Resolution and Restructuring - Fannie & Freddie

The Rescue of Fannie Mae and Freddie Mac – Module A: The Conservatorships

Purpose

To prevent the housing GSEs from becoming insolvent and to allow these GSEs to continue to maintain the secondary mortgage market, supporting US mortgage lending.

Key Terms

-

Announcement DateSeptember 7, 2008

-

Operational DateSeptember 6, 2008

-

Expiration DateIndefinite/None announced

-

Return to ProfitabilityFY2012

-

Legal AuthorityHERA §1117

-

FunderUS Department of the Treasury

-

ConservatorThe Federal Housing Finance Agency (FHFA)

-

Total Investment$191.5 billion

Two government-sponsored enterprises (GSEs), the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac), dominated the secondary mortgage market during the US housing crisis, collectively holding or guaranteeing $5.3 trillion in mortgage assets by late 2007. As the crisis escalated, the two GSEs began to report substantial losses and their survival became uncertain. On September 6, 2008, the GSEs’ new regulator, the Federal Housing Finance Agency (FHFA), placed the firms into indefinite conservatorships, one step of a four-part government intervention to stabilize the enterprises. This case study evaluates the purpose and efficacy of the conservatorships and finds that they accomplished their emergency goals of stabilizing the GSEs and allowing them to maintain the secondary mortgage market. However, the FHFA Office of Inspector General concluded that the agency could better accomplish its oversight mission by proactively exerting greater control over its conservator approval process. As of this case study’s publication, the conservatorship for both companies is ongoing.

Concurrent with the US housing market’s collapse, the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac) began to post substantial losses in the last two quarters of 2007. These two government-sponsored enterprises (GSEs), which were thought to be backed by an implicit government guarantee, had $5.3 trillion of guaranteed mortgage-backed securities (MBS) and debt outstanding as of December 2007. Given their size and importance in the secondary mortgage market, the potential insolvency of either GSE threatened to destabilize the entire housing market and the financial system.

Recognizing that Fannie Mae and Freddie Mac might not be able to stabilize on their own, financial officials called for legislation to create a new regulator that could marshal taxpayer funds to rescue the GSEs. On July 30, 2008, the government passed the Housing and Economic Recovery Act of 2008 (HERA), which created a new GSE regulator, the Federal Housing Finance Agency (FHFA), and provided Treasury with emergency powers to provide funding to rescue the GSEs, should they need it. Confronted with further deterioration of the two GSEs, the FHFA placed them into indefinite conservatorships on September 6, 2008, as part of a four-part rescue plan to stabilize the GSEs.

As conservator, the FHFA immediately suspended dividends on all outstanding stock, replaced both GSEs’ CEOs and boards, and then managed the firms indirectly, promising to preserve their precrisis business operations as much as possible. The Treasury funded the firms in conservatorship pursuant to Senior Preferred Stock Purchase Agreements(SPSPAs), ultimately investing a combined $191.5 billion between 2008 and 2017. While both GSEs remained solvent and continued to maintain a secondary mortgage market throughout the crisis, they reported annual losses until 2012. In February 2012, the FHFA submitted a new plan for conservatorship, which focused more on preparing the GSEs and the secondary mortgage market for operations after conservatorship. As of this case study’s publication, however, no plan to end the conservatorships has progressed beyond the drafting phase.

Most scholars and evaluators agree that the conservatorships successfully accomplished short-term emergency goals because Fannie Mae and Freddie Mac remained solvent. The interventions also allowed the GSEs to continue purchasing loans and issuing and guaranteeing MBS to the secondary mortgage market when private-label securitization dried up during the crisis. However, the conservatorships have been criticized for poor oversight and for at times prioritizing the GSEs’ financial health over the government’s broader crisis-fighting goals.

Key Design Decisions

Legal Authority

1

The government passed HERA in July 2008 to provide enhanced resolution alternatives to the GSEs’ regulator in light of the severely weakened condition of the firms, their critical role in the stability of the mortgage and housing markets, and the stresses then impacting those markets (among other things) (Frame et al. 2015, 14). Prior to HERA, OFHEO (Office of Federal Housing Enterprise Oversight, former GSE regulator) could have taken the firms into conservatorship, but there existed no viable funding to support such a move, largely rendering the authority ineffective (Frame et al. 2015, 5). Also, the GSEs were exempt from the US bankruptcy code, and there was no authority for OFHEO to place them in receivership (Frame et al. 2015, 18–21). HERA created a new regulator, the FHFA, and provided mechanisms for Treasury to fund the firms during an emergency period, ensuring their solvency during a conservatorship (Frame et al. 2015, 18–21). HERA also provided the FHFA expanded authority to place the firms into receivership if necessary (Frame et al. 2015, 18–21). (See Thompson and Kulam (2021) for more information regarding HERA.)

Other Options

1

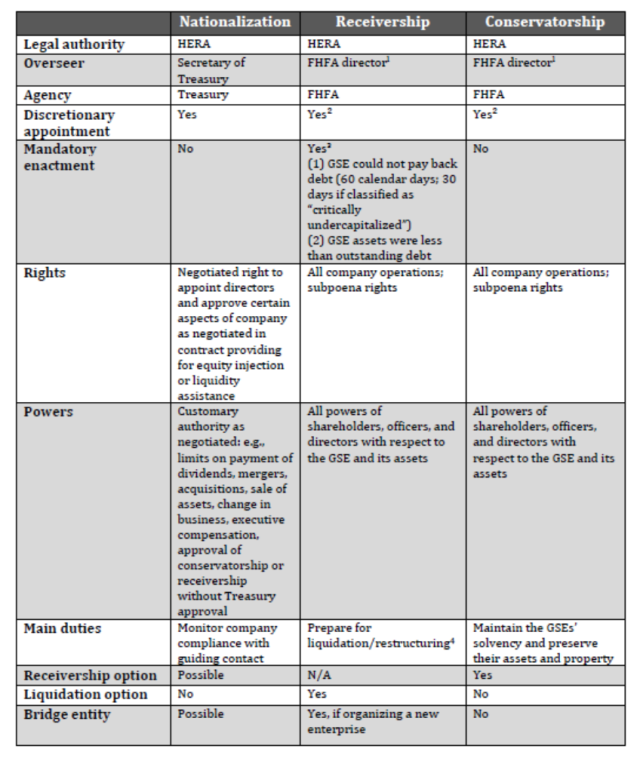

W. Scott Frame et al. (2015) dismiss the claim that Treasury could have stabilized the GSEs by simply buying their debt or MBS without a formal apparatus (21). Noting the amount of capital required to stabilize the GSEs, Frame et al. argue that the Treasury needed a mechanism to ensure that it could continuously fund the GSEs in the needed amounts (which were unknown at the time, but estimates of which were in the tens of billions) (Frame et al. 2015, 21). As such, Treasury required a government intervention to establish and operate such a mechanism (Frame et al. 2015, 19). Operating with the common understanding that the government needed to save the GSEs, Frame et al. identify three options that government officials could have taken.

