Reserve Requirements

Russia: Reserve Requirements, 1998

Purpose

“To overcome an acute liquidity crisis in the banking system and restore an efficient payments system” (CBR 1999)

Key Terms

-

Range of RR Ratio (RRR) Peak-to-TroughUp to 16% for some liabilities to a flat rate of 5%; see Key Design Decision No. 12, Changes in Reserve Requirements

-

RRR Increase PeriodStarting March 19, 1999

-

RRR Decrease PeriodFebruary 1–December 1, 1998

-

Legal AuthorityArticle 75, Russian Constitution; Article 38, Law on Central Bank

-

Interest/Remuneration on ReservesUnremunerated, except for a separate, voluntary deposit facility

-

Notable FeaturesUse of discretionary, unscheduled RR changes for individual banks, including lower RR ratios for banks with large exposures to defaulted Russian treasuries, to enable multilateral clearing operations

-

OutcomesRR balances decreased RUR 18.3 billion (USD 2.8 billion) over the easing period

During the 1998 ruble crisis, the Central Bank of the Russian Federation (CBR) relied on reserve requirements (RR) to bring stability to the ruble’s exchange rate corridor and, over time, to inject liquidity into the frozen domestic banking system. First, in February 1998, the CBR unified the RR ratio on ruble and foreign currency liabilities to facilitate ruble financing. Second, after the devaluation of the ruble in August, the CBR lowered the RR ratio to provide liquidity to the banking system. Third, the CBR revised the computation of the RR ratio to provide relief to banks in an effort to restore the frozen payment system. Russia’s RR policy, in concert with other liquidity measures, in particular multilateral clearing operations, succeeded in unfreezing the Russian payment system in late 1998. The CBR began to raise RR ratios in mid-March 1999 in response to rising inflation. However, some argue that the regulatory forbearance surrounding CBR liquidity assistance allowed banks to act imprudently, contributing to an erosion of public trust in the Russian financial system. Over the reserve requirement easing period, from the beginning of August until the beginning of December, balances of RR accounts decreased from RUR 37.3 billion (USD 6 billion) to RUR 19 billion, reflecting the liquidity injected through these measures.

After a long record of foreign capital inflows into Russia’s emerging market economy, the domestic financial markets deteriorated in October 1997 as spillovers from the East Asian currency crisis undermined confidence in the ruble’s (RUR) fixed exchange rate corridorFThe ruble exchange rate corridor, maintained up until August 17, 1998, fixed the exchange at a midpoint of 6.20 rubles (RUR) to the US dollar (USD) and could fluctuate 15% above or below that target (CBR 1999). to the US dollar (USD) (Antczak 2001; CBR 1999). The first wave of speculative attacks on the ruble began in November 1997, as foreign investors sold ruble-denominated government treasury securities, known as GKO-OFZs. This forced the Central Bank of the Russian Federation (CBR) to shed roughly USD 6 billionFBased on the midpoint of the fixed exchange rate corridor, RUR 6.20 per US dollar (CBR 1999). (RUR 37.3 billion) of its USD 23 billion foreign reserves to defend the exchange rate peg (Chiodo and Owyang 2002; Johnson 2018, 213). Early in 1998, the CBR stopped directly purchasing government securities (e.g., GKO-OFZ), which it had previously done to keep domestic interest rates low (CBR 1999).

On February 1, 1998, the CBR implemented the first major policy measure of the year, which signaled its commitment to protecting the ruble corridor. It sharply raised its policy rate and the rates on its liquidity facilities. At the same time, it significantly revised the reserve requirement (RR) system (Interfax AIF 1998).

RRs were one of the CBR’s most important monetary policy tools (CBR 1998c). All “credit institutions” licensed to perform banking operations (banks) were subject to RRs (CBR 1996, vol. 37, para. 1.5).FThe CBR sometimes uses the term “credit institutions” interchangeably with “banks” (CBR 1999). As of the beginning of 1998, there were 1,686 credit institutions licensed to conduct banking operations, of which 1,664 were banks while the remaining 22 were “non-bank credit institutions” (CBR 1998c). The CBR required them to deposit a specified portion (RR ratio) of their liabilities into a blocked-off account (RR account) with the CBR (Baliño, Hoelscher, and Horder 1997; CBR 1999). While funds in RR accounts were typically static, the CBR permitted banks that complied with RRs in the preceding six-month period to use averaging, decreasing the burden of the RR (Baliño, Hoelscher, and Horder 1997). Funds in RR accounts paid no interest (Baliño 1998).

Before February 1, the CBR differentiated RRs according to both maturity of deposits and currency denomination. Ruble-denominated liabilities faced the highest RR ratios and were organized into three tiers, ranked from highest to lowest RR ratios: demand accounts and time liabilities up to 30 days (14%), time liabilities between 31 and 90 days (11%), and time liabilities over 90 days (8%). Foreign currency–denominated accounts of all maturities required 9% reserves (CBR 1998c).

From February 1 through the end of August, the CBR administered a new, unified RR system under which all commercial banks’ borrowings became subject to a common RR ratio of 11%, independent of deposit maturity and currency denomination (CBR 1998e; CBR 1999). The policy change lowered RR ratios for short-term ruble-denominated funds and raised RR ratios for foreign currency funds (CBR 1998c). The CBR’s intent was to make it easier for banks to borrow in rubles and more expensive to borrow in other currencies (CBR 1999; Interfax AIF 1998).

Between February and April, investor confidence in the Russian economy improved; however, in May, domestic financial markets suffered another shock as foreign investors liquidated their holdings of ruble treasuries (GKO-OFZs) (Antczak 2001; CBR 1999). The market froze, as foreign investors had held half the stock of ruble treasuries (Antczak 2001). In June, the government ran out of funds to make bond payments, forcing the CBR to intervene in the treasury market. The escalating payment challenges for both the government and Russian banks—which were heavily exposed to illiquid ruble instruments—undermined the CBR’s ability to defend the exchange rate (CBR 1999). By August, market participants anticipated a devaluation of the ruble (Ippolito 2002).

