisis (Hauser 2020, 10). Hauser said that conditions in core funding markets had normalized by mid-2020, as large UK firms had been able to return to private debt markets.

From January through September 2020, UK corporations raised more funding than in previous years (BoE MPC 2020b). UK firms raised about GBP 70 billion between March and August 2020, with positive trends in both equity issuance and borrowing from banks (BoE FPC 2020b; BoE MPC 2020b). Corporate borrowing rates generally fell after the introduction of various government schemes in March 2020 (BoE MPC 2020a). UK companies stopped issuing corporate bonds during the first half of March, but issuance resumed during the second half and sharply increased in April (BoE FPC 2020a). Overall, UK monetary and financing conditions eased slightly between May and August 2020 (BoE MPC 2020a).

Key Design Decisions

Purpose

1

Chancellor of the Exchequer Rishi Sunak and Bank of England Governor Andrew Bailey characterized the Covid Corporate Financing Facility as a stopgap measure for corporate funding (Bailey 2020; Sunak 2020). The CCFF was meant to temporarily support corporations by stimulating both primary and secondary markets for commercial paper (Sunak 2020). The CCFF’s target recipients were fundamentally secure companies that usually financed their working capital through short-term funding markets but found themselves unable to access financial markets during the COVID-19 uncertainty.

In March 2020, Bailey anticipated that the evolving COVID-19 shock would rattle supply chains and stifle economic activity, disrupting cash flows for British corporations during a period of high demand for corporate credit (Bailey 2020). The BoE launched the CCFF to help businesses continue to pay regular operational expenses, such as salaries, rents, and supplier invoices. By directly intervening in short-term credit markets, the BoE attempted to preserve the banking system’s lending capacity for a variety of bank-dependent companies, such as small and medium-sized enterprises (SMEs) (Bailey 2020; BoE/HMT 2020a).

Part of a Package

1

One week before announcing the CCFF on March 17, 2020, BoE and Her Majesty’s Treasury revealed measures meant to support banks’ lending capacity, including the Term Funding Scheme with additional incentives for lending to SMEs (TFSME) and a reduction in the UK countercyclical capital buffer rate to 0% (BoE/HMT 2020a). On March 23, 2020, HMT also established the Coronavirus Business Interruption Loan Scheme, which indirectly funded businesses and guaranteed the value of loans provided by participating banks (UK Gov 2020). On April 20, 2020, the UK government launched the Coronavirus Future Fund, which provided convertible loans to companies unable to access other government loan programs because they did not yet have revenues or profits (DBEIS/HMT/BBB 2020). UK authorities also announced the Bounce Back Loan Scheme, which guaranteed loans to SMEs, on April 27, 2020 (DBEIS 2020).

Legal Authority

1

Primary CCFF documents do not identify the legal authority on which the program relied. The Financial Services Act 2021 (FSA 2012) and a related memorandum of understanding (MoU) describe the procedures under which the Bank of England may provide crisis support to financial institutions with indemnification from HMT (HMT 2017). They do not mention the possibility that a BoE crisis program would support nonfinancial corporations. Still, BoE and HMT followed similar procedures in creating the CCFF program. As the legislation requires for BoE crisis programs that utilize HMT funds, the BoE governor and the chancellor exchanged letters describing their agreement about the purpose of the program and clarifying the roles of their respective organizations (Bailey 2020; HMT 2017; Sunak 2020).

Both letters make clear that the CCFF was an HMT program, not a BoE program. BoE Governor Bailey’s letter to Chancellor Sunak notes that the CCFF was “HM Treasury’s facility, with the Bank providing agency services to HM Treasury under an agency agreement” (Bailey 2020, 1). Both letters identify support for nonfinancial corporations as the primary goal of the program. However, Bailey’s letter also identifies a broader financial stability purpose, noting that it would “help to retain the capacity of the banking system to lend to a much broader range of companies” (Bailey 2020, 1).

Detailed policies and procedures for BoE crisis support to financial institutions are described in Part 4 of FSA 2012 and the related MoUFThis MoU represents the HMT’s, BoE’s, and Prudential Regulatory Authority’s (PRA’s) interpretation of each entity’s crisis-related responsibilities. In the wake of the Global Financial Crisis, the UK government enacted regulatory reforms through FSA 2012 (Metrick and Rhee 2018). Part 4 of FSA 2012 describes collaboration among HMT, BoE, PRA, and the Financial Services Authority (FSA 2012). Section 65 of Part 4 requires HMT to publish an MoU outlining the regulators’ plans to comply with FSA 2012 during a crisis (FSA 2012). on Resolution Planning and Financial Crisis Management. While BoE has “primary operational responsibility for financial crisis management,” HMT has “sole responsibility for any decision involving public funds” (HMT 2017, 1). HMT can grant additional operational abilities to BoE during crisis circumstances via its powers of direction, which HMT can exercise only after meeting two conditions. First, the BoE Governor must immediately notify HMT in writing if BOE suspects that HMT might need to use public funds to provide financial assistance or support related to financial institutions (FSA 2012). Second, after consulting with the BoE governor, the chancellor can then exercise HMT’s power of direction on determining that a directed measure is “either a necessary response to a serious threat to financial stability, or where financial assistance has already been provided in respect of a firm to resolve or reduce such a serious threat, necessary to protect the public interest” (HMT 2017, 8).