Nationalization. The first option was nationalization, which Frame et al. (2015) define as purchasing and controlling at least an 80% equity stake in each company (21). The government considered this option the least favorable because the government would have been compelled to assume all liability for Fannie Mae and Freddie Mac and to consolidate their operations onto its balance sheet (Frame et al. 2015, 21).

However, the definition of the term “nationalization” is fluid, unlike the definitions of “conservatorship” and “receivership” (which are discussed later) (Elliott 2009, 7). For the purposes of this paper, “nationalization” refers to the government gaining a controlling interest in a company (one that might be greater than 50% but less than 80%) such that it is empowered to make or influence critical decisions about how the company operates. Nationalization can be accomplished in a variety of ways but does not denote application of a specific, prescribed administrative process, such as conservatorship or receivership, or the FDIC bank resolution process, although such processes may be employed (Elliott 2009, 13–15).

In light of this working definition, the government could have nationalized the GSEs by making—via Treasury—a substantial financial contribution and gaining via contractual agreement (such as a stock purchase agreement, memorandum of understanding, or shareholders’ agreement) certain constraints on the GSEs operations (Lockhart 2018, 12). (Also see Appendix B.) However, taking control of the GSEs without the benefit of a known and predictable framework could have created operational and legal messes (Jester et al. 2018, 7). Treasury’s ability to operate the companies would still have been subject to management’s compliance with the operative contract and complicated by the need to comply with various regulations regarding preservation of the GSE charters (Lockhart 2018, 12). Treasury Secretary Paulson was of the opinion that such an arrangement would not adequately protect the taxpayers and, thus, would not agree to contribute capital to the GSEs without their being in a conservatorship or receivership (Jester et al. 2018; Lockhart 2018, 12).

Receivership. After the passage of HERA, receivership was a second viable option available to the government (Frame et al. 2015, 18). The intent of a receivership is to wind down an organization rather than merely stabilize it and have it continue operations (Jester et al. 2018, 7). Under HERA, invoking a receivership would mean the application of timelines and the need for a bridge entity since the GSEs could be dissolved only by an act of Congress (Frame et al. 2015, 18–19). Additionally, the FHFA would be compelled to reform the firms as they were released from receivership, which would have been required in five years (Frame et al. 2015, 20). However, the structure of the GSEs had been debated for years, and Congress had yet to resolve those concerns (Frame et al. 2015, 20).

Dan Jester served in Paulson’s Treasury during the rescue and, with other Treasury officials, questioned the feasibility of setting up the receiverships in time to be effective (Jester et al. 2018, 7). They doubted the GSEs would acquiesce to such a forceful intervention and worried the firms would respond by filing lawsuits and drumming up congressional opposition to it (Jester et al. 2018, 7). Secretary Paulson also worried that receiverships might also “spook the markets” and might put some debtholders at risk, increasing instability of some banks and other financial institutions (Lockhart 2018, 12). Moreover, even if the receiverships were put in place, Jester et al. expressed doubt that the FHFA—a new agency with “no institutional experience managing a receivership”—was up to the task of overseeing the successful implementation of one (Jester et al. 2018, 7).

Conservatorship. The final option was conservatorship. Although a conservatorship could last indefinitely, it was seen as a temporary measure that would allow the government to take control of the companies and stabilize them for continued operation, while Congress considered how to address the more contentious structural aspects of the GSEs’ special status (Frame et al. 2015, 20; Jester et al. 2018, 7). Conservatorship also was seen as an option that could be implemented swiftly, which was important given the rising number of concerns at other major financial institutions that were debtholders (Frame et al. 2015, 20; Jester et al. 2018, 7–8).

Most importantly, however, conservatorship allowed the GSEs to continue their operations and supply the secondary mortgage market, something critically needed as the private market severely contracted (Frame et al. 2015, 26–27; Jester et al. 2018, 7). The efficacy of this option hinged on the Treasury’s ability to finance the conservatorship, which was made possible by HERA (Frame et al. 2015, 19). Frame et al. (2015) note that if the Treasury could not have financed the conservatorship, then receivership would have been the best option (20). HERA also included a clause that allowed the FHFA to later place the GSEs into receivership from conservatorship (Frame et al. 2015, 21). However, James Lockhart, then director of the FHFA, stated that this was something that his agency never seriously considered (Lockhart 2018, 8–10). See Appendix B for a comparison of the attributes of the three possible solutions and see Wiggins et al. (2021) for further discussion of the conservatorship decision.

Communication

2

Secretary Paulson identifies secrecy, speed, and timing as the three aspects in the execution of Fannie Mae and Freddie Mac’s conservatorship that avoided a protracted battle with the GSEs, news leaks to the public, and a major market swing (Paulson 2010, chap. 1). After keeping the conservatorship discussion (and later the conservatorship decision) a secret for several weeks, Paulson, FHFA Director Lockhart, and Fed Chairman Ben Bernanke presented the option to Fannie Mae and Freddie Mac’s CEOs with no warning (Paulson 2010, chap. 1). These officials knew that the CEOs might fight to keep their positions and thus gave them no time to publicize the conservatorship or solicit assistance from their political contacts on Capitol Hill (Paulson 2010, 75–76). Paulson feared that if either CEO decided to resist the conservatorship, they could delay its implementation and instigate panic in the markets (Paulson 2010, 75–76).

Federal officials also met with Fannie Mae’s CEO and executive board first, since they anticipated that Fannie Mae’s team would be more resistant to the idea (Paulson 2010, 83–84). Federal officials took caution to avoid any press coverage of the event and selected the FHFA’s office as the location for their private meetings with Fannie Mae and Freddie Mac (Paulson 2010, 83–84). They arranged for the first meeting with Fannie Mae to start at 4:00pm on Friday, September 5 so that the markets would have closed before the meeting had finished (Paulson 2010, 83–84). After each meeting, they informed members of the House Financial Services Committee and Senate Banking Committee, so that they would not be surprised when the news broke to the public (Paulson 2010, 87–93). Lockhart and Paulson announced the conservatorships as part of a four-part rescue plan for the GSEs on Sunday, giving the public an opportunity to react before markets reopened on Monday (Paulson 2010, 95–98).

