Account Guarantee Programs

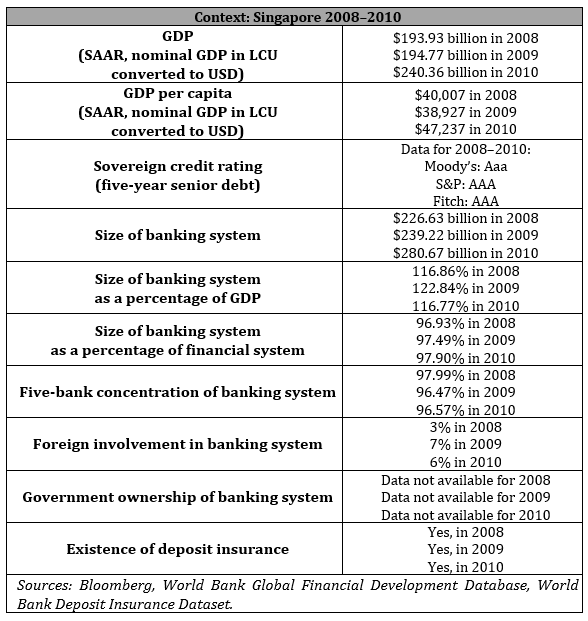

Singapore: Government Guarantee on Deposits

Purpose

“To avoid an erosion of banks’ deposit base and ensure a level international playing field for banks in Singapore” (MOF and MAS 2008)

Key Terms

-

Launch DatesAnnouncement: Oct. 16, 2008; Authorization: Oct. 16, 2008; Operation: Oct. 16, 2008

-

End DateDecember 31, 2010

-

Eligible InstitutionsBanks, finance companies, and merchant banks licensed by the MAS, and credit cooperatives

-

Eligible Accounts“All Singapore Dollar and foreign currency deposits of individual and nonbank customers” in eligible institutions

-

FeesNo fees, government reserve used to fund the program

-

Size of GuaranteeUnlimited guarantee

-

CoverageSGD 700 billion

-

OutcomesNo claims made

-

Notable FeaturesThe GGD expanded coverage to depositor types (notably private companies) and depository types (credit cooperatives) that the existing deposit insurance did not cover; Singapore cooperated with Malaysia to announce their crisis-time deposit guarantee programs; Singapore cooperated with Hong Kong and Malaysia to formulate a uniform exit strategy

Key Design Decisions

Purpose

Part of a Package

Administration

Governance

Communication

Size of Guarantee

Source and Size of Funding

Eligible Institutions

Eligible Accounts

Fees

Process for Exercising Guarantee

Other Restrictions

Duration

Key Program Documents

Taxonomy

Intervention Categories:

- Account Guarantee Programs