Broad-Based Emergency Liquidity

New York Clearing House Association: The Crisis of 1914

Purpose

To provide temporary liquidity to member banks of the NYCH and lessen their need to liquidate assets to settle clearing balances

Key Terms

-

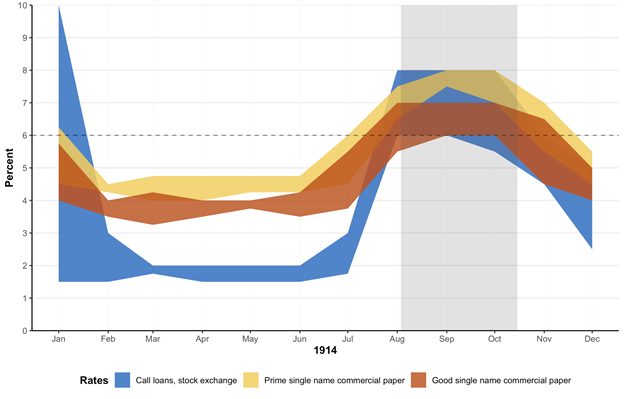

Launch DatesAnnouncement and issuance: August 3, 1914

-

Expiration DateFinal issuance: October 15, 1914; Final cancellation: November 28, 1914

-

Legal AuthorityNot applicable

-

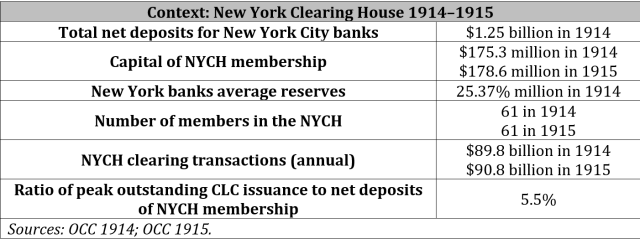

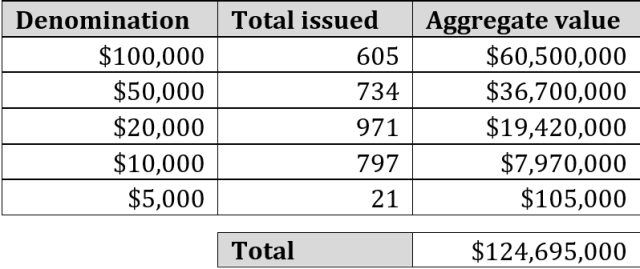

Peak Outstanding$109 million on September 25, 1914

-

ParticipantsMembers of the NYCH, including trust companies

-

Rate6% on circulating CLCs

-

CollateralCommercial paper, bonds and other securities, and collateral loans

-

Loan DurationNot applicable

-

Notable FeaturesPaired with Aldrich-Vreeland emergency currency

-

OutcomesPanic subsided, and the Federal Reserve System began operating shortly thereafter

Key Design Decisions

Purpose

Part of a Package

Management

Administration

Eligible Participants

Funding Source

Program Size

Individual Participation Limits

Rate Charged

Eligible Collateral or Assets

Loan Duration

Other Conditions

Impact on Monetary Policy Transmission

Other Options

Similar Programs in Other Countries

Communication

Disclosure

Stigma Strategy

Exit Strategy

Key Program Documents

Taxonomy

Intervention Categories:

- Broad-Based Emergency Liquidity

Countries and Regions:

- United States

Crises:

- National Banking Era Crises (1863-1913)