Resolution and Restructuring in Europe: Pre- and Post-BRRD

Netherlands: SNS Reaal Restructuring, 2013

Purpose

To ensure uninterrupted services for SNS Reaal customers, the minister of finance stated that “the real estate branch will be isolated financially and operationally from the institution” (Minister of Finance 2013a, 2)

Key Terms

-

Size and Nature of InstitutionFinancial conglomerate featuring a systemically important banking institution holding 2.6 million checking and savings accounts and an insurance subsidiary

-

Source of FailureLosses in SNS Property Finance

-

Start DateDecember 19, 2013

-

End DateDecember 31, 2017

-

Approach to Resolution and RestructuringTransfer of troubled real estate portfolio to a separate real estate management organization and progressive wind-down

-

OutcomesThe state sold the insurance division and Property Finance after spending EUR 700 million to isolate Property Finance

-

Notable FeaturesThe nationalization of SNS Reaal was the first use of the Intervention Act, which included expropriation as a tool for nationalization

In February 2013, the Dutch minister of finance nationalized SNS Reaal, a financial conglomerate that was primarily composed of SNS Bank and Reaal Insurance, after the firm proved unable to remedy a large capital deficit caused by losses in the real estate portfolio of SNS Bank. Alongside the nationalization, the minister of finance announced a EUR 3.7 billion (USD 5 billion) rescue package that included a capital injection and significant restructuring. The goals of the restructuring plan were to isolate the real estate portfolio in a “bad bank” and to sell the insurance subsidiary. The state transferred shareholding responsibilities to NL Financial Investments (NLFI), an independent entity that exercised shareholder rights and oversight in nationalized financial institutions. NLFI oversaw the sale of both the real estate portfolio and the insurance subsidiary to private parties. In 2015, the state announced that it would wind down the holding company of the conglomerate (renamed SRH N.V). On January 1, 2018, the stand-alone bank that resulted from the restructuring became known as de Volksbank. The Dutch state remains the sole shareholder of de Volksbank, with NLFI citing a lack of market interest in a sale.

This module describes the Dutch restructuring of SNS Reaal from February 2013 to January 2018. The ad hoc capital injection provided to SNS Reaal is described in the corresponding case (George, forthcoming).

SNS Reaal N.V. was a Dutch financial conglomerate that included banking subsidiary SNS Bank and insurance subsidiary Reaal Insurance. SNS Property Finance was the real estate portfolio of SNS Bank (EC 2013a).

In 2011, the Dutch National Bank (DNB) identified SNS Bank as one of four systemically important financial institutions subject to heightened supervision policy. In December 2011, the DNB and the Ministry of Finance concluded that there was a strong possibility of a capital shortfall at SNS Bank that could not be solved solely through private means. As such, they formed a joint project group to evaluate potential private, private-public, and public intervention options (Minister of Finance 2013a; Netherlands 2013).

By January 2013, it became clear that the situation at SNS Bank regarding the real estate portfolio was urgent. The Supervisory Review and Evaluation Process (SREP), a regular capital adequacy review conducted by the DNB, revealed that the expected real estate portfolio losses necessitated twice the amount of core capital the conglomerate had. SNS Bank experienced a depositor run, its share price collapsed, and it lost access to capital markets (FSB 2014; Minister of Finance 2013a; World Bank 2016). The DNB notified the minister of finance of SNS Bank’s precarious position on January 24, 2013. It had informed SNS Reaal of the SREP results on January 18, and sent a letter on January 27, 2013, imposing a deadline of January 31 to develop a solution to remedy the capital deficit. The minister of finance announced the nationalization of the conglomerate on February 1, 2013 (EC 2013a; Minister of Finance 2013a; Netherlands 2013; van Tartwijk 2013).

The nationalization involved the purchase of EUR 2.2 billion in new shares, including EUR 1.9 billion in SNS Bank and EUR 300 million in the holding company, SNS Reaal. The government also wrote off the EUR 848 million remaining on the hybrid capital instruments extended to the bank in 2008 and set aside EUR 0.7 billion for losses on the real estate portfolio, bringing the total expected cost to the state to EUR 3.7 billion at the time of nationalization. The government expropriated shares, hybrid capital, and subordinated debt to offset the costs of the intervention. The capital injection preceded a restructuring plan intended to isolate the real estate portfolio as a “bad bank” (renamed Propertize) and divest the insurance subsidiary. When the European Commission (EC) approved the restructuring plan in December 2013, the nominal cost of state measures totaled approximately EUR 5 billionFThis total included a bridge loan provided to SNS Reaal (See Key Design Decision No. 2, Part of Package).. A June 2014 EC recording of transactions stated that the total loss assigned to the capital injection from expropriated securities was EUR 1 billion (EC 2013a; EC 2013b; EC 2014; Minister of Finance 2013a). The minister of finance announced the state’s intention to transfer shareholding administration to NL Financial Investments (NLFI) as soon as possible in the February 1 nationalization announcement. NLFI is a private body that the minister of finance created to ensure commercial, nonpolitical governance of nationalized financial institutions. NLFI exercised the shareholder responsibilities of the injected capital starting on December 31, 2013 (Minister of Finance 2013a; NLFI 2014).

