Broad-Based Asset Management Programs

The Resolution and Collection Corporation of Japan

Purpose

“[A]ccelerate the recovery and collection of non-performing loans transferred from failed [and solvent] financial institutions through a fair and transparent process in order to minimize public costs” (DICJ 2005a, i).

Key Terms

-

Launch DatesAnnouncement (merger): October 1998 Operational: April 1, 1999

-

Wind-down DatesExpiration date for transfers: N/A for insolvent; March 31, 2005, for solvent

-

Size and Type of NPL ProblemOfficial estimate of 17% of banking system loans in 1998 (Lincoln 1998) Corporate, equities, and real estate

-

Program SizeNot specified at outset

-

Eligible InstitutionsAll Japanese financial institutions Both open and closed banks

-

UsageSolvent: ¥353 billion (purchase price) for ¥4,004 billion (book value, approximately $37 billion) Insolvent: ¥6,366 billion (purchase price) for an estimated ¥29,000 billion (book value)

-

OutcomesSolvent: Recovered ¥642 billion on ¥353 billion Insolvent: Recovered ¥7,143 billion on ¥6,366 billion

-

Ownership StructureGovernment-owned

-

Notable FeaturesSpecial investigative powers to take on difficult cases such as those tied to organized crime; purchased loans at a steep discount; created from merger of prior asset management agencies

Though the Japanese real estate and stock market bubble burst in the early 1990s, the ensuing financial crisis in Japan did not reach a systemic level until 1997, when four large financial institutions failed in a single month. Because of their heavy exposure to real estate and equity markets, Japanese banks had a nonperforming loan (NPL) problem, which was prolonged, and private sector estimates of the scale of the NPL problem differed significantly from the official estimates. In response, the Japanese government created multiple asset management companies; the Resolution and Collection Corporation (RCC) was the result of the merger of two narrowly focused, semi-governmental agencies. The RCC, which began operating in 1999, was tasked with purchasing NPLs from both solvent and insolvent financial institutions. In 2001, its scope was expanded to include corporate restructuring and revitalization. Though there was no specified sunset date for insolvent institutions, the purchase window for solvent financial institutions ended on March 31, 2005. The RCC purchased ¥4,004 billion (approximately $37 billion) in bad debt (book value) at a purchase price of ¥353 billion from solvent institutions by March 2005, and it collected ¥642 billion by March 2008. The RCC purchased ¥6,366 billion in assets (estimated ¥29,000 billion book value) from failed financial institutions and recovered ¥7,143 billion by the end of March 2008. Though the RCC is operational as of today, its operations are no longer focused on resolving the 1990s crisis.

|

GDP per capita (SAAR, nominal GDP in LCU converted to USD) |

$31,903 in 1998 $36,027 in 1999 |

|

Sovereign credit rating (5-year senior debt) |

Data for Q4 1998: Fitch: AAA Moody’s: Aa1 S&P: AAA

Data for Q4 1999: Fitch: AAA Moody’s: Aa1 S&P: AAA |

|

Size of banking system |

$9,727 billion in 1998 $11,331 billion in 1999 |

|

Size of banking system as a percentage of GDP |

215.1% in 1998 223.9% in 1999 |

|

Size of banking system as a percentage of financial system |

79.2% in 1998 78.5% in 1999 |

|

5-bank concentration of banking system |

43.6% in 1998 42.1% in 1999 |

|

Foreign involvement in banking system |

Data not available for 1998–1999 |

|

Government ownership of banking system |

Data not available for 1998–1999 |

|

Existence of deposit insurance |

Yes in 1998 Yes in 1999 |

|

Sources: Bloomberg, World Bank Global Financial Development Database, World Bank Deposit Insurance Dataset. |

The Japanese financial crisis of the 1990s was prolonged as banks and the government were slow to acknowledge and respond to a massive nonperforming loan (NPL) problem. In 1998, two asset management agencies merged to create the Resolution and Collection Corporation (RCC), which was tasked with the purchase and disposal of NPLs from solvent and insolvent financial institutions. The RCC began operations in 1999, but its operations were limited, as the full scale of the NPL problem was still not recognized.

The government took more aggressive action to address the NPL problem in 2001 by adding corporate restructuring and revitalization to the RCC’s scope. In 2002, the RCC was allowed to purchase NPLs from solvent institutions at market value. The deadline to purchase assets from solvent institutions was March 31, 2005, but no deadline was set for failed institutions. By March 2005, the RCC had purchased ¥4,004 billion of loans (book value), approximately $37 billion, at a purchase price of ¥353 billion from solvent institutions, and it had recovered ¥642 billion by March 2008. The RCC recovered ¥7,143 billion on total purchases of ¥6,366 billion (estimated ¥29,000 billion book value) from failed financial institutions by March 31, 2008. The RCC assisted with corporate restructuring of 569 borrowers between 2001 and 2008.

Many observers believe that Japan’s banking problems were prolonged in the 1990s and 2000s due to the unwillingness of the government and financial sector to recognize the extent of the NPL problem. The RCC, which the government created to address the NPL problem, has been criticized due to its relatively limited scope: it ultimately purchased a total of ¥33 trillion in loans (book value); private economists at the time estimated the NPL problem at ¥100 trillion to ¥250 trillion. Others argue that the RCC was limited in effectiveness as the purchase price offered to solvent financial institutions was often steeply discounted because the RCC sought to minimize the risk of transferring losses to taxpayers. Others have stated that corporate restructuring was outside the RCC’s value-adding capabilities. However, it has been recognized that the RCC recovered in excess of its purchase price in its disposal of assets from failed and solvent institutions.

