Broad-Based Emergency Liquidity

Thailand: Financial Institutions Development Fund Liquidity Support

Purpose

“to provide financial assistance to troubled financial institutions, containing financial damages and mitigating the threat to stability of the financial institution system” (BOT n.d.)

Key Terms

-

Launch DatesFebruary 1997 (operational); August 1997 (announcement of restructuring plan); December 1997 (permanent closure of 56 finance companies)

-

Expiration DateJanuary 1998

-

Legal AuthorityOne emergency decree in 1985 authorizing the facility; another in 1997 authorizing FIDF to relinquish collateral

-

Peak OutstandingTHB 434 billion in August 1997

-

ParticipantsUp to 91 nonbank finance companies and four commercial banks

-

RateUnknown

-

CollateralTHB 800 billion from finance companies in government bonds and promissory notes

-

Loan DurationLoan maturities unknown

-

Notable FeaturesSupport not disclosed, funded by repos

-

Outcomes56 of 58 suspended finance companies closed; FIDF lost THB 244 billion, ultimately paid by banks and taxpayers

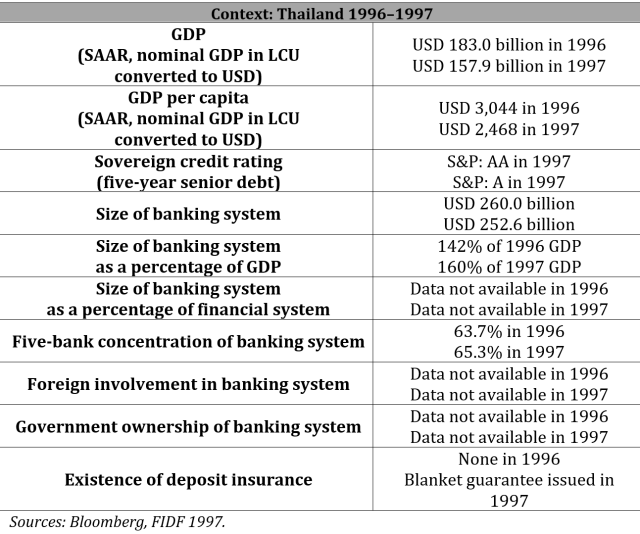

International investors launched three speculative attacks on the Thai baht in 1996 and 1997 following one high-profile banking failure, constant departures from the Bank of Thailand (BOT), and slumping returns on stocks and real estate. Though the BOT succeeded in the baht’s defense, the BOT’s depleted reserves were unable to fend off domestic troubles that emerged in early 1997. The speculative attacks increased the cost of foreign-denominated debt—which accounted for 18% of all bank lending—and forced up interbank lending yields. The decade-long boom in foreign capital inflows had generally overvalued assets, and banks found themselves in need of outside financing to meet short-term obligations. The Financial Institutions Development Fund (FIDF), created in 1985 by the BOT to support troubled institutions, quietly provided more than THB 400 million (USD 17 billion) to nonbank finance companies between March 1997 and July 1997. Ultimately, this support did not contain the problem, and by August the BOT had temporarily suspended 58 finance companies. Crisis support ended in January 1998, after the BOT permanently closed 56 of the 58 suspended finance companies and converted FIDF loans to four commercial banks into equity. The liquidity support to finance companies peaked at more than THB 434 billion outstanding in August 1997. The FIDF lost at least THB 244 billion from the liquidity support to finance companies and an unknown amount from the support of commercial banks. That burden, about 15% of GDP, ultimately fell to the BOT and FIDF, which expects to repay FIDF bonds by 2030.

Keywords: Asian Financial Crisis, emergency liquidity, FIDF, Thailand, Tom Yam Kung crisis

Between 1980 and 1997, Thailand’s per capita income nearly quadrupled because of rapid export growth and high investment levels from sources in and outside of the country (Nabi and Shivakumar 2001). In 1993, the government adopted a framework to promote foreign investment in the country (Haksar and Giorgianni 2000). The Bank of Thailand (BOT) administered the exchange rate through a managed float (Nabi and Shivakumar 2001); with stable conditions, foreign lending through this framework quickly accounted for 18% of all bank lending (Haksar and Giorgianni 2000). This lending helped secure Thailand’s continued growth but exposed it to exchange rate movements. Currency speculators attacked the baht three times, and the BOT defended it three times, initially ruling out devaluation. The size of the foreign debt position “began to dictate the policy agenda that finally led to the crisis” (Nabi and Shivakumar 2001). The BOT accumulated large forward positions that whittled its international reserves from more than USD 39 billion in November 1996 to just over USD 1 billion in July 1997 (BOT 1998), when the baht was floated and immediately depreciated (Nabi and Shivakumar 2001).

Meanwhile, inside Thailand, financial institutions experienced the growth in foreign credit as a sharp increase in portfolio investment (as opposed to relatively illiquid foreign direct investment). With bank reserves growing slightly, portfolio investment more than doubled between 1993 and 1997. This growth exposed institutions to a loss of investor confidence and, ultimately, further deterioration of the baht. Confidence-busting signs appeared in 1996, when the mid-sized Bangkok Bank of Commerce collapsed, followed by the country’s largest decline in exports, low bank profit growth, and a slump in real estate. The burst real estate bubble proved significant because finance companies—Thai nonbank lenders that took deposits—had concentrated exposures to real estate and consumer loans (Nabi and Shivakumar 2001; BOT 2003).

Finance companies had also borrowed almost exclusively in the short or medium term (BOT 2003; Nabi and Shivakumar 2001). Thailand’s regulatory framework was too slow to monitor problems. For instance, it considered loans performing until 12 months of delinquent. In 1997, deposit runs began as depositors “fled to quality,” moving much of their deposits to commercial banks (Haksar and Giorgianni 2000).