The restructuring plan established December 31, 2017, as the end of the restructuring period. The government finalized the sale of Propertize to a consortium led by JPMorgan on September 27, 2016, for EUR 895.3 million. On September 30, 2015, NLFI renamed the holding company SRH N.V. and announced that its activities were being wound down. The resulting stand-alone bank was rebranded as de Volksbank on January 1, 2018. Though the NLFI produces regular reports with strategies for reprivatization, the state remains the sole shareholder of de Volksbank as of the writing of this case study (De Volksbank n.d.; EC 2013b; NLFI 2015a; NLFI 2015d). The timeline of intervention events is shown in Figure 1.

Figure 1: Timeline of Events Related to the Rescue of SNS Reaal

Sources: De Volksbank n.d; EC 2013a; EC 2013b; Minister of Finance 2013a; NLFI 2015a; NLFI 2015d.

A 2016 report by Matthias Haentjens of the World Bank identifies several parallels between the resolution of SNS Reaal and the resolution framework that the European Union (EU) created through the Bank Recovery and Resolution Directive (BRRD) more than two years later. Specifically, the report likens the Dutch expropriation measures to the bail-in measures outlined by the BRRD. As such, the report asserts that the same parties would likely have been wiped out under a BRRD style of resolution (World Bank 2016).

Several sources directly mention the decision by the minister of finance to not expropriate senior debt at SNS Reaal. A peer review report published by the Financial Stability Board (FSB) states that the DNB advised the minister of finance that expropriating senior debt would result in increased contagion risk due to the heavy reliance of Dutch banks on unsecured funding markets rather than local deposits. In a separate paper, Haentjens also mentions the risk of ratings downgrades of Dutch banks in the event that senior bondholders were forced to accept losses on their bonds (FSB 2014; Haentjens 2013).

In his letter to Parliament announcing the nationalization of SNS Reaal, the minister of finance stated that in the future, “living wills” should exist for large financial institutions to make their resolutions easier. The 2014 FSB report evaluating the Dutch measures makes a similar recommendation, asserting that the state should create an explicit legal basis for the establishment of living wills by all financial institutions. A report by Reg Cap Analytics further emphasizes the potential impact of living wills, asserting that BRRD-style planning and preparation measures may have allowed authorities to identify the extent of the structural issues at SNS Reaal more quickly. This may have allowed for more proactive restructuring measures prior to nationalization (FSB 2014; Minister of Finance 2013a; Morrison and Phillips 2014).

The DNB and Ministry of Finance jointly commissioned an evaluation report from an independent body on the nationalization of SNS Reaal. As a whole, the report defends the nationalization decision given the looming threat to financial stability and the lack of viable alternatives. That said, the report does not evaluate the total costs of the intervention, citing the lack of information available at the time of writing. In terms of recommendations, the report emphasizes governance changes within the DNB and Ministry of Finance, closer coordination with the EC, and legal changes to bring the resolution framework in line with the BRRD and create an explicit legal basis for expropriation and other resolution tools (Evaluation Committee 2014).

Key Design Decisions

Purpose

1

The Dutch National Bank identified SNS Reaal as one of four systemically important financial institutions in the Netherlands in 2011. SNS Bank, the banking division of SNS Reaal, was significantly exposed to losses suffered in the real estate market due to its Property Finance division. In addition to issues in SNS Property Finance, the conglomerate was also troubled by an issue of double leverage. Double leverage is a situation wherein a holding company lends money to a subsidiary. This being the relationship between SNS Reaal and its subsidiaries, the insurance and banking arms of the company were closely intertwined. If parts were sold off, a portion of the resulting funds would need to be used to redeem loans taken out by the overall holding company, rather than the full amount going toward solving the issues in the real estate portfolio (Minister of Finance 2013a).

The DNB conducted a regular Supervisory Review and Evaluation Process in January 2013, which reviewed the firm’s capital adequacy based on activity valuations provided by Cushman & Wakefield (C&W). They found that to absorb the losses from the Property Finance division, the firm would need to double its capital. On January 18, 2013, the DNB notified SNS Reaal of the SREP results, and on January 27, it gave the firm a January 31 deadline to develop a plan to fix the capital deficit (EC 2013a; EC 2013b; Minister of Finance 2013a).

Regarding potential solutions to the capital deficit, a solution in which the three other systemically important banks participated in the bank or holding company proved impossible without a guarantee. The individual sale of the insurance subsidiary would not provide enough relief on its own, and a private solution did not materialize for SNS Bank. The final hope was a private equity solution, which proved unviable on January 31, 2013 (FSB 2014; van Tartwijk 2013).

On February 1, 2013, the minister of finance nationalized SNS Reaal following the conglomerate’s failure to meet the deadline established by the DNB. The minister of finance reasoned, “Without intervention, SNS Bank would irrevocably go bankrupt . . . I had no other option but to nationalize SNS Reaal” (Netherlands 2013, 1)FThe minister of finance also cited the lack of “living wills” for Dutch banks and called for their creation in order to guide the measures authorities take in the face of irreversible problems at a financial institution (Minister of Finance 2013a, 3).. The activation of the deposit guarantee scheme (DGS) would have meant an enormous cost burden for other Dutch banksFOf the estimated EUR 36.4 billion in SNS Reaal deposits as of February 1, 2013, EUR 35.2 billion were insured under the national deposit guarantee scheme (World Bank 2016).. The nationalization announcement outlined the intervention measures and stated the restructuring goals. The announcement directly referenced the real estate portfolio, stating that “the source of the problems, the real estate branch, will be isolated financially and operationally from the institution” (Minister of Finance 2013a, 2). The minister of finance intended to isolate the Property Finance division and divest Reaal Insurance, resulting in a single stand-alone retail bank (EC 2013b; Minister of Finance 2013a; Netherlands 2013).