The MoU also describes how HMT could direct BoE to form a special purpose vehicle (SPV), BoE’s discretion in offsetting newly created central bank reserves, and HMT and BoE’s communicative responsibilities. For more information about the CCFF’s SPV, governance measures, and source of funding, please refer to Key Design Decision No. 5, Administration, No. 8, Use of SPV, and No. 10, Source(s) of Funding.

Governance

1

BoE and HMT officials met regularly to oversee BoE’s operation of the CCFF, identify risks to the public sector balance sheet, and review the potential effects on specific sectors and markets (BoE 2021f). The CCFF followed several of BoE’s corporate governance arrangements that the CCFF board determined were appropriate for policy goals and applicable to the facility.

Because HMT bore the ultimate risk of the CCFF, BoE operated under a Financial Risk Management Framework that reflected HMT’s risk standards to develop an investment strategy that would “[minimize] overall risk through the appropriate choice of portfolio and risk management practices” (BoE 2021f, 5). The framework describes broad risk parameters such as eligible asset classes, investment limits, credit risk, and counterparties, as well as procedures for undertaking transactions, monitoring risk, accounting, and making payments.

The CCFF’s board met quarterly to review the CCFF’s financial, legal, operational, and risk updates. The board annually reviewed an Internal Control Framework, which covered everyday governance and decision-making, implementation of CCFF operations, BoE’s support processes, and risk management and controls.

Administration

1

Though CCFF was HMT’s facility, BoE owned and ran the subsidiary, the Covid Corporate Financing Facility Limited (CCFFL),FFor simplicity, this case refers to BoE—rather than the subsidiary itself—when describing actions taken by the CCFFL’s directors. on HMT’s behalf (Bailey 2020; BoE 2021a). Under an agency agreement, BoE served as HMT’s operating agent in lending markets, so BoE operated the CCFF by creating and implementing the infrastructure and support necessary to execute CCFF operations, which were either provided by BoE or solicited from third parties by BoE (Bailey 2020; BoE 2021f; Sunak 2020). BoE coordinated with HMT on eligibility criteria, guidelines, and controls, and BoE executed the CCFF’s day-to-day functions and transactions (BoE 2021f). BoE also processed the CCFF applications (BoE 2021a). Four BoE officialsFThis group included BoE’s executive directors for financial stability; banking, payments, and innovation; markets; and the chief financial officer (BoE 2021f). served as CCFF directors during its year of operation; their role was to maintain clear processes for monitoring and managing risk (BoE 2021f). BoE’s Financial Risk Management Division analyzed the CCFF’s financial risks and BoE’s Financial Risk and Resilience Division was responsible for CCFF’s risk decisions and management frameworks.

Under FSA 2012, HMT is able to fund an emergency program in an amount equal to its real or anticipated expenses (FSA 2012). HMT indemnified BoE’s actions under the CCFF, so BoE was neither responsible for any losses or expenses incurred from the facility nor owed any profit generated from the facility to HMT (Bailey 2020; BoE 2021f). HMT also created the CCFF’s risk management framework and made final decisions about an individual participant’s admission into the facility (Bailey 2020). HMT also reserved the right to change any company’s terms of access (including drawing limits) to the CCFF at any time (BoE/HMT 2020f).

Freshfields Bruckhaus Deringer LLP (Freshfields) is an international law firm that advised BoE on all legal aspects of the CCFF, prepared the terms by which corporations issued commercial paper to the CCFF, negotiated all the legal agreements between BoE and HMT, and assisted with BoE’s internal documentation (Freshfields n.d.).

Communication

1

On March 17, 2020, Rishi Sunak and Andrew Bailey publicly exchanged letters in which they describe the CCFF as a temporary funding measure meant to alleviate cash flow shortages faced by businesses that were otherwise healthy, enabling them to continue paying wages, rent, and supplier fees (Bailey 2020; Sunak 2020). The officials suggest that by offering an alternative source of financing, the program would also preserve the banking system’s capacity to lend to small and medium-sized enterprises (Bailey 2020; Sunak 2020). On the same day, BoE and HMT announced the facility’s launch in a news release and said that the CCFF would broadly help “UK businesses and households to bridge a temporarily difficult period and thereby to mitigate any longer-lasting effects of Covid-19 on jobs, growth, and the UK economy” (BoE/HMT 2020a).