In a joint statement on August 17, the Russian government announced that it would default on ruble treasuries (GKO-OFZs) maturing before 2000, and the CBR announced that it would allow the ruble to devalue by widening the corridor from RUR 5.25-7.15 (centered around RUR 6.20) to RUR 6.00-9.50 per US dollar. The government also declared a 90-day moratorium on debt repayment to foreign creditors (CBR 1999; Chiodo and Owyang 2002).

On August 24, one week after the default, the CBR made a second change to RRs, decreasing the uniform 11% ratio to 10% (Segodnia 1998b). The CBR announced that the change would allow it to inject RUR 4 billion of surplus RR funds to banks’ interbank settlement accounts (correspondent accounts) at the CBR (Segodnia 1998b).

On September 1, the CBR dramatically changed RR policy to ease liquidity for banks that were heavily exposed to defaulted treasuries. It created a new system for differentiating RR ratios based on banks’ treasury exposures. The CBR lowered the RR ratio to 5% for banks whose treasuries were 40% or more of their working assets. Banks with 20-40% of working assets in treasuries would meet a 7.5% ratio. Banks with less than 20% of working assets in treasuries would continue to meet the existing RR ratio of 10% (CBR 1998c). These changes injected significant liquidity into the banking system, yet banks continued to liquidate rubles for foreign currency (Antczak 2001; Owen and Robinson 2003, 32). On September 1, the same day as these RR changes went into effect, the ruble depreciated past the upper bound (RUR 9.50 per US dollar) of the corridor and the CBR decided to switch to a floating exchange rate (Antczak 2001; CBR 1999).

On September 17, the CBR revalued foreign currency borrowings for the purpose of calculating corresponding RRs, based on the ruble exchange rate on August 14, prior to devaluation (CBR 1999). This measure further released liquidity for Russian banks, contributing to a reduction in banks’ required reserves for foreign currency liabilities from RUR 11.6 billion at the end of August 1998 to RUR 6.8 billion at the end of September (Owen and Robinson 2003, 134).

Starting the following day, the CBR administered three multilateral clearing operations, taking place on three consecutive Fridays—September 18, 25, and October 2 (CBR 1999). The CBR gave participating banks overnight loans at low interest rates in order to quickly settle balances by the end of Friday. As the CBR worked with banks over the weekend to offset mutual interbank liabilities, the CBR allowed certain banks to use portions of the RR accounts, transferred to correspondent accounts (Russian Telegraph 1998). In total, the three rounds of multilateral clearing operations cleared RUR 54.6 billion outstanding payments and released RUR 7.1 billion of RR funds into the banking system (CBR 1999; Cherkasov 1998).

Since many banks, particularly large ones, used parts of their RR accounts to make payments during the clearing operations, not all banks technically complied with the statutory RRs (Buza 1998; Cherkasov 1998). Therefore, between the clearing operations and December 1, 1998, the CBR negotiated regulatory relief for certain banks, allowing some banks to receive lower RR ratios (see Key Design Decision No. 12B, Changes in Reserve Requirements).

On December 1, 1998, the CBR reunified the RR system under a single 5% ratio for all liabilities and recalculated foreign currency liabilities using the current exchange rate. At the same time, the CBR conducted a review of RR account funds and discovered an RR shortfall of 18.6%. The CBR decided to waive the associated fine and not recover the RR deficits from banks that participated in the multilateral clearing operations (CBR 1999).

As many of the domestic payment challenges eased and domestic inflation creeped up, the CBR began to tighten monetary policy in the first quarter of 1999 (Owen and Robinson 2003, 31, 133, 135). The CBR thus began raising RR ratios, beginning in March 1999 with a uniform increase from 5% to 7%, then to 8.5% in June (CBR 2000).

The CBR’s RR relaxations, following the default on August 17, were among the largest liquidity operations undertaken by the CBR during the post-default crisis period; these relaxations contributed to an aggregate decrease of RUR 18.3 billion in required reserve funds between August 1998 and December 1998 (Owen and Robinson 2003, 134). Throughout the period, the CBR provided large amounts of liquidity to the frozen banking system through both official RR ratio reductions (August 24, September 1, and December 1) and unofficial relaxations—implemented during and following the multilateral clearing operations (Antczak 2001; CBR 1998e; Cherkasov 1998). See Figure 1 for the liquidity provided through RR relaxations compared with that of other CBR instruments (Owen and Robinson 2003, 133–34).

Figure 1: CBR Liquidity Injections into the Banking System, 1996–1999

Source: Owen and Robinson 2003, 134.

Source: Owen and Robinson 2003, 134.

According to Robinson (Owens and Robinson 2003, 31), the CBR’s liquidity injections, including RR relaxations, succeeded in restoring functioning to a frozen domestic payment system, providing lift-off for the real economy. However, banks inevitably sold much of the rubles they received from liquidity injections on the foreign exchange market, further deteriorating ruble stability. This is evident in the timing of RR relaxations on August 26 and September 1. On August 26, banks received RUR 4 billion in liquidity from RR reductions (Segodnia 1998b). Between August 26 and September 1, when the next relaxation took effect, the value of the ruble continued to fall, forcing the CBR to eventually abandon the fixed exchange rate system altogether, in a switch to a float on September 2 (Antczak 2001).

Key Design Decisions

Purpose

1

During the 1998 Russian ruble crisis, the Central Bank of the Russian Federation (CBR) implemented several changes to reserve requirements (RR) in two separate crisis periods: before and after ruble treasury default and ruble devaluation on August 17, 1998. Pre-default, the CBR managed a narrow ruble exchange rate corridor, fixed within a 15% range of 6.20 rubles (RUR) to the US dollar (USD) (CBR 1999). During the 1998 pre-default period, the CBR introduced only one change to RRs, on February 1 (CBR 1998e). In an attempt to ease ruble liquidity and to simplify the otherwise fragmented requirements on reserve ratios, the CBR implemented a single RR of 11% for both foreign and domestic currency accountsFExcluding the unchanged, 8% RR for ruble household deposits of the state-owned bank, Sberbank (CBR 1999). (CBR 1999). The change reflected an increase in the RRs on foreign currency accounts and a decrease on short-term accounts denominated in rubles. The CBR said its intent was to “[encourage] credit institutions to expand their ruble resources and [discourage] the use of the dollar in the Russian economy” (CBR 1999).