Part of a Package

1

During the Global Financial Crisis of 2007–2009 (GFC), the Dutch Ministry of Finance extended EUR 750 million of State Aid to SNS Reaal. The aid came in the form of hybrid capital, similar to preferred shares, that the government considered eligible for treatment as Tier 1 capital under Basel capital rules. It had a coupon of either 8.5% or an increasing percentage of the company shareholders’ dividend. But the bank continued to struggle as nonperforming loans accumulated in its real estate portfolio. At the time of nationalization, SNS Reaal had paid back EUR 185 million, but a penalty charge of 50% on the remaining EUR 565 million resulted in a total outstanding balance of EUR 848 million (EC 2013a; Minister of Finance 2013a).

The minister of finance nationalized SNS Reaal on February 1, 2013, after rejecting a last-minute plan submitted by a private equity firm to purchase the bank with government backing. The nationalization announcement included a EUR 3.7 billion aid package, which included the use of EUR 700 million for a real estate management organization for the isolation of SNS Property Finance from the rest of the firm. EUR 2.2 billion went toward capital injections for SNS Bank and the holding companyFA full account of the ad hoc capital injection provided to SNS Reaal is detailed in George (forthcoming).. The remaining EUR 848 million went toward writing off the outstanding balance from the aforementioned 2008 State Aid provided to SNS Reaal (Minister of Finance 2013a).

The minister of finance also provided a EUR 1.1 billion bridge loan to help SNS Reaal meet its short-term funding needs. The bridge loan helped SNS Reaal repay medium-term notes and intercompany funding from Reaal Insurance. The terms of the bridge loan instruments specified a maximum maturity of less than one year and a credit spread of 110 basis points above the higher of the Euro Interbank Offered Rate (EURIBOR) or Dutch state funding rates (EC 2013b).

SNS Reaal also benefited from previously received government guarantees on newly issued debt. Issuances of debt amounting to EUR 4.48 billion were covered by this debt guarantee scheme (EC 2013b).

Legal Authority

1

The public intervention measures taken for SNS Reaal were the first use of the Special Measures Financial Enterprises Act (Intervention Act). The Intervention Act, which was passed on February 14, 2012, with a retroactive effective date of January 20, 2012, granted the minister of finance broad powers of nationalization and expropriation in the interest of financial stability (IR Global 2013; Netherlands 2012). A full account of the terms of this act and its significance can be found in Appendix A.

The Dutch government also required approval of all measures from the European Commission. The EC approved the nationalization and rescue aid measures on February 22, 2013, and gave Dutch authorities six months to submit a restructuring plan. The minister of finance submitted the final restructuring plan on August 19, 2013, and the EC approved the plan on December 19, 2013 (EC 2013b).

Section 6 of the Intervention Act outlines the right of expropriated parties to appeal their expropriation to the Council of State. A large number of parties submitted formal appeals, which the council heard on February 15, 2013. Many appeals objected to the use of Cushman & Wakefield’s valuation of Property Finance as the basis for the decision by the minister of finance. On February 25, 2013, the council decided in favor of the minister of finance, stating that the expropriation was called for given the circumstances (Council of State 2013a; Council of State 2013b; Netherlands 2012).

Administration

1

The minister of finance used the resolution powers granted by the Intervention Act to nationalize SNS Reaal on February 1, 2013. The minister immediately stated his intention to transfer the shareholding responsibilities to NL Financial Investments, an independent, publicly funded institution that exercised shareholder responsibilities in nationalized financial institutions. NLFI is led by a board consisting of three members appointed by the minister of finance. Board members serve four-year terms and can be reappointed by the minister. Individuals associated with the Dutch government or Dutch financial institutions are not permitted to serve, as per the NLFI’s articles of association (Minister of Finance 2013a; Netherlands 2022; NLFI 2014).

Throughout 2013, NLFI prepared for the transfer of shares. On December 31, 2013, the state formally transferred 100% of the shares in SNS Reaal to NLFI. The state separately transferred shares of SNS Property Finance to achieve the isolation. NLFI produced reports advising the minister on avenues to privatize the different divisions (NLFI 2014; NLFI 2015c; NLFI 2015d; SeeNews Netherlands 2013).

The Intervention Act states that the DNB may prepare a transfer plan for financial institutions in which there are signs of “dangerous development” (Netherlands 2012, art. 3:159c). Pursuant to the transfer plan, the DNB thus has the power to transfer assets, liabilities, and equity subject to approval by the Amsterdam District Court. This language designates the DNB as the resolution authority for financial institutions that are failing or likely to fail (FSB 2014; Netherlands 2012).

