Broad-Based Capital Injections

Norway – GBIF/SBIF

Purpose

The GBIF was established as a short-term facility to manage government ownership in banks initially through loans to the two industry guarantee funds for savings and commercial banks respectively, and later through capital injections.

Key Terms

-

Announcement DateJanuary 25, 1991

-

Operational DateMarch 15, 1991

-

Wind-down DatesN/A

-

Legal AuthorityAct on Government Bank Insurance Fund January 1991

-

Peak UsageNOK 16.2 billion ($1.9 billion)

-

ParticipantsFokus Bank, Christiania Bank, Den norske Bank, others

-

AdministratorKing, Norges Bank, Banking Insurance and Securities Commission

Privately owned banks had funded the Savings Bank Guarantee Fund (SBGF) and Commercial Bank Guarantee Fund (CBGF) between 1921-1938 to provide guarantees and capital injections to struggling banks. Bank legislation in 1961 made participation in such guarantee funds compulsory for all Norwegian banks, and they were reorganized according to that law. However, after banks began to struggle in the late 1980s, the two funds quickly ran out of resources. The Norwegian Parliament (Storting) created the Government Bank Insurance Fund (GBIF) in March 1991 to loan money to the two funds. They both quickly incurred unsustainable amounts of debt to the government. In November 1991, the Storting gave the GBIF the power to inject capital directly into banks through subordinated debt, common and preferred equity, and primary capital certificates, with the Storting allocating NOK 5 billion ($590 million) in initial funding to the GBIF. At the same time, it established the Government Bank Investment Fund (Norwegian Statens Bankinvesteringsfond, SBIF) to provide liquidity to struggling but solvent banks. From 1991-93, the GBIF and SBIF bought stakes in many banks, including three of the four largest: Fokus Bank, Den norske Bank, and Christiania Bank. In 2002, the GBIF transferred to the SBIF its last shares in Den norske Bank and ceased operating. In 2004, the SBIF transferred to the Norwegian Ministry of Finance and Industry its 34% stake in DnB NOR, the entity that resulted from the merger of Den norske Bank and the Union Bank of Norway, and ceased operating.

|

Norway Context 1991–1995 |

|

|

GDP (SAAR, Nominal GDP in LCU converted to USD) |

119,700,000,000 USD 1991 |

|

GDP per capita (SAAR, Nominal GDP in LCU converted to USD) |

$45,858 in 1991 |

|

Sovereign credit rating (5-year senior debt) |

Not available |

|

Exchange Rate (to USD) |

6.49 NOK to USD |

|

Size of banking system |

Not available |

|

Size of banking system as a percentage of GDP |

1991 Bank deposits are 52.6% of GDP |

|

Size of banking system as a percentage of financial system |

Not available |

|

Five-bank concentration of banking system |

Five-bank asset concentration of 12.8% in 1998 |

|

Foreign involvement in banking system |

5% in 1995 |

|

Government ownership of banking system |

32% in 1995 |

|

Existence of deposit insurance |

Not available |

|

Sources: IMF International Financial Statistics, World Bank Global Financial Development Database. |

The Norwegian banking crisis emerged in the late 1980s following rapid financial deregulation, excessive bank lending, and a drop in oil prices. The banking industry first addressed the crisis in 1988-90 through its own self-funded Savings Bank Guarantee Fund (SBGF) and Commercial Bank Guarantee Fund (CBGF), but both quickly ran out of money. Norway established the Government Bank Insurance Fund (GBIF) in March 1991 to extend government loans to the two private bank guarantee funds. The two funds used these loans to inject capital into Norwegian banks while guaranteeing their liabilities, but their debt burdens mounted, and they could not meet the need for capital.

In November 1991, the Norwegian Parliament (called the “Storting”) allowed the GBIF to make direct capital injections to distressed banks and established the Government Bank Investment Fund (SBIF) to maintain state ownership of banks in the longer term. The Storting allocated NOK 13.5 billion to the GBIF. However, the GBIF made 17 capital injections totaling NOK 16.2 billion in the years 1991-93 as it received interest on part of its capital, the CBGF and SBGF made payments on their loans, and the GBIF sold shares to the SBIF. The NOK 16.2 billion includes NOK 13.1 billion of direct capital injections by the GBIF into banks, most of which went to Norway’s three largest banks: Fokus Bank, Christiania Bank, and Den norske Bank. It also includes GBIF loans of NOK 554 million to the SBGF to inject capital into savings banks and NOK 2.5 billion to the CBGF to inject capital into commercial banks. In addition to the GBIF capital injections, the Norwegian government also allocated NOK 1 billion to the SBGF and introduced a program of subsidized, low-interest central bank deposits, which cost the government about NOK 2.7 billion.

After 1993, no more injections were required. The GBIF slowly sold its shares in banks while receiving loan repayments. In 2002, it transferred its remaining holdings to the SBIF and closed. In 2004, the SBIF transferred its holding of DnB NOR, the result of the merger of Den norske bank and the Union Bank of Norway, to the Ministry of Trade and Finance and closed.

International observers generally view the government’s use of capital injections through the GBIF and SBIF as a success that reduced the cost of the crisis, created normal conditions for borrowers, and prevented the spread of financial problems and bank failures. However, some observers suggested the government faced a conflict of interest in its role as both a regulator and a shareholder. Some also criticized the government’s unilateral decision to write down the value of its shares in Fokus Bank and Christiania Bank.

Key Design Decisions

Part of a Package

1

The GBIF was not explicitly part of a package, although the Norwegian government did pursue other policies to address the financial crisis (Moe 2004). These included loans from Norges Bank at below-market interest rates, which amounted to about 10% of banks’ funding in late 1991; a Storting grant to the Savings Bank Guarantee Fund (SBGF); and a 75% reduction of banks’ annual premiums to their respective guarantee funds.

On March 5, 1991, the Storting established the Government Bank Insurance Fund (GBIF), allocating NOK 5 billion to fund it. The Storting gave the GBIF a specific mandate: to lend public money to the two private bank deposit guarantee funds, CBGF and SBGF, to recapitalize failing banks (Bergo 2003). The CBGF used the borrowed funds to complete the bailout of Fokus Bank and to begin injecting capital into Christiania Bank (Ongena 2003). Shortly thereafter, Den norske bank, the largest Norwegian commercial bank, announced its own need for capital injections. It became clear that the GBIF’s funding would not be sufficient to recapitalize the three banks.