On August 17, against persistent capital flight from ruble assets, the CBR could no longer defend the fixed exchange rate and effectively devalued the ruble by adopting a wider corridor: between 6.00 and 9.50 RUR/USD. The wider corridor still proved unsustainable, and the CBR abandoned the fixed exchange rate and floated the ruble on September 2 (Antczak 2001; CBR 1999).

In the post-default period—as policy efforts pivoted away from exchange rate stability—the CBR administered several relaxations of reserve requirements in concert with other liquidity instruments “to restore the payments system and interbank relations, which were seriously damaged by the crisis” (CBR 1999).

Part of a Package

1

Following August 17, the CBR used several tools, in addition to relaxing RRs, to provide liquidity assistance to the illiquid banking system. The CBR extended direct loans to commercial banks through its existing Lombard and Overnight lending facilities, as discussed in a separate case study by Hoffner (2022b). Another supplementary case study by Hoffner (2022a) explores the CBR’s issuance of its own zero-coupon bonds, OBRs, used by banks at standing lending facilities and newly introduced repo operations. The CBR also extended long-term rehabilitation loans secured by bank equity to select commercial banks (CBR 1999). See Hoffner (2022b) for more information on other supplementary programs the CBR used to support domestic banks during the 1998 crisis.

The CBR also administered two notable measures in coordination with RR relaxation: multilateral clearing operations and regulatory forbearance. Key Design Decision No. 12B, Changes in Reserve Requirements, discusses regulatory forbearance (CBR 1999; Ippolito 2002).

Multilateral Clearing Operations

In three separate iterations, on September 18, 25, and October 2, 1998, the CBR conducted multilateral clearing operations to address the backlog of nonpayments in the interbank lending market (CBR 1999). The CBR reduced individual banks’ required reserves on a case-by-case basis to facilitate these operations (IMF 1999). See “Discretionary RR Changes” in Key Design Decision No. 12A, Changes in Reserve Requirements.

The CBR announced the first of these measures on Friday, September 18. The Russian Telegraph described it as the CBR’s most important decision for Russia’s payment system. The CBR encouraged banks in the five largest regions of Russia to participate in the clearing operation by giving the CBR access to their entire client card file.FTranslation challenges complicate the description of this operation and what exactly “client card file” refers to. The source says that providing the CBR with this file revealed both the budgetary and client debts of a bank (Russian Telegraph 1998). This file would reveal each bank’s outstanding liabilities to its clients and to the government, which the CBR referred to as “budgetary” debts (Russian Telegraph 1998). In exchange, the CBR provided participants with an overnight loan at a low interest rateFAnother article (Cherkasov 1998) describes the reverse: the CBR first allowed banks to use RR funds and, if insufficient to settle balances, the CBR provided a low interest rate, overnight loan. in order to quickly settle end-of day balances on Friday, September 18; if a bank needed additional support to clear, the CBR allowed the bank to draw down its own RR funds at the central bank. The CBR then worked with participating banks throughout the night and into the weekend to mutually offset interbank liabilities so that on Monday, the following business day, banks could resume payments. The CBR did not make foreign currency available to banks on that Friday, in order to prevent banks from immediately selling the additional ruble funds on the foreign exchange market (Russian Telegraph 1998).

The CBR ran a similar procedure in the second and third rounds of multilateral clearing operations, which took place on the two subsequent Fridays and also lasted into the weekend (Buza 1998; CBR 1999; Cherkasov 1998). In the first round, most of the largest Russian banks chose not to participate because they did not want to give the CBR their client files. In response, the CBR ordered the Moscow Interbank Currency Exchange (MICEX) to temporarily suspend the six of the largest banks from currency trades (Cherkasov 1998). In the second round, the CBR expanded the operation to include 38 regions in Russia; in this round, the CBR selectively lowered RRs for large, connected Moscow banks to free up liquidity for their regional branches to clear payments throughout the many regions (Buza 1998; Cherkasov 1998). The final round expanded to 73 regions, covering most of Russia. Despite the regional expansion in the third round, the first and second rounds were significantly larger in volume. Together, the three rounds of multilateral clearing operations cleared RUR 54.6 billion outstanding payments for the domestic banking system (Cherkasov 1998).

In the most controversial component of the multilateral clearing operations, the CBR purchased an undisclosed amount of defaulted treasuries from banks at par to allow them to meet their payment obligations (Cherkasov 1998; Russian Telegraph 1998). While the CBR did not publicly reveal the total amount of GKO bills redeemed, one source estimated that the CBR purchased at least RUR 7 billion between the first two rounds of clearing. The move was particularly controversial from the perspective of foreign investors who still held significant portions of illiquid, defaulted GKO bills and, unlike participating domestic banks, could not sell their holdings (Cherkasov 1998).

The CBR chose not to collect RR shortfalls from or penalize the banks whose reserve ratios the CBR had lowered on a discretionary basis during the multilateral clearing operations (CBR 1999).

Legal Authority

1

Article 75 of the Russian constitution both defined the CBR’s primary policy directive as “ensuring the stability of the ruble” and provided for legal independence from other government institutions in pursuing that mandate (Russian Federation 1993).

Article 38 of the Federal Law of the Central Bank (Central Bank Law) specifically authorized the CBR’s board of directors to set RR terms for banks, subject to constraints (CBR 1998c). Article 38 laid out the following legal constraints on RR management (Central Bank Law 1990, N 394-1, article 38):

- RR ratios cannot exceed 20% of a bank’s liabilities.

- RR changes cannot exceed five percentage points at a given time.

- The CBR can recover RR shortfalls from banks and fine the violating institution; penalties cannot exceed double the refinancing rate (policy rate).

The CBR also noted that it had the right to make unscheduled changes in reserve requirements, as it described in Bank of Russia Directive No. 414U, dated November 17, 1998 (CBR 1999). Article 38 of the Central Bank Law states that the CBR may differentiate RRs between banks (Central Bank Law 1990, N 394-1, article 38). This was the basis of the CBR’s use of unscheduled, discretionary RRs for individual banks during the multilateral clearing operations.

In the pre-default period, the CBR managed RR policy in accordance with its primary objective of ruble stability. As it became clear that the CBR could no longer protect the exchange rate regime, the CBR focused policy efforts toward restoring the domestic payment system and reviving domestic banks (CBR 1998d; CBR 1999). In addition to currency stability, Article 3 of the Central Bank Law lists two other main objectives of the CBR: “[promoting] the development and enhancement of the Russian banking system and [ensuring] the efficient and uninterrupted functioning of the settlements system” (CBR 1998d).