Governance

1

Dutch authorities submitted their final restructuring plan for SNS Reaal on August 19, 2013, and the EC approved the plan on December 19, 2013. The state then transferred the shares of SNS Reaal to NLFI on December 31, 2013. By transferring shareholding responsibilities to NLFI, the minister of finance aimed to ensure the avoidance of any conflict of interest as the supervisor of the restructuring effort. In preparing for the transfer, NLFI consulted the Dutch Authority for Consumers & Markets (ACM)FThe ACM is a Dutch body primarily concerned with ensuring fair competition and protecting consumer interests. on measures guaranteeing that SNS Reaal and NLFI’s other holdings (ABN AMRO and ASR) remained independent companies with their own management. This consultation ensured that no coordination of commercial policy could occur, and no competition-sensitive information could be exchanged between the NLFI’s holdings. The consultation also resulted in restrictions on the appointment of NLFI board members and the designation of an observer to monitor the NLFI (EC 2013b; NLFI 2014).

NLFI has issued advisory reports to the Ministry of Finance regarding options to reprivatize various parts of SNS Reaal, as well as annual reports. The minister of finance reported to the Dutch Parliament and the EC regarding SNS Reaal’s restructuring (Minister of Finance 2013a; NLFI 2014; NLFI 2015c; NLFI 2015d; NLFI 2016b).

The DNB and Ministry of Finance jointly commissioned an independent body to evaluate the nationalization. The central question of the evaluation was whether the DNB and Ministry of Finance acted in a timely and sufficient manner with regard to SNS Reaal. Among other conclusions, the report criticizes the minister of finance, stating that solutions to SNS Reaal’s problems should have started as early as 2009. However, the report characterizes the decision to nationalize SNS Reaal as “well defendable” though the authors note that complete information on the total costs was not yet available (Evaluation Committee 2014).

Communication

1

The minister of finance announced the state’s intent to recapitalize and restructure SNS Reaal in his statement announcing the nationalization of the institution. The minister also announced that the claims of shareholders and subordinated debt holders were being written off. Given the state’s previous provision of aid in 2008, the minister wanted to ensure that parties that had knowingly financed SNS Property Finance would be held accountable. Following the receipt of a large number of complaints from expropriated parties in SNS Reaal, the Dutch Council of State announced its decision in defense of the minister of finance’s right to expropriate shares and hybrid debt instruments on February 25, 2013. A letter from the minister of finance on March 4, 2013, communicated the list of expropriated parties and confirmed that expropriated shares and securities received no compensation (Council of State 2013b; Minister of Finance 2013b; Netherlands 2013).

In the nationalization announcement, the minister of finance stated his intention to return the various parts of SNS Reaal to the private sector as soon as market conditions allowed for it. NLFI played an important role in the communication of restructuring efforts, providing regular updates on the sale of Propertize and Reaal Insurance. NLFI sent letters to the minister of finance that served as advisory reports on the sale of both entities. NLFI press releases also announced the start of the sale period for Propertize on December 8, 2015, and the finalization of the sale on September 27, 2016 (Netherlands 2013; NLFI 2015b; NLFI 2015c; NLFI 2015d; NLFI 2016a). All NLFI publications were publicly available during the restructuring periodFIndependently verified by author using the Internet Archive’s “Wayback Machine” (https://web.archive.org)..

Source and Size of Funding

1

The Dutch state funded the restructuring process using public money and offsetting the costs by expropriating shareholders and hybrid debt holders. The minister of finance anticipated EUR 3.7 billion in direct costs to the state, and the restructuring plan placed the approximate nominal cost at EUR 5 billion. This total comprised the capital injections, the bridge loan, the write-off of the remaining balance of the 2008 State Aid, and the transfer and capitalization of the property finance “bad bank.” The aggregated value of the expropriated instruments totaled EUR 1.84 billion. A June 2014 EC recording of transactions stated that the total loss assigned to the EUR 2.2 billion capital injection from expropriated securities was EUR 1.13 billion. The remaining EUR 1.07 billion was recorded as an acquisition of equity by the government, with no impact on the government deficit (EC 2013b; EC 2014; Minister of Finance 2013a).

The minister of finance also levied a one-time resolution tax on the banking sector, contributing EUR 1 billion toward the intervention measures. This tax spread a portion of the costs of the intervention across the banking sector in a fashion similar to the wave of losses that would have occurred if SNS Bank had failed (Minister of Finance 2013a).

Upon isolating SNS Property Finance from SNS Reaal, SNS Bank realized a EUR 725 million loss, which corresponded to the amount of Property Finance’s shareholders’ equity. At the time of the transfer, SNS Property Finance also owed EUR 4.5 billion to SNS Bank. The state provided EUR 500 million of capital to Property Finance, of which EUR 400 million was used to lower the outstanding debt to EUR 4.1 billion (SNS Bank 2014).

In the spring of 2023, the Dutch court system required the Dutch state to pay EUR 805 million in compensation to certain expropriated creditors (see Key Design Decision No. 9, Treatment of Creditors and Equity Holders) (Netherlands n.d.a).