Key Design Decisions

Part of a Package

2

Over the course of 1998, the Japanese government passed several laws to address the systemic financial crisis. The Financial Function Stabilization Act, passed in February 1998, made ¥30 trillion available to the government for capital injections and deposit protection (Hoshi and Kashyap 2010). In October 1998, the Diet, the Japanese legislative body, passed the Financial Revitalization Act and replaced the Financial Function Stabilization Act with the Prompt Recapitalization Act (DICJ 2008). The Prompt Recapitalization Act “stipulate[d] a temporary emergency measure regarding capital injection to financial institutions” (DICJ 1999). The Financial Reconstruction Committee was established in 1998 to oversee the bank restructuring process (Kanaya and Woo 2000).

The government approved two rounds of capital injections: the first, under the Financial Function Stabilization Act, in March 1998 (¥1.8 trillion) and the second, under the Prompt Recapitalization Act, in March 1999 (¥7.5 trillion) (Hoshi and Kashyap 2010). The RCC could purchase preferred shares and subordinated debt from financial institutions as a part of the Prompt Recapitalization Act, though the capital injections were overseen by the Financial Reconstruction Committee.FFor more information on the 1998 and 1999 capital injections, see the forthcoming cases on the broad-based capital injections in Japan in the Journal of Financial Crises.

The Financial Revitalization Act included the principles for the resolution of failed financial institutions (DICJ 1999). As a part of the Financial Revitalization Act, the HLAC and the RCB were merged to create the RCC, which commenced operations on April 1, 1999 (Kanaya and Woo 2000). Concurrently, the government was in the process of nationalizing the Long-Term Credit Bank of Japan and the Nippon Credit Bank (Hoshi and Kashyap 2010).

The scope of the RCC was expanded in 2001 to include corporate debt restructuring and revitalization. Prime Minister Koizumi, in a policy speech to the Diet in 2001, stated that the function of the RCC would be expanded and that a fund for further corporate revitalization would be established (Koizumi 2001). The Front-Loaded Reform Program included a measure to reinforce the disposal of NPLs and stated that the RCC would “establish a headquarters for corporate restructuring in order to facilitate rehabilitation of companies” in November 2001 (Cabinet Office 2001a). In 2003, the government established another agency, the Industrial Revitalization Corporation of Japan, which was intended to work with the RCC to address the NPL problem in Japan. The IRCJ was given the purpose of restructuring the bad loans it purchased and assisting with the corporate revitalization of borrowers. The IRCJ had a purchase window of two years and focused on purchasing bad debt from distressed debtor companies that were viable and likely to be successfully rehabilitated (Takagi n.d.).

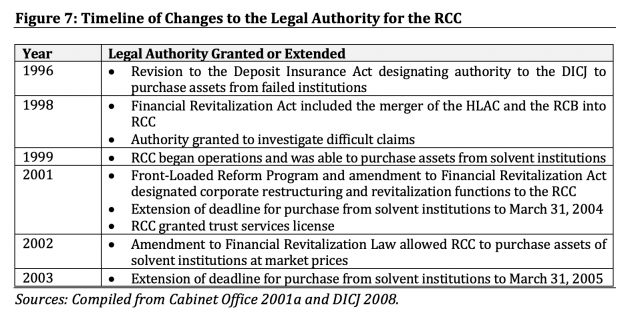

Legal Authority

1

The RCC was a fully owned subsidiary of the Deposit Insurance Corporation of Japan. The function to manage, collect, and dispose of assets from bankrupt institutions was designated to the DICJ in the Deposit Insurance Act; the DICJ was also designated the authority to take action on specified difficult collection claims, including claims tied to organized crime (DICJ 2008; Otake 1999b). The Deposit Insurance Act was amended in 1996 to allow the DICJ to purchase assets from failed institutions as a method to provide funds to failed financial institutions (Koo and Sasaki 2010). The Financial Revitalization Act was enacted in 1998 and established the RCC, from the merger of the RCB and the HLAC, as a subsidiary of the DICJ (DICJ 2008). Before the RCC began operations, the scope of its authority was expanded to include the purchase, management, collection, and disposal of assets from sound financial institutions, which was delegated in the Financial Revitalization Act (Koo and Sasaki 2010). The DICJ designated debt recovery and real estate management and disposal work to the RCC, which performed these activities “on behalf of the DICJ” (DICJ 2003).

Additional legal authority was delegated to the RCC in a variety of measures in the years after its establishment. In 2001, Prime Minister Junichiro Koizumi established a set of structural reform policies, which included corporate restructuring (Koizumi 2001), and the Front-Loaded Reform Program of 2001 stated that the RCC was to establish a corporate revitalization headquarters (Cabinet Office 2001a). The ability to purchase assets from solvent institutions at market value was delegated in an amendment to the Financial Revitalization Act in 2002 (DICJ 2008). Additionally, the RCC was granted a trust services license to engage in securitization and was given the authority to participate in auctions. The Program for Financial Revival, established by the Financial Services Agency and introduced in 2002, further reiterated that the scope of the RCC included corporate restructuring (FSA 2002). Furthermore, amendments to the Financial Revitalization Act in 2001 and 2003 ultimately prolonged the window for asset purchases from solvent institutions to March 31, 2005 (DICJ 2008).

