Bank Debt Guarantee Programs

Polish Guarantee Scheme

Purpose

To facilitate short- and medium-term liquidity in the interbank market to solvent financial institutions in Poland.

Key Terms

-

Announcement DateNovember 30, 2008

-

Operational DateMarch 13, 2009

-

Date of First Guaranteed Debt IssuanceN/A

-

Issuance Window Expiration DateInitially December 31, 2009; after 18 extensions: November 30, 2018

-

Program SizeInitially PLN 40 billion ($13.7 billion); increased in 2012 to PLN 160 billion

-

UsageNone

-

OutcomesN/A

-

Notable FeaturesRequired participants to provide the government with collateral

Key Design Decisions

Program Size

Eligible Institutions

Eligible Debt - Type

Eligible Debt - Maturities

Eligible Debt - Currencies

Participation Limits for Individual Firms

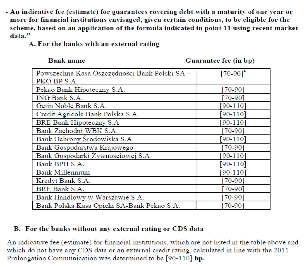

Fees

Other Conditions

Program Issuance Window

Key Program Documents

Taxonomy

Intervention Categories:

- Bank Debt Guarantee Programs

Countries and Regions:

- Poland

Crises:

- Global Financial Crisis