Approach to Resolution and Restructuring

1

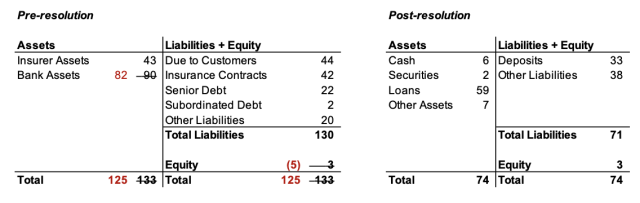

The two major goals of the restructuring effort were: (a) spinning off Property Finance into a “bad bank” and (b) divesting the Reaal insurance subsidiary. Throughout 2012, the minister of finance and DNB considered several other options to restructure SNS Reaal. A solution in which the three other systemically important banks participated in the bank or holding company proved impossible without a guarantee. The individual sale of the insurance subsidiary would not provide enough relief on its own, and a private solution did not materialize for SNS Bank. The final hope was a private equity solution, which proved unviable on January 31, 2013. Seeing no other options, the minister of finance nationalized SNS Reaal on February 1, 2013 (EC 2013b; FSB 2014; Minister of Finance 2013a). The balance sheet before and after resolution is shown in Figure 2.

Figure 2: SNS Reaal Pro Forma Balance Sheets (EUR billions)

Note: Pre-resolution balance sheet illustrates the EUR 8 billion Property Finance unit write-down.

Source: SNS Bank 2014.

Property Finance Spin-off

The minister of finance saw the spinning off of the Property Finance division as essential to restoring viability to SNS Bank. The Property Finance spin-off facilitated liquidity access for SNS Bank, and the divestment of Reaal Insurance removed the double leverage on the balance sheet of SNS Reaal. The restructuring plan submitted to the EC stated that this action shrunk the balance sheet of the overall conglomerate by 6% and decreased the risk weighted assets (RWAs) by 30%. As such, the spin-off would stimulate access to liquidity via private funding for SNS Bank. The minister of finance set the transfer value of Property Finance, writing off EUR 2.8 billion on the total assets as of June 30, 2012. These write-offs loosely adhered with a valuation given by Cushman & Wakefield, an advisor of the Dutch state that accounted for potential losses in Property Finance during the 2012 SREP. The C&W valuation estimated that the Property Finance portfolio was worth no more than EUR 5 billion, and a news report stated that the estimated value of the portfolio was EUR 4.8 billion (EC 2013b; Minister of Finance 2013a; SeeNews Netherlands 2013; SNS Bank 2014). The minister of finance based the transfer to the “bad bank” on this valuation. On December 31, 2013, the Dutch state paid a transfer price above market value, transferring the Property Finance shares for a symbolic EUR 1. The state then immediately transferred the 50,003 shares, each with a nominal value of EUR 50, to NL Financial Investments. As per the restructuring plan submitted to the EC, this amounted to an additional EUR 859 million in State Aid, defined as the difference between the transfer price and the market price. The NLFI rebranded the bad bank as Propertize on January 1, 2014. SNS Bank realized a EUR 725 million loss at the time of the transfer, corresponding to the equity of SNS Property Finance. SNS Bank also initially funded Propertize, with a state guarantee of EUR 4.1 billion. NLFI instructed the management of Propertize to decrease its portfolio of mortgages and property in order to minimize risk (EC 2013b; Minister of Finance 2013a; NLFI 2014; NLFI 2015d; SNS Bank 2014). The structure of SNS Reaal following the spin-off is shown in Figure 3.

Figure 3: Structure of SNS Reaal before and after Intervention

Source: Author’s analysis of Financial Stability Board (2014, 50).

Divestment of Reaal Insurance

The restructuring plan also indicated that the divestment of Reaal Insurance was the solution to the problem of double leverage. The insurance division was rebranded as VIVAT Verzekeringen on July 1, 2014, as part of this process of separation. Upon divesting the insurance from the banking division, authorities announced that the overarching holding company, SRH N.V, would cease operations. As such, the entity that existed in the aftermath of the restructuring was a stand-alone retail bank (formerly SNS Bank). The state officially split SNS Bank from SNS Reaal on September 30, 2015, transferring the shareholding responsibilities to NLFI. For the purposes of exercising shareholder powers, the state created a holding company called SNS Holding B.V., which owned all the shares. NLFI managed 100% of the share capital and exercised full voting rights in this entity. The restructuring plan made the Dutch state’s intention to reprivatize the bank explicitly clear (EC 2013b; NLFI 2015a; NLFI 2016b; VIVAT Verzekeringen 2015).

In pursuit of the goal of divesting Reaal insurance, the minister of finance instructed NLFI to execute the sale of the insurance subsidiary on June 6, 2014. On February 15, 2015, NLFI submitted an advisory report to the minister of finance regarding the sale of the insurance division of Reaal. In the report, NLFI indicated that it issued invitations to 86 parties and received two nonbinding offers, one from ASR on October 20, 2014, and the other from Anbang Group Holdings on December 18, 2014. NLFI admitted both to the due diligence phase and established a deadline of the end of January 2015 for submission of a binding offer. Anbang submitted a binding offer on January 30, 2015. Anbang committed to repaying three internal loans totaling EUR 552 million as well as a 140%–150% recapitalization, which NLFI estimated to cost between EUR 770 million and EUR 1 billion. NLFI made a positive recommendation of the offer in its report, subject to the approval of the supervisory authorities of both the Netherlands and China. Sources differ on the purchase price, with European outlets reporting a sale in the range of EUR 85 million to EUR 150 million and Chinese sources stating that Anbang paid a symbolic EUR 1 alongside a capital investment. NLFI reported that the Dutch state did not recoup any funds from the sale of VIVAT (NLFI 2015c; NLFI 2015d; SNS Reaal 2015; Ti 2016).

