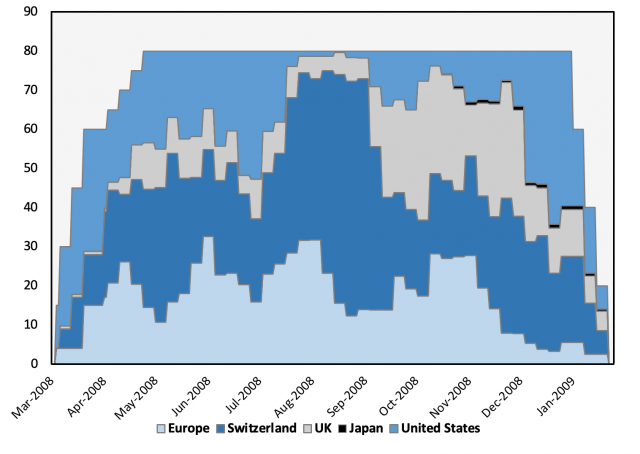

ST OMO was not given much attention nor formal evaluation. It was simply a set of open market operations done under a lender-of-last-resort pretense rather than as part of conventional monetary policy. This led to two important distinctions. First, that the funding term for ST OMO repos was longer than for conventional repurchase agreements. Repo and reverse repo agreements conducted in normal times most commonly had overnight terms, with the longest term allowed normally being 65 days. Second, the single-tranche aspect of the program allowed agency MBS to be put up as collateral at a lower effective rate despite their underlying risk, thus providing much-needed funding to considerably strained term funding markets, which had all but frozen. However, since ST OMO was also introduced around the same time as many other programs, such as TSLF and the PDCF, it was more difficult to disentangle the stand-alone impact it had on term funding markets.

Michael J. Fleming explained that, while ST OMO had market-determined pricing, which appeared to keep auction rates high, the usage of the program and the subsequent decline in stop-out rates suggests that the auctions were priced well (Fleming 2012). Certain institutions, such as Credit Suisse, Goldman Sachs, BNP Paribas, Countrywide, and Cantor Fitzgerald, had more than half their outstanding credit at the Federal Reserve as single-tranche repos (Eisenbeis and Herring 2014). Robert Eisenbeis and Richard Herring suggested that these five primary dealers, as well as Morgan Stanley, RBS, UBS, Deutsche Bank, and Barclays, had a non-negligible amount of ST OMOs outstanding, and thus benefited quite a bit. However, for this group of dealers, the authors of the paper stated that ST OMO “had negligible impact” (Eisenbeis and Herring 2014). Generally, however, there appears to be very limited evaluation on the impact of ST OMO itself, especially compared to TAF, TSLF, and PDCF. In spite of its use as a lender-of-last-resort facility, the small size of the program ($80 billion outstanding at any given time) and standard legal basis may have contributed to a relative lack of evaluation, as well.

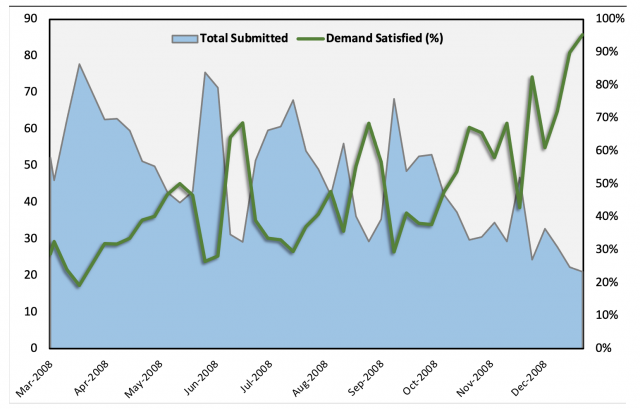

Bill English and Trish Mosser discussed some aspects of ST OMO, explaining that, “it was simple to announce and implement and was well-understood by the primary dealers, with no stigma attached to its use” (English and Mosser 2018). Additionally, since it was an FRA Section 14 program and used conventional authority, its implementation was immediate. The authors cited an immediate, verifiable positive impact on one-month repo spreads for agency MBS, which quickly fell after ST OMO and the other primary dealer programs were put in place. Initial demand was quite high for the program but tapered off once other, broader facilities were put in place.See Figure 6 for more information. Finally, they explained that, due to the comparatively narrow range of usable collateral, the program was not as effective as it could have been in easing term funding market strains (English and Mosser 2018).

|

Figure 6: Amounts Submitted to Single-Tranche Auctions (left axis, USD billions) and Demand Satisfied (right axis, %)

|

|

|

|

Note: Demand Satisfied is calculated by dividing the total amount submitted by primary dealers during a given weekly single-tranche repo auction by the amount accepted by the Federal Reserve Bank of New York. Thus, it is the weekly proportion of primary dealer demand for the facility that was met by the FRBNY. In March 2008, weekly amounts accepted were $15 billion, and from the end of April to the final auction on December 31, 2008, weekly amounts accepted stayed constant at $20 billion per week.

Source: FRBNY.

|

Despite a lack of academic attention, in 2011, the program garnered a fair bit of press in the public sphere, most notably in an article written by Bob Ivry. He lambasted the program for being “secretive” and containing transaction-level details such as bank-specific participation, collateral used, and rates paid, that had not been revealed to anyone in the public sphere (Ivry 2011).

David Altig, executive vice president and director of research at the Federal Reserve Bank of Atlanta, challenged these criticisms, stating that he believed the transactions were not secretive, as the FRBNY had issued a press release on March 7, 2008, that specified some of the details of ST OMO. Additionally, Altig argued that the press releases, combined with the overall auction results (which were published) and the fact that the list of primary dealers was readily available, suggested that the program was far from secretive (Altig 2011).

Well-known financial journalist Felix Salmon mostly sided with Altig in the discussion about ST OMO, but he pointed out that Altig’s remarks “made the Fed seem a lot more transparent than it actually is.” Additionally, he criticized the Fed for not bothering to enhance public understanding of the program, explaining that Ivry’s article was the first time that many in the public sphere, including then–Representative Barney Frank, found out about the program (Salmon 2011).

While it is true that, in the summer of 2011, the Federal Reserve released transaction-level data for many of these programs, including ST OMO, it was forced to do so after being sued by Bloomberg reporters in November 2008 under the Freedom of Information Act (FOIA). Only after a 16-month legal battle, combined with an appeal that ended with a ruling against the Fed, did it release transaction-level data. The reluctance could have been due to a lack of desire on the part of the Fed to disclose the information of individual banks that were most vulnerable, to avoid stigma against them (Feuer 2010; Ivry and Keoun 2011).