Special Powers

1

The DICJ supported the RCC in the collection and recovery of assets from “malicious debtors and others” including “obstructed recovery cases involving antisocial forces” (DICJ 2008). Some considered the “antisocial forces,” also known as organized crime or the yakuza, to be a key factor contributing to the size of the NPL problem as well as the slow recovery and disposal of NPLs in Japan. Estimates for the number of loans related to the yakuza varied significantly, with one estimate at 80% and others at 10% or 30% (Holley 1996). Banks and financial institutions made loans to yakuza borrowers, some of which became nonperforming after the collapse of the real estate asset price bubble. In some cases, the yakuza prevented banks from foreclosing on property and prevented auctions, as the yakuza squatted in empty units and buildings (Sugawara 1995). By 2002, 18% of the loans the RCC had purchased were yakuza-related (Bremner 2002). The National Police Agency backed the RCC to aid with the seizure of property, and the DICJ established Special Investigation Divisions to enhance the recovery of assets. The DICJ “reinforced support for the fair handling of collections in obstructed recovery cases by providing meticulous guidance and advice to the RCC concerning the monitoring and analysis of behaviors of debts in the process of subsequent negotiation on recovery” (DICJ 2008).

Mandate

1

The RCC had the mandate to “accelerate the recovery and collection of non-performing loans transferred from failed [and solvent] financial institutions through a fair and transparent process in order to minimize public costs” (DICJ 2005a). The government later expanded the RCC’s scope and mandate to include corporate restructuring, a trust services license, and the ability to purchase NPLs at market value from solvent financial institutions.

Communication

1

With the establishment of the RCC, the government projected confidence in its ability to resolve the NPL problem. The president of the RCC was frequently quoted in press releases and articles in the Japan Times. He was seen as a strong leader of the organization (Otake 1999b). When he began to lead the RCC, he stated, “This new job is an urgent and important task since the banks’ blood vessels are clogged with bad loans” (Japan Times 1999a). Upon its establishment, the RCC was deemed to “[signal] the birth of a powerful state-backed organ to collect bad loans” (Otake 1999a). During the first purchase window for solvent financial institutions, the president of the RCC recognized that the total was less than anticipated but was confident that future windows would be more fruitful (Otake 1999b).

However, there was a “divergence between the government’s characterization of the condition of the banking industry and that of outsiders” (Hoshi and Kashyap 2010). There were conflicting messages regarding the scope of the NPL problem in Japan, with private estimates, bank estimates, and official estimates varying in the estimated scale of the problem; in fact, the “official estimates of bad loans were regarded as a ‘lower bound’” of the scope of the NPL problem (Tandon 2005). In a further example of the lack of consensus, IMF directors and government officials were not aligned on the urgency of the crisis. IMF analysts urged the government to take decisive and aggressive action given the scale of the crisis (Japan Times 1999d). However, the statements released by the government contradicted the IMF—in February 1999, an MOF official stated that the financial crisis would be over within a matter of weeks (Hoshi and Kashyap 2010).

In addition, there was public uncertainty and distrust of the government’s reforms and interventions, following the use of taxpayer funding of ¥685 billion for the jusen problem in 1996. This assistance was viewed unfavorably by the public, as it reflected the government reneging on its promise not to rely on taxpayer funds to resolve the crisis. After this experience, it became politically unpopular to advocate for programs that would utilize taxpayer funds for bank assistance (Nakaso 2001).

When the government began to expand the scope of the RCC to include corporate restructuring, a trust services license, and the ability to purchase NPLs at market value from solvent financial institutions, the government was presenting a message of confidence in the abilities of the RCC to work toward the objective of resolving the NPL crisis (Yanagisawa 2001). There was public speculation surrounding the RCC’s added functionalities, including hope that the RCC would “have the teeth to promote disposal of the banks’ huge bad loans, following in the footsteps of the Resolution Trust Corp” (Kishima 2001).

Furthermore, the government began to more aggressively combat the NPL problem in the early 2000s, with leaders making public statements about the need to address the crisis. Prime Minister Junichiro Koizumi actively spoke about the need to resolve the NPL problem, specifically stating that the RCC would be an important lever to do so (Koizumi 2001). Another key figure in addressing the NPL problem was the FSA minister, Heizo Takenaka, who developed the Program for Financial Revival, which set the goal to resolve the NPL problem by FY2004 (FSA 2002). Both Koizumi and Takenaka supported the proactive utilization of the RCC to mitigate the NPL crisis.

The IMF recognized that the FSA, BOJ, DICJ, and RCC all demonstrated “a high degree of transparency” in their operations (IMF 2003). The activities of the RCC were reported by the DICJ. The DICJ explicitly published the names of the failed firms receiving financial assistance in press releases and public statements, but it does not appear to have published the solvent financial institution participants. Press releases regarding failed firms outlined the financial assistance scheme, the book value of the assets transferred to the RCC, and the purchase price for the assets.FSee DICJ n.d. for examples of the financial assistance schemes for failed institutions.

Ownership Structure

1

The RCC was established via the merger of the Housing Loan Administration Corporation and the Resolution and Collection Bank, both of which were established in the years prior to 1998 to resolve bad debt from specific financial institutions or types of financial institutions. The HLAC was a 100% subsidiary of the DICJ, while the RCB was a 75% subsidiary of the DICJ. An amendment to the Deposit Insurance Act and the Financial Revitalization Act (also referred to as the Financial Function Reconstruction Law), enabled the merger of the two to create the RCC.