In late 1991, the Storting took action to strengthen the banks’ finances (Haare 2016). The measures included an expansion of the GBIF by NOK 6 billion; the establishment of the Government Bank Investment Fund (SBIF) with NOK 4.5 billion; subsidized, low-interest deposits from Norges Bank; reduced premium payments that the banks were required to pay the two bank guarantee funds; an appropriation of NOK 1 billion to the SBGF; and reduced liquidity requirements for banks. Most importantly, it allowed the GBIF to make direct capital injections in banks, rather than just loans to the two private bank guarantee funds.

The GBIF was established as a short-term facility to manage government ownership in banks, while the SBIF was established to manage long-term state investments in the banking sector on commercial principles, rather than purely for financial stability purposes (Drees 1998, Munthe 1992). The SBIF worked with private investors to provide capital to banks that were not in crisis to help overcome the lack of confidence in the markets (Moe 2004). After 1995, the GBIF became more of a contingency body and the SBIF managed state ownership in the banking industry.

Legal Authority

1

The GBIF was a temporary facility that was intended to provide loans to the Commercial and Savings Bank Guarantee Funds, so that they in turn could capitalize distressed banks (Drees 1998). The Norwegian government planned to wind the GBIF down by 2000 and transfer the shares it held to the SBIF. The SBIF was established as an indefinite facility to manage long-term state investments in banks. The Norwegian government used the SBIF’s interest in Norway’s two largest commercial banks to ensure that they focused on financing Norwegian industries and that they would not lend imprudently.

The Storting initially proposed establishing the GBIF on January 25, 1991 and established it on March 15, 1991. The Storting allowed the GBIF to make direct capital injections on November 29, 1991 (Moe 2004). This allowed the GBIF to purchase shares, primary capital certificatesFA primary capital certificate was the equity instrument of savings banks. Certificate holders had somewhat limited rights compared to shareholders of commercial banks., or other equity capital instruments in Norwegian banks that could not raise private capital. This mechanism would result in GBIF’s owning 100% of the shares in banks that had lost all their capital.

The Government Bank Investment Fund (SBIF) was established in November 1991 with NOK 4.5 billion (Drees 1998). The SBIF was intended to make capital injections on commercial principles and help banks that were not in crisis raise capital when there was a general lack of confidence in the markets (Moe 2004). It was designed to participate alongside private investors in bank capital instruments. During the same time, Norway made amendments to the Community Banking Act that allowed the government to write down a bank’s share capital to zero, forcing losses on shareholders, if less than 25% of its share capital remained.

The Relationship Between the GBIF and the SBIF

Initially in 1991, when the SBIF was established and the GBIF was granted permission to make capital injections, it was not clear what the relationship between the two institutions would be (Moe 2004). A 1992 document maintained that the GBIF’s equity holdings were in service of crisis management while the SBIF’s holdings were in an investor role alongside private owners. The GBIF provided capital support to struggling banks during the crisis, making sure to impose requirements including cost cutting and balance sheet reductions that helped maintain stability. The GBIF’s purchases of shares and primary capital certificates granted it varying degrees of ownership in different banks, but it generally avoided directly intervening in bank operations, preferring to exert influence as a contracting party.

Governance

1

The GBIF was governed by a board of experts that made its decisions, carrying out operations at a distance from political authorities. The three-member board was appointed by the Government and supplemented by two non-voting representatives from Norges Bank and the Norwegian financial supervisor under the Ministry of Finance, the BISC (Banking, Insurance, and Securities Commission), with a secretariat provided by Norges Bank (Moe 2004, Storting 1991a). However, it maintained a close relationship with Norwegian financial supervisors and Norges Bank, the latter of which also played a role in Norway’s financial stability infrastructure (Bergo 2003). Norges Bank was the lender of last resort for recapitalized banks, and a source of liquidity support to sound financial institutions, though banks did not have to resort to its provisions as they generally kept their funding.

Source of Injections

2

The GBIF was initially funded with 5 billion NOK, later increased with an additional 6 billion NOK in November 1991, when the Storting allowed it to make direct capital injections in banks (Andersen 2014; Drees 1998). The SBIF was funded by 4.5 NOK to invest in banks alongside private investors, eventually disposing of its shares. In total, the Storting appropriated NOK 13.5 billion to the GBIF (Moe 2004).

Prior to the establishment of the GBIF, these guarantee funds could recapitalize a failed bank or provide guarantees and financial support to facilitate a takeover, if those options were more cost-effective than liquidating the bank and paying the depositors (Bergo 2003). Membership was compulsory and banks paid membership fees. By 1988, the CBGF had NOK 4.1 billion of capital (2.4% of member banks’ deposits from nonbanks). The SBGF had NOK 1.4 billion of capital, with member banks providing guarantees of NOK 1.6 billion from their own funds. Savings banks increased their guarantees through the SBGF by NOK 700 million in 1989. Both funds had the Banking, Insurance, and Securities Commission (BISC) and Norges Bank represented on their boards, along with five members elected by member banks (Moe 2004). At the onset of the crisis, the CBGF injected $65 million (NOK 1.3 billion) into impaired banks and facilitated their mergers with healthier banks. These capital injections appeared to stabilize the banking industry by spring 1990 (Ongena 2003).

However, in January 1991, Norway’s three largest commercial banks announced losses (Ongena 2003). Funds previously available through international markets were no longer available or were prohibitively expensive. Recapitalizing Fokus bank, Norway’s third-largest commercial bank, depleted nearly all of CBGF’s remaining capital by February 1991. The banking system was in danger of collapsing without further aid. At the peak of the crisis in 1991, bank loan losses equaled 2.8% of GDP, while 9% of outstanding loans were non-performing (Bergo 2003). The CBGF and SBGF were effectively depleted, and they could no longer insure deposits after the situation deteriorated at the largest banks (Moe 2004).