Disclosure

1

In his CCFF announcement letter, Rishi Sunak copied the prime minister, chair of the Treasury Committee, and chair of the Public Accounts Committee (Sunak 2020). BoE and HMT were also responsible for communicating relevant crisis information to the public (HMT 2017).

Beginning June 4, 2020, BoE published on a weekly basis the names of corporations whose commercial paper was sold to the facility as part of an effort to make the CCFF more transparent (BoE/HMT 2020c).

SPV Involvement

1

HMT directed BoE to create a special purpose vehicle, separate from BoE’s balance sheet, for BoE to conduct the special market assistance. This is in line with the BoE-HMT MoU on assistance to financial institutions involving HMT funds (HMT 2017). HMT indemnified BoE and the SPV, and decided how the SPV ought to be financed: HMT could issue debt, BoE could lend to the SPV while HMT provided its share capital, or HMT and BoE could find another way to fund the program. The Covid Corporate Financing Facility Limited was funded by BoE’s loan and nominal capital, while HMT’s indemnity covered the facility’s losses (BoE 2021f). If BoE was directed to lend to the SPV, BoE decided whether and how to offset the subsequent expansion of central bank reserves, similarly to how it independently conducts monetary policy (HMT 2017). CCFF was financed by the creation of central bank reserves (BoE/HMT 2020b).

CCFFL became a wholly owned subsidiary of BoE on March 19, 2020 (BoE 2021f). The CCFFL was originally incorporated by solicitors acting on BoE’s behalf, on May 16, 2019, under the original name “Freshfields 01 Limited.” Freshfields advised BoE on all legal aspects of the CCFF and created the new subsidiary (Freshfields n.d.). After Freshfields 01 Limited stayed dormant during 2019, Michael Raffan, a partner at Freshfields, served as a director during BoE’s reception on March 19, 2020, and resigned on the same day that the subsidiary was renamed to CCFFL (BoE 2021f).

Program Size

1

The facility did not have an overall size limit or a cap to the total amount of CP that BoE could purchase within a day (BoE 2021a; Sunak 2020). BoE’s Monetary Policy Committee (MPC) said that the aggregate amount of CCFF asset purchases financed by central bank reserves would inform the MPC’s decisions about non-CCFF purchases of government and corporate bonds (Bailey 2020).

BoE did limit primary market purchases of CP by each issuer (BoE/HMT 2020b). Upon request, BoE could reveal these limits to the relevant individual issuers and the eligible dealers acting on the issuer’s behalf (BoE 2021a). If two or more issuers belonged to the same group or were affiliates of each other, BoE could apply a single aggregate limit rather than multiple underlying limits.

Beginning on October 9, 2020, any issuer whose long-term credit rating was at or below BBB-/Baa3/BBB (low) after March 1, 2020, faced a maximum drawing limit of GBP 300 million (BoE/HMT 2020f). Participants with outstanding drawings above GBP 300 million were exempt from the updated drawing limits.

Source(s) of Funding

1

Because HMT directed BoE to lend to the SPV, BoE decided whether and how to offset the subsequent expansion of central bank reserves, similarly to how it independently conducts monetary policy (HMT 2017). CCFF purchases were financed by central bank reserves (BoE/HMT 2020b). To purchase commercial paper, BoE credited counterparties’ reserve accounts with reserves, which appeared as a liability to BoE, in exchange for commercial paper, which was an asset transferred to the CCFFL. By paying for the securities that showed up as assets in its subsidiary, BoE in effect made a loan to the CCFFL. CCFFL repaid the loan from BoE when the commercial paper matured or was repaid early; CCFFL accrued interest charges on the loan and repaid them all after the CCFF closed (BoE 2021f). The difference between the fair value of CCFFL’s assets and liabilities were covered by HMT’s indemnity.

HMT’s indemnity counted as a contingent liability on HMT’s balance sheet; losses crystallized if a participant defaulted on commercial paper issued into the CCFF (BoE 2021f).