Administration

1

The CBR’s board of directors set RR ratios and other central rules associated with depositing reserves in accountsFDomestic banks had three main accounts at the CBR: an RR account (unremunerated), a correspondent sub-account (for banks to use in settling interbank balances), and a voluntary deposit account (interest bearing with maturities of up to two weeks) (Baliño, Hoelscher, and Horder 1997; CBR 1999). Voluntary deposit accounts represented a much smaller component of the monetary base (1.8% by end of 1998) when compared to RR (8.1%) and correspondent (12.6%) accounts (CBR 1999). with the CBR (CBR 1998c). The board of directors delegated the administrative duties, including collecting RR funds, to the CBR’s regional settlement and cash centers (CBR 1996, article 1.6; Segodnia 1998b). These regional centers reviewed RR account balances on the first day of each month. Although the regional centers assessed RR compliance on a monthly basis, the board of directors could use discretion for extraordinary RRs and review banks’ RR balances at any point in the month (CBR 1996, article 1.7).

Governance

1

Domestic banks documented their own account balances daily and reported their funds subject to RRs on a monthly basis to their CBR’s regional cash and settlement centers (CBR 1996, 37, article 2.4). The high reliance on self-reporting from banks resulted in frequent data inaccuracies (Owen and Robinson 2003).

Post-default, the CBR conducted scheduled reviews of RRs twice, on September 1 and December 1, 1998. In these two reviews, the CBR conducted comprehensive examinations of banks’ RR compliance, which revealed large shortfalls in RR funds (CBR 1999).

The State Duma—the lower house of the Federal Assembly (Russian Parliament)—appointed and could dismiss the chairman of the CBR as well as other directors; dismissal of the chairman required presidential approval and could be done only if the chairman violated the law (CBR 1998d; Johnson 2018). The State Duma also appointed an auditor to review the CBR’s reports (CBR 1998d).

The Association of Russian Banks (ARB)FBy the end of 1998, ARB members represented 707 commercial banks, or roughly half of all commercial banks, including most of the largest banks (Johnson 2018, 6). In addition to lobbying, some ARB members also held seats in the State Duma and directly influenced financial laws (Johnson 2018). The ARB frequently asked the CBR to relax monetary policy by lowering RRs (Johnson 2018, 116; Moiseev 1998; Segodnia 1998a). was an interest group of commercial banks that lobbied the government to implement favorable financial legislation (Johnson 2018, 14). Commercial banks, represented by the ARB, continued to petition for the CBR to relax RRs throughout the pre-default period; however, the CBR did not entertain these requests until after the default, once it had abandoned the tight ruble corridor (Johnson 2018, 116; Moiseev 1998; Segodnia 1998a).

Communication

1

Before the start of each year, the CBR submitted to Parliament (State Duma) a document, called Guidelines for the Single State Monetary Policy (henceforth “Guidelines”), which summarized the CBR’s policy goals and constraints for the year ahead (CBR 1999). The 1998 Guidelines, which the CBR delivered to Parliament toward the end of November 1997, communicated the CBR’s intention to lower RRs on ruble deposits and raise those on foreign accounts; the CBR intended to strengthen the ruble against depreciating pressures to preserve the ruble exchange rate corridor. The plans to raise RRs on foreign liabilities in the 1998 Guidelines disappointed the commercial banks of the ARB that had wished for a reduction in foreign currency RRs (Cherkasov 1997; Ekonomika i Zhizn’ 1997). Parliament also refused to approve the Guidelines; however, due to its legal independence, the CBR did not require Parliament’s approval.FThe CBR faced considerable parliamentary opposition to the 1998 Guidelines and the CBR’s aggressive defense of the ruble (through rate hikes and RR policies) (Ekonomika i Zhizn’ 1997). In April 1998, the Russian Parliament’s Federation Council (upper house) submitted a draft bill to the State Duma, which proposed to limit the CBR’s independence, in part by requiring Guidelines to receive legal approval (NG Polytechnics 1998); this controversial bill, however, did not pass the State Duma (Kuzmichev 1998). Adhering to the 1998 Guidelines, the CBR’s public relations department circulated a press release on January 30, 1998, that announced the lowering of RRs on ruble accounts and raising of RRs on foreign currency accounts, effective February 1 (CBR 1998b; Nezavisimaia Gazeta 1998). According to the CBR, the RR changes along with rate hikes helped discourage speculative bets against the ruble (Interfax AIF 1998).

In the post-default period of 1998, the 1998 Guidelines became obsolete, as the CBR no longer upheld the rigid ruble corridor; post-default RR policy, therefore, did not necessarily conform to the parameters of the 1998 Guidelines (CBR 1999).

CBR implemented the first of the post-default RR relaxations on August 24 and communicated the decision at least as early as August 22, based on contemporary news articles (Segodnia 1998b). The CBR’s subsequent RR change, implemented on September 1, may not have been publicly disclosed until after the fact, since news articles reported on the change several days later (Ekonomika i Zhizn’ 1998; Vremia MN 1998). Additionally, one article reported that the September 1 change—namely, the differentiating of RRs based on banks’ exposure to defaulted treasuries—would be in effect for two years, ending September 1, 2000 (Vremia MN 1998). Before the end of the year, on December 1, 1998, the CBR replaced this RR policy with a unified RR ratio (CBR 1999).

Despite some of the CBR’s inconsistent RR communication in the post-default period, the CBR disclosed RR policy more transparently than other liquidity operations. The CBR regularly detailed changes in RR measures on its website and in its monthly bulletin (CBR 1998c; CBR 1998e). In contrast, the CBR did not publicly disclose many of the operations of its lending programs in the post-default period, a choice that drew frequent criticism in the press (Ladygin 1999; Rao 1998). See Key Design Decision No. 18, Disclosure, in Hoffner (2022b) for further discussion on the limited disclosure of CBR lending facilities.