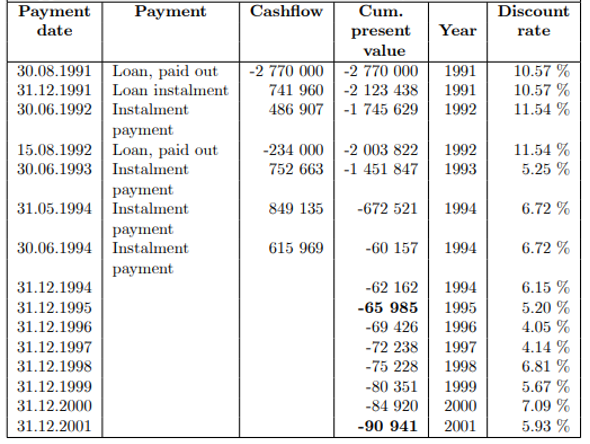

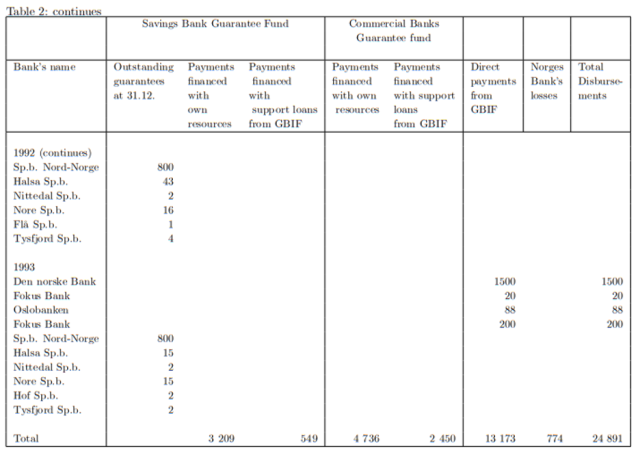

After the GBIF was founded, it was able to make loans to the CBGF and SBGF so that they could better recapitalize failing banks. Figure 4 shows the loans made from the GBIF to the two guarantee funds and Figure 5 shows how the guarantee funds supported banks. Figure 6 shows a timeline of bank support from these institutions.

Figure 4: Support Loans to the SBGF and the CBGF (in thousands of NOK)

Source: Moe 2004.

Source: Moe 2004.

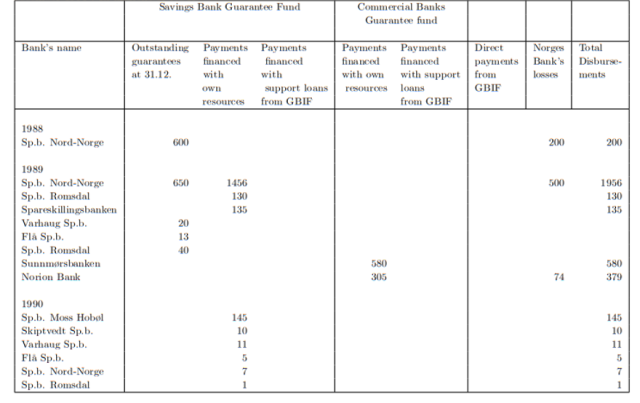

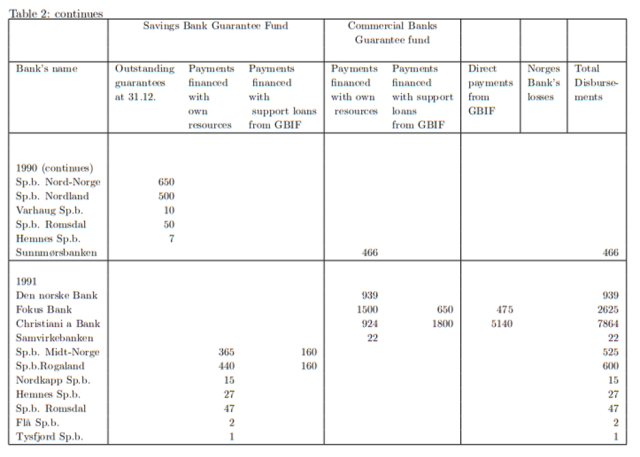

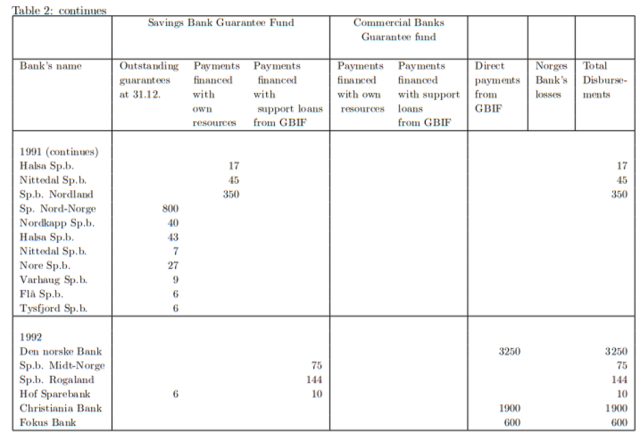

Figure 5: Disbursements and Outstanding Guarantees in Connection with Guarantee Funds’ Involvement January 1, 1988–December 31, 1993 (in millions of NOK)

Source: Moe 2004.

Source: Moe 2004.

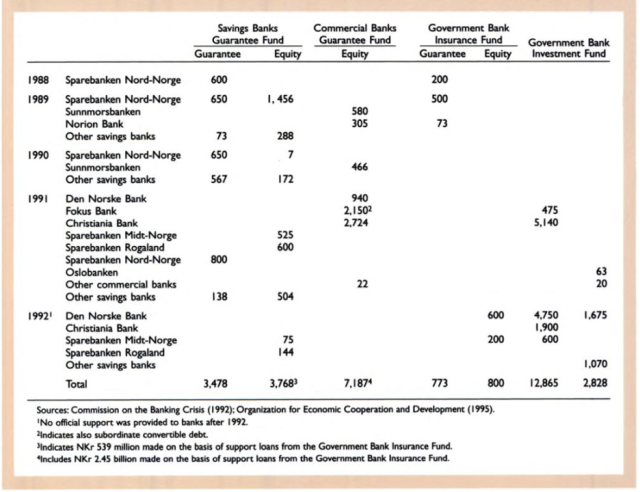

Figure 6: Norway: Funds Used in Rescue Operations

Source: Drees 1998.

Source: Drees 1998.

Eligible Institutions

1

When the GBIF was originally established on March 5, 1991, its mandate was to lend public money to the two private bank deposit guarantee funds, CBGF and SBGF, so that they could continue to recapitalize failing banks (Ongena 2003, Bergo 2003).