The FHFA has used plans, reports, and scorecards to disseminate information and increase public transparency regarding the conservatorships. On December 15, 2008, the FHFA released its first annual performance plan, for fiscal year 2009. The plan outlined the FHFA’s objectives for the GSEs and detailed how it would use its resources to achieve those objectives (FHFA 2008e). Beginning in 2010, the FHFA also released a quarterly Conservator’s Report on the Enterprises’ Financial Performance, which summarized the fiscal health of both enterprises under conservatorship; the report lasted through the first quarter of 2013 (FHFA 2013). In 2012, the FHFA began to release an annual scorecard, which was designed to make the FHFA’s duties and objectives more transparent for the public (FHFA 2012b; FHFA 2021). The FHFA also continued the practice of publishing the GSEs’ annual examination results within the annual reports to Congress.

Through its regular reports, the FHFA identified at least two reasons for governing the GSEs transparently: (1) to increase public confidence in the GSEs and foster secondary mortgage market activity, and (2) to inform taxpayers FHFA’s efforts to prevent foreclosure (FHFA 2008d, 137–46; FHFA 2009b, 61–62). In addition, DeMarco, who replaced Lockhart in 2009 as FHFA acting director, acknowledged that taxpayer funds kept Fannie Mae and Freddie Mac in operation (DeMarco 2010, 3). For this reason, DeMarco pledged to outline how the FHFA had limited, and would continue to limit, GSE losses (DeMarco 2010). Additionally, as the GSEs by their size were systemic in nature, many investors around the world were paying attention to developments with respect to the conservatorships (Paulson 2010, 77–78).

Administration

6

When the FHFA placed Fannie Mae and Freddie Mac into conservatorship, it also replaced the firms’ CEOs and appointed new nonexecutive chairmen of the boards (FHFA 2008b). Secretary Paulson expressed the gravity of the intervention to justify firing the GSEs’ CEOs (Paulson 2010, 93–94). When asked for his rationale to fire Fannie Mae’s CEO, he replied, “I don’t think that you could do something this drastic and not change the CEO” (Paulson 2010, 93–94). FHFA director Lockhart justified removing the GSE boards with similar logic and noted, “Although it is not necessary in a conservatorship, new boards are being formed as a matter of good governance” (Lockhart 2008).

As conservator, the FHFA ascended to all authority of the boards and management but eventually delegated some of that authority back to the new board and management while retaining a right of review (DeMarco 2010, 3–4). Even under conservatorship, in exercising their authority, the GSE officers remained “subject to the legal responsibility to use sound and prudent business judgment in their stewardship of their companies” (DeMarco 2010, 3).

The FHFA adopted this approach to save money, to increase public confidence in the two GSEs, and most importantly, to keep the GSEs operating. After enacting the conservatorship, the FHFA froze the GSEs’ dividend payments and shareholder voting rights (except for Treasury’s senior preferred stock) (Fannie Mae 2008b, 21). The FHFA estimated that freezing dividends would save the GSEs about $2 billion in reserve capital annually (FHFA 2008b). The GSE stock remains outstanding, but there is no guarantee that it will be restored to its full rights when the firms exit the conservatorships (Fannie Mae 2008b, 50; FHFA 2008c, 3).

Given Treasury’s funding commitment to guarantee GSE solvency (up to the stated limits), the GSE bondholders were protected (Jester et al. 2018, 8–9). Federal officials recognized that protecting bondholders was critical to minimize immediate risks to the financial system, to protect future investors in debt and MBS, and to quiet any concerns about the government’s credibility (Lockhart 2009; Paulson 2010; UST 2008). On the day after Fannie and Freddie entered conservatorship, FHFA announced that conservatorship did not change the legitimacy of current and future financial contracts (FHFA 2008a; Lockhart 2008). Important factors supporting the government’s decision to protect all holders of debt and MBS included: (1) the sheer size of the GSEs’ liabilities, (2) the nature of the bondholders, and (3) the GSEs’ close alignment with the government (Jester et al. 2018, 8–9; UST 2008).

GSE debt and obligations benefited from an “implied government guarantee,” which helped them enjoy a robust market with their debt being widely held (Frame et al. 2015, 1). Much of this debt was held by foreign central banks and foreign and domestic financial institutions that believed that GSEs’ securities were effectively risk-free (UST 2008). Secretary Paulson felt that allowing the international debtholders to suffer losses could undermine foreign investors’ confidence in the United States’ creditworthiness, which could cause a run on the dollar or a Treasury sell-off (CBO 2010, 22; Paulson 2010, 77–78). Also, many domestic banks, which were already under stress, held GSE debt due to favorable capital rules (Rice and Rose 2016, 7–9).

The government’s actions, in essence, made the implied guarantee firm, which seems to have increased confidence in the GSEs, which Lockhart (2008) and Frame et al. (2015, 22) argue is evidenced in falling yields—at least before Lehman Brothers collapsed. (See also Wiggins et al. [2021] for further discussion of these points.)

To manage the conservatorships, the FHFA established a new infrastructureFThe FHFA described efforts to enhance its governance practices through various white papers and annual reports (FHFA-OIG 2015, 13). consisting of the Office of Conservatorship Operations and the Conservatorship Governance Committee (FHFA-OIG 2012a, 20–21). The OCO acted as the liaison and administrator between the GSEs and the FHFA, relying on FHFA resources to resolve issues (FHFA-OIG 2012a, 20–21). The CGC was composed of senior FHFA executives whose goal was to “ensure coordination on regulatory or supervisory matters that might need to be brought to the attention of the conservator” (FHFA-OIG 2012a, 21).

Because the OCO employed only six people, the OCO also relied on the regulatory resources throughout the FHFA to evaluate the GSEs’ success in achieving these goals and address conservator issues (FHFA-OIG 2012a, 21; FHFA-OIG 2012b, 22–23). One audit report highlights the possible tensions that may arise from FHFA’s status as both conservator and supervisor: “For example, FHFA could potentially be faced with criticizing its own actions or those of its senior officials” (FHFA-OIG 2012a, 30). The Office of Inspector General also noted that the conflict was partly addressed by the delegation of most management decisions to the enterprises’ boards and managers (FHFA-OIG 2012a, 30).

The FHFA defended its original structure and claimed that the unknown duration of conservatorship prevented the agency from making long-term investments in its own infrastructure (FHFA-OIG 2012a, 31–32).