In response, a corporation controlled by the BOT to support troubled institutions called the Financial Institutions Development Fund (FIDF) lent heavily to distressed finance companies (Tunyasiri 1997). The FIDF was established in 1985 to mitigate threats to financial stability. It received funding through fees it charged Thai financial institutions and from the BOT, which also appointed the FIDF’s officers. Despite the FIDF’s legal status as a separate entity, the World Bank (1990) found that it operated much like an arm of the BOT. Santiprabhob (2021), the former BOT governor, noted it had few permanent staff and relied on BOT staff during the crisis.

Between March 1997 and July 1997, the FIDF provided more than THB 400 billion (USD 17 billion)FThe baht was fixed at THB 25=USD 1 until July 2, 1997. It then peaked above THB 50 per dollar before settling around THB 40 to the dollar (Nabi and Shivakumar 2001). A Bank of Thailand report indicates that as of the end of July 1997, finance companies’ liabilities to FIDF were THB 410.6 billion (BOT 2009a). in liquidity support to 66 of Thailand’s 91 finance companies (Lindgren et al. 2000; Haksar and Giorgianni 2000; BOT 2009a).FThe data that we have located regarding FIDF lending is somewhat imprecise. Sources (for example, Hasker and Giorgianni 2000 and World Bank 1997) indicate that the FIDF lent to suspended finance companies, non-suspended FCs, and also to some commercial banks, although it is not always clear how much was lent to which group at which time. However, one World Bank report (World Bank 1997) cites the Bank of Thailand as the source for the following amounts outstanding as of the end of August 1997: Loans to suspended finance companies, THB 368 billion; loans to 33 open finance companies, THB 16 billion; loans to banks, THB 128 billion; total: THB 512 billion. It provided this support without informing the public (Lauridsen 1998; Prateepchaikul 1997), later defending its actions—if not its decision to not disclose support—as a necessary measure to increase financial sector liquidity (Meesane and Tunyasiri 1998). Publicly, the BOT announced in late June that it had suspended 16 finance companies because their capital was inadequate. It also said at the time that it would not suspend any more finance companies (Lindgren et al. 2000). Later, cabinet members alleged that the BOT had failed to report FIDF activities, though it is not clear whether the BOT was legally required to disclose FIDF lending (Meesane and Tunyasiri 1998). But other finance companies were still struggling. On August 5, 1997, the BOT suspended 42 more finance companies, despite having said there would be no further suspensions (Lindgren et al. 2000). This represented the end of the FIDF’s undisclosed liquidity support, , although the FIDF did continue to provide support to closed and open financial companies. (Hasker and Giorgianni 2000; World Bank 1997).

The FIDF funded its intervention in finance companies by issuing bonds and entering repurchase agreements with the same large commercial and foreign banks that received deposits from weakened financial institutions (Lindgren et al. 2000; Santiprabhob 2003). FIDF repos pushed up seven-day rates and distorted the short-term market, making the FIDF eager to end its liquidity support (Suthiwart-Narueput and Pradittatsanee 1999; Sirithaveeporn and Yuthamanop 1998).

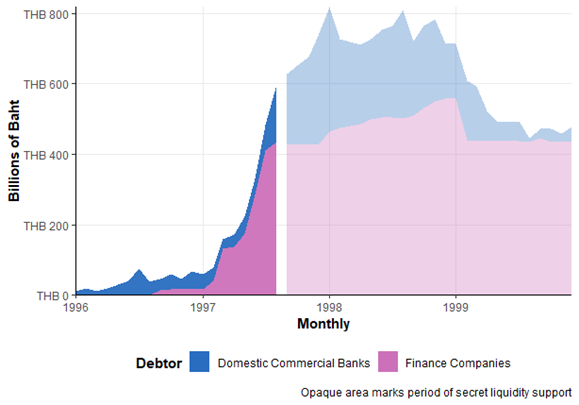

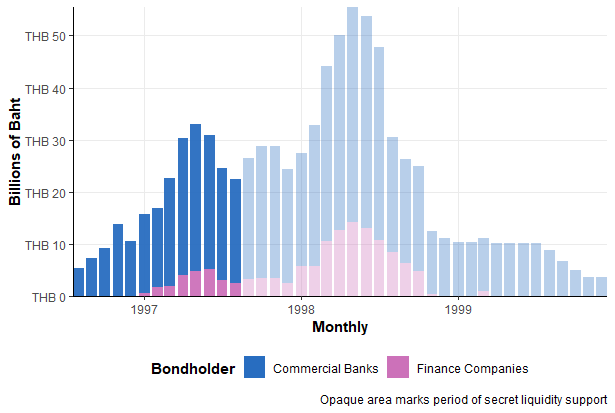

To exit its crisis support, the FIDF assumed significant losses on its support to finance companies and commercial banks. In October 1997, it relinquished preferential claims on counterparty collateral (Emergency Decree B.E. 2540 1997; World Bank 1997). In December, the BOT closed 56 of the 58 suspended finance companies, ending any possibility of repayment without a state-facilitated resolution process. Also in December, the FIDF began converting large amounts of its liquidity support to commercial banks to equity, recapitalizing the banks in the process (Haksar and Giorgianni 2000). As markets calmed, the FIDF continued to provide liquidity through the end of the 1990s (see Figure 1) and operated as a standing facility well after the end of the Asian Financial Crisis.