When the Storting extended the mandate of the GBIF in late 1991, distressed banks were eligible to receive capital injections directly from the GBIF (Drees 1998). These banks were also eligible for SBIF share purchases, which occurred on a commercial and long-term basis.

The GBIF also injected capital to liquidate Oslobanken. Though Norwegian banks as a whole reported improvements in 1993, Oslobanken, which was already owned in part by the SBIF, applied for GBIF capital since it could not meet its capital requirement (Moe 2004). The GBIF initially had rejected this request, instead attempting and failing to orchestrate a merger with another bank. It is unclear why GBIF had rejected the request. Due to the bank’s reported negative equity capital and a concern for systemic risk, the GBIF injected capital alongside CBGF guarantees to facilitate the liquidation of Oslobanken. This concluded in November 2000.

Capital Characteristics

1

GBIF

In early 1991, Christiania Bank and Fokus Bank both applied for capital injections from the CBGF. The CBGF had depleted funds, so in August 1991, the GBIF loaned nearly half its funding to the CBGF to finance capital injections of NOK 1.8 billion of preferred shares in Christiania Bank and NOK 650 million of preferred shares in Fokus Bank (Kaen 1997). In October 1991, the GBIF provided two loans of NOK 160 million to the SBGF to recapitalize Sparebanken Rogaland and Sparebanken Midt-Norge. These capital injections were intended to bring the recapitalized banks to capital adequacy by the end of the year (Moe 2004). The GBIF designed these injections to be preferred capital without voting rights that accrued dividends (Storting 1991c).

In the third quarter of 1991, Christiania Bank had incurred losses so great that all common and preferred equity capital, of which NOK 2.7 billion had been injected by the CBGF, was written off (Moe 2004). Fokus Bank had made losses that wiped out all common equity and some preferred equity, while Den norske Bank had only NOK 327 million of share capital and all its preferred equity remaining.

The GBIF signed agreements to provide all three banks capital injections mostly in common equity, and helped Den norske and Christiania banks achieve an 8% capital ratio by the end of 1991 and you can see these transactions in Figure 7. Fokus Bank achieved a 5.5% capital ratio, but this was adequate as it had promised to reduce its balance sheet significantly in the following two years. By the end of 1991, the government completely took over Fokus Bank and Christiana Bank, and became the majority owner of Den norske Bank (Moe 2004).

Later in 1992, as the banks continued to post losses, the GBIF agreed to provide NOK 4 billion in mostly preferred equity to again bring Den norske Bank and Christiania Bank up to an 8% capital adequacy ratio, subject to additional appropriations by the Norwegian Storting, and to help Fokus Bank achieve the 8% capital adequacy ratio, which occurred after it sold some of its holdings (Moe 2004; Figure 7). This would also bring Fokus Bank to an 8% capital ratio after parts of the bank were sold as per its contract with GBIF. The GBIF agreed to inject NOK 600 million in Den norske Bank, and NOK 200 million in Fokus Bank if their capital ratios dipped below 3.8% in late 1993, but this did not occur.

The GBIF later sold 229 million shares of Christiania Bank to the SBIF at a price based on the equity capital per share in the bank’s 1992 annual accounts. The GBIF also had contracted to provide Fokus Bank additional capital if needed to maintain its capital requirements, and in 1993, contributed NOK 20 million to help it merge with Samvirkebanken (Moe 2004). Consequently, there was a small minority of private owners in Fokus bank.

The GBIF also made loans to the SBGF to support capital injections to Sparebanken Rogaland and Sparebanken Midt-Norge (Moe 2004).

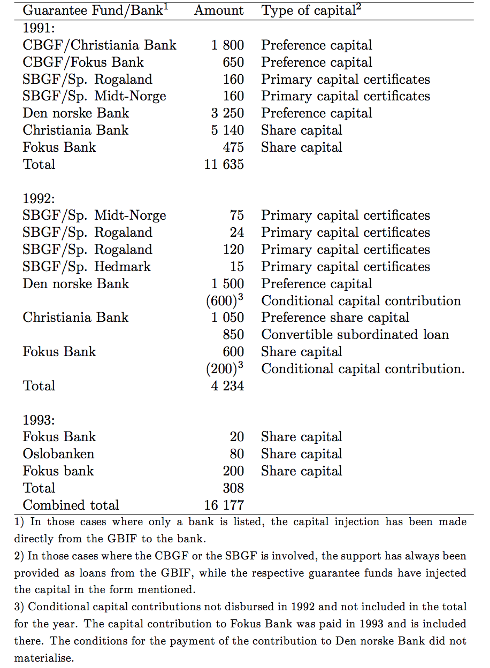

Figure 7: Overview of GBIF’s Decisions Concerning Support Measures (in millions of NOK)

Source: Moe 2004.

Source: Moe 2004.

SBIF

The SBIF made two primary capital certificate injections in 1991, purchasing 19.6% of Oslobanken and 32.3% of Samvirkebanken to meet capital adequacy requirements (Figure 7). It also made two convertible loans in the savings bank Union Bank of Norway totaling NOK 1 billion and convertible loans of NOK 70 million and NOK 25.6 million in the savings banks Sparebanken Vest and Sparebanken Møre respectively. Of the 1992 capital injections, NOK 1.5 billion occurred through the sale of equity capital to the SBIF (Moe 2004).

Restructuring Plan

1

Before GBIF directly injected capital, it conducted an audit of the bank and required that all losses calculated by an audit would first be borne by the original private shareholders (Milne 2009). This decision is generally made by the banks’ General Meetings, but if the bank refused to do so, an amendment to the Commercial Bank Act allowed the government to write down the share capital of the bank against the losses in the audited interim account (Bergo 2003). This was done twice, when shareholders refused to write down a bank’s shares as required by GBIF. This made certain that shareholders bore a bank’s losses before taxpayer money was put on the table.

The conditions imposed on injections made through GBIF support were unattractive to shareholders and bank managers, incentivizing them to try private-sector solutions first, and use the GBIF only as a last resort (Bergo 2003). These conditions also made sure that GBIF-capitalized banks did not have a competitive advantage over other banks. The condition that required losses to be absorbed by shareholders was also imperative in gaining political support from the electorate to conduct rescue operations.