Nevertheless, the FHFA agreed with most of the OIG recommendations and took steps to implement them (FHFA-OIG 2012b, 31–37). As it became more apparent that the GSEs would not soon exit the conservatorship, the FHFA refined its strategic plans and evaluation mechanisms by developing a reporting scorecard; establishing an approval tracking and resolution process; and in 2013, consolidating all conservator functions into a Division of Conservatorship, which employed 25 people as compared to the previous six-person OCO (FHFA-OIG 2012b, 9–11; FHFA-OIG 2015, 11, 14).

The FHFA’s inspector general (IG) noted that a conservator generally can take one of three approaches: “Actively managing every aspect of an entity’s operations; Monitoring the conserved entities’ decision-making and stepping in when it feels it is appropriate; or deferring to the conserved entity on most decisions and stepping in only in cases of greater significance” (FHFA-OIG 2012a, 22). The IG noted that FHFA had taken the third approach.

FHFA has determined to (1) delegate authority for general corporate governance and day-to-day matters to the Enterprises’ boards of directors and executive management, and (2) retain authority for certain significant decisions. (FHFA-OIG 2015, 11–12)

Within three months of establishing the conservatorships, the FHFA had delegated significant authority to the new boards of directors and CEOs (FHFA-OIG 2012a, 22, 30). It did this as an efficient way to run the massive businesses consistent with the tenets of the conservatorship—to manage the firms as going concerns, stabilize them financially, and return them to independent operation (FHFA-OIG 2012a, 23). However, it’s important to note that the FHFA retained authority over a group of key business decisions, for which it required the GSEs to seek prior approval (FHFA-OIG 2012a, 19–20). These powers were referred to as nondelegated authorities (FHFA-OIG 2012b, 6). Among other things, these included capital actions, compensation policies, and other large transactions, including legal settlements, merger activities, and deals with subsidiaries (FHFA-OIG 2012a, 19–20). (See Figure 2 for a summary of the nondelegated authorities.) In addition to specified nondelegated authorities, the FHFA retained the right to review (and to overturn) any other business decision it deemed important along the way (DeMarco 2010, 3–4).

The FHFA cited three reasons in defense of its style of conservatorship: efficiency, concordant goals, and operational savings (FHFA-OIG 2012a, 23–24). The GSE employees knew the business and were well equipped to continue to carry out normal business operations (FHFA-OIG 2012a, 23). The goals of the enterprises were consistent with those of the conservatorships, i.e., return the firms to stability: “FHFA views part of its ‘preserve and conserve’ mandate to include preserving the entities as private companies with the capacity and responsibility to make business decisions following normal corporate governance procedures” (FHFA-OIG 2012b, 31). Acting Director Edward J. DeMarco suggested that delegating authority to GSEs created operational savings because FHFA avoided duplicating work that the GSEs were already doing (FHFA-OIG 2012a, 23–24).

Instead, the FHFA communicated with the GSE employees about the conservatorship and tried to maximize retention (FHFA-OIG 2012a, 13). The OCO and the CGC worked to ensure that the firms were operating in a manner consistent with their delegations of authority, the stated conservator goals, and the overall objectives of the conservatorship (FHFA-OIG 2012a, 20–21).

However, the OIG found that the agency’s practices were flawed:

FHFA-OIG’s reports consistently have revealed two trends: (1) the Agency, in its role as a conservator, does not independently test and validate Enterprise decision-making; and (2) the Agency, in its role as a regulator, is not proactive in its oversight and enforcement. In addition, FHFA may not have enough examiners to meet its oversight responsibilities. (FHFA-OIG 2012a, 2)

As a result of these procedures, the OIG criticized FHFA for not overseeing several major decisions that the GSEs made (FHFA-OIG 2012b, 12–13). These included changes to Fannie’s single-family underwriting standards and the High Touch Servicing Program, whereby Fannie Mae transferred $1.5 billion in mortgage servicing rights to third-party specialty servicers (FHFA-OIG 2012b, 12–13). The inspector general also found that the agency often failed to question decisions that were submitted to it for approval and relied too often on management’s decision without an independent proof or business case (FHFA-OIG 2012b, 20–22).

Additionally, the OIG concluded that the agency could better accomplish its oversight mission by proactively exerting greater control over its conservator approval process:

Specifically, FHFA-OIG recommends that the Agency: (1) revisit FHFA’s non-delegated authorities to ensure that significant Enterprise business decisions are sent to the conservator for approval; (2) guide the Enterprises to establish processes to ensure that actions requiring conservator approval are properly submitted for consideration; (3) properly analyze, document, and support conservator decisions; and (4) confirm compliance by the Enterprises with conservator decisions. FHFA agreed with most of FHFA-OIG’s recommendations.” (FHFA-OIG 2012b, sec. “At a Glance”)

The GSE intervention was designed to keep the firms in operation so that they could “continue to fulfill their mission of providing stability, liquidity, and affordability to the [mortgage] market” (FHFA 2009a, ii). As a result, under the conservatorship, the FHFA directed the GSEs to continue their key business operations and MBS securitizations and placed no restrictions on the amount of MBS they could issue or guarantee (FHFA 2008d, 92). Under the SPSPAs, they also were allowed to expand their portfolios for a short time—up to a limit of $850 billion—before having to start reducing them in 2010 (UST/Fannie Mae 2008, 9). The GSEs’ ability to continue operations was especially critical early in the conservatorship; when private-label securitization shrank during the global credit crisis, the GSEs assumed a still larger role in the housing market and purchased a greater proportion of new mortgages (OFHEO 2008, 9–17).

The GSEs’ housing mission was also targeted to assist with the government’s wider foreclosure prevention efforts. At the end of 2008, FHFA reported the GSEs were “playing an important role in assisting the federal government in foreclosure mitigation activities” (FHFA 2009a, 4). Less than one year after the conservatorship began, the GSEs started to participate in the Home Affordable Refinance Program (HARP) and Home Affordable Modification Program (HAMP) (FHFA 2010b, 7–8). HARP and HAMP were intended to serve the dual goals of limiting GSE credit losses and alleviating wider mortgage market stress, both of which were important for the GSEs’ long-term stability (DeMarco 2010, 5; FHFA 2009a, 85–87; FHFA 2010b, 7–8).

During the mortgage crisis, the government continued to prioritize affordable housing goals and relied on Fannie Mae, Freddie Mac, and the Federal Home Loan Banks to meet them (CBO 2010, vii; Lockhart 2009). Through HERA, FHFA received the authority to enforce these goals (which had previously rested with the US Department of Housing and Urban Development) but mandated a change in the way they were structured beginning in 2010 (FHFA 2010b, 3–4). Within the first year of the conservatorship, the FHFA adjusted its affordable housing goals to account for prevailing market conditions (Lockhart 2009). By the end of 2010, a new structure was in place, and the GSEs were required to meet four core single-family goals, one multifamily “special affordable” goal, and two related subgoals, on an annual basis (FHFA 2011, 97).