Assets Qualifying as Reserves

1

The CBR did not allow banks to use any income-generating assets when depositing RR account funds (CBR 1996, 37, article 1.8). To form RR accounts, banks had to transfer rubles from their correspondent accounts to RR accounts, indicating that qualifying assets were all denominated in rubles (CBR 1996, 37, article 3.2). Additionally, banks would subtract any ruble cash on hand from the amount owed when computing their RRs (CBR 1998a, 175-U, annex 1).

Reservable Liabilities

1

The CBR defined reservable liabilities as either ruble or foreign currency liabilities in settlement accounts, current and deposit accounts, budgetary accounts (debts to the government), and extra-budgetary accounts (debts to pensions and other quasi-government accounts) (CBR 1998a, vol. 175-U, para. 2.1).

As described in Key Design Decision No. 10A, Changes in Reserve Requirements, before February 1, 1998, the CBR applied four different RR ratios according to maturity and currency of reservable liabilities: ruble demand accounts and time liabilities up to 30 days, ruble time liabilities between 31 and 90 days, ruble time liabilities over 90 days, and foreign currency funds (CBR 1998c). From February 1 until September 1, the CBR applied the same RR ratios regardless of the maturity or currency denomination of reservable liabilities (CBR 1998e; Nezavisimaia Gazeta 1998). On September 1, the CBR applied separate RRs for foreign currency liabilities before reunifying all RRs on December 1 (CBR 1998c).

Computation

1

To manage reserve requirements, the CBR developed a system in 1994 under which banks could choose among four options to calculate their respective deposit base subject to an RR. Banks calculated the size of their deposit bases monthly as of one of the following (Baliño, Hoelscher, and Horder 1997):

- The first day of the month

- The 16th day of the month

- The daily averages over the month

- The average of deposits at the end of each five-day period over a month

This fragmented system, however, provided for less transparency and consistency in how banks reported their deposits. As of May 1996, the CBR only allowed banks to report their deposit base using an average of daily balances between the 5th and 30th day of the month (Baliño, Hoelscher, and Horder 1997).

For mandatory reserves held in the RR account, the CBR allowed for an additional averaging mechanism accessible to banks that had complied with RRs in the preceding six-month period. Banks approved for this RR averaging had to ensure that the monthly average balance of their RR accounts complied with statutory RR ratios. However, on a given day, approved banks could reduce RR funds below the statutory ratio and transfer up to 5% of these funds to their correspondent accounts to settle interbank balances. As a result, such banks received additional liquidity from their RR funds (Baliño, Hoelscher, and Horder 1997).

The CBR implemented changes in RR ratios by shifting banks’ balances held in RR and correspondent accounts. For instance, when lowering RR ratios, the CBR transferred the excess funds of RR accounts to banks’ correspondent accounts, which banks could freely use for interbank payments (Segodnia 1998b).

The CBR developed a fee schedule, based on the refencing rate (policy rate), for banks whose reserves fell below required levels; see to Figure 2 (CBR 1996, appendix 10). However, the CBR did not always collect such fines. Key Design Decision No. 10B, Changes in Reserve Requirements, provides further information on the CBR’s decision to waive fees for select banks.

Figure 2: Fees Associated with Failing to Meet Reserve Requirements

Source: CBR 1996, 37, appendix 10.

Eligible Institutions

1

The 1990 Federal Law on Banks and Banking defined a credit institution as a legal entity, licensed by the CBR to carry out banking operations in pursuit of profit, as its main objective. Credit institutions were domestically licensed and sorted into two categories: banks and non-bank credit institutions (NBCOs). Banks were exclusively allowed to attract deposits from individuals and businesses, which they could then use to invest or make payments (Russian Federation 1990, 395–I, article 1). Article 25 of the law required all credit institutions to adhere to the RR ratios put forth by the CBR (Russian Federation 1990, 395–I, article 25).

Between February 1 and September 1, 1998, all “credit institutions,” with the exception of Sberbank, faced the same RR terms on their liabilities (CBR 1999). Sberbank was the state-owned savings bank and possessed about three-quarters of household deposits in Russia (IMF 1999). Sberbank benefited from an already lower RR ratio for its ruble-denominated household-deposits than commercial banks faced (CBR 1998e). When the CBR changed the RR system on September 1, 1998, by differentiating ratios according to three tiers, the CBR set Sberbank’s RR ratios on the lowest of the tiers (CBR 1999).

Timing

1

In the pre-default period—from the start of 1998 to August 17—the CBR changed the RR only once, on February 1, by unifying the otherwise differentiated RR system along a single RR ratio (CBR 1998e). As part of the same announcement, the CBR also dramatically increased the refinancing rate from 28% to 42%, effective February 2, with the primary CBR lending facility (Lombard) also adopting this higher rate. Together, these CBR measures attempted to bolster ruble demand and maintain the exchange rate corridor (Interfax AIF 1998).

The treasury default and ruble devaluation resulted in immense portfolio losses and heavy foreign debt exposures for commercial banks; subsequently, in the post-default period, the CBR implemented RR policy measures more frequently and aggressively (CBR 1998e; Ippolito 2002). On August 24, 1998, one week after the default, the CBR reduced RR ratios unilaterally (CBR 1999). On September 1, one week after this reduction, the CBR relaxed RRs sharply to help banks with large treasury exposures. On the same day, the ruble depreciated past the limits of the corridor, prompting the CBR to switch to a floating exchange rate on September 2 (Antczak 2001; CBR 1999).

The CBR implemented the next official RR change on December 1, 1998, during a scheduled review of RRs. The CBR conducted these RR reviews, which included examinations of RR compliance, twice in the post-default period: on September 1 and December 1 (CBR 1999).

Changes in Reserve Requirements

2

Throughout the 1998 crisis, the CBR implemented many changes to its RR policy; this case identifies four categories of changes:

- Changes to RR ratios for commercial banks

- Changes to RR ratios for Sberbank

- Changes to the calculation of foreign currency RRs

- Discretionary RR changes

Commercial Banks

Before February 1, 1998, the CBR differentiated RR ratios with respect to both maturity (demand vs. time deposits) and currency account (ruble vs. foreign-denominated) (CBR 1998c). Beginning February 1, the CBR simplified RRs to a common 11% ratio for all “attracted funds” regardless of term and currency (CBR 1998e; Nezavisimaia Gazeta 1998). This change represented a reduction in short-term ruble RRs, which typically exceeded RRs on foreign currency deposits, and an increase in foreign currency RRs. The CBR maintained this unified 11% RR ratio until just after the default on August 17 (CBR 1998c).