Fate of Existing Board and Management

1

The GBIF replaced two bank-elected members each from the boards of the CBGF and the SBGF after it began making loans to them. This gave the government a majority of four on each seven-member board. These new guarantee-fund boards would choose the new boards of recapitalized banks. They often replaced bank management, though it was not required (Moe 2004; Bergo 2003). However, the governance structure of the banks remained intact while the ownership was transferred to the GBIF (Bergo 2005). This ensured that politicians could not easily micromanage the recapitalized banks and prevented the GBIF from interfering in the banks’ day-to-day business operations. A commenter close to the program confirmed that there was agreement among authorities that government funds should not have lasting and direct influence on the daily operations of the banks.

Other Conditions

1

Capital support through the private bank guarantee funds required a bank to present a business plan that improved profits and reduced risk-weighted assets (Drees 1998). For loans made to the private bank guarantee funds, the GBIF had the power to impose conditions on both the private bank guarantee funds and banks that received injections from them (Moe 2004).

Capital injections performed through Norwegian private bank guarantee funds or directly from the GBIF were contingent on reducing bank operating costs, downsizing some activities, and taking measures to restrain growth in total assets. The banks that received GBIF injections were required to regularly update the GBIF on their compliance with the conditions set during the injections and their progress towards profitability (Bergo 2005). Conditions could include programs for cutting operating costs and bank branches (Moe 2004). These conditions were customized for each bank and made public (Bergo 2003).

The GBIF required the write-down of old capital to cover bank losses prior to capital injections to Fokus, Christiania, and Den norske banks in 1991. The shareholders of Fokus and Christiania banks could not agree on how their capital should be written down, so the Norwegian government issued royal decrees on December 20, 1991, that wrote their common equity capital down to zero. The GBIF subsequently became the sole common equity shareholder of Fokus and Christiania banks; as Den norske Bank still had private common equity shareholders, the GBIF purchased preferred shares from it. In 1991 Den norske Bank also acquired mortgage company RealKredit, whose shareholders purchased shares in the bank and underwrote new preference capital alongside the SBIF (Moe 2004). The SBIF subsequently became the majority owner of Den norske Bank with 55.6% of its shares.

In 1992, the lowest priority capital was written down against uncovered losses prior to new capital injections. In Den norske Bank, private share capital, CBGF preferred capital, and the lowest rated GBIF preferred capital were written down to zero, while in Christiania Bank, the par value of common shares was written down from NOK 25 to NOK 7. Fokus bank had all its CBGF preferred capital written down to zero, and its common shares were written down from NOK 25 to NOK 11 (Moe 2004). In 1991-92, the CBGF lost NOK 5.8 billion on the preferred shares it purchased in the top three Norwegian banks.

As the crisis eased in 1993, the GBIF became increasingly confronted with issues of ownership and increases of capital, especially as existing agreements between GBIF and the banks that received capital injections often conflicted with pricing bank shares sensibly when GBIF was considering exiting its injections. When Christiania and Den norske banks sought to issue new capital, the GBIF replaced its agreements with the banks to allow it (Moe 2004). The new agreements clarified the GBIF’s temporary role as a contingency safety net until the CBGF regained sufficient resources; the agreements required regular reporting to the GBIF but allowed the banks to make commercial decisions without encumberment. Fokus Bank arranged a similar agreement in 1995.

Exit Strategy

1

In June 1992, the Norwegian state offered former shareholders a call option on 25% of its shareholding of Christiania Bank (Munthe 1992). They were offered at 16 NOK each, a discount of 36% from their book value of 25 NOK, and a discount of 66% relative to the purchase price of 46.73 NOK that the government had paid. Still, former shareholders purchased only 2.3% of the shares offered (Moe 2004).

There was no set deadline for reprivatizing the banks that received capital injections, allowing the GBIF to set its own strategy for selling the shares it held (Bergo 2005). However, the GBIF was intended to be a temporary measure, and its participations were to be gradually phased out after the crisis (Munthe 1992).

The Norwegian Storting addressed the GBIF and SBIF’s role in the banks in 1993-94, by calling for a continuation of at least one-third state ownership of Den norske and Christiania banks through 1997 to maintain decision-making in Norway, focusing on Norwegian industries (Moe 2004). State ownership of Fokus bank was maintained. The SBIF was to dispose of its holdings in all but the two major banks, selling assets gradually when commercial conditions allowed it.

In December 1993, Christiania Bank sought additional private capital to strengthen its capitalization, and issued NOK 2 billion of equity, bringing the government’s stake down to 68.9% (Moe 2004). The GBIF decided to convert its preferred shares in Den norske Bank to common equity, making the GBIF the majority owner; the government owned 87.5% of Den norske Bank in December 1993. The following spring, Den norske Bank issued NOK 1 billion in shares, and the GBIF also sold NOK 1 billion of its shares, reducing state ownership to 72%.

During the crisis, the SBGF had purchased primary capital certificates in three savings banks with its own funds and GBIF loans (Moe 2004). In spring 1994, it sold these above par and repaid its GBIF debt with NOK 2 billion outstanding, eliminating all obligations the savings-bank sector had to the GBIF.

As the GBIF was intended to be a safety net until the CBGF and the SBGF could support their own industries, money was transferred from the GBIF to the Treasury as shares were sold from 1994 onward based on the GBIF’s liquidity needs (Moe 2004). While the SBGF had regained its health by that time, the CBGF did not repay its GBIF loans until 1995, and the GBIF remained part of the commercial bank safety net while it rebuilt its capital.

The government gradually sold GBIF’s shares in banks after the crisis to the SBIF and on the open market (Meinich 2019). The GBIF sold Fokus Bank to Danske Bank, and gradually sold Christiania Bank, which eventually merged with Nordea, a pan-Nordic group (Honkapohja 2009). The GBIF also sold Den norske Bank shares gradually, though the government still owns 34% of DnB NOR, the entity resulting from the merger of Den norske Bank and the Union Bank of Norway. The GBIF’s holding amounted to about 20% of Norway’s total banking assets as of 2005 (Bergo 2005).

The Norwegian government kept its 34.21% holding in DnB NOR to prevent it being sold to foreign banks as of 2019 (Steigum 2010; DnB Group 2020).