Through HERA, the FHFA had the power to review any decision affecting executive compensation and could amend GSE compensation practices as it saw fitFThese broad authorities over executive compensation were granted as part of the arrangement enabling Treasury to purchase GSE obligations. Like Treasury’s purchasing authority, these powers were temporary and set to expire December 31, 2009. However, on a permanent basis, HERA gave the FHFA other powers over executive compensation, including the authority to withhold executive compensation and prohibit severance payments. For more information, see Sections 1113, 1114, and 1117 of HERA (Public Law 110-289). (FHFA 2009a, 84).

During the conservatorship, acting FHFA Acting Director DeMarco (who replaced Lockhart in September 2009) identified enabling the GSEs to retain and recruit talented executives as key to fulfilling his agency’s mission as conservator (DeMarco 2011). Without competent executives, the two firms were at high risk of running into trouble yet again—an operational risk that could result in more losses and potentially add billions of dollars to the steep price taxpayers already had paid (DeMarco 2011).

Early in the conservatorship, the GSEs endured “key person risk” to their human resources (FHFA 2010b, 17–18, 41). FHFA officials argued that potential downsizing, possible dechartering, and general public scrutiny could have motivated executives to leave (FHFA 2010b, 17–18, 41). To offset its key person risk, the FHFA set out to adjust executive compensation policies to give talented executives more of an incentive to stay (FHFA 2010b, 17–18, 41).

After consulting with Treasury (including the Special Master for TARP Executive Compensation) and the boards of both firms, and retaining a private consulting firm (Hays Group) to serve as advisor, the FHFA instituted a three-pronged executive compensation policy at both firms (DeMarco 2011). FHFA designed the new system to both motivate high-performing executives to stay and curb the GSEs’ pre-conservatorship excesses (DeMarco 2011). For example: FHFA prohibited the golden parachutes that were formerly promised to outgoing CEOs and other senior executives (DeMarco 2011). Although prior executive compensation policies included company stock, FHFA pivoted to a cash-only compensation scheme because regulators sought to prevent executives from taking excess risks to raise the low prices of their company shares (DeMarco 2011).

The new system provided for three components of executive compensation—(1) base salary, (2) deferred salary, and (3) performance-based incentives—and was modeled after policies put in place at “institutions receiving exceptional TARP assistance” (DeMarco 2011). Important aspects of these components are highlighted below:

- Except for a few top executives, maximum base salaries was set at $500,00—less than half of what they were prior to conservatorship.

- Performance-based compensation was determined using only two years of results given the lack of a clear long-term plan for the firms.

- Deferred salary was paid out a year after the base portion and was to be forfeited by officials choosing to leave before the year’s deferred payments were due.

- Deferred payments made up the largest portion of top executives’ total compensation packages. (DeMarco 2011)

In March 2011, the FHFA-OIG published a report analyzing the executive compensation policies put in place at both entities and criticized the FHFA for its lack of formal enforcement of the new policies (FHFA-OIG 2011, sec. “At a Glance”). The report advised the FHFA to: (1) make information on GSE executive compensation more accessible to the public (and “more user-friendly”) and (2) develop formal control mechanisms to better enforce the entities’ compliance with the new policies (FHFA-OIG 2011, 20–22).

FHFA balanced the need to attract and retain qualified leadership with mandatory restrictions on executive compensation, which was a challenge for both the firms and their conservator. In 2019, audits by the FHFA-OIG found that FHFA’s approval of senior executive succession planning at both firms had “acted to circumvent the congressionally mandated cap on CEO compensation” (FHFA-OIG 2019a, 1–4; FHFA-OIG 2019b, 1–5).FSee FHFA-OIG 2019a for the latest report on Fannie Mae and FHFA-OIG 2019b for the latest report on Freddie Mac. The firms disagreed with the auditor’s conclusions (FHFA-OIG 2019a, 1–4; FHFA-OIG 2019b, 1–5).

W. Scott Frame et al. (2015) argue that the conservatorships succeeded as emergency interventions successfully stabilizing the GSEs (30). First, the intervention prevented agency debtholders and MBS holders from experiencing losses at a time when such institutions were already being challenged to navigate the worsening crisis, shielding the vast number of counterparties from negative impacts and containing the GSEs’ weaknesses from bringing down the entire financial system (Frame et al. 2015, 26–27). In addition, a 2010 Congressional Budget Office (CBO) report claimed that, in general, replacing an implicit government guarantee with an explicit guarantee, as was done in the intervention, was likely to improve the liquidity of the GSEs’ MBS by ensuring a more robust market by attracting a broader and more stable group of investors (CBO 2010, 17). However, the report also cautions that other countervailing factors must also be considered to gauge the true effect (CBO 2010, 17).

Second, the program allowed the GSEs to continue purchasing loans and issuing and guaranteeing MBS, which maintained the flow of funding and helped to stabilize the mortgage market (Frame et al. 2015).

Frame et al. (2015) note that the FHFA’s focus on the financial health of the GSEs may have limited the overall mortgage supply; as the FHFA urged Fannie Mae and Freddie Mac to return defaulted mortgages to their originators or sellers, originators tightened underwriting standards (27–28). While stringent underwriting standards helped to reduce the GSEs’ losses, they also shrank the supply of mortgage credit, which, Frame et al. (2015) argue, contributed to the market’s slow recovery (27–28). In contrast, the Mortgage Bankers Association (MBA) contends that the FHFA’s decision to abolish preferential underwriting standards facilitated small lenders’ higher postcrisis market share of mortgage origination and refinancing (MBA 2017, 6). In addition, Winston Sale argues that the FHFA cut the GSEs’ affordable housing goals to stabilize the market during the crisis (Sale 2009, 300–07).

Some scholars find that FHFA actions have weakened other sectors of the economy. Tara Rice and Johnathan Rose contend that the conservatorship weakened the balance sheets of banks exposed to GSE preferred shares (2016, 86). They argue that the FHFA’s decision to suspend dividends on preferred shareholders harmed already struggling banks, particularly community banks, which held large quantities of GSE stock (Rice and Rose 2016, 86). Fifteen banks closed because of this decision, the authors suggest, and two more were forced to sell themselves (Rice and Rose 2016, 86).