Governance/Administration

1

The former president of the HLAC, Kohei Nakabo, became the president of the RCC. The RCC was staffed by the previous HLAC and RCB employees (Otake 1999a). When the RCC was established in April 1999, it had approximately 1,900 employees (Nakaso 2001). According to an analysis of asset management companies published by the Bank for International Settlements, the RCC had “limited” independence in the legal environment and was not granted special legal protection for staff (Fung et al. 2004).

The DICJ oversaw and provided guidance to the RCC, while the FSA and BOJ provided external governance and oversight (Fung et al. 2004). The DICJ provided the RCC “with the guidance and advice necessary to execute its recovery activities; such as uncovering hidden assets by exercising the right to inspect properties” (DICJ 2005a).

Program Size

1

There were no restrictions placed on the RCC regarding the total sum of NPLs it could purchase (Fung et al. 2004).

Funding Source

1

The government of Japan provided the funding for the RCC. The DICJ issued government-guaranteed bonds and injected the proceeds into the RCC. At the time of its initial operations, the RCC had ¥212 billion in capital (Kang 2003). There was no loss-sharing arrangement for the RCC and selling institutions, as the RCC did not have recourse to the originator banks for the losses incurred when it sold collateral associated with a loan (Hoshi and Kashyap 2004). Because there was strong public sentiment to avoid incurring losses, the RCC purchased assets at a steep discount from book value—on average a 78% discount from failed institutions and a 91% discount from healthy institutions—making it unlikely that the RCC would recognize losses on the sale or collection of assets (Koo and Sasaki 2010; Nakaso 2001).

Eligible Institutions

1

According to Article 53 of the Financial Revitalization Act, the eligible institutions included: managed financial institutions, agreement successor banks, and special public management banks (Law No. 132 1998). The definition of “financial institution,” as presented in the Deposit Insurance Act, included major, regional, and city banks as well as credit unions and credit cooperatives (DIA 1971). Other eligible financial institutions included bridge banks, the Federation of Agricultural Cooperative Associations, and the Federation of Fisheries Cooperative Associations (DICJ 1998). Special public management banks refer to banks such as the Long-Term Credit Bank and Nippon Credit Bank, which were temporarily nationalized banks (Law No. 132 1998).

Eligible Assets

1

The types of assets that the RCC could purchase from solvent institutions included loans, suspense payments, interest receivables, and accounts receivables for borrowers classified as “bankrupt, de facto bankrupt or in danger of bankruptcy” (DICJ 2002a). Loans that were ineligible included loans to public welfare corporations, loans with disputed claims, loans to borrowers undergoing reorganization, loans to nonresidents, and loans for overseas real estate (DICJ 1999).

For the transfer of assets in the case of a failed institution, the assets eligible for purchase were the assets considered unsuitable for the bridge bank or banks under special management to hold (DICJ 1999).

Acquisition - Mechanics

2

The RCC was engaged as needed for insolvent financial institutions, as the DICJ was involved in overseeing the financial assistance process. In the case of a failed financial institution, the DICJ, FSA, and courts were involved in overseeing and managing the resolution process. The FSA appointed a financial administrator; if no assuming institution was found, the FSA found a bridge bank. The failed institution and assuming institution(s) submitted an application to the DICJ for assistance, and the DICJ determined whether to provide assistance. The financial assistance could take “the form of a monetary grant, loan or deposit of funds, purchase of assets, guarantee of liabilities, assumption of financial obligations, subscription of preferred shares, etc. or loss sharing.” If there was an assuming financial institution, the assets that the assuming bank did not want were transferred to the RCC. The purchase of assets would be agreed upon by the failed institution, the assuming financial institution(s) or bridge bank, the RCC, the DICJ, and the FSA (DICJ 2008).

For the purchase of assets from solvent financial institutions, the RCC announced the first application window when it began its operations; the application window was from June 22 to July 9, 1999 (Japan Times 1999c). The application window for solvent institutions “as a rule [took] place four times a year,” but the RCC was also able to consult with individual financial institutions on the purchase window if requested (DICJ 2003). After receiving applications, the RCC evaluated the applications from interested banks and offered a price to the banks; the DICJ provided guidance on the offer price. If interested, the banks then submitted a formal application to initiate the sale and would work with the RCC to coordinate the purchase (Japan Times 1999c). The window for sales was initially set to expire in 2001 but was ultimately extended to March 31, 2005 (DICJ 2008).

Acquisition - Pricing

1

The RCC determined the purchase price for NPLs on a case-by-case basis with guidance from the DICJ and the Purchase Price Examination Board (an advisory body) (Nanto 2009). The Purchase Price Examination Board was an advisory body of the DICJ governor (DICJ 2008). The Purchase Price Examination Board originally had three members, but it was expanded in 2002 to have five members (DICJ 2003). The RCC did not have recourse to the financial institutions selling the loans; thus, the RCC established a process to ensure the price “reflected fair value” (Packer 2000). The determination of the purchase price was to “[take] into consideration the risk of assets becoming uncollectable and the administrative expenses required for purchase and collection of the assets in question” (DICJ 1999). The RCC established a multistage process for pricing the NPLs in which a real estate appraiser submitted a valuation of the property, and the RCC, FRC, and DICJ reviewed and approved the valuation (Packer 2000). In addition, the RCC sought guidance from the MOF and FSA in determining purchase price (Japan Times 1999b). The purchase price also required approval from the prime minister, though the Financial Reconstruction Commission granted approval until January 2001 (DICJ 2008). In the first years of operations, the RCC purchased loans at a steep discount, paying an average of 3.8% of the original book value (Japan Times 2001b).