Treatment of Creditors and Equity Holders

1

In his letter to parliament announcing the intervention measures, the minister of finance stated his clear intention to hold private parties accountable for the costs of restructuring the operations of SNS Reaal. As such, the minister of finance used the power granted to him by the Intervention Act to expropriate the shareholders and subordinated debt holders of SNS Reaal and SNS Bank (Minister of Finance 2013a; Minister of Finance 2013b).

The expropriated parties included all shareholders and a variety of hybrid debt holders in SNS Reaal. As such, the expropriated instruments included: (i) all shares issued by SNS Reaal or SNS Bank, (ii) all SNS Reaal core Tier 1 capital securities, (iii) all subordinated bonds issued by SNS Reaal or SNS Bank, (iv) all loans contracted by SNS Reaal or SNS Bank (Minister of Finance 2013b).

The minister of finance and DNB notably decided against expropriating senior debt holders despite having the right to do so. The minister’s position was that the increased risk would lead to senior bondholders demanding higher interest rates on their bonds. This fear was legitimated by the threat that rating agency Fitch would downgrade Dutch banks if it appeared that senior bondholders could be forced to take losses on their bonds. The minister viewed this as unacceptable for the stability of the Dutch banking sector (FSB 2014; Haentjens 2013).

Included in the expropriated securities were third series participation certificates with SNS Bank totaling EUR 57 million. The minister of finance requested an investigation into the sale of the certificates to retail clients. Following this investigation, SNS Bank made a proposal to the clients in question on July 11, 2013, which 97% accepted, resulting in payouts over the course of the year totaling EUR 51.3 million (EC 2013a; SNS Bank 2014).

On February 11, 2021, a Dutch court ruled that the Dutch state needed to provide compensation to certain subordinated creditors whose claims were expropriated. The Dutch Supreme Court ratified the decision on April 21, 2023, and the Dutch state commenced a compensation scheme. The state was required to pay an overall sum of EUR 805 million; the compensation breakdown is detailed in Appendix B (Netherlands n.d.a; Netherlands n.d.b).

Treatment of Clients

1

The Dutch intervention measures safeguarded the claims of all depositors in SNS Bank. Article 3:267f of the Intervention Act states that any contractual early termination rights cannot be exercised without receiving permission from the DNB (Minister of Finance 2013a; Netherlands 2012).

Treatment of Assets

1

The state transferred SNS Property Finance to NLFI on December 31, 2013. On January 1, 2014, NLFI altered the articles of association to change the name to Propertize. NLFI stated that the purpose of Propertize was to downsize the portfolio of property and property financing over the ensuing 10 years. This would optimize revenue while lowering risks and costs (NLFI 2014).

Treatment of Board and Management

1

In the nationalization announcement, the minister of finance also stated that the chief executive officer (CEO) and chief financial officer (CFO) of SNS Reaal had stepped down. The minister announced their replacements on the same day. Gerard van Olphen became the new CEO, leaving the chief financial risk officer (CFRO) position at Achmea, the largest insurer in the Netherlands. Maurice Oostendorp became the CFRO, leaving a CFO position at VGZFCareer information found through LinkedIn.. The chair of the supervisory board also resigned, and the minister of finance stated that the deputy chair would assume the duties of the chair (EuropaWire 2013; Netherlands 2013).

An investigation initiated in 2012 and continued in 2013 also found evidence of irregularities at SNS Property Finance. This resulted in the termination of 18 external employees hired by Property Finance, including a former director and multiple members of the management team (SNS Bank 2014).

Cross-Border Cooperation

1

The Dutch government communicated with EC authorities to receive approval for the restructuring plan (see Key Design Decision No. 3, Legal Authority) (EC 2013b).

Other Conditions

1

Upon becoming the sole shareholder of SNS Reaal, the Dutch state made several commitments to the EC on behalf of the firm. SNS Reaal committed to not take a stake in any acquisitions, refrain from making payments on hybrid debt instruments, and refrain from advertising its state ownership. The Dutch state agreed to comply with EU remuneration rules to ensure a suitably high rate of interest on the bridge loan such that SNS Reaal had a strong incentive to pay back the loan as soon as market circumstances allowed (see Key Design Decision No. 2, Part of a Package). They also agreed to notify the EC of any additional intervention measures and the intended restructuring plan for the firm (EC 2013a; EC 2013b). NLFI also required Propertize to significantly downsize the risk within its portfolio and stated that new risks “should be avoided as much as possible” (NLFI 2015d, 6).

As a condition of its approval, the EC stated that SNS Reaal had to “refrain from employing any aggressive commercial strategies which would not take place without the State support” (NLFI 2014). NLFI was responsible for preventing any anticompetitive practices in its management of different companies. NLFI committed to use its authority only to appoint supervisory board members at companies to ensure sufficient expertise and adequate composition. Pursuant to this aim, NLFI board members were barred from being members of management or supervisory boards at financial institutions or subsidiaries (NLFI 2014).