Post-default, on August 24, the CBR lowered the unified RR ratio from 11% to 10%; the change amounted to a liquidity injection of RUR 4 billion (Segodnia 1998b).

With effect September 1, and lasting through the end of November, the CBR lowered RR ratios based on a three-tier system. Figure 3 summarizes the tiers, which depended on a commercial bank’s exposure to defaulted ruble treasuries (GKO-OFZ) (CBR 1998c).

Figure 3: RR Ratios for Russian Commercial Banks, September 1–November 30, 1998

Source: CBR 1998c

Source: CBR 1998c

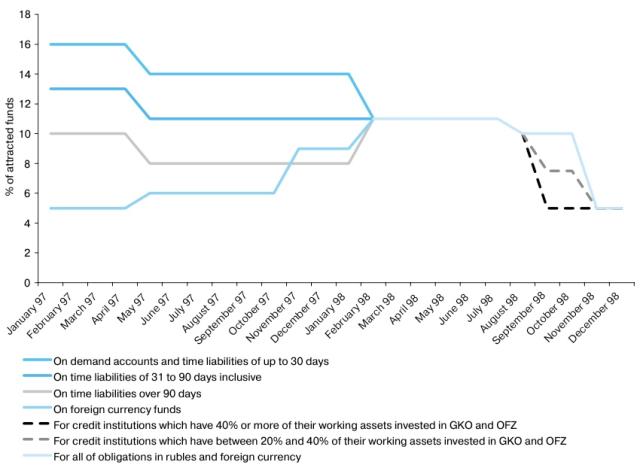

Finally, on December 1, the CBR once again unified RRs to a single ratio of 5% on all liabilities in ruble and foreign currencies (CBR 1998c). See Figure 4 for a complete timeline of RR ratio changes from the beginning of 1997 to the end of 1998.

Figure 4: Changes in Required Reserve Ratios for Russian Commercial Banks, 1997–1998

Source: CBR 1998c.

Source: CBR 1998c.

Sberbank

Throughout 1998, Russia’s state-owned bank, Sberbank, faced separate RR ratios for certain account types, which the CBR also changed on August 24 and September 1. From the start of 1998 until August 24, the RR ratio on Sberbank’s ruble-denominated household deposits remained constant at 8%; the CBR cut the rate to 7% on August 24 and then to 5% on September 3. The CBR also cut the RR ratio on Sberbank’s ruble and foreign currency liabilities to 5% on September 1 (CBR 1999).

Calculation of RRs for Foreign Currency Liabilities

On September 17, 1998, the CBR changed its method for calculating foreign currency borrowings subject to RRs. Thereafter, all RRs on foreign currency borrowings were revalued according to the ruble exchange rate as of August 14, 1998, pre-default and before the ruble devaluation (CBR 1999).FPer Bloomberg, USD 1.00 = RUR 6.27 on August 14, 1998. By September 17, 1998, USD 1.00 = RUR 12.45. This revaluation contributed to a decline in banks’ required reserves from RUR 11.6 billion at the end of August to RUR 6.8 billion at the end of September (Owen and Robinson 2003). Beginning on December 1, the CBR recalculated the value of foreign currency borrowings subject to RRs at the current ruble exchange rate (CBR 1999). In context, required reserves on foreign currency borrowings rose from RUR 4.8 billion at the end of November to RUR 8.3 billion at the end of December 1998 (Owen and Robinson 2003).

Discretionary RR Changes

Sources suggest that the CBR made various relaxations in RR ratios for individual banks on a case-by-case basis between the two official RR adjustment dates, on September 1 and December 1, 1998. Following the third round of multilateral clearing operations, a contemporary news article discussed how the CBR planned to change the RR policy to implement discretionary, bank-specific RR reductions (Cherkasov 1998). On October 7, another news article reported that a CBR representative had said that the CBR would likely take advantage of its legal power to differentiate RRs by individual banks (Segodnia 1998c). Antczak (2001) provides additional evidence by noting that in the post-default period, RR ratios differed significantly among banks, and the largest banks often received the lowest RRs. The CBR’s traditional RR disclosures, namely its monthly bulletin and website, did not, however, detail bank-specific RR changes (CBR 1998c; CBR 1998e).

Despite the CBR’s significant relaxing of RR in the post-default period, banks, in large part, failed to meet the reduced requirements because of the treasury defaults and depreciated ruble. Between January and August of 1998, the CBR noted that shortfalls on RRs ranged from 0.3% to 0.4%. In the post-default period, the CBR conducted two reviews of banks’ RRs, on September 1 and December 1, and found RR shortfalls of 2.5% and 18.6%, respectively. Between these two reviews, the CBR continued to relax requirements alongside three iterations of multilateral clearing operations to cancel debts between participating banks (CBR 1999). Following the December 1 review, the CBR neither levied fines against nor collected the reserve shortfalls of these participating banks. The CBR granted regulatory forbearance to “create favourable conditions for the implementation of measures to overcome financial difficulties” (CBR 1999).

Changes in Interest/Remuneration

1

Banks’ RR accounts with the CBR were unremunerated, which afforded the CBR greater influence over the exchange rate by changing the cost of borrowing in ruble or foreign currencies through RR policy (Baliño 1998; CBR 1996, article 1.9).

The CBR offered a remunerated deposit facility (deposit accounts) where banks could deposit surplus funds at CBR branches. Historically, banks expressed little interest in the facility since rates, set by the CBR, fell significantly below treasury yields. The CBR allowed domestic banks to deposit funds through fixed-maturity auctionsFIt is unclear if the CBR used an auction process for its deposit facility in 1998 since the IMF sources covered CBR operations through 1997 (Baliño, Hoelscher, and Horder 1997). on an overnight, next-day, one-week, and two-week (beginning October 8, 1998) basis (Baliño, Hoelscher, and Horder 1997; CBR 1999). Throughout the year, the CBR changed terms of the deposit facility both to regulate liquidity and support monetary policy. Over the course of 1998, interest rates on the deposit facility ranged from 3% to 80% annually (CBR 1999). The CBR changed interest rates on the deposit facility in correlation with other domestic interest rates, such as the rates on Lombard lending and interbank financing (CBR 1998c). In 1998, the CBR also expanded eligibility for the deposit facility by lowering the minimum deposit requirement from RUR 50 million to RUR 30 million on October 26, then to RUR 20 million on November 23 (CBR 1999).