The steep discount the RCC paid for loans was considered to be a deterrent to healthy banks interested in selling their NPLs. In a Cabinet Report in 2001, the government recognized that the NPL problem was worsening and stated that “[t]he government will also make the price-setting formula more flexible in order to facilitate purchases of nonperforming loans by the Deposit Insurance Corporation of Japan and the RCC” (Cabinet Office 2001b). Given the increasing pressure to resolve the NPL problem, the government passed an amendment to the Financial Revitalization Act, effective January 2002, which allowed the RCC to purchase NPLs from “sound financial institutions at ‘market value’” (DICJ 2002a). However, some critics believed that this was not enough and advocated that the RCC should purchase loans at book value (Japan Times 2002a; 2002b). A cross-party coalition was established to study the proposal, and after analysis, the RCC president announced that he did not support the plan, as the RCC sought to avoid recognizing losses that would ultimately be transferred to taxpayers (Japan Times 2002c). As another measure to promote flexibility in purchase price, the RCC was given the ability to bid in NPL auctions in 2001 (IMF 2002). Between 1999 and 2005, the RCC’s purchase price of NPLs from solvent institutions was an average of 9% of book value (DICJ 2005b). According to an estimate, the RCC purchased assets from insolvent institutions at an average of 22% of book value (Koo and Sasaki 2010).

Management and Disposal

2

The RCC ultimately utilized the following methods for disposal of NPLs: collection, sales, securitization, and/or operational and financial restructuring. In its first years of operations, the RCC was limited in disposal methods, and the RCC was slow to dispose of assets (IMF 2002). The RCC received its trust license to securitize nonperforming assets in 2001, after which it began issuing asset-backed securities (Kang 2003). The Program for Financial Revival called for the RCC to accelerate the sales and collections of loans, which led the RCC announce its “Basic Policy Concerning the Liquidation and Securitization of Assets Held by the RCC,” under which the RCC would “more actively” consider sales and securitization when the methods were economically rational and advantageous. “The RCC adopted a method to sell multiple claims in bulk (bulk sales) through bidding at the end of FY2002” (DICJ 2008). Due to the expanded disposal options, the RCC was more aggressive in its disposal of NPLs between 2001 and 2008; its total balance of debt decreased from ¥5.8 trillion to ¥1.1 trillion (Hoshi and Kashyap 2010).

The corporate restructuring function was delegated to the RCC in 2001 through an amendment to the Financial Revitalization Act and the Cabinet Office’s Front-Loaded Reform Program. The Front-Loaded Reform Program called for the RCC to establish a headquarters for financial revival (Cabinet Office 2001a). The RCC began operations related to corporate restructuring in November 2001. The RCC established the Corporate Revitalization Study Committee as an advisory body with the purpose of evaluating the feasibility of each revitalization case (DICJ 2008). The corporate restructuring function was strongly encouraged in the FSA’s Program for Financial Revival in 2002 as well (FSA 2002). Corporate revitalization could take multiple forms: the RCC was involved in legal revitalization in which it utilized legal proceedings to enforce rehabilitation, and it was involved in cases of private revitalization that involved debt or business restructuring with the consent of other creditors (DICJ 2008). The RCC used its trust license to support the revitalization of firms for which a revitalization case was submitted to the RCC by a different financial institution. The RCC evaluated cases based on the following criteria: the continuation value of the business, the willingness of the firm to make repayments, disclosure transparency, and the economic rationality for the creditor (RCC 2018). Between November 2001 and March 31, 2008, the RCC assisted with 569 cases of revitalization (DICJ 2008). Overall, the RCC assisted with the restructuring of ¥6.2 trillion in debt (Hoshi and Kashyap 2010).

Timeframe

1

There was no official sunset date for the RCC, as the RCC continues to operate (with new capabilities and authority) to the present date (Fung et al. 2004; RCC 2018). The deadline for the purchase of NPLs from solvent institutions was initially set for March 31, 2001, and was later extended to March 31, 2005 (DICJ 2008).

The definition of nonperforming loans in Japan was initially inadequate, and provisioning standards were lax. Both of these factors contributed to a slow recovery and a difficult environment to resolve NPLs. The authorities gradually revised the regulatory frameworks, but the “lack of adequate provisioning and public disclosure obscured the actual status of the NPLs problem in the financial system and delayed the introduction of much needed comprehensive action” (Nakaso 2001).

In postcrisis analysis, some scholars have argued that the purchase price for NPLs from the solvent banks was too low, which disincentivized these banks from selling to the RCC. Proponents of this argument state that the usage of the RCC was limited as it “[offered] unattractive pricing to banks for the acquisition of NPLs … owing to political reluctance to recognize financial loss” (Fung et al. 2004). The move to allow the RCC to purchase NPLs at market value was seen as a step in the right direction to accelerate the disposal of bad loans. Takeo Hoshi and Anil Kashyap argue that the RCC case illustrates that asset purchase programs are not sufficient to address bank solvency problems (Hoshi and Kashyap 2010). According to an estimate from Richard Koo and Masaya Sasaki, the RCC was able to buy bad assets at a 78% discount to book value from failed institutions and a 91% discount to book value from healthy institutions. In addition, their analysis shows that the “total value of assets purchased by the [RCC from solvent institutions] was an order of magnitude lower than that of assets purchased from failed institutions” which is “a reminder of how difficult it is to remove assets on which large losses must be booked from the balance sheets of healthy institutions” (Koo and Sasaki 2010).