Eligible Institutions

1

Eligible issuers. Under the CCFF, eligible issuers included “companies or limited liability partnerships (LLPs) (in each case, including their finance subsidiaries) that make a material contributionF“Material contribution” generally referred to companies and LLPs incorporated in the UK or foreign-incorporated parents with “genuine business” in the UK (BoE 2021a). Companies and LLPs could also meet this requirement by having a significant number of employees, revenue, customers, or operating sites in the UK. to economic activity in the UK,” as determined by BoE’s risk management staff (BoE 2021a, 2). The CCFF was potentially open to companies and LLPs that had no history of issuing CP but were capable of doing so. Ineligible issuers included:

- Public bodies or authorities, or entities partially owned by public bodies or authorities;

- Banks, building societies, insurance companies, and other financial institutions regulated by BoE or the Financial Conduct Authority;

- Leveraged investment vehicles; and

- Companies or LLPs within groups whose main lines of business are subject to financial regulation.

Eligible issuers were required to have a short-term investment-grade rating prior to the pandemic from at least one rating agencyFInvestment-grade ratings include minimum short-term credit ratings of A-3/P-3/F-3/R-3 or long-term credit ratings of BBB-/Baa3/BBB-/BBB from at least one of Standard & Poor’s, Moody’s, Fitch, or DBRS Morningstar. or otherwise demonstrate their financial health (BoE 2021a; BoE/HMT 2020e). Issuers with split ratings, where one or more rating agency rated their short-term credit below the minimum, were ineligible (BoE 2021a).

If a short-term credit rating was unavailable, BoE considered whether a long-term credit rating could be used for CCFF eligibility and pricing, or BoE independently determined whether the issuer exhibited sufficient financial health. BoE and HMT considered an issuer’s eligibility at the lowest rating (of negative watch or outlook) as of March 1, 2020.

An issuer that did not have a public investment-grade rating could seek banks’ internal ratings or a credit quality assessment from one of the major credit rating agencies—each of which needed to be dated March 1, 2020, and shared (privately, if needed) with BoE and HMT (BoE/HMT 2020e). Issuers opting for banks’ internal ratings normally needed at least three investment-grade and no speculative ratings.FExceptions included issuers with average ratings of at least BBB/Baa2/BBB/BBB or two bank ratings of at least BBB+/Baa1/BBB+/BBB (BoE/HMT 2020e). BoE also requested that banks’ internal ratings be sent in a form clearly indicating that the ratings came from the banks and not the issuers themselves.

With effect on October 9, 2020, BoE and HMT updated the credit quality review process for new issuance into the CCFF to minimize the risk of issuers defaulting under the program (BoE 2021f; BoE/HMT 2020f). After the update, applicants and participants were required to keep continuously high credit ratings from March 1, 2020, through the date of application (BoE/HMT 2020f). Eligible issuers were required to maintain current investment-grade credit ratings: the short-term equivalent of at least A3/P3/F3/R3 or a long-term equivalent of at least BBB-/Baa3/BBB-/BBB. If an issuer’s credit rating fell below investment grade, they could request a review with HMT, which determined the issuer’s eligibility according to the facility’s purpose: to “provide short term liquidity support to fundamentally strong businesses” (BoE/HMT 2020f, 2).

Eligible issuers were allowed to access only one of the UK’s following support programs: the CCFF, the Coronavirus Large Business Interruption Loan Scheme, the Coronavirus Business Interruption Loan Scheme, or the Bounce Back Loan Scheme (BoE 2021g). This restriction did not apply to other programs, such as the Coronavirus Job Retention Scheme.

Eligible issuers in the primary market had to sign and submit an issuer undertaking and confidentiality agreement, provide evidence of authority to sign in a form acceptable to BoE, and complete and submit an Issuer Eligibility Form – Primary Market) (BoE 2020a; BoE 2021a). Eligible issuers also had to guarantee that the CCFF securities ranked at least pari passu with their other senior unsecured debt from the same group (BoE 2021a). BoE had to be able to recognize and rely on the guarantee; eligible issuers also had to provide a legal opinion about the guarantee that BoE, the CCFF, and HMT could reference.

Beginning on October 9, 2020, eligible issuers had to take additional steps before issuing new CP to the CCFF, in line with the updated credit quality review (BoE/HMT 2020f). Eligible issuers had to notify BoE at least five business days ahead of the requested sale date; BoE confirmed in the interim whether the transaction could proceed. The notification needed to include evidence of an investment-grade credit rating. If the eligible issuer had a point-in-time rating from a recognized credit rating agency, their rating must have been dated no earlier than eight weeks before the proposed sale date. If an issuer pursued a review with HMT, HMT could take up to six weeks to conduct the review before reporting the outcome to the issuer; HMT also had sole discretion to allow the issuer to issue into the CCFF during the review period.

After reviewing available information, either BoE or HMT could declare any business ineligible for the CCFF for any reason (BoE/HMT 2020f). HMT reserved the right to change the terms of access to the CCFF for any business at any time.