Duration

1

The European Commission formally approved the Dutch intervention measures on February 22, 2013. The EC granted Dutch authorities six months to submit a restructuring plan. The minister of finance referenced the possible creation of a broader restructuring plan for SNS Reaal in his February 1 letter to parliament concerning the nationalization. The DNB and the minister of finance intended to isolate the Property Finance division from SNS banking and resolve the issues caused by the firm’s double leverage by divesting the insurance division. The Dutch government submitted the plan on August 19, 2013, and the European Commission announced its approval on December 19, 2013 (EC 2013a; EC 2013b; Minister of Finance 2013a).

The advisory report written by NLFI in October 2015 stated that a sale of Propertize was potentially more beneficial than continued downsizing of its portfolio. As market conditions stabilized, customers became more able to refinance their agreements with other financial institutions. NLFI forbade Propertize from taking on new risk, which prevented the entity from offering refinancing prospects. NLFI also reported growing difficulties with employee retention. These two factors contributed to NLFI recommending the sale of Propertize in its advisory report. The minister of finance informed parliament of his intention to sell Propertize on October 16, 2015, and NLFI announced the start of the auction process on December 8, 2015. On September 27, 2016, NLFI announced the finalization of its sale of Propertize to a consortium led by Lone Star and JPMorgan for EUR 895.3 million (NLFI 2015b; NLFI 2015d; NLFI 2016a).

On June 6, 2014, the minister of finance instructed NLFI to execute the sales process for the insurance division of SNS Reaal, which was rebranded as VIVAT Verzekeringen. NLFI received a binding offer from Anbang Group Holdings on January 30, 2015. On February 15, 2015, NLFI sent an advisory report to the minister of finance detailing the terms of the offer. SNS Reaal announced the sale of VIVAT Verzekeringen on February 16, 2015 (NLFI 2015c; SNS Reaal 2015).

The restructuring plan submitted to the EC established December 31, 2017, as the end of the restructuring period. In his original letter to parliament, the minister of finance placed a mandate on SNS Reaal’s management to return the company to the private sector as soon as possible. On January 1, 2018, the stand-alone entity that resulted from the restructuring was rebranded as de Volksbank. NLFI periodically submits reports to the minister of finance and Dutch Parliament discussing steps and conditions for privatization. However, the state remains the sole shareholder in de Volksbank as of the writing of this case study (De Volksbank n.d.; EC 2013b; Minister of Finance 2013a).

Key Program Documents

-

(De Volksbank n.d.) De Volksbank. n.d. “De Volksbank’s History.” Accessed June 7, 2023.

Web page overview of the history of De Volksbank.

-

(Netherlands n.d.a) Kingdom of the Netherlands (Netherlands). n.d.a. “Compensation for the Expropriation of SNS REAAL and SNS Bank.” Accessed September 11, 2023.

Web page detailing the ex post compensation scheme for certain creditors expropriated during the restructuring of SNS Reaal.

-

(Netherlands n.d.b) Kingdom of the Netherlands (Netherlands). n.d.b. “Types of Compensation.” Accessed September 11, 2023.

Web page breaking down the different types of creditors that received compensation for their expropriated claims.

-

(EC 2013a) European Commission (EC). 2013a. “State Aid SA.35382–The Netherlands Rescue SNS REAAL 2013.” Letter from the European Commission to Dutch authorities, February 22, 2013.

Letter from the European Commission to Dutch authorities approving the rescue aid provided to SNS Reaal.

-

(EC 2014) European Commission (EC). 2014. “Recording of Transactions Relating to the Nationalization of SNS Reaal in Q1 and Q4 of 2013.” Letter from the EC to Dutch authorities, June 6, 2014.

Letter detailing the date and costs of intervention measures for SNS Reaal.

-

(Minister of Finance 2013a) Minister of Finance, Netherlands. 2013a. “Letter from Minister of Finance to the Chair of the Parliament Concerning the Nationalization of SNS REAAL.” Letter from Minister of Finance to the Parliament, February 1, 2013.

Letter to Parliament from the Dutch minister of finance detailing the nationalization of SNS Reaal and further intervention measures.

-

(Netherlands 2012) Kingdom of the Netherlands (Netherlands). 2012. Special Measures Financial Enterprises Act. February 14, 2012.

Law giving the minister of finance the power to expropriate shareholders and hybrid security holders (Unofficial Translation).

-

(Netherlands 2022) Kingdom of the Netherlands (Netherlands). 2022. NL Financial Investments Articles of Association. March 25, 2022.

Law establishing NL Financial Investments and outlining the body’s governance and responsibilities (Translated by the Kingdom of the Netherlands).

-

(EuropaWire 2013) EuropaWire. 2013. “Gerard van Olphen Leaves Achmea and Becomes CEO at SNS Reaal.” EuropaWire, February 1, 2013.

News article reporting on the new CEO of SNS Reaal.

-

(IR Global 2013) IR Global. 2013. “The Dutch Interventiewet (Intervention Act).” IR Global, February 7, 2013.

Overview of the Dutch Intervention Act and the new powers it created.

-

(Minister of Finance 2013b) Minister of Finance, Netherlands. 2013b. “Letter from Regarding the Offer for Compensation with Respect to Expropriation of Securities and Capital Components of SNS Reaal and SNS Bank, March 4, 2013,” March 4, 2013.

Letter confirming that expropriated parties of SNS Reaal would not receive compensation (Dutch and unofficial English translation).

-

(Mondaq 2011) Mondaq. 2011. “Netherlands: Intervention Act.” Mondaq, April 26, 2011.