The FIDF recovered between THB 300 billion and THB 700 billion from its liquidity operations. There is both uncertainty and ambiguity in these estimates. The uncertainty comes from the fact that recovery could come from a number of different sources, each of which owed the FIDF for more than just liquidity support. The ambiguity comes from the different definitions of liquidity support among the documents surveyed. The FIDF eventually restructured its liabilities as long-term debt by issuing THB 776 billion in bonds (BOT 2002). As of 2015, the FIDF—which ultimately assumed financial responsibility for the debt—expected to repay its loans by 2030 (Emergency Decree B.E. 2555 2012; Sangwongwanich 2015).

Figure 1: Non-Repo Liabilities Owed to the Bank of Thailand

Note: Finance company data shows the liabilities owed explicitly to the FIDF, while commercial bank data does not disaggregate its liabilities to the BOT. Source: BOT 2009a; BOT 2003b.

Note: Finance company data shows the liabilities owed explicitly to the FIDF, while commercial bank data does not disaggregate its liabilities to the BOT. Source: BOT 2009a; BOT 2003b.

The FIDF provided finance companies and banks with liquidity support equal to 22% of GDP in its fight against the Asian Financial Crisis (Lindgren et al. 2000). However, a regulatory framework that limited FIDF’s ability to gauge the health of financial institutions and the high cost of borrowing exposed the FIDF to substantial risks. Moreover, inconsistent communication damaged market confidence, hampering the efforts of FIDF and the BOT to contain the crisis (Nabi and Shivakumar 2001), causing the FIDF to close finance companies and release its claims on collateral. These measures, in turn, hurt the ability of the FIDF to collect on its debtors (World Bank 1997). It was able to recover a significant portion of this debt through debt-to-equity conversions and collections by the asset management company created by the government to recover finance company loans (Santiprabhob 2003). The FIDF ultimately lost more than THB 400 billion after accounting for these recoveries (BOT 2002). Still, most observers argue that the FIDF averted the total collapse or nationalization of Thailand’s domestic banking sector (Lindgren et al. 2000; Sangwongwanich 2015).

Key Design Decisions

Purpose

1

The minutes of crisis-era BOT meetings are not public, so it is difficult to pin down the FIDF’s precise mandate. A parliamentary commission investigated the FIDF and wrote that the BOT considered liquidity support only as a measure to buy time (Nukul Commission 1998), while the BOT governor said, “The bank did it because it wanted to boost the liquidity of the financial sector” to resolve a crisis of confidence (Meesane and Tunyasiri 1998). As an institution, FIDF’s stated purpose from its creation was “reconstructing and developing the financial institution system to accord its strength and stability,” and it was not configured to respond quickly to a financial crisis (BOT 2018).

Legal Authority

1

A royal decree in 1985 first created the FIDF as a legally distinct entity within the BOT (2018). At the onset of the crisis, FIDF’s powers included lending money, investing in financial institutions, and supporting creditors (World Bank 1990). In 1997, liquidity problems deepened to threaten finance company creditors, prompting an emergency decree in October that allowed the FIDF to relax collateral requirements when the FIDF’s board of directors “deem[ed] it necessary to restore the fairness and soundness of financial system” (Emergency Decree B.E. 2540 1997).

Part of a Package

1

No other government bodies coordinated with the FIDF to support Thailand’s domestic institutions. Coordinated measures began only after the 58 finance companies were suspended and the support was made public.

Management

1

Though legislation made the FIDF a separate legal entity, it was controlled by the BOT. The board of directors was part of the central bank; the BOT governor chaired the board of directors; and BOT officials appointed the FIDF manager. The former BOT governor said that board members were not likely to disagree with BOT experts (Santiprabhob 2021). A former manager of the Fund said that each loan larger than THB 50,000 required the BOT governor’s approval (Yuthamanop 1998).

Cabinet members suggested that the BOT had a legal responsibility to report FIDF activities, though primary source documents and academic works considering the disclosure framework of the FIDF were not found. It seems clear that the FIDF was accountable only to the BOT in practice. In 1998, Parliament created the Nukul Commission to identify the causes of the crisis and to review the FIDF’s support of distressed financial institutions. Its report said that the FIDF:

itself lack[ed] independence. To inspect any institution’s financial position, it had to depend on the BOT’s Financial Institutions Supervision and Examination Department. In order to expedite action by the Fund, the management board of the Fund has given broad powers to the Chairman (who is also BOT’s governor), rendering it incapable of scrutinising BOT’s action carefully (Nukul Commission 1998).

Administration

1

There is little information on how the FIDF selected counterparties. When the BOT suspended 16 finance companies in June, it cited their capital and liquidity needs (Lindgren et al. 2000). The BOT governor said that market observers viewed the suspensions with suspicion because the BOT did not give the criteria it used to identify undercapitalized firms (Santiprabhob 2003). When the BOT later suspended 42 more finance companies, it again cited concerns about their solvency, but a World Bank report said that the FIDF had made the decision based on the companies’ level of indebtedness (World Bank 1997). The World Bank noted that the regulatory framework did not allow authorities to quickly monitor the health of finance companies and banks. For instance, loans were considered performing until 12 months of delinquency, which overestimated asset quality (Haksar and Giorgianni 2000). As a result, the FIDF—which had little permanent staff and borrowed officials from the BOT—relied on prior bank examinations when it loaned to finance companies (Santiprabhob 2021).

Eligible Participants

1

The Bank of Thailand Act (BOT 2018) allowed the FIDF to transact with any counterparty. In practice, the FIDF was created to support nonbank finance companies, of which there were 91 in 1997. During the first part of the year, FIDF lending to finance companies grew significantly, from THB 16.8 billion at the end of 1996 to THB 410.6 billion at the end of July, immediately before the second round of suspensions (BOT 2009a). The size of these institutions relative to Thailand’s financial sector is not known, but 58 of these finance companies—those that were suspended by the BOT in June and August 1997—represented the majority of Thailand’s finance companies and 14% of its financial sector (Haksar and Giorgianni 2000). The FIDF also provided loans to several banks. The public was aware that the four banks were distressed but not that they were receiving aid at the scale that the FIDF provided; these banks were Bangkok Metropolitan, First City, Siam City, and Bangkok Bank of Commerce.

