Account Guarantee Programs

Romania: Bank Deposit Guarantee Fund

Purpose

To maintain confidence in the financial system and to ensure its proper functioning in the global financial context

Key Terms

-

Launch DatesIncrease to EUR 50,000 Announcement: Oct. 12, 2008 Authorization: Oct. 14, 2008 Operation: Oct. 15, 2008 Increase to EUR 100,000 Announcement: Dec. 28, 2010 Authorized: Dec. 28, 2010 Operation: Dec. 31, 2010

-

End DateAdopted as permanent, with the ultimate guarantee set at EUR 100,000

-

Eligible InstitutionsAll institutions registered with the National Bank of Romania; foreign banks also eligible for coverage

-

Eligible AccountsVarious deposit accounts

-

Fees0.1% on covered deposits in 2008, 0.2% in 2009 and 2010

-

Size of GuaranteeOriginally EUR 50,000. Later raised to EUR 100,000

-

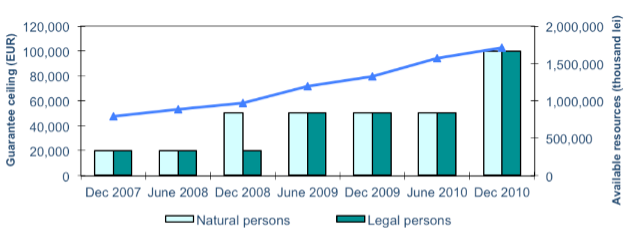

CoverageCovered RON 75.3 billion in 2009

-

OutcomesNo failures between 2008 and 2010

-

Notable FeaturesThe FGDB was partially funded by standby credit lines until 2010; The FGDB could mandate banks to make payouts on its behalf

Key Design Decisions

Purpose

Part of a Package

Administration

Governance

Communication

Size of Guarantee

Source and Size of Funding

Eligible Institutions

Eligible Accounts

Fees

Process for Exercising Guarantee

Other Restrictions

Duration

Key Program Documents

Taxonomy

Intervention Categories:

- Account Guarantee Programs

Countries and Regions:

- Romania

Crises:

- Global Financial Crisis