From a governance and operational standpoint, several audits by the FHFA’s Office of Inspector General found that the FHFA “can better accomplish its oversight mission by proactively exerting greater control over its conservator approval process” (FHFA-OIG 2012b, sec. “At a Glance”). OIG also found that FHFA did not properly monitor several components of GSE operations, which resulted in both companies taking inappropriate financial risks (FHFA-OIG 2012b, sec. “At a Glance”). For example, a 2015 audit noted that the FHFA lacked a formal review process for the GSEs’ compensatory fee settlements and large mortgaging service transfers (FHFA-OIG 2015, 15–16). The OIG also found that the FHFA did not have an apparatus to measure properly the GSEs’ performance levels or a system to monitor all company operations (FHFA-OIG 2015, 15–16). In 2014, for instance, the FHFA did not detect that Fannie Mae and Freddie Mac had over-reimbursed their lender-based insurance servicers by approximately $159 million ($89 million for Fannie Mae and $70 million for Freddie Mac) (FHFA-OIG 2015, 16).

Other factors cited by the OIG and the FHFA that have impacted the efficacy of the conservatorship:

- The unique size of the GSEs, which were factors larger than any other entity to have been previously resolved by the government;

- The unique nature of Fannie Mae and Freddie Mac as GSEs, which presented operational challenges and limited the conservator’s exit strategies;

- The fact that the FHFA was a newly established agency, which at the time of the conservatorship was forming itself;

- Significant turnover of GSE personnel, particularly at the management levels, despite retention efforts; and

- Tensions between the FHFA’s role as regulator and conservator. (FHFA-OIG 2012a, 26–33)

Scholars generally find that the conservatorship has been unsatisfactory with respect to the longer-term objective of resolving the GSEs’ structural issues and removing the enterprises from conservatorship (Frame et al. 2015, 27–30). Despite the government’s intention to use the conservatorship temporarily, they remain in effect more than 12 years later.

While the GSEs continue to operate under conservatorship, Congress has yet to resolve the longer-term questions of how to terminate the conservatorships or what would be a new form for the entities (Frame et al. 2015, 30). The FHFA cannot discharge the GSEs from conservatorship without Treasury’s approval, and all parties seem to agree that releasing the GSEs from the conservatorship in their current form, with their quasi-public/private hybridity and implicit government guarantee intact, would not be ideal (FHFA-OIG 2012a, 31–32). It is unlikely that the conservatorships will end until Congress agrees on what form the entities should have upon release from the FHFA’s control (FHFA-OIG 2015, 6).

Despite these views, Jester et al. are of the opinion that enacting the conservatorships without developing a plan to exit them was entirely appropriate at the time, as the Treasury was focused on stemming the crisis rather than solving the broader policy issues that had helped to instigate the GSEs’ demise (Jester et al. 2018, 16–17).

- Board of Governors of the Federal Reserve System (BGFRS). 2008. “Discount Windo…

- Congressional Budget Office (CBO). 2010. “Fannie Mae, Freddie Mac, and the Fede…

- DeMarco, Edward J. 2010. “Letter to Congress,” February 2, 2010.

- ———. 2011. “Statement of Edward J. DeMarco before the U.S. House Committee on O…

- Elliott, Douglas J. 2009. “Bank Nationalization: What Is It? Should We Do It?” …

- Federal Home Loan Mortgage Corporation (Freddie Mac). 2008. “Monthly Volume Sum…

- ———. 2009. “Form 10-K.” US Securities and Exchange Commission. December 31, 200…

- ———. 2010. “Monthly Volume Summary: December 2010.” US Securities and Exchange …

- ———. 2012. “Monthly Volume Summary: December 2012.” US Securities and Exchange …

- ———. 2014. “Monthly Volume Summary: December 2014.” US Securities and Exchange …

- ———. 2016. “Monthly Volume Summary: December 2016.” US Securities and Exchange …

- Federal Housing Finance Agency (FHFA). n.d.-a. “Conservatorship.” Accessed Marc…

- ———. n.d.-b. “Residential Mortgage Debt Outstanding—Enterprise Share, 1990–2010…

- ———. 2008a. “Press Release: Statement of FHFA Regarding Contracts of Enterprise…

- ———. 2008b. “Statement of FHFA Director James B. Lockhart.” September 7, 2008.

- ———. 2008c. “Fact Sheet: Questions and Answers on Conservatorship.” September 9…

- ———. 2008d. “Performance and Accountability Report 2008.” November 17, 2008

- ———. 2008e. “FY 2009 Performance Plan.” December 15, 2008.

- ———. 2009a. “Report to Congress 2008, Revised.” May 18, 2009.

- ———. 2009b. “Performance and Accountability Report 2009.” November 16, 2009.

- ———. 2010a. “Market Data.” 2010.

- ———. 2010b. “Report to Congress 2009.” May 25, 2010.

- ———. 2011. “Report to Congress 2010.” June 13, 2011.

- ———. 2012a. “A Strategic Plan for Enterprise Conservatorships: The Next Chapter…

- ———. 2012b. “2012 Conservatorship Scorecard.” March 9, 2012.

- ———. 2012c. “Performance and Accountability Report 2012.” November 15, 2012.

- ———. 2013. “Conservator’s Report on the Enterprises’ Financial Performance.” Ab…

- ———. 2014. “The 2014 Strategic Plan for the Conservatorships of Fannie Mae and …

- ———. 2019. “Treasury and Federal Reserve Purchase Programs for GSE and Mortgage…

- ———. 2021. “Scorecard for Fannie Mae, Freddie Mac, and Common Securitization So…

- Federal Housing Finance Agency, Office of Inspector General (FHFA-OIG). 2011. “…

- ———. 2012a. “FHFA-OIG’s Current Assessment of FHFA’s Conservatorships of Fannie…

- ———. 2012b. “FHFA’s Conservator Approval Process for Fannie Mae and Freddie Mac…

- ———. 2015. “FHFA’s Conservatorships of Fannie Mae and Freddie Mac: A Long and C…

- ———. 2019a. “FHFA’s Approval of Senior Executive Succession Planning at Fannie …

- ———. 2019b. “FHFA’s Approval of Senior Executive Succession Planning at Freddie…

- Federal National Mortgage Association (Fannie Mae). 2008a. “Monthly Summary: De…

- ———. 2008b. “Form 10-K.” US Securities and Exchange Commission. December 31, 20…

- ———. 2009. “Form 10-K.” US Securities and Exchange Commission. December 31, 200…

- ———. 2010. “Monthly Summary: December 2010.” US Securities and Exchange Commiss…