Other Restrictions

1

We have not discovered additional restrictions on reserve requirements.

Impact on Monetary Policy Transmission

1

On August 17, along with the government’s default on ruble treasuries, the CBR widened the ruble corridor from a tight band (+/- 15%) of around RUR 6.20 per US dollar to a wider range of between RUR 6.00 and 9.50—which it intended to maintain through the end of 1998 (CBR 1999). The subsequent relaxation of RRs on August 24 added RUR 4 billion to banks’ correspondent accounts, which freed up additional ruble funds to be sold on the foreign exchange market (Nezavisimaia Gazeta 1998; Owen and Robinson 2003). The ruble continued to depreciate, which the CBR attempted to offset through foreign exchange interventions. On September 1, the same day the CBR introduced large RR relaxation measures, the ruble fell below the limit of the wider corridor; the CBR opted not to intervene and instead switched to a floating exchange rate, beginning September 2 (Antczak 2001; CBR 1999). Less than one week after the float, the ruble depreciated to RUR 20 per US dollar and thereafter stabilized to RUR 15.00-16.00 per US dollar, as shown in Figure 5 (Antczak 2001).

Figure 5: Daily Ruble Exchange Rate, August 1998–January 1999

Source: Antczak 2001.

Source: Antczak 2001.

With the switch to a floating exchange rate, the goals of monetary policy shifted, and for the CBR, “control over the money supply became the most important tool to combat inflation” (CBR 1999). Yet the CBR noted that its responsibilities for both handling the economic crisis—absent of government budget resources post-default—and controlling inflation “contradicted one another” (CBR 1999). The CBR’s initial crisis response, including large relaxations of RR, took the form of large liquidity injections to revive the illiquid banking system, at the expense of inflation (CBR 1999; Owen and Robinson 2003). Inflation climbed through the end 1998, and the CBR began tightening monetary policy in the beginning of 1999 (Owen and Robinson 2003).

Duration

1

According to a contemporary news article, when the CBR changed RR policy on September 1, 1998, the CBR indicated that this new system of differentiating RR based on ruble treasury holdings would remain in place for two years, until September 1, 2000 (Vremia MN 1998). Nevertheless, on November 16, 1998, the CBR decided to further lower the RR and, beginning December 1, the CBR used a uniform 5% RR ratio for all banks’ borrowings (CBR 1999).

After the resolution of many of the payment blockages in the domestic banking system, and as inflation persisted, the CBR started tightening monetary policy later in the first quarter of 1999. The CBR raised RR ratios from 5% to 7% in March and to 8.5% in June (CBR 2000; Owen and Robinson 2003).

Key Program Documents

-

(CBR 1996) Central Bank of the Russian Federation (CBR). 1996. On Mandatory Reserves of Credit Institutions Deposited with the Central Bank of the Russian Federation. 37 N.

CBR order detailing the rules and procedures for required reserves.

-

(CBR 1998a) Central Bank of the Russian Federation (CBR). 1998a. On Introducing Amendments and Additions to the Regulations of the Bank of Russia “On Mandatory Reserves of Credit Institutions Deposited with the Central Bank of the Russian Federation.” 175-U N.

CBR instruction introducing new changes to reserve requirements in 1998.

-

(Central Bank Law 1990) Central Bank Law. 1990. On the Central Bank of the Russian Federation, Article 38. N 394-1 FZ.

Article 38 of the Law on the Central Bank, describing the rules for reserve requirements, including amendments through 1998.

-

(Russian Federation 1990) Russian Federation. 1990. The Federal Law on Banks and Banking. 395–I FZ.

Federal Law establishing the rules and regulations of the banking system.

-

(Russian Federation 1993) Russian Federation. 1993. “Constitution of the Russian Federation,” 1993.

Document of the Russian Constitution outlining the CBR’s legal responsibilities.

-

(Buza 1998) Buza, Vitaly. 1998. “Short (September 26, 1998).” Segodnia, September 26, 1998.

Article discussing the second multilateral clearing operation held on September 25, 1998.

-

(Cherkasov 1997) Cherkasov, Denis. 1997. “Banks Ask to Loosen Monetary Policy.” Kommersant, November 26, 1997.

Article discussing the CBR’s upcoming submission of its Guidelines for Single State Monetary Policy for 1998 and the ARB’s requests.

-

(Cherkasov 1998) Cherkasov, Denis. 1998. “Banks Passed the Third Test.” Izvestiia, October 7, 1998.

Article discussing the third round of multilateral clearing operations, which took place on October 2, 1998.

-

(Ekonomika i Zhizn’ 1997) Ekonomika i Zhizn’. 1997. “Monetary Policy for 1998 in Experts’ Estimates,” November 29, 1997.

Article discussing the CBR’s Guidelines for Single State Monetary Policy for 1998, which was not approved by the State Duma.

-

(Ekonomika i Zhizn’ 1998) Ekonomika i Zhizn’. 1998. “Central Bank of Russia. Board of Directors. Decision Dated September 1, 1998. On Measures to Protect the Deposits of the Population in Banks,” September 12, 1998.

Article discussing the CBR’s monetary policy decisions on September 1, 1998, including changes to reserve requirements.

-

(Interfax AIF 1998) Interfax AIF. 1998. “Theme of the Week (February 2, 1998),” February 9, 1998.

Article describing the CBR’s comments on the RR changes introduced on February 1, 1998.

-

(Kuzmichev 1998) Kuzmichev, Vladislav. 1998. “Reduce the Independence of the Central Bank Failed.” Nezavisimaia Gazeta, June 18, 1998.

Article discussing the failed draft bill to reduce CBR independence.

-

(Ladygin 1999) Ladygin, Dmitry. 1999. “‘Beavers’ Flew Away.” Kommersant, December 15, 1999.

Newspaper article discussing the first OBR auction for 1999.

-

(Moiseev 1998) Moiseev, Igor. 1998. “Deputies Want to Put the Central Bank ‘Failed.’” Segodnia, March 6, 1998.