Funding Source

1

The Bank of Thailand Act (BOT 2018) allowed the BOT to allocate money from its reserves to the FIDF, but, in practice, the FIDF issued debt and entered repurchase agreements to finance its liquidity support. In July 1996, the FIDF board decided to issue its first THB 10 billion in bonds “to fund the system’s mushrooming liquidity needs” (Nukul Commission 1998). The BOT, along with commercial banks, purchased these bonds (Lindgren et al. 2000, 95). But the FIDF could not issue long-term bonds, and Santiprabhob (2021) suggested that the FIDF would need substantial BOT subscription to provide several hundred billion baht in support. However, as the central bank, the BOT could not purchase unlimited amounts of FIDF bonds, lest it violate legal restrictions on financing government activities.

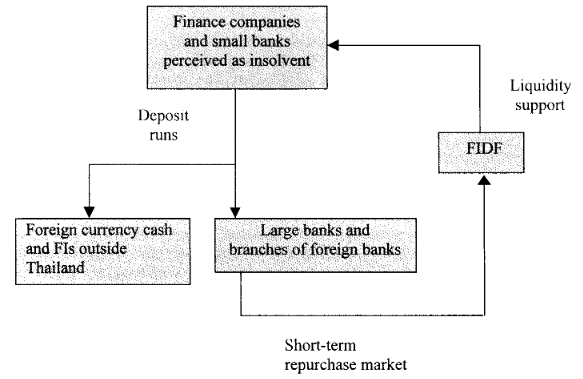

More substantial was the FIDF’s repo activity. These borrowings amounted to as much as THB 350 billion a month (BOT 2006). Santiprabhob (2003; 2021) described a circular flow of funds (see Figure 2) between weaker financial institutions, healthy—and often foreign—commercial banks, and the FIDF. As depositors fled the weak institutions, they deposited money in healthy commercial banks. To support weak institutions, the FIDF lent short-term funds by borrowing from those healthy banks. Seven-day repo rates in excess of 14% prevailed for a year starting in July 1997 (Suthiwart-Narueput and Pradittatsanee 1999), but the FIDF continued to refinance these agreements multiple times a week as depositors fled the weak finance companies for the FIDF’s creditors (Santiprabhob 2003). The FIDF decided to use repos to keep liquidity support short to prevent the courts from finding that the FIDF’s intervention amounted to capital support (Santiprabhob 2021).

Figure 2: Flow of Funds during the 1997 Financial Crisis

Source: Santiprabhob 2003.

Source: Santiprabhob 2003.

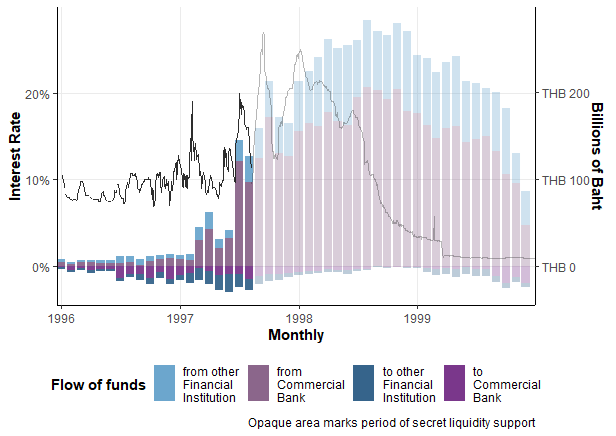

In April 1998, with hundreds of billions in outstanding claims on the recipients of liquidity support, Thailand moved to stop entering repurchase agreements in favor of government-issued debt. The Minister of Finance had said that the FIDF had “seriously unbalanced the short-term money market, affecting liquidity and causing interest rates to stay high” (Sirithaveeporn and Yuthamanop 1998). An emergency decree authorized the FIDF to issue long-term local debt (the term of the FIDF’s previous debt is unknown) (Sirithaveeporn and Yuthamanop 1998), and, on August 14, the Ministry of Finance (MOF) and BOT announced a THB 500 billion tranche of FIDF bonds guaranteed by the MOF to assume FIDF losses (Nimmanahaeminda and Sonakul 1998). In 2000, the MOF guaranteed bonds issued by the FIDF worth THB 112 billion (BOT 2002). In 2002, the BOT estimated FIDF’s total losses at THB 1.4 trillion: at least THB 430 billion can be attributed to liquidity support for finance companies (Lauridsen 1998), with an almost equal amount of liquidity support for banks (later converted to equity; see Santiprabhob 2003). See Figure 3 for a visualization of the repo volume during the crisis and the rates charged on repo borrowing.

Figure 3: Repo Volume and the Seven-Day Repurchase Rate

Source: BOT 1999; BOT 2006.

Source: BOT 1999; BOT 2006.

Thailand then passed an emergency decree empowering the MOF to issue up to THB 780 billion in bonds to cover the remaining losses. The government issued THB 300 billion of savings bonds in 2002. Originally, the BOT paid the outstanding principal out of its profits, while the MOF paid the interest (BOT 2002), but an Emergency Decree in 2012 made the BOT responsible for both components to free up space in the nation’s budget for flood recovery (Emergency Decree B.E. 2555 2012). In 2015, the FIDF said that it expected to repay its debt by 2030 (Sangwongwanich 2015) and reported THB 741 billion in debt outstanding in December 2020 (Public Debt Management Office 2021). See Figure 4 for a depiction of the breakdown of FIDF bondholders.