- ———. 2012. “Monthly Summary: December 2012.” US Securities and Exchange Commiss…

- ———. 2014. “Monthly Summary: December 2014.” US Securities and Exchange Commiss…

- ———. 2016. “Monthly Summary: December 2016.” US Securities and Exchange Commiss…

- Federal Open Market Committee (FOMC). 2008. “Minutes of the Federal Open Market…

- Financial Crisis Inquiry Commission (FCIC). 2011a. “Chapter 3: Securitization a…

- ———. 2011b. “Chapter 7: The Mortgage Machine.” In The Financial Crisis Inquiry …

- ———. 2011c. “Chapter 17: The Takeover of Fannie Mae and Freddie Mac.” In The Fi…

- Frame, W. Scott, Andreas Fuster, Joseph Tracy, and James Vickery. 2015. “The Re…

- Harting, Bruce. 2008. “GSEs: Risks, Rewards, and Imperatives.” Lehman Brothers …

- Housing and Economic Recovery Act of 2008 (HERA 2008). 2008. Public Law 110-289…

- Jester, Dan, Matthew Kabaker, Jeremiah Norton, and Lee Sachs. 2018. “Rescuing t…

- Lockhart, James B., III. 2008. “The Appointment of FHFA as Conservator for Fann…

- ———. 2009. “Meeting the Challenges of the Financial Crisis.” Federal Housing Fi…

- ———. 2018. Yale Program on Financial Stability Lessons Learned Oral History Pro…

- Mortgage Bankers Association (MBA). 2017. “GSE Reform: Creating a Sustainable, …

- Office of Federal Housing Enterprise Oversight (OFHEO). 2008. “Report to Congre…

- Paulson, Henry M., Jr. 2010. On the Brink: Inside the Race to Stop the Collapse…

- Rice, Tara, and Jonathan Rose. 2016. “When Good Investments Go Bad: The Contrac…

- Sale, Winston. 2009. “Effect of the Conservatorship of Fannie Mae and Freddie M…

- Solomon, Steven Davidoff, and David Zaring. 2015. “After the Deal: Fannie, Fred…

- Thompson, Daniel. 2021. “The Rescue of Fannie Mae and Freddie Mac – Module B: T…

- Thompson, Daniel and Adam Kulam. 2021. “The Rescue of Fannie Mae and Freddie Ma…

- US Department of the Treasury (UST). 2008. “Press Release: Statement by Secreta…

- ———. 2011. “Reforming America’s Housing Finance Market: A Report to Congress.” …

- US Department of the Treasury and Federal National Mortgage Association (UST/Fa…

- Vergara, Emily. 2021. “The Rescue of Fannie Mae and Freddie Mac – Module C: GSE…

- Wiggins, Rosalind Z., Benjamin Henken, Daniel Thompson, Adam Kulam, and Andrew …

- Zanger-Tishler, Michael, and Rosalind Z. Wiggins. 2021. “The Rescue of Fannie M…

Key Program Documents

-

Christopher Dickerson to James B. Lockhart: Proposed Appointment of the Federal Housing Finance Agency as Conservator for Fannie Mae (09/06/2008)

Memo from Christopher Dickinson to James Lockhart that includes reasons for conservatorship and the background of the case.

-

Christopher Dickerson to Daniel Mudd (09/04/2008)

Midyear report that classifies Fannie Mae as critically undercapitalized, which would give FHFA Director Lockhart discretion to take Fannie Mae into receivership (see Key Design Decision No. 2 for more information).

-

Christopher Dickerson to Richard Syron (09/04/2008)

Midyear report that classifies Freddie Mac as critically undercapitalized, which would give FHFA Director Lockhart discretion to take Freddie Mac into receivership (see Key Design Decision No. 2 for more information).

-

Fact Sheet: Questions and Answers on Conservatorship (09/07/2008)

Defines conservator, its function, goals, and other generally asked questions.

-

Conservatorship Strategic Plan 2012

Focuses on shrinking the GSEs’ role in the mortgage market while continuing to provide an adequate supply to the market.

-

Conservatorship Strategic Plan 2014

Focuses less attention on reducing the size of Fannie and Freddie’s market share.

-

Letter: Edward DeMarco to Committee on Banking, Housing and Urban Affairs and Committee on Financial Services (DeMarco 2010)

Outlines the FHFA’s commitment to scale back the GSEs’ portfolios and establish a new process for product review.

-

Emergency Economic Stabilization Act of 2008 (§1424)

Mandates that the FHFA act to prevent foreclosures.

-

Housing and Economic Recovery Act of 2008 (HERA 2008, §1117)

Legally authorizes the FHFA to take Fannie and Freddie into a conservatorship.

-

Meeting the Challenges of the Financial Crisis (Lockhart 2009)

Outlines actions taken by the FHFA, Treasury, and the Fed in the first six months of conservatorship.

-

Statement by Secretary Henry M. Paulson, Jr. on Treasury and Federal Housing Finance Agency Action to Protect Financial Markets and Taxpayers (UST 2008)

Treasury press release that announces the four-part rescue plan for the GSEs, including the conservatorship.

-

Statement of FHFA Regarding Contracts of Enterprises in Conservatorship (FHFA 2008a)

Asserts that both GSEs will honor existing contracts and are able to enter new contracts.

-

The Appointment of FHFA as Conservator for Fannie Mae and Freddie Mac (Lockhart 2008)

Outlines the weaknesses of OFHEO (former GSE regulator) and explains why the FHFA decided to enter Fannie and Freddie into a conservatorship.

-

As Crisis Grew, a Few Options Shrank to One (09/07/2008)

Generally represents the media reaction and level of public understanding just after the conservatorship was enacted.

-

In Rescue to Stabilize Lending, U.S. Takes over Mortgage Finance Titans (Stephen Labaton and Edmund L. Andrews, 09/08/2008)

Generally represents the media reaction and level of public understanding just after the conservatorship was enacted.

-

After the Deal: Fannie, Freddie, and the Financial Crisis Aftermath (Solomon and Zaring 2015)

Explains the legal ramifications of the conservatorship, with particular emphasis on the 2012 amendment.

-

Effect of the Conservatorship of Fannie Mae and Freddie Mac on Affordable Housing (Sale 2009)

Explains how the conservatorship affected the GSEs’ affordable housing goals.

-

The Rescue of Fannie Mae and Freddie Mac (Frame et al. 2015)

Addresses the causes of the conservatorship and evaluates the program’s efficacy in the short run and the long run.