The GBIF’s shares were managed by the SBIF starting in 1995. By the end of 1995, Fokus Bank had been fully privatized, and by the end of 1996, the GBIF and SBIF only held reduced stakes in Den norske Bank and Christiania bank (Moe 2004). Later the Storting recommended the state retain ownership in only one institution, which would be Den norske Bank; consequently, Christiania Bank shares were sold to Merita Nordbanken in 2000. In the spring of 2001, the last remaining shares held by the GBIF, 104 million shares or 13% of DnB NOR, were sold in the open market, and the GBIF was subsequently no longer an owner of bank shares (Meinich 2019).

It became clear that the GBIF was no longer necessary to support the two private bank deposit guarantee funds by 2001, and in 2002, the Fund was abolished (Moe 2004). Christiania, Fokus, and Den norske bank no longer had to report quarterly to the GBIF.

Similarly, the SBIF transferred excess funds to the Treasury from 1993 onwards, paying more than NOK 26 billion in dividends to the state before it was dissolved in 2004. In 2003, the SBIF had a 47.8% stake in DnB ASA, the parent company of Den norske, which merged with the Union Bank of Norway to form DnB NOR ASA in December 2003 (Moe 2004). The SBIF initially held 28.1% of the merged company, though the Norwegian Storting agreed that the SBIF should make private purchases to increase its stake to 34% of DnB NOR. In 2004, when the SBIF was terminated, its DnB NOR shares were transferred to the Ministry of Trade and Industry.

Amendments to Relevant Regulation

1

This was to force the banks to take on the losses before the taxpayers’ money was injected into these banks. This authority was used in two instances where shareholders refused to write down a bank’s shares as required by GBIF. Shareholders in one bank brought the case to the courts but lost (Bergo 2003).

The government shareholding in DnB NOR illustrates the “too-big-to-fail” problem endemic to all Nordic countries (Steigum 2010). DnB NOR’s total assets amounted to about 90% of Norway’s GDP. As of 2019, the GBIF holds a blocking 34% minority in DnB NOR, amounting to about 20% of Norway’s banking sector (Bergo 2005; DnB Group 2020).

After the crisis, the two major banks that were rescued had profit-to-asset ratios that were similar to other Norwegian banks that had not been recapitalized by the GBIF (Bergo 2005). Bergo, Deputy Governor of Norges Bank, acknowledged the success of GBIF interventions in Norwegian banks, but raised a few concerns. First, there exists a potential conflict of interest between the government’s role as a regulator and supervisor of financial markets, and its role as a shareholder. In addition, how will the GBIF’s interest in DnB NOR affect its actions if DnB NOR fails? After the winding down of the GBIF, the Norwegian government transferred the management of DnB NOR from the Ministry of Finance to the Ministry of Industry, so that the regulating body was not directly responsible for the shares. Bergo believes it is possible but unlikely that political authorities would intervene in the bank for political purposes; it would be difficult, as the government is a minority owner of DnB NOR, and its governance structure does not give a minority owner easy control. However, Bergo is concerned that the government might be unwilling to write down DnB NOR shares to cover losses, or would not credibly treat it the same way as privately owned banks.

A commenter close to the program remarked that most of the decisions on solving the banking crises in Norway had broad political support in the Storting. He stated that there was agreement that government funds should not have lasting and direct influence on the daily operations of the banks. Without strong Norwegian private-capital owners, the conservatives in government agreed that the government should maintain a key role as owner in DnB NOR. The alternative would have been to let foreign owners dominate the operations of the largest bank in Norway. The key decision where the Ministry of Finance took an active and leading role, was the appointment of the board of the bank, and the Ministry took care not to be strongly involved in other operations of the bank.

Since banks that received a capital injection from the government were able to continue their normal operations, borrowers faced normal credit conditions (Bergo 2003). Bergo asserts that the economic costs of the crisis were greatly reduced because capital injections saved some banks from closure and maintained the supply of credit. The GBIF was established as a third line of defense, after equity capital and private bank guarantee funds, and was successful in preventing systemic damage caused by bank losses. However, Bergo also supported closing the GBIF to avoid moral hazard after the crisis and advocated for solutions that focus on saving the financial system rather than shoring up individual banks.

The government’s decision to write the capital of Fokus and Christiania banks to zero was controversial. A 1997 retrospective government report studied the bank’s values and simulated alternatives, ultimately deciding that it was a prudent decision. However, it criticized the government for preventing private shareholders from articulating arguments in their defense prior to the write-down of their shares. This contributed to a lack of confidence in the decision. The report concludes that there is some doubt about whether it was necessary to write down shares in Den norske Bank, which had fewer losses and whose losses came about in part due to its government-orchestrated purchase of Realkredit. The report criticizes the government for not evaluating Den norske Bank’s discounted future profit value, which the report estimates would have sufficed to demonstrate that even ordinary share capital had value and did not need to be written down (Moe 2004). However, Den norske Bank’s own shareholders decided to write down the capital instead of seeking better prospects.

- Andersen, Steffen. 2014. Evolution of Nordic Finance. New York, NY: Palgrave Ma…

- Bergo, Jarle. December 10, 2003. “Crisis Resolution and Financial Stability in …

- Bergo, Jarle. June 17, 2005. “Government Ownership of Banks – The Norwegian Exp…

- DnB Group. March 4, 2020. “Annual Report 2019.” DnB Group.

- Drees, Burkhard, and Pazarbaşioğlu Ceyla. 1998. “The Nordic Banking Crises: P…

- Haare, Harald, Arild Lund, and Jon A. Solheim. 2016. “Norges Bank’s financial s…

- Honkapohja, Seppo. January 21, 2009. “The 1990’s Financial Crises in Nordic Cou…

- Kaen, Fred, and Dag Michalsen. June 1997. “The Effects of the Norwegian Banking…

- Meinich, Per. 2019. “Statens Banksikringsfond” Store Norske Leksikon.