Figure 4: Holdings of FIDF Bonds

Source: BOT 2003b; BOT 2009a.

Source: BOT 2003b; BOT 2009a.

Prior to the crisis, the FIDF had levied an annual 0.1% fee on deposits of its member institutions (World Bank 1997). This money was originally intended to capitalize the FIDF and fund operating expenses (World Bank 1990). Given that deposits hovered just above 4 trillion baht during 1997 (Haksar and Giorgianni 2000), this fee could have brought the FIDF slightly more than 4 billion baht annually, just 1% of the liquidity support provided in early 1997. Emergency Decree B.E. 2540 (1997)—which also allowed the FIDF to make unsecured loans—enabled the FIDF Management Committee to raise the fees it charged member institutions, but only up to 1% of deposits. Rather, credit from the BOT and proceeds from investments provided the FIDF with the monies it used to inject capital in distressed institutions following a banking crisis in 1985. The FIDF did not carry an explicit mandate to insure the deposits of its member institutions, but the World Bank (1990) believed that it would insure deposits should a crisis hit.

The FIDF bore heavy losses for the sake of finance company creditors. In September 1997, the MOF said that the loans of just over THB 500 billion had been secured by collateral worth more than THB 800 billion (Notharit 1997). These were largely preferential claims in a position senior to the borrowers’ other unsecured creditors. Yet the World Bank (1997) estimated the value of collateral securing finance company liquidity support at less than 50% of the FIDF’s exposure. In part, this devaluation was caused by the country’s currency crisis, but Santiprabhob (2003) notes that debtors of finance companies were unable to refinance or negotiate for their collateral once those finance companies had been suspended. The suspension served to further squeeze liquidity in the Thai financial system. The FIDF’s preferential claims also hurt finance company creditors, which could not access the collateral promised to them (World Bank 1997). Once the FIDF decided to release its preferential claims on collateral, it of course limited its recovery opportunities.

Program Size

1

The FIDF provided increasing amounts of support to finance companies during the first part of 1997. Amounts outstanding stood at THB 16.8 billion at the end of 1996 and rose dramatically, beginning in February, to peak at THB 434 billion at the end of August, shortly after suspension of an additional 42 finance companies was announced (BOT 2009a). The FIDF continued to provide funding to closed and open finance companies and to some banks through the end of the year, when 56 of the 58 suspended finance companies were closed permanently. Such funding also continued into 1998, as the FIDF pursued its restructuring programs (Hasker and Giorgianni 2000; World Bank 1997).

Individual Participation Limits

1

No documents suggest that the FIDF capped participants’ borrowing limits. Some finance companies borrowed more than four times the value of their capital (Lindgren et al. 2000).

Rate Charged

1

In late 1997, the BOT tied rates to the BOT repo rate plus a variable penalty between 1% and 2.5%, depending on the level of indebtedness and size of support if uncollateralized (World Bank 1997). As shown in Figure 3, this rate sometimes exceeded 20% in 1997 and 1998.

Santiprabhob (2021) and a BOT official working in 1997 said that the rates for liquidity support were at market prices or slightly above, in keeping with lender-of-last-resort principles. However, the World Bank (1997) said that the FIDF provided support at below-market rates between March 1997 and July 1997. The World Bank cited the FIDF’s decision to not impose penalty rates as a cause of its ballooning liabilities.

After the support ended, many companies (especially those finance companies that the BOT suspended) faced difficulties repaying their debts. The Fund allowed debtors to submit rehabilitation plans and extend the length of repayment up to eight years. The FIDF charged a penalty rate to suspended institutions when compared to nonsuspended institutions (World Bank 1997), though very little of this rehabilitated debt would ultimately be repaid (BOT 2009a).

Eligible Collateral or Assets

1

FIDF support originally required government bonds as collateral, but finance companies began shedding their liquid assets in the summer of 1997 amid deposit runs. As these runs intensified, the FIDF began providing support against collateral of dubious value, including promissory notes of finance company debtors that would ultimately be worthless when many of those issuers entered bankruptcy (Santiprabhob 2003). Additionally, much of the collateral the FIDF required was not perfected (World Bank 1997).

Following the suspension of 58 finance companies in August 1997, the government weighed two actions that could free up FIDF collateral to recovery by private creditors: the release of the FIDF’s preferential claims on debtor collateral and the provision of unsecured liquidity support by the FIDF. If the FIDF could not release the collateral securing its emergency loans to finance companies, then the bankruptcy of a finance company would simply push its nonperforming loans to its creditors, shielding the FIDF at the expense of the financial sector it was created to protect. In October, Emergency Decree B.E. 2540 (1997) granted the FIDF the authority both to release collateral and to make new unsecured loans.

Loan Duration

1

If the FIDF provided liquidity support at a standard maturity, the documents surveyed do not indicate what that may have been. Santiprabhob (2021) suggested that credit was on-call for a short term. Given that the structure of funding was tied to seven-day repurchase agreements, support may have carried seven-day maturities. In any case, the MOF closed 56 of the 58 suspended finance companies in December 1997, before those companies repaid their debts. The MOF’s announcement ended the FIDF’s large-scale liquidity support of finance companies (Haksar and Giorgianni 2000), leaving the FIDF with more than THB 400 billion in unpaid claims on finance companies (BOT 2006; Lauridsen 1998). (For a breakdown of support by whether finance company counterparties were open or closed, see Haksar and Giorgianni 2000.) FIDF crisis intervention ended in January 1998, after the government nationalized four commercial banks (Lauridsen 1998). As markets calmed, the FIDF continued to provide liquidity through the end of the 1990s (see Figure 1) and operated well after the end of the Asian Financial Crisis.

Other Conditions

1

Support did not appear to carry any other conditions. After the undisclosed support ended, the FIDF imposed conditions on borrowing from the credit line.