On September 22, 2020, BoE and HMT announced that applications to become eligible dealers or issuers for the CCFF would close on December 31, 2020 (BoE/HMT 2020d). Issuers that were already accepted into the CCFF were still able to issue new CP to the CCFF until the facility’s date of closure (BoE/HMT 2020e).

Eligible Dealers. BoE identified eligible dealers for the CCFF on a case-by-case basis (BoE 2021a). To become a CCFF counterparty, dealers needed to be authorized according to Part 4a of the Financial Services and Markets Act 2000 (BoE 2021a; FSMA 2000).

Eligible dealers had to complete and submit the CCFF Application Form and, if they were accepted, sign and return an Admission Letter (BoE 2021a). If a dealer sought to sell CP in the secondary market through the CCFF, BoE could require them to first complete the Issuer Eligibility Form – Secondary Market (BoE 2021a; BoE 2020b).

Auction or Standing Facility

1

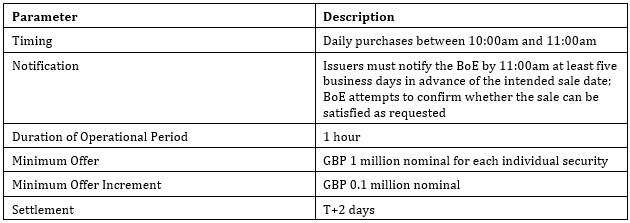

All CP purchases were bilateral transactions without limits on BoE’s daily purchases (BoE 2021a). Before counterparties could submit offers to the CCFF, BoE had to confirm securities were eligible. The facility operated according to the purchase parameters described in Figure 2.

Figure 2: CCFF Purchase Parameters

For primary market purchases, counterparties had to offer details about the issuer, the facility from which the CPs were issued, the maturity date,FMaturity dates had to adhere to the “modified following convention,” which means that interest payments falling on nonbusiness days (that is, holidays and weekends) had to arrive on the following business day (BoE 2021c, 16). If the following business day fell in the next calendar month, then the interest payments had to arrive on the preceding business day. and the nominal amount offered (BoE 2021a). BoE’s sterling desk confirmed “as soon as reasonably practical” whether an offer had been accepted; BoE confirmed the cash amount and, for primary market purchases, the maturity date (BoE 2021a, 7). After a primary market offer was accepted, the counterparty ought to have confirmed the ISIN of the new CP issued as soon as possible (BoE 2021a). For an individual eligible issuer, BoE purchased CP on the primary market from only one eligible dealer each day; issuers were expected to arrange their issuance such that only one eligible dealer sold CP to the CCFF on any given day (BoE 2021a). BoE had the right to cancel or postpone an operational period at any time (BoE 2021a).

For secondary market purchases, counterparties had to provide BoE with the security’s ISIN and ticker, the original issue price and date (or money market yield on an amortized cost basis), the maturity date, and the nominal amount offered (BoE 2021a). Counterparties received a similar confirmation from BoE for secondary market purchases.

BoE sent the transaction confirmations via email on the day of the transaction (BoE 2021a). The counterparty had to identify any discrepancies within 24 hours. If a CCFF security did not mature on the agreed maturity date due to the eligible issuer’s error, BoE could charge the issuer a late payment equal to “valuation equivalent to the extended maturity plus a flat fee of 0.2 [basis points (bps)] on the nominal size of the transaction” (BoE 2021a). As described in the CCFF Terms and Conditions, counterparties had to reimburse BoE all their costs, charges fees, and other expenses, including transfer taxes, registration charges, and value-added taxes incurred in connection with the transfer of securities.

Loan or Purchase

1

On March 17, 2020, HMT authorized BoE to lend funds to an SPV through which the BoE purchased both newly issued CP in the primary market and after issuance in the secondary market—all from eligible dealers (BoE 2021f; BoE/HMT 2020e). BoE purchased all CP at a spread over reference rates (BoE/HMT 2020e).

Eligible Collateral or Assets

1

Under the CCFF, BoE purchased sterling-denominated CP with the following features:

- Maturity between one week and 12 months, if issued to BoE at-issue by a dealer; drawings could be rolled while the CCFF was open, subject to eligibility;

- Issued directly into Euroclear and/or Clearstream;

- Met International Capital Market Association (ICMA) standards, was governed by English law, and subject to English courts;

- Accompanied by a security guarantee, if requested by BoE (as described in Key Design Decision No. 10, Source(s) of Funding). (BoE 2021a)

BoE could not approve CP with certain nonstandard features, such as extendibility or subordination (BoE 2021a). BoE confirmed eligibility bilaterally with the relevant issuer. BoE and HMT had the right to deem any security ineligible for any reason—including securities that BoE had previously purchased if BoE later deemed them ineligible. BoE did not have the right to:

- Cancel any CP (irrespective of ineligibility);

- Change the terms of any CP purchased under the CCFF; or

- Force the issuer to repurchase newly ineligible CP. (BoE 2021a)

Loan Amounts (or Purchase Price)

1

BoE purchased CP at a spread above a reference rate, which was based on the current sterling overnight index swap curve (BoE 2021a). The CCFF spreads were meant to resemble market spreads before the COVID-19 crisis.