Others have argued that the RCC was not aggressive enough in its purchase and disposal of NPLs and that the RCC should have set performance and time-bound targets for disposal of assets (Kang 2003). Hoshi and Kashyap argue that the RCC was slow in selling off the loans it purchased and essentially operated as a warehouse for bad loans in the initial years of operations (Hoshi and Kashyap 2010). By 2002, the RCC had “played only a minor role in reducing bank NPLs, having so far purchased only ¥1.3 trillion in distressed assets (face value) at an average discount of 96 percent” (IMF 2002). Before 2001, the RCC could only collect or sell individual loans; after 2001, the RCC was able to securitize NPLs, assist with debt restructuring, and utilize bulk sales to dispose of loans. Due to the expanded disposal options, the RCC was more aggressive in its disposal of NPLs between 2001 and 2008; the total balance of debt decreased from ¥5.8 trillion to ¥1.1 trillion, and the RCC disposed of many assets for more than the purchase price (Hoshi and Kashyap 2010).

Other scholars argue that the RCC was valuable as it provided the opportunity for banks to remove NPLs from their portfolios in the absence of demand in the market (Fujii and Kawai 2010). By March 2005, the RCC had purchased ¥4,004 billion of NPLs (book value) from solvent institutions for a purchase price of ¥353 billion, and the cumulative amount of recoveries as of 2008 was ¥642 billion, with no additional purchases made (DICJ 2005b; 2008). The RCC purchased a total of ¥6,366 billion in NPLs from failed institutions and had collected ¥7,143 billion by March 2008 (DICJ 2008).

When the RCC was enabled to engage in corporate restructuring, there was criticism that the RCC lacked the expertise, bandwidth, and resources necessary to effectively restructure corporate debt. Some argued that the RCC “should focus on asset disposal and leave the lead role in corporate restructuring to the private sector” (Kang 2003). With the establishment of the IRCJ, some were concerned that there was no “clear-cut” delineation between the functions of the two bodies; Nicole Pohl argues that there were elements of “competition” between the two (Pohl 2005). Hoshi and Kashyap argue that “the division of labor between the RCC and IRCJ [was] not as clear as it is often discussed. However, the RCC was “ultimately involved” in restructuring ¥6.2 trillion in bad debts for 577 borrowers. The authors recognize that by assisting with corporate rehabilitation, the RCC began to address the underlying cause of the NPL problem in Japan (Hoshi and Kashyap 2010).

- Bank of Japan (BOJ). 2006. “Financial System Report.” July 10, 2006.

- Bremner, Brian. 2002. “The Yakuza: Bad Debts, Bad Men.” Bloomberg, February 22,…

- Caballero, Ricardo J., Takeo Hoshi, and Anil K. Kashyap. 2006. “Zombie Lending …

- Cabinet Office. 2001a. “Summary of the ‘Front-Loaded Reform Program.’” Governme…

- ———. 2001b. “Annual Report on Japan’s Economy and Public Finance 2000-2001.” Go…

- Deposit Insurance Act of Japan (DIA). 1971. Act No. 34 of April 1, 1971.

- Deposit Insurance Corporation of Japan (DICJ). n.d. Website: “Financial Assista…

- ———. 1999. “Annual Report 1998.” April 1998–March 1999.

- ———. 2000. “Annual Report 1999.” April 1999–March 2000.

- ———. 2001. “Annual Report 2000.” April 2000–March 2001.

- ———.2002a. “Purchase Price of Sound Institutions’ Assets under Article 53 of th…

- ———. 2002b. “Annual Report 2001.” April 2001–March 2002.

- ———. 2003. “Annual Report 2002.” April 2002–March 2003.

- ———. 2005a. “Annual Report 2004.” April 2004–March 2005.

- ———. 2005b. “Assets Purchased from Sound Financial Institutions.” Website: DICJ…

- ———. 2008. “Annual Report 2007/2008.” April 2007–March 2008.

- ———. 2013. “Annual Report 2012/2013.” April 2012–March 2013.

- Financial Services Authority (FSA). 2002. “Program for Financial Revival–Reviva…

- ———. 2003. “The Gap between Major Banks’ Self-Assessment and the Result of FSA’…

- Fujii, Mariko, and Masahiro Kawai. 2010. “Lessons from Japan’s Banking Crisis, …

- Fung, Ben, Jason George, Stefan Hohl, and Guonan Ma. 2004. “Public Asset Manage…

- Hayashi, Tomoaki. 2015. “Chapter 21: Japan: Regulatory Development of the Banki…

- Holley, David. 1996. “Japan Mob Muddies Real Estate Loan Crisis.” Los Angeles T…

- Hoshi, Takeo, and Anil K. Kashyap. 1999. “The Japanese Banking Crisis: Where Di…

- ———. 2004. “Solutions to the Japanese Banking Crisis: What Might Work and What …

- ———. 2010. “Will the U.S. Bank Recapitalization Succeed? Eight Lessons from Jap…

- International Monetary Fund (IMF). 2002. “Japan: Article IV Consultation—Staff …

- ———. 2003. “Japan: Financial System Stability Assessment and Supplementary Info…

- Japan Times. 1996. “‘Jusen’ Loan-Recovery Body Established.” July 27, 1996.

- ———. 1999a. “Debt Collector Starts Operation.” April 2, 1999.

- ———. 1999b. “RCC Plans Bad Loan Buys from June.” May 28, 1999.

- ———. 1999c. “RCC to Buy Risky Loans.” June 18, 1999.

- ———. 1999d. “Bank Restructuring Falls Short: IMF.” September 10, 1999.