Impact on Monetary Policy Transmission

1

Documents surveyed do not discuss the transmission of BOT monetary policy.

Other Options

1

Though Thailand had no deposit guarantee prior to 1997, observers such as the World Bank (1990) believed that it was widely assumed that the FIDF and government offered an implicit guarantee that it would not let depositors sustain a loss of their monies on deposit. The FIDF (1997) made this guarantee explicit in 1997, when it insured “all depositors and creditors of financial institutions that still operate[d] normal business” for two years (Mehta 1997). The FIDF pledged to pay those insured within 30 days of their claims. There does not appear to have been a cap on account or credit sizes, though the FIDF would not pay excessive interest rates over those offered by the largest Thai commercial banks (FIDF 1997).

The FIDF financed this blanket guarantee by issuing its government-backed bonds (FIDF 1997). “Despite, or perhaps because of, the large fiscal cost of the government’s emergency guarantee of deposits, the market did not view the move as credible” (Nabi and Shivakumar 2001). However, the government was still responsible for paying out to depositors and creditors, lest it be viewed as even less credible. The World Bank (1997) said that measures such as the blanket guarantee increased the cost of the crisis to the Thai government.

Similar Programs in Other Countries

1

Research did not determine similar programs in other countries at the time.

Communication

1

When the Thai Parliament learned of the extent of borrowing, the FIDF had already lent several hundred billion baht. The first indications came in early July, when a Member of Parliament accused the Prime Minister of wasting some THB 350 billion to rescue finance companies (Tumcharoen 1997). This episode appeared to have gone unnoticed. A month later, however, the BOT suffered a storm of criticism after it reported lending THB 430 billion—about 10% of GDP (Lauridsen 1998)—to finance companies before their suspension and ultimate failure (Tunyasiri 1997; Prateepchaikul 1997). At this point, the Prime Minister defended the FIDF on the basis that it had secured collateral against the loans (Tunyasiri 1997). The Minister of Finance said that the collateral outweighed the liquidity support by THB 800 billion to THB 500 billion (Notharit 1997).

Moreover, the BOT had “repeatedly guaranteed” the viability of the same finance companies that had received liquidity support (Santiprabhob 2003). When the BOT announced in March 1997 that ten finance companies needed to raise capital, it assured the solvency of the rest of the subsector. When the BOT announced in June 1997 that it would suspend 16 finance companies over capital inadequacy concerns, it again assured the market that the remaining finance companies were in good financial health, and that it would suspend no more finance companies (Lindgren et al. 2000). So, when it suspended 42 additional finance companies, the subsequent announcement of a deposit guarantee and credit line was unable to assuage concerns (Santiprabhob 2003).

In late 1997, the MOF committed to reflecting the FIDF cost explicitly in the Thai budget as part of a World Bank loan proposal (World Bank 1997). Following budgets and policy papers communicated the outstanding FIDF debt (BOT 2002; Suthiwart-Narueput and Pradittatsanee 1999; Public Debt Management Office 2021).

Disclosure

1

As discussed, the FIDF did not disclose its support until after finance companies were suspended. Knowledge of the THB 430 billion liability came through the BOT’s balance-sheet reporting. It is unclear, however, what responsibility or power the FIDF had to disclose its support. The FIDF did not disclose how much it lent to each institution.

Stigma Strategy

1

No documents discussed the BOT’s strategy for dealing with borrower stigma. However, the decision not to disclose liquidity support prevented market observers from stigmatizing the borrowers. Market participants suspected that more finance companies than the BOT reported were in danger, but they did not know which faced the gravest peril (Santiprabhob 2003).

Exit Strategy

1

There was no predetermined end date for FIDF intervention, but Santiprabhob (2021) cited the cost of borrowing as an incentive for borrowers to find other lenders. Support effectively ended when the possibilities for repayment ended. After the BOT suspended 16 finance companies in June 1997, the MOF established a committee to facilitate their merger and consolidation with Krung Thai Thanakit (KTT), a state-owned finance company (Santiprabhob 2003; Haksar and Giorgianni 2000). Another 42 finance companies were suspended in August and given 60 days to submit rehabilitation plans. In December, the MOF announced the closure of all but two of the 58 suspended firms (Haksar and Giorgianni 2000).

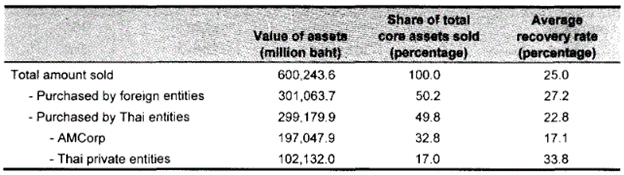

The Financial Sector Restructuring Authority (FRA)—created out of the committee that reviewed the first 16 suspensions (Santiprabhob 2003)—assumed the assets of closed finance companies; it began auctions and reached agreements to compensate creditors of the 42 companies later suspended. As of 2000, the FRA had recovered 28% of the THB 666 billion in nominal assets of the 56 finance companies (Haksar and Giorgianni 2000).

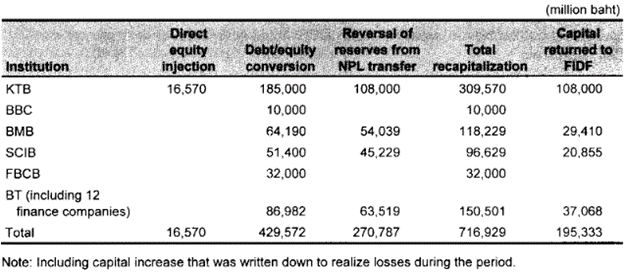

The FIDF took a different approach to the commercial banks to which it had provided emergency liquidity. Four banks to which the FIDF had provided large amounts of liquidity—Bangkok Metropolitan, First City, Siam City, and Bangkok Bank of Commerce—saw their FIDF claims converted to equity while shareholder capital was simultaneously written down (Lauridsen 1998). This mechanism sometimes overcapitalized the banks, which had returned THB 195 billion of capital to FIDF as of 2002 (Santiprabhob 2003).FFIDF converted debt of the four commercial banks and Bank Thailand into equity that it then spread to state-owned Krung Thai Bank (KTB; see Santiprabhob 2003 for an account of KTB’s recapitalization).