Primary market CP purchases relied on a discount rate based on the maturity-matched OIS rate, determined by BoE on the date of the transaction. BoE determined the respective reference OIS rate at 9:45am on the date of operation. BoE also applied money market yield conventions. The spread between the reference rate and the CP depended on the eligible issuer’s credit rating; BoE communicated this spread through its website and the sterling desk. If an issuer had a split rating, BoE used the lowest rating to determine the spread. BoE set the spreads above OIS at the rates indicated in Figure 3.

Figure 3: CCFF Spreads above OIS Reference Rate

Secondary market CP purchases occurred at the lower of: (1) amortized cost from the issue price, and (2) the price implied by the method used for primary market purchases (BoE 2021a). On July 1, 2020, BoE added a fee to each secondary market purchase, equal to 5 bps on the yield on the transaction (BoE 2021b; BoE/HMT 2020e).

The pricing schedule was made available on March 23, 2020, the date on which the facility became operational (BoE/HMT 2020e). All trade pricing was rounded to three decimal points (BoE 2021a).

Haircuts

1

There were no haircuts applicable to the CCFF.

Interest Rate

1

There were no interest rates applicable to the CCFF.

Fees

1

If a CCFF security did not mature on the agreed-upon maturity date due to the eligible issuer’s error, BoE could charge the issuer a late payment equal to “valuation equivalent to the extended maturity plus a flat fee of 0.2 [bps] on the nominal size of the transaction” (BoE 2021a, 10). As described in the CCFF Terms and Conditions, counterparties had to reimburse BoE all their costs, charges fees, and other expenses, including transfer taxes, registration charges, and value-added taxes incurred in connection with the transfer of securities.

On July 1, 2020, BoE added a fee to each secondary market purchase, equal to 5 bps on the yield on the transaction (BoE 2021b; BoE/HMT 2020e).

BoE usually assigned an additional fee for early repayments, which was deducted from the yield offered in the resale before BoE determined the final price and cash process (BoE 2021a). Early repurchases made between May 19 and June 30, 2020, were exempt from this fee (BoE/HMT 2020e). The minimum size of securities that the facility could sell back to the original seller was set at the lower of: (1) GBP 1 million nominal or (2) the full amount held in the CCFF (BoE 2021a). The resale amounts needed to be expressed in increments of GBP 0.1 million nominal.

Term

1

Terms were not applicable under the CCFF.

Other Conditions

1

To minimize the likelihood of CCFF participants’ default, BoE and HMT required businesses that wanted to issue debt with a term past May 19, 2021, to first send a letter to HMT describing their commitment to restraining dividends, capital distributions, and senior executive pay if their CP was outstanding (BoE 2021f; BoE/HMT 2020c). This requirement also applied to active program participants who had successfully increased their outstanding CCFF drawing limitsFBoE and HMT’s October 9, 2020, joint market notice adds an investment-rating qualifier: “Issuers will be required to provide a letter of commitment in relation to [capital distributions and senior executive pay] if an increase in an issuer’s CCFF limit, over and above that suggested by the issuer’s investment rating, is requested and approved . . .” (BoE/HMT 2020e, 4). (BoE/HMT 2020d). Exceptions included LLPs that had to pay partners. LLPs could remunerate partners at a level that HMT deemed appropriate, relative to payment distributions from the 2019–2020 financial year (BoE 2021g). The purpose of these letters of commitment was to incentivize and enable companies to repay any CCFF borrowings that were scheduled to mature after the facility had closed to new drawings (BoE/HMT 2020c). HMT had the right to publish these letters of commitment if HMT became aware that the company did not comply with the letter’s terms (BoE 2021a). On September 22, 2020, BoE and HMT clarified that the deadline for submitting letters of commitment was December 31, 2020 (BoE/HMT 2020d).

Regulatory Relief

1

There was no regulatory relief applicable to the CCFF.

International Cooperation

1

There was no international coordination applicable to the CCFF.

Duration

1

On March 18, 2020, BoE and HMT stated in a market notice that the CCFF was supposed to last 12 months and that BoE would notify the public of the closure date six months in advance (BoE/HMT 2020b). BoE stressed that applications to sell CP (either as an issuer or as a dealer) would have to be received and accepted by December 31, 2020 (BoE/HMT 2020d). On September 22, 2020, BoE circulated the program’s intended date of closure: March 23, 2021 (BoE/HMT 2020d). While BoE purchased securities with maturities dated later than March 23, 2021, BoE did not purchase CP (irrespective of maturity date) after March 22, 2021.