- Milne, Alistair. 2009. “The Fall of the House of Credit: What Went Wrong in Ban…

- Moe, Thorvald G, Jon A. Solheim, and Bent Vale. May 2004. “The Norwegian Bankin…

- Munthe, Preben. 1992. “Bankkrisen Utredning.” Oslo: Statens forvaltningstjenest…

- Ongena, Steven, David C Smith, and Dag Michalsen. January 2003. “Firms and Thei…

- Steigum, Erling. December 30, 2010.“The Norwegian Banking Crisis in the 1990s: …

- Storting. January 25, 1991. “Om lov om Statens Banksikringsfond.” (Act on State…

- Storting. October 25, 1991. “Om lov om Statens Bankinvesteringsfond.” (Act on S…

- Storting. November 29, 1991. “Forskrift for virksomheten til Statens Banksikrin…

- Storting. June 4, 2003. Parliament Meeting June 4, 2003. “Møte onsdag den 4. ju…

Key Program Documents

-

(Meinich 2019). Statens Banksikringsfond.

Encyclopaedia entry on the GBIF.

-

(Storting 1991a) Act on State Bank Guarantee Fund (01/25/1991)

Original law establishing the GBIF and its powers.

-

(Storting 1991b) Act on State Bank Investment Fund (10/25/1991)

Original law establishing the SBIF and its capacity.

-

(Storting 1991c) Regulations for the Activities of the GBIF (11/29/1991)

Update to GBIF’s powers allowing it to make direct capital injections.

-

(Storting 2003) Parliament Meeting June 4, 2003

Transcript of discussion on continued state ownership of DnB NOR and increase of ownership from 28.1% to 34%.

-

(Gerdrup 2003) Three Episodes of Financial Fragility in Norway Since the 1890s

BIS paper on Norwegian financial crises.

-

(Honkapohja 2014) Financial Crises: Lessons from the Nordic Experience

Paper on Nordic financial crises and their outcomes.

-

(Munthe 1992) Bankkrisen Utredning

Norwegian government report on the banking crisis.

-

(Vittas 1992) Financial Regulation: Changing the Rules of the Game

Paper on banking crises policymaking, and regulatory reform.

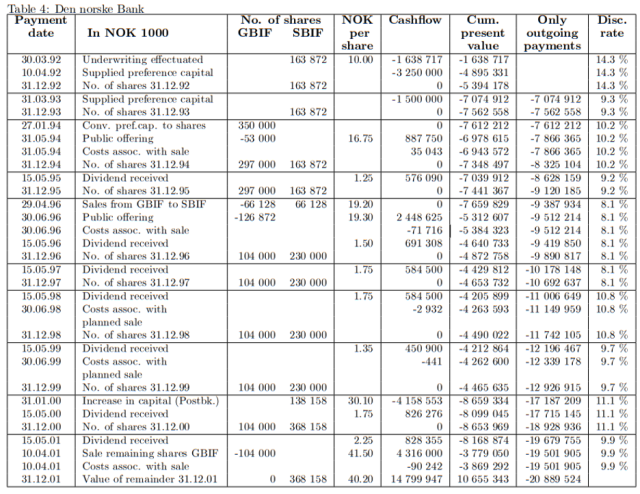

Appendix A: Den norske Bank

Source: Moe 2004.

Source: Moe 2004.

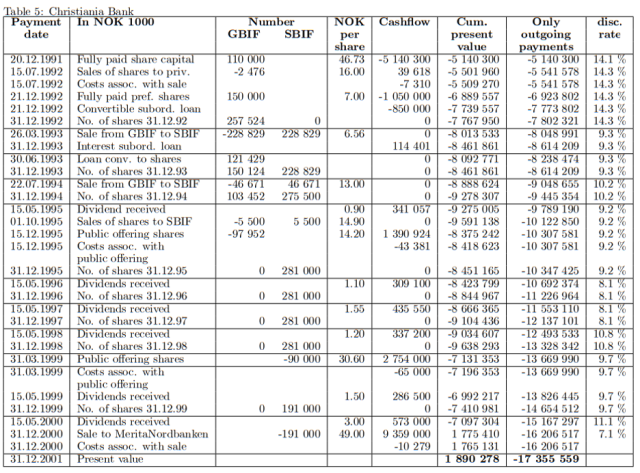

Appendix B: Christiania Bank

Source: Moe 2004.

Source: Moe 2004.

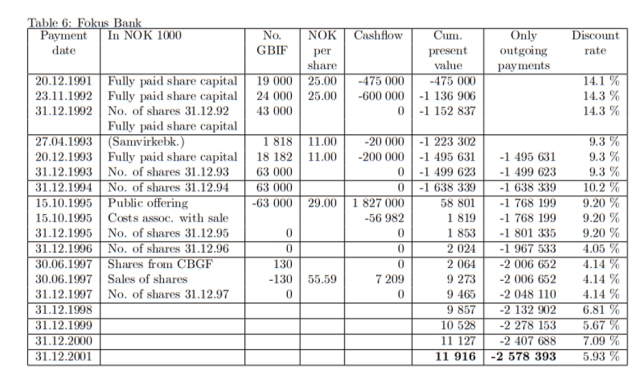

Appendix C: Fokus Bank

Source: Moe 2004.

Source: Moe 2004.

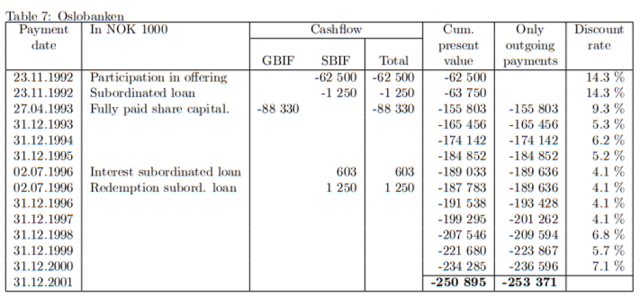

Appendix D: Oslobanken

Source: Moe 2004.

Source: Moe 2004.

Appendix E: Sparebanken NOR

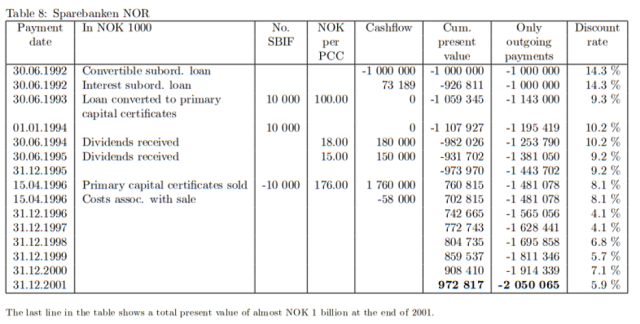

Source: Moe 2004.