- ———. 2001a. “Debt Collector Handed License to Speed Up Bad-Loan Disposal.” Sept…

- ———. 2001b. “Coalition Finalized Bill Adding to RCC’s Powers to Clear Loans.” O…

- ———. 2002a. “RCC Should Buy Bad Loans at Book Value: Yamasaki.” February 17, 20…

- ———. 2002b. “Coalition to Study Book-Value Buys by RCC.” February 21, 2002.

- ———. 2002c. “RCC Chief Airs Concern over ‘Secondary Losses.’” September 28, 200…

- Kanaya, Akihiro, and David Woo. 2000. “The Japanese Banking Crisis of the 1990s…

- Kang, Kenneth. 2003. “Chapter 4: The Resolution and Collection Corporation and …

- Kishima, Shinichi. 2001. “RCC’s Revamp Offers Hope against NPLs.” Japan Times, …

- Koizumi, Junichiro. 2001. “Policy Speech by Prime Minister Junichiro Koizumi to…

- Koo, Richard, and Masaya Sasaki. 2010. “Japan’s Disposal of Bad Loans: Failure …

- Law No. 132: Act on the Emergency Measures for Rehabilitation of Financial Func…

- Lincoln, Edward J. 1998. “Japan’s Financial Problems.” Brookings Institution. B…

- ———. 2002. “The Japanese Economy: What We Know, Think We Know, and Don't Know.”…

- Milhaupt, Curtis J., and Mark D. West. 2004. “Chapter 4: The ‘Jusen Problem.’” …

- Nakaso, Hiroshi. 2001. “The Financial Crisis in Japan during the 1990s: How the…

- Nanto, Dick K. 2009. “The Global Financial Crisis: Lessons from Japan’s Lost De…

- Otake, Tomoko. 1999a. “HLAC, RCB Merger Creates New Collection Agency.” Japan T…

- ———. 1999b. “Pile of Bad, Yakuza-Tied Debts Awaits New President of RCC.” Japan…

- Packer, Frank. 1994. “The Disposal of Bad Loans in Japan: A Review of Recent Po…

- ———. 2000. “Chapter 6: The Disposal of Bad Loans in Japan: The Case of the CCPC…

- Pohl, Nicole. 2005. “Industrial Revitalization in Japan: The Role of the Govern…

- Resolution and Collection Corporation (RCC). 2018. “Fiscal Year 2018 Overview o…

- Sugawara, Sandra. 1995. “Gangsters Aggravating Japanese Banking Crisis.” Washin…

- Takagi, Shinjiro. n.d. “Foundation of the Industrial Revitalization Corporation…

- Takenaka, Heizo. 2002. “Statement by Heizo Takenaka, Minister for Financial Ser…

- Tandon, Rameshwar. 2005. The Japanese Economy and the Way Forward. London: Palg…

- Unnava, Vaasavi. 2021. Financial Functions Stabilization Act. Forthcoming in th…

- Unnava, Vaasavi. 2021. Prompt Recapitalization Act. Forthcoming in the Journal …

- Yanagisawa, Hakuo. 2001. “Japan’s Financial Sector Reform: Progress and Challen…

- ———. 2002. “Japanese Financial Sector: Progress and Prospect.” Keynote address …

Key Program Documents

-

Assets Purchased from Sound Financial Institutions.

A summary of the RCC’s operations and purchases of assets from solvent institutions.

-

Program for Financial Revival–Revival of the Japanese Economy through Resolving Non-Performing Loans Problems of Major Banks.

A summary of the government’s financial sector reform program targeting the resolution of NPLs in 2002.

-

Summary of the ‘Front-Loaded Reform Program’.

A summary of the government’s financial sector reform program in 2001.

-

Purchase Price of Sound Institutions’ Assets under Article 53 of the Financial Revitalization Law.

A document outlining the RCC’s purchase price methodology for assets from solvent financial institutions.

-

Deposit Insurance Act of Japan.

The law establishing the deposit insurance system in Japan that outlines the DICJ’s authority.

-

Law No. 132: Act on the Emergency Measures for Rehabilitation of Financial Functions.

The statute passed in Japan in response to the escalating financial crisis.

-

Foundation of the Industrial Revitalization Corporation in Japan.

A document outlining the IRCJ in Japan from the leader of the agency.

-

Japanese Financial Sector: Progress and Prospect.

A speech on the progress of the financial sector restructuring from an official in the FSA.

-

Japan’s Financial Sector Reform: Progress and Challenges.

A speech on the progress of the financial sector restructuring from an official in the FSA.

-

Policy Speech by Prime Minister Junichiro Koizumi to the 153rd Session of the Diet.

A speech from the prime minister that covers financial sector restructuring and support.

-

Statement by Heizo Takenaka, Minister for Financial Services.

A speech from the minister for financial services outlining the government’s financial system restructuring.

-

The Gap between Major Banks’ Self-Assessment and the Result of FSA’s Inspections.

A press release announcing the discrepancies between banks’ self-assessments and the FSA’s assessments.

-

Bank Restructuring Falls Short: IMF.

An article in the Japan Times summarizing an IMF report on the insufficiency of the financial system restructuring to date.

-

Coalition Finalized Bill Adding to RCC’s Powers to Clear Loans.

An article in the Japan Times describing legal progress in expanding the RCC’s abilities.

-

Coalition to Study Book-Value Buys by RCC.

An article in the Japan Times describing the proposal to allow the RCC to buy assets at book value.

-

Debt Collector Handed License to Speed Up Bad-Loan Disposal.

An article in the Japan Times outlining the RCC’s additional legal authority.