The FIDF lost at least THB 244 billion from liquidity support (Santiprabhob 2003, tables 5.2 and 6.2). There is both uncertainty and ambiguity in these estimates. The uncertainty comes from the fact that recovery could come from a number of different sources, each of which owed the FIDF for more than just liquidity support. Finance companies could have repaid loans before their closure (if they were among those closed), but these repayments cannot be disentangled from the finance company liabilities added during 1997 (BOT 2003). Ambiguity comes from the different definitions of liquidity support among the documents surveyed. For example, Teo et al. (2000, 95) includes a measure of the debt-to-equity conversion without describing its calculation, and claims that FIDF liabilities eclipsed THB 1 trillion. On the other hand, the BOT (2002) describes funds lost to liquidity support, deposit insurance, and recapitalization, all of which could conceivably be debited to liquidity support.

Key Program Documents

-

(BOT n.d.) Bank of Thailand (BOT). n.d. “Financial Institutions Development Fund.” Bank of Thailand. Accessed January 22, 2021.

Official BOT overview of the FIDF’s history and 21st-century operations.

-

(Lindgren et al. 2000) Lindgren, Carl-Johan, Tomás Baliño, Charles Enoch, Anne-Marie Gulde, Marc Quintyn, and Leslie Teo. 2000. “Financial Sector Crisis and Restructuring: Lessons from Asia.” Washington DC: International Monetary Fund.

Paper reviewing the various policy responses of the Indonesian, Korean, and Thai governments to the Asian Financial Crisis of 1997.

-

(Santiprabhob 2021) Santiprabhob, Veerathai. 2021. Interview with Veerathai Santiprabhob. Zoom.

YPFS interview with author and former BOT governor about specifics from Thailand’s experience of Asian Financial Crisis.

-

(Nimmanahaeminda and Sonakul 1998) Nimmanahaeminda, Tarrin, and M. R. Chatumongol Sonakul. 1998. “Thailand Letter of Intent, August 25, 1998,” August 25, 1998.

Letter of Intent from Thai government officials to the International Monetary Fund (IMF) as part of the IMF loan designated for restructuring the Thai financial sector The letter describes the purpose of the capital support facilities, capital terms, and other participatory conditions.

-

(BOT 2018) Bank of Thailand Act (BOT). 2018. B.E. 2485 (1942) 39.

Legislation originally authorizing the FIDF, with amendments up to 2018.

-

(Emergency Decree B.E. 2540 1997) Amending the Bank of Thailand Act, B.E. 2485 (No. 2). 1997. Emergency Decree B.E. 2540.

Emergency Decree allowing the FIDF to make unsecured loans, relinquish collateral already held, and raise member fees.

-

(Emergency Decree B.E. 2555 2012) Improving the Debt Management of Loan Made by the Ministry of Finance to Assist the Financial Institutions Development Fund. 2012. Emergency Decree B.E. 2555 6.

Emergency legislation changing the cost-sharing regime from one that split financial responsibility between the BOT and the MOF to one that placed sole responsibility on the BOT, owing to the need for fiscal space to pay for flood damages.

-

(BOT 2002) Bank of Thailand (BOT). 2002. “Fiscalization of Financial Institutions Development Fund’s Losses.” News 22/2002. Bank of Thailand.

Notice describing the repayment plan for FIDF debt.

-

(FIDF 1997) Financial Institutions Development Fund (FIDF). 1997. “Insurance for Depositors and Creditors of Financial Institutions.” Press release 52/1997. Bank of Thailand.

Press release announcing and detailing the blanket deposit and credit guarantee.

-

(Meesane and Tunyasiri 1998) Meesane, Somchai, and Yuwadee Tunyasiri. 1998. “Ministers Vent Anger on Central Bank Boss.” Bangkok Post, March 4, 1998, sec. Banking.

Newspaper article describing the anger of cabinet officials over the publication of FIDF losses.

-

(Mehta 1997) Mehta, Harish. 1997. “BOT Starts Credit Line, Deposit Guarantee for Finance Sector.” Business Times Singapore, August 9, 1997. Factiva.

Newspaper article describing the credit line and deposit guarantee for commercial banks and healthy finance companies, and repo funding process for the FIDF.

-

(Notharit 1997) Notharit, Wut. 1997. “Thanong Admits Government Made Some Financial Mistakes.” Bangkok Post, September 26, 1997.

Newspaper article featuring quotes from one of Thailand’s many crisis-era finance ministers that show the understanding of the MOF that FIDF claims were protected by collateral.

-

(Prateepchaikul 1997) Prateepchaikul, Verra. 1997. “And She Thought Soros Was No. #1.” Bangkok Post, August 12, 1997, sec. Commentary.

Editorial criticizing the FIDF for administering secret liquidity support to unhealthy institutions.

-

(Sangwongwanich 2015) Sangwongwanich, Pathom. 2015. “FIDF Set to Clear Debt Ahead of Schedule.” Bangkok Post, August 13, 2015, sec. Business.

Article describing the FIDF’s debt burden and repayment plan.