Key Program Documents

-

(Bailey 2020) Bailey, Andrew. Letter to Rishi Sunak. March 17, 2020. “Letter about Launch of the Covid Corporate Financing Facility (CCFF).”

Describes the origin and purpose of the CCFF.

-

(BoE 2021g) Bank of England (BoE). August 20, 2021. “Covid Corporate Financing Facility (CCFF).”

Provides information about the CCFF, including commons questions and answers.

-

(Sunak 2020) Sunak, Rishi. March 17, 2020. “Letter about Launch of the Covid Corporate Financing Facility (CCFF).” Letter to Andrew Bailey.

Describes the origin and purpose of the CCFF.

-

(BoE 2020a) Bank of England (BoE). 2020. “COVID Corporate Financing Facility (CCFF) Issuer Eligibility Form – Primary Market.”

Serves as the application for primary market issuers to participate in the CCFF.

-

(BoE 2020b) Bank of England (BoE). 2020. “COVID Corporate Financing Facility (CCFF) Issuer Eligibility Form – Secondary Market.”

Serves as the application for secondary market participants to enroll in the CCFF.

-

(BoE 2021a) Bank of England (BoE). March 11, 2021. “The Covid Corporate Financing Facility (CCFF): CCFF Operating Procedures.”

Describes in detail the operational details of the CCFF, including eligibility, applications, and closure of the program, CCFF operations, and settlement processes.

-

(BoE 2021b) Bank of England (BoE). July 13, 2021. “Bank of England Market Operations Guide: Information for Participants.”

Web page containing links to the relevant information about the BoE’s various programs. The page is meant for prospective and current market participants.

-

(BoE 2021c) Bank of England (BoE). July 2021. “Best Practice Guide for GBP Loans: The Working Group on Sterling Risk-Free Reference Rates.”

Defines “modified following convention” in relation to maturity dates and interest payments of securities, which applied to assets purchased by BoE through the CCFF.

-

(FSA 2012) Financial Services Act 2012 (FSA). 2012.

Describes the actions that must be taken by the BoE, HMT, and other regulators during a financial crisis. The FSA 2012 includes language about the procedures under which the BoE may provide crisis support to financial institutions with indemnification from HMT.

-

(FSMA 2000) Financial Services and Markets Act 2000 (FSMA). 2000.

Describes the legal authorization required for counterparties to transact with the BoE. Part 4a of the FSMA 2000 addresses dealer criteria.

-

(HMT 2017) Her Majesty’s Treasury (HMT). October 2017. “Memorandum of Understanding on Resolution Planning and Financial Crisis Management.”

Describes the roles and responsibilities of HMT, the BoE, and other British financial regulators after the Global Financial Crisis. The FSA 2012 required HMT to publish this MoU as part of the UK’s larger efforts to prepare for future financial crises.

-

(BoE 2021e) Bank of England (BoE). August 25, 2021. “Covid Corporate Financing Facility (CCFF) Data.”

Exhibits BoE’s weekly purchases through the CCFF.

-

(BoE/HMT 2020a) Bank of England and Her Majesty’s Treasury (BoE/HMT). March 17, 2020. “HM Treasury and the Bank of England Launch a Covid Corporate Financing Facility (CCFF).” Press release.

Announces the CCFF as a joint program between BoE and HMT and describes the program in broad details.

-

(BoE/HMT 2020b) Bank of England and Her Majesty’s Treasury (BoE/HMT). March 18, 2020. “Joint HM Treasury and Bank of England Covid Corporate Financing Facility (CCFF).”

Announces the creation of the CCFF and includes major program details: operation, length, financing, eligible issuers, eligible securities, limits on the BoE’s holdings, eligible counterparties, prices, submission of offers, settlement arrangements, and other published information.

-

(BoE/HMT 2020c) Bank of England and Her Majesty’s Treasury (BoE/HMT). May 19, 2020. “Update to the Covid Corporate Financing Facility - 19 May 2020.”

Updates CCFF participants on new requirements: (1) participants with terms extending beyond May 19, 2021, had to commit in writing to restricting dividends, capital distributions, and senior executive pay; and (2) participants became able to withdraw their CCFF borrowings early.

-

(BoE/HMT 2020d) Bank of England and Her Majesty’s Treasury (BoE/HMT). September 22, 2020. “Update on the Covid Corporate Financing Facility (CCFF) - Market Notice 22 September 2020.”