Source: Moe 2004.

Appendix F: Timeline of Major Events

1988: Failure of Sunnmørsbanken; CBGF guarantee of its commitments, and Norges Bank liquidity support (Moe 2004).

November 1988: Sparebanken Nord and Tromsø Sparebank insolvent.

July 1989: Sparebanken Nord and Tromsø Sparebank merge to make Sparebanken Nord-Norge; get NOK 1.5 billion loan from Norges Bank.

October 1989: Norion Bank fails; CBGF guarantees only nonbank deposits; Norges Bank loses on its loans and provides a new liquidity loan that CBGF guarantees.

January 1990: Sunnmørsbanken merges with Christiania Bank.

Late 1990: Fokus Bank gets NOK 1.5 billion guarantee from CBGF.

1989-1990: SBGF disburses NOK 1.9 billion (1% total assets of savings banks) in nine banks, and guarantees of NOK 1.2 billion; CBGF makes NOK 1.4 billion of provisions to Sunnmørsbanken and Norion Bank and agrees to make capital injections on a case-by-case basis up to NOK 2 billion amongst all member banks (Moe 2004).

January 25, 1991: Proposal to establish the GBIF.

March 15, 1991: GBIF is established with capital of NOK 5 billion.

June 17, 1991: CBGF approves injection of preferred capital to Den norske Bank, Christiania Bank, and Smvirkebanken NOK 1.6 billion.

Late June 1991: Equity guarantee of NOK 1.5 billion in Fokus Bank replaced with NOK 1.5 billion in preferred shares.

June 28, 1991: CBGF offered NOK 1 billion of preferred shares; distributed only to Samvirkebanken, though other banks also applied for support: NOK 196 million was allocated.

August 1991: GBIF provides support loans to the CBGF for preferred share capital injections to Christiania Bank and Fokus Bank, respectively.

October 1991: GBIF gives SBGF two loans of NOK 160 million each to buy primary capital certificates in Sparebanken Rogaland and Sparebanken Midt-Norge.

October 1991: The Storting establishes the SBIF with NOK 4.5 billion; allocates an additional NOK 6 billion to GBIF, proposes subsidized deposits from Norges Bank, reduced premium payments to two guarantee funds, appropriates NOK 1 billion to the SBGF, and reduces liquidity requirements for banks.

November 29, 1991: The Storting allows the GBIF to directly purchase shares, primary capital certificates and other equity capital instruments, and allows the King in Council to write down bank shares (Moe 2004).

December 20, 1991: Share capital of Christiania Bank and Fokus Bank are written down to zero and GBIF purchases share capital in both banks, becoming their sole owner.

1991: SBIF investment of 19.6% in new shares in Oslobanken; SBIF investment of 32.2% in new shares in Samvirkebanken.

Spring 1992: GBIF offers former shareholders of Christiania Bank the option to purchase 25% of shares; 2.3% were repurchased; SBIF and investors underwrite preferred shares in Den norske Bank—SBIF owns 55.6% of shares.

Spring/Summer 1992: GBIF makes three loans of NOK 219 million to SBGF to fund capital injections to Sparebanken Rogaland and Sparebanken Midt-Norge, as well as a NOK 15 million loan to cover deficit in Hof Sparebank and the SBGF’s guarantee liability in Hedmark Sparebanken.

Late 1992: GBIF injects NOK 4 billion to Fokus, Den norske, and Christiania banks to help them achieve capital adequacy ratios; NOK 1.5 billion of this was SBIF injections.

Late 1992: Den norske share capital, CBGF preferred shares, and low-ranking GBIF preferred shares written down to zero; Christiania shares written down from NOK 25 to NOK 7, Fokus Bank CBGF preferred shares written down to zero, and share par value written down NOK 25 to NOK 11 (Moe 2004).

1992: SBIF invests NOK 1 billion of convertible subordinated debt in Union Bank of Norway and NOK 700 million in Sparebanken Vest and NOK 25.6 million in Sparebanken Møre.

April 1993: Oslobanken applies for GBIF funding—GBIF says no but injects share capital to help liquidate the bank.

December 1993: Christiania Bank raises NOK 2 billion of private share capital—government stake reduced to 68.9%; GBIF converts preferred shares in Den norske Bank to shares making GBIF majority owner of 87.5%.

1993: GBIF provides conditional capital of NOK 20 million of shares to help facilitate the merger of Fokus Bank and Samvirkebanken; SBIF converts subordinated debt in Sparebanken NOR to shares, owning 48% of the bank in 1993; GBIF writes down all shares of Oslobanken and becomes its sole owner.

Late 1993: New agreement between GBIF and Christiania bank that ended the obligation of the bank to report to the GBIF, and the GBIF ability to impose new requirements, as soon as the bank achieved its capital ratio and the CBGF achieved its minimum size to serve as the safety net for the industry.

Early 1994: New agreement between GBIF and Den norske Bank.

May/June 1994: NOK 1 billion of GBIF Den norske shares and NOK 1 billion of new Den norske shares sold in market—government ownership down to 72%.

Spring 1994: SBGF sells primary capital certificates in Sparebanken Rogaland, Sparebanken Midt-Norge, and Sparebanken Nord-Norge above par and repays all its debt to GBIF with NOK 2 billion remaining. End of savings-bank sector obligations to GBIF.

Spring 1995: New agreement between GBIF and Fokus Bank.

1994-1995: GBIF transfers ownership of banks to the SBIF but keeps 16.2% of Den norske Bank.

1995: GBIF sells Fokus Bank to Danske Bank; CBGF repays all its loans obligations to GBIF.

1996: GBIF sells Christiania Bank shares to SBIF and market.

2000: GBIF liquidates Oslobanken completely; SBIF sells its shares in Christiania Bank to Merita Nordbanken.

2001: GBIF sells 104 million shares or 13% of Den norske Bank into the open market.

2002: GBIF abolished.

2003: Den norske Bank merges with Union Bank of Norway to form DnB NOR. SBIF 47.8% share of Den norske becomes 28.1% of DnB NOR.

2004: SBIF terminated; shares in DnB NOR transferred to Ministry of Trade and Industry.

Taxonomy

Intervention Categories:

- Broad-Based Capital Injections

Countries and Regions:

- Norway

Crises:

- Norwegian Banking Crisis 1990s