-

When Good Investments Go Bad: The Contraction in Community Bank Lending after the 2008 GSE Takeover (Rice and Rose 2016)

Examines and evaluates the effects the conservatorship, mainly from the perspective of banks.

-

2008 Annual Report to Congress (OFHEO 2008)

Covers basic operations, market contractions, financial health of the GSEs, and risk. See subsequent years’ reports below.

-

2008, Revised (FHFA 2009a).

Revised version of 2008 FHFA annual report to Congress.

-

2009 (FHFA 2010b).

2009 edition of FHFA annual report to Congress.

-

2010 (FHFA 2011).

2010 edition of FHFA annual report to Congress.

-

2011 (FHFA 06/13/2012).

2011 edition of FHFA annual report to Congress.

-

2012 (FHFA 06/13/2013).

2012 edition of FHFA annual report to Congress.

-

2013 (FHFA 06/13/2014).

2013 edition of FHFA annual report to Congress.

-

2014 (FHFA 06/15/2015).

2014 edition of FHFA annual report to Congress.

-

2015 (FHFA 06/15/2016).

2015 edition of FHFA annual report to Congress.

-

2016 (FHFA 06/15/2017).

2016 edition of FHFA annual report to Congress.

-

2008 Performance and Accountability Report (FHFA 2008d)

Describes factors leading up to conservatorship, operations of the FHFA, goals of the FHFA, and management strategies. See subsequent years’ reports below.

-

2009 (FHFA 2009b).

2009 edition of FHFA Performance & Accountability Report.

-

2010 (FHFA 11/15/2010).

2010 edition of FHFA Performance & Accountability Report.

-

2011 (FHFA 11/14/2011).

2011 edition of FHFA Performance & Accountability Report.

-

2012 (FHFA 2012c).

2012 edition of FHFA Performance & Accountability Report.

-

2013 (FHFA 12/16/2013).

2013 edition of FHFA Performance & Accountability Report.

-

2014 (FHFA 11/17/2014).

2014 edition of FHFA Performance & Accountability Report.

-

2015 (FHFA 11/16/2015).

2015 edition of FHFA Performance & Accountability Report.

-

2016 (FHFA 11/15/2016).

2016 edition of FHFA Performance & Accountability Report.

-

2012 Conservatorship Scorecard (FHFA 2012b)

Establishes objectives and schedules to meet the goals outlined in the FHFA’s strategic plans. See subsequent years’ scorecards below.

-

2013 (FHFA 03/04/2013).

Establishes objectives and schedules to meet the goals outlined in the 2013 FHFA strategic plan.

-

2014 Scorecard for Fannie Mae, Freddie Mac, and Common Securitization Solutions (FHFA 05/13/2014).

Establishes objectives and schedules to meet the goals outlined in the 2014 FHFA strategic plan.

-

2015 (FHFA 01/14/2015).

Establishes objectives and schedules to meet the goals outlined in the 2015 FHFA strategic plan.

-

2016 (FHFA 12/17/2015).

Establishes objectives and schedules to meet the goals outlined in the 2016 FHFA strategic plan.

-

Fannie Mae, Freddie Mac, and the Federal Role in the Secondary Mortgage Market (CBO 2010)

Analyzes reasons for federal involvement in the secondary mortgage market and provides alternative approaches for the future of the secondary mortgage market.

-

GSE Reform: Creating a Sustainable, More Vibrant Secondary Mortgage Market (MBA 2017)

Develops a new GSE structure that could be sustainable for the GSEs after the conservatorship.

-

Housing Finance at a Glance: A Monthly Chartbook [sic] (Urban Institute 01/2016)

Includes annualized data on market indicators, GSE portfolios limits, mortgage originations, et cetera.

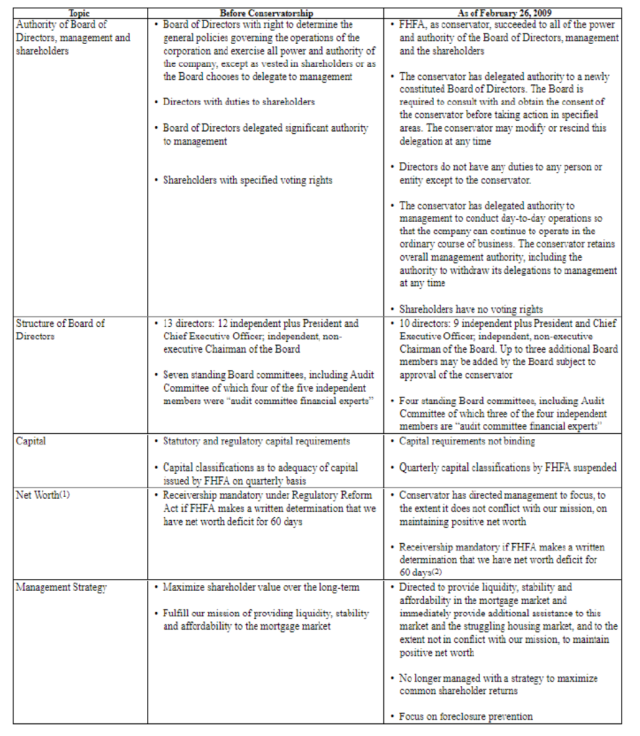

Appendix A: Changes to Company Focus under Conservatorship

Source: Fannie Mae 2008b.

Source: Fannie Mae 2008b.

Appendix B: Rescue Options (after the Passage of HERA)

ˡ In consultation with the chairman of the Federal Reserve.

² FHFA director could take either GSE into conservatorship or receivership for any of the following reasons: (a) Assets were less than its obligations; (b) substantial dissipation of assets; (c) unsafe or unsound condition; (d) cease and desist orders; (e) concealment or refusal to provide the books, papers, etc.; (f) inability to pay obligations or meet the demands of creditors; (g) losses that would deplete capital, with little chance of recapitalization; (h) any legal violations; (i) by request of its board of directors or shareholders; (j) undercapitalization; (k) critical undercapitalization; and/or (l) money laundering.

ᵌ At the discretion of the FHFA director.

4 In order to restructure the GSEs into new entities, the FHFA and Treasury required congressional approval to revoke the GSEs’ charters. Until that point, the charter would remain in the bridge entity.

Compiled by Daniel Thompson.

Sources for receivership and conservatorship: HERA 2008, Frame et al. 2015.

Sources for nationalization: Elliott 2009, Frame et al. 2015.

Taxonomy

Intervention Categories:

- Resolution and Restructuring - Fannie & Freddie

Institutions:

- Fannie & Freddie

Countries and Regions:

- United States

Crises:

- Global Financial Crisis