Updates CCFF participants on: (1) the closure date of the CCFF, and (2) the deadline for letters of commitment to joining the CCFF.

-

(BoE/HMT 2020e) Bank of England and Her Majesty’s Treasury (BoE/HMT). October 9, 2020. “Joint HM Treasury and Bank of England Covid Corporate Financing Facility (CCFF) - Consolidated Market Notice 9 October 2020.”

Describes the CCFF’s operation and updates the effective provisions for joining the program.

-

(BoE/HMT 2020f) Bank of England and Her Majesty’s Treasury (BoE/HMT). October 9, 2020. “Update on the Covid Corporate Financing Facility (CCFF) - Market Notice 9 October 2020.”

Updates CCFF participants on: (1) program closure date, (2) credit quality review for new issuance, (3) process for new issuance, (4) drawing limits, (5) maintaining current drawings, and (6) further information.

-

(BoE 2021d) Bank of England (BoE). February 2, 2021. “Our Support for Large Employers Affected by the Covid Crisis.”

Describes the participation of large British employers in the CCFF, including issuance according to industry/sector and borrowed amounts.

-

(DBEIS 2020) Department for Business, Energy & Industrial Strategy (DBEIS). April 27, 2020. “Apply for a Coronavirus Bounce Back Loan.”

Describes the application process for the Coronavirus Bounce Back Loan, a corporate support measure launched at a time near the CCFF’s start.

-

(DBEIS/HMT/BBB 2020) Department for Business, Energy & Industrial Strategy, Her Majesty’s Treasury, and British Business Bank (DBEIS/HMT/BBB). April 20, 2020. “Apply for the Coronavirus Future Fund.”

Describes the application process for the Coronavirus Future Fund, a corporate support measure launched at a time near the CCFF’s start.

-

(Freshfields n.d.) Freshfields Bruckhaus Deringer LLP (Freshfields). n.d. “Bank of England CCFF: Extending a Lifeline to UK Businesses.” Accessed October 18, 2021.

Describes a British law firm’s involvement with the creation of the CCFFL.

-

(HMT 2021a) Her Majesty’s Treasury (HMT). March 25, 2021. “Government-Backed Loans Help Thousands of Businesses to Protect Jobs During Pandemic.”

Describes the CCFF, in conjunction with other corporate support measures, in terms of the number of jobs and employers assisted.

-

(UK Gov 2020) United Kingdom Government (UK Gov). March 23, 2020. “Coronavirus - Business Support to Launch from Today.”

Describes the CCFF as one of several government support measures meant to reinforce the British workforce and economy.

-

(Hauser 2020) Hauser, Andrew. June 5, 2020. “Seven Moments in Spring: Covid-19, Financial Markets and the Bank of England’s Balance Sheet Operations.” Speech given to Bloomberg in London, England. Bank of England.

Speech describing the effects of the BoE’s market intervention on gilt and corporate bond activity.

-

(Metrick and Rhee 2018) Metrick, Andrew, and June Rhee. September 14, 2018. “Regulatory Reform.” Annual Review of Financial Economics 2018, no. 10: 153–72.

Describes the steps taken by British authorities to correct the financial regulatory landscape after the Global Financial Crisis.

-

(BoE 2021f) Bank of England (BoE). June 17, 2021. “Covid Corporate Financing Facility Limited Annual Report and Accounts: 1 March 2020 - 28 February 2021.”

Describes the activities and holdings of the CCFFL between 2020 and 2021.

-

(BoE FPC 2020a) Bank of England, Financial Policy Committee (BoE FPC). May 6, 2020. “Interim Financial Stability Report.”

Describes the financial stability conditions across the United Kingdom during the outbreak of COVID-19.

-

(BoE FPC 2020b) Bank of England, Financial Policy Committee (BoE FPC). August 2020. “Financial Stability Report August 2020.”

Describes corporate activity of UK firms in early to mid-2020.

-

(BoE MPC 2020a) Bank of England, Monetary Policy Committee (BoE MPC). August 2020. “Monetary Policy Report August 2020.”

Describes corporate activity of UK firms in early to mid-2020.

-

(BoE MPC 2020b) Bank of England, Monetary Policy Committee (BoE MPC). November 5, 2020. “Monetary Policy Report November 2020.”

Describes corporate activity of UK firms in early to mid-2020.

-

(HMT 2021b) Her Majesty’s Treasury (HMT). March 3, 2021. Budget 2021: Protecting the Jobs and Livelihoods of the British People.

Describes the number of businesses and employees supported by the CCFF.

Taxonomy

Intervention Categories:

- Market Support Programs

Countries and Regions:

- United Kingdom

Crises:

- COVID-19