-

(Sirithaveeporn and Yuthamanop 1998) Sirithaveeporn, Wichit, and Parista Yuthamanop. 1998. “Measures to Boost Liquidity Approved.” Bangkok Post, April 29, 1998, sec. Economy.

Article describing, among other measures to fund the reform and support of Thailand’s economy, a decree passed to allow the FIDF to issue long-term local bonds.

-

(Tumcharoen 1997) Tumcharoen, Surasak. 1997. “Chavalit Accused of Wasting B550b on Futile Measures—Suthep Cites Report on Post-Float Fallout.” Bangkok Post, July 4, 1997.

News article first alleging massive support by the FIDF.

-

(Tunyasiri 1997) Tunyasiri, Yuwadee. 1997. “Erring Executives Face Punishments.” Bangkok Post, August 10, 1997, sec. Economy.

Newspaper article describing the reactions of public figures such as the Prime Minister to the admission that the FIDF had lent hundreds of millions of baht to suspended finance companies.

-

(Yuthamanop 1998) Yuthamanop, Parista. 1998. “Officials Defend Decisions of Fund.” Bangkok Post, March 5, 1998. Factiva.

News article describing the admission by the BOT that the FIDF had liabilities in excess of one trillion baht.

-

(Public Debt Management Office 2021) Public Debt Management Office. 2021. “Public Debt Outstanding.” Ministry of Finance.

Data showing, among other public debts, those attributed to the FIDF (in billions of baht).

-

(BOT 1998) Bank of Thailand (BOT). 1998. “International Reserves.” EC_XT_030. Bangkok: Bank of Thailand.

Data showing the diminution of BOT reserves during its currency crisis.

-

(BOT 1999) Bank of Thailand (BOT). 1999. “Repurchase Rates & Volumes.” FM_RT_005.

Data showing the repurchase rates of different maturities and the daily total volume of repurchase agreements.

-

(BOT 2003) Bank of Thailand (BOT). 2003. “Loan of Finance and Finance & Securities Companies Classified by Purpose (Outstanding).” XLS_MB_030. Bangkok: Bank of Thailand.

Data showing the composition of finance company portfolios before and during the crisis.

-

(BOT 2003b) Bank of Thailand (BOT). 2003b. “Operation of Commercial Banks.” XLS_MB_006. Bangkok: Bank of Thailand.

Data showing the sources and uses of commercial banks funds during the crisis.

-

(BOT 2006) Bank of Thailand (BOT). 2006. “Central Bank Sectoral Balance Sheet.” EC_MB_010. Bangkok: Bank of Thailand.

Data showing the assets and liabilities of the Bank of Thailand during the crisis.

-

(BOT 2009a) Bank of Thailand (BOT). 2009a. “Assets and Liabilities of Finance Companies.” XLS_MB_028.

Data showing FIDF support to finance companies and purchases of FIDF bonds by finance companies.

-

(Haksar and Giorgianni 2000) Haksar, Vikram, and Lorenzo Giorgianni. 2000. “Financial Sector Restructuring.” In Thailand: Selected Issues, 27–44. Staff Country Report 00/21. Washington, D.C.: International Monetary Fund.

Staff report describing Thailand’s economic crisis and measures taken by the government.

-

(Nukul Commission 1998) Nukul Commission. 1998. Analysis and Evaluation on Facts behind Thailand’s Economic Crisis. Translated by Nation Multimedia Group. Bangkok: Nation Multimedia Group.

Report by the Commission Tasked with Making Recommendations to Improve the Efficiency and Management of Thailand’s Financial System.

-

(Santiprabhob 2003) Santiprabhob, Veerathai. 2003. Lessons Learned from Thailand’s Experience with Financial-Sector Restructuring. Bangkok, Thailand: Thailand Development Research Institute.

Study commissioned by one of Thailand’s think tanks analyzing the government’s response to the crisis.

-

(Suthiwart-Narueput and Pradittatsanee 1999) Suthiwart-Narueput, Sethaput, and Varan Pradittatsanee. 1999. “Public Debt and Economic Policy During the Economic Crisis.” Thai Ministry of Finance, Policy Research Institute.

Describes the Thai government’s issuance of public debt to finance the capital support facilities, covering the emergency legislation passed to enable the issuance.

-

(World Bank 1990) World Bank. 1990. “Financial Sector Study.” 8403. Thailand. Asia Region: World Bank.

Report describing the FIDF’s status prior to the Asian Financial Crisis.

-

(World Bank 1997) World Bank. 1997. “Proposed Loan in the Amount of US$350 Million to the Kingdom of Thailand for Finance Companies Restructuring.” Report and recommendation P-7211-TH. Washington, D.C.: World Bank Group.

Proposal describing funding, pricing, exit strategy, and size of FIDF crisis support.

-

(Lauridsen 1998) Lauridsen, Laurids S. 1998. “The Financial Crisis in Thailand: Causes, Conduct and Consequences?” World Development 26, no. 8: 1575–91.

Early academic study recounting, among other things, the government’s response to the financial crisis.

-

(Nabi and Shivakumar 2001) Nabi, Ijaz, and Jayasankar Shivakumar. 2001. “Back from the Brink: Thailand’s Response to the 1997 Economic Crisis.” 22865. Directions in Development. Washington, D.C.: World Bank Group.

World Bank study describing the causes and response of Thailand to the currency, financial, and economic crises.

Figure 5: Recapitalization of State-Owned Banks (1998–2002)

Source: Santiprabhob 2003.

Source: Santiprabhob 2003.

Figure 6: Recoveries from FRA Auctions (1997–2001)

Source: Santiprabhob 2003.

Source: Santiprabhob 2003.

Taxonomy

Intervention Categories:

- Broad-Based Emergency Liquidity

Countries and Regions:

- Thailand

Crises:

- Asian Financial Crisis 1997