Article discussing a draft law in parliament that would reduce the CBR’s independence by giving the State Duma the authority to reject the CBR’s main directions of monetary policy for each year.

-

(Nezavisimaia Gazeta 1998) Nezavisimaia Gazeta. 1998. “Short (January 31, 1998),” January 31, 1998.

Article discussing the CBR’s RR changes to be implemented on February 1, 1998.

-

(NG Polytechnics 1998) NG Polytechnics. 1998. “The Central Bank Should Be Responsible for Its Business,” April 14, 1998.

Article describing the Federation Council’s draft law, which attempted to reduce the CBR’s independence.

-

(Rao 1998) Rao, Sujata. 1998. “Central Bank Tries New Loan Scheme.” Moscow Times, October 9, 1998.

News article describing monetary operations in the aftermath of the default where treasury instruments froze.

-

(Russian Telegraph 1998) Russian Telegraph. 1998. “The Central Bank Revives the Payment System.” Russian Telegraph, September 18, 1998.

News article discussing the CBR’s commencement of multilateral clearing operations on September 18, 1998.

-

(Segodnia 1998a) Segodnia. 1998a. “Short (June 6, 1998),” June 6, 1998.

Article discussing the ARB’s proposal for a reduction in reserve requirements by the CBR.

-

(Segodnia 1998b) Segodnia. 1998b. “Short (August 22, 1998),” August 22, 1998.

Article discussing the CBR’s RR changes to be implemented on August 24, 1998.

-

(Segodnia 1998c) Segodnia. 1998c. “Short (October 7, 1998),” October 7, 1998.

Article discussing the CBR’s consideration of setting bank-specific RRs.

-

(Vremia MN 1998) Vremia MN. 1998. “The Central Bank Established Differentiated Standards of Mandatory Reserves,” September 3, 1998.

Article discussing the CBR’s RR changes on September 1, 1998.

-

(CBR 1998b) Central Bank of the Russian Federation (CBR). 1998b. “On the Norms of Required Reserves of Credit Institutions and the Savings Bank of the Russian Federation Deposited with the Bank of Russia,” January 30, 1998.

CBR telegram communicating the first change to reserve requirements in 1998.

-

(Baliño 1998) Baliño, Tomás J. T. 1998. “Monetary Policy in Russia.” Finance and Development 35, no. 4 (December 1998).

Article in IMF publication describing the developments of the CBR’s monetary policy tools up to 1998.

-

(CBR 1998c) Central Bank of the Russian Federation (CBR). 1998c. “Bulletin of Banking Statistics No. 12 (67),” 1998.

Archived monthly publication of banking statistics as of the end of November 1998 including monetary operations of the CBR.

-

(CBR 1998d) Central Bank of the Russian Federation (CBR). 1998d. Legal Status.

Archived CBR webpage outlining the various legal frameworks relevant to the Russian banking system and the CBR.

-

(CBR 1998e) Central Bank of the Russian Federation (CBR). 1998e. “Monetary Policy Measures.” Updated November 24, 1998, 1998.

An archived webpage of the CBR listing monetary policy measures through the end of 1998.

-

(CBR 1999) Central Bank of the Russian Federation (CBR). 1999. “Annual Report 1998,” 1999.

1998 annual report by the CBR describing the liquidity operations during the crisis.

-

(CBR 2000) Central Bank of the Russian Federation (CBR). 2000. “Annual Report 1999,” 2000.

1999 annual report by the CBR describing the developments in CBR liquidity operations after the crisis.

-

(IMF 1999) International Monetary Fund (IMF). 1999. “Russia: Recent Economic Developments.” IMF Staff Country Report No. 99/100, September 1999, 1999.

IMF staff report reviewing the developments in the Russian economy, particularly in 1998 during the crisis.

-

(Antczak 2001) Antczak, Rafal. 2001. “The Russian Crisis of 1998.” In The Episodes of Currency Crises in the European Transition Economies, edited by Marek Dabrowski, 23–51. CASE Report 40. Warsaw: Center for Social and Economic Research.

Report detailing the CBR’s intervention during the 1998 crisis.

-

(Baliño, Hoelscher, and Horder 1997) Baliño, Tomás J. T., David S Hoelscher, and Jakob Horder. 1997. “Evolution of Monetary Policy Instruments in Russia.” IMF Working Paper 97/180, December 1997.

IMF report describing the development of monetary instruments through 1997 in Russia.

-

(Chiodo and Owyang 2002) Chiodo, Abbigail J., and Michael T. Owyang. 2002. “A Case Study of a Currency Crisis: The Russian Default of 1998.” Federal Reserve Bank of St. Louis Review 84, no. 6 (November/December) 2002: 7–18.

Article describing the 1998 Russian debt default.

-

(Hoffner 2022a) Hoffner, Benjamin. 2022a. “Russia: Central Bank Bonds, 1998.” Journal of Financial Crises 4, no. 2.

Case study on the CBR’s introduction of its own Bank of Russia bonds (OBRs) as part of its liquidity relief during the 1998 Russian crisis.

-

(Hoffner 2022b) Hoffner, Benjamin. 2022b. “Russia: Lombard and Overnight Loans, 1998.” Journal of Financial Crises 4, no. 2.

Case study on the developments of Lombard and overnight/intraday lending during the 1998 Russian crisis.

-

(Ippolito 2002) Ippolito, Filippo. 2002. “The Banking Sector Rescue in Russia.” BOFIT Online 2002/12, December 2002, 2002.

Report from the Bank of Finland Institute for Economies in Transition covering the stabilization loans by the CBR in 1998.

-

(Johnson 2018) Johnson, Juliet. 2018. A Fistful of Rubles: The Rise and Fall of the Russian Banking System. Ithaca, NY: Cornell University Press.

Book discussing the history of the CBR and its actions in 1998 during the crisis.

-

(Owen and Robinson 2003) Owen, David Edwin Wynn, and David O. Robinson. 2003. Russia Rebounds. Washington, DC: International Monetary Fund.

Book discussing the structural reforms in Russia, particularly those related to restructuring in 1999.

Taxonomy

Intervention Categories:

- Reserve Requirements

Countries and Regions:

- Russia

Crises:

- Russian Ruble Crisis (1998)