-

Debt Collector Starts Operation.

An article in the Japan Times announcing the RCC’s operational launch.

-

Gangsters Aggravating Japanese Banking Crisis.

An article in the Washington Post describing the impact of organized crime on the bad loan and banking problems.

-

HLAC, RCB merger Creates New Collection Agency.

An article in the Japan Times announcing the merger of the RCB and HLAC into the RCC.

-

Japan Mob Muddies Real Estate Loan Crisis.

An article in the Los Angeles Times that describes the influence of organized crime on the NPL problem, specifically the real estate loan crisis.

-

‘Jusen’ Loan-Recovery Body Established.

An article in the Japan Times announcing the establishment of the HLAC and its objective to resolve and manage debt from the ‘jusen’ companies.

-

Pile of Bad, Yakuza-Tied Debts Awaits New President of RCC.

An article from the Japan Times describing the challenges facing the RCC upon its launch.

-

RCC Chief Airs Concern over ‘Secondary Losses’.

An article in the Japan Times describing concerns about losses on assets and pricing.

-

RCC Plans Bad Loan Buys from June.

An article describing the RCC’s expected launch.

-

RCC Should Buy Bad Loans at Book Value: Yamasaki.

An article describing an argument that the RCC should be able to buy assets at book value.

-

RCC to Buy Risky Loans.

An article announcing the RCC’s launch and purchase of bad loans.

-

RCC’s Revamp Offers Hope against NPLs.

An article in the Japan Times describing the RCC’s new legal authority and activities and the expectations around its expanded capabilities.

-

The Yakuza: Bad Debts, Bad Men.

An article in Bloomberg outlining the challenges posed by organized crime in resolving bad debt in Japan.

-

Industrial Revitalization in Japan: The Role of the Government vs the Market.

A paper describing the IRJC’s operations and its impact on corporate restructuring in Japan.

-

Japan: Regulatory Development of the Banking Resolution Regime.

An overview of the evolution of Japan’s bank and financial system restructuring authority.

-

Japan’s Disposal of Bad Loans: Failure or Success?

An analysis of Japan’s response to the financial crisis and NPL problem.

-

Japan’s Financial Problems.

A paper describing the origin and escalation of financial sector problems in Japan.

-

Lessons from Japan’s Banking Crisis, 1991–2005.

An academic paper outlining key lessons learned from the Japanese response to the financial crisis of the 1990s.

-

Public Asset Management Companies in East Asia: A Comparative Study.

An analysis and comparison of multiple AMCs established in the wake of the Asian Financial Crisis.

-

Solutions to the Japanese Banking Crisis: What Might Work and What Definitely Will Fail.

An analysis of the banking crisis in Japan that evaluates resolution options and their viability.

-

The Disposal of Bad Loans in Japan: A Review of Recent Policy Initiatives.

A paper describing the response to the financial crisis as of 1994.

-

The Disposal of Bad Loans in Japan: The Case of the CCPC.

A book chapter describing the response to the NPL problem in Japan, specifically, the operations and outcomes of the CCPC, a semipublic agency.

-

The Financial Crisis in Japan during the 1990s: How the Bank of Japan Responded and the Lessons Learnt.

A paper describing the BOJ’s response to the financial crisis of the 1990s and key lessons learned from the response.

-

The Global Financial Crisis: Lessons from Japan’s Lost Decade of the 1990s.

A paper drawing lessons from the Japanese financial crisis in the 1990s to apply to the US response to the Global Financial Crisis.

-

The Japanese Banking Crisis of the 1990s - Sources and Lessons.

A paper outlining the origin and lessons from the 1990s banking crisis in Japan.

-

The Japanese Banking Crisis: Where Did It Come from and How Will It End?

An academic paper on the Japanese financial crisis that describes its origins.

-

The Japanese Economy and the Way Forward.

A book describing the Japanese economy, the crisis response, and the economic prospects.

-

The Japanese Economy: What We Know, Think We Know, and Don’t Know.

A paper analyzing the Japanese economy over the preceding decade during the financial crisis and the prolonged recovery.

-

The Resolution and Collection Corporation and the Market for Distressed Debt in Japan.

A book chapter that describes the RCC and its operations.

-

Will the U.S. Bank Recapitalization Succeed? Eight Lessons from Japan.

An analysis of the Japanese financial crisis response and lessons that could be applied to the US response to the Global Financial Crisis.

-

Zombie Lending and Depressed Restructuring in Japan.

An academic paper on bank lending to zombie firms and its impact on economic recovery.

-

Annual Report 1998.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 1999.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2000.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2001.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2002.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2003.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2004.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2007/2008.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report 2012/2013.

The annual report from the DICJ, which outlines its activities related to financial system restructuring and the RCC’s activities.

-

Annual Report on Japan’s Economy and Public Finance 2000-2001.

The annual report from the Cabinet Office of Japan on the economy, government spending, and public debt.

-

Financial System Report.

A report from the Bank of Japan on the stability of the financial system in 2006.

-

Fiscal Year 2018 Overview of the RCC’s Activities.

The RCC’s annual report from 2018 outlining its operations and finances.

-

Japan: Article IV Consultation.

An IMF report on the financial and macroeconomic context in Japan including policy recommendations and evaluations.

-

Japan: Financial System Stability Assessment and Supplementary Information.

An IMF report on the financial system in Japan including policy recommendations and evaluations.

Taxonomy

Intervention Categories:

- Broad-Based Asset Management Programs

Countries and Regions:

- Japan

Crises:

- Japanese Crisis 1990s