Overview of the passage of the Dutch Intervention Act and its implications.

-

(SeeNews Netherlands 2013) SeeNews Netherlands. 2013. “SNS Reaal Transfers Property Unit to Dutch State.” SeeNews Netherlands, December 31, 2013.

News article reporting the transfer of SNS Property Finance to the Dutch state.

-

(Ti 2016) Ti, Zhuan. 2016. “Anbang Turns Vivat a Profit-Maker.” China Daily, September 19, 2016.

News article discussing sale of VIVAT Verzekeringen to Anbang Insurance Group and its return to profitability.

-

(van Tartwijk 2013) van Tartwijk, Maarten. 2013. “Netherlands Nationalizes SNS Reaal.” The Wall Street Journal Asia, February 4, 2013.

News article discussing the nationalization of SNS Reaal.

-

(Council of State 2013a) Council of State, Netherlands. 2013a. “Court Hearing for the Decree to Expropriate SNS Reaal.” Press release, February 12, 2013.

Press release announcing the court date when the Council of State was to hear appeals against the expropriation of SNS Reaal (in Dutch).

-

(Council of State 2013b) Council of State. 2013b. “Minister of Finance Was Entitled to Expropriate SNS Securities and Loans, but Not Future Claims.” Press release, February 25, 2013.

Press release announcing the Council of State’s decision regarding complaints filed against the expropriation of SNS Reaal security holders.

-

(NLFI 2015a) NL Financial Investments (NLFI). 2015a. “NLFI Becomes Sole Shareholder of SNS Holding B.V.” Press release, October 1, 2015.

Press release announcing the transfer of SNS Holding BV shares to NLFI.

-

(NLFI 2015b) NL Financial Investments (NLFI). 2015b. “Start Sale Process of Propertize B.V.” Press release, December 8, 2015.

Press release announcing the start of the auction process for Propertize.

-

(NLFI 2016a) NL Financial Investments (NLFI). 2016a. “Sale of Propertize B.V. Finalized.” Press release, September 27, 2016.

Press release announcing the finalization of the sale of Propertize.

-

(SNS Reaal 2015) SNS Reaal. 2015. “SNS Reaal Announces Sale [of] VIVAT Verzekeringen to Anbang Insurance Group.” Press release, February 16, 2015.

Press release announcing the sale of VIVAT Verzekeringen to a Chinese insurance firm.

-

(Evaluation Committee 2014) Hoekstra, Rein Jan, and Jean Frijns. 2014. “The Report of the Evaluation Committee on the Nationalization of SNS Reaal.” Report commissioned by Dutch National Bank and the Ministry of Finance, January 23, 2014.

Unofficial translation of the evaluation committee report on the nationalization of SNS Reaal.

-

(FSB 2014) Financial Stability Board (FSB). 2014. “Peer Review of the Netherlands.” Review Report, November 11, 2014.

A review of the Netherlands’ resolution framework by the Financial Stability Board.

-

(Morrison and Phillips 2014) Morrison, Scott, and Stephen Phillips. 2014. “The Nationalisation of SNS – Lessons Learnt.” Reg Cap Analytics, October 14, 2014.

Report summarizing the nationalization of SNS Reaal and identifying areas of improvement.

-

(NLFI 2014) NL Financial Investments (NLFI). 2014. 2013 Annual Report.

Annual report of the 2013 activities conducted by NLFI.

-

(NLFI 2015c) NL Financial Investments (NLFI). 2015c. “Advisory Report on the Conditional Sale of REAAL N.V. to Anbang Insurance Group Co. Limited.” Report No. 2015/58, February 15, 2015.

Advisory report submitted to the minister of finance regarding the sale of Reaal Insurance.

-

(NLFI 2015d) NL Financial Investments (NLFI). 2015d. “Advice for the Sale of Propertize,” October 16, 2015.

Advisory report submitted to the minister of finance concerning the future of Propertize (Translated by the NLFI).

-

(NLFI 2016b) NL Financial Investments (NLFI). 2016b. “Advisory Report on the Future Direction of SNS Bank,” June 2016.

Advisory report on the opportunities to reprivatize SNS Bank.

-

(SNS Bank 2014) SNS Bank. 2014. 2013 Annual Report.

Annual report for SNS Bank for 2013.

-

(VIVAT Verzekeringen 2015) VIVAT Verzekeringen. 2015. 2014 Annual Report REAAL NV.

Annual report of Reaal Insurance for 2014.

-

(Haentjens 2013) Haentjens, Matthias. 2013. “What Happens When a Systemically Important Financial Institution Fails: Some Company Law Observations Re. SNS Reaal.” European Company Law 10, no. 2 (June): 70–74.

Article discussing the Dutch intervention measures for SNS Reaal in 2013.

-

(George, forthcoming) George, Ayodeji. forthcoming. “Netherlands: SNS Reaal Capital Injection, 2008.” Journal of Financial Crises, forthcoming.

YPFS case study examining the ad hoc capital injection provided to SNS Reaal in 2008.

-

(McNamara et al. 2024) McNamara, Christian M., Carey K. Mott, Salil Gupta, Greg Feldberg, and Andrew Metrick. 2024. “Survey of Resolution and Restructuring in Europe, Pre- and Post-BRRD.” Journal of Financial Crises 6, no. 1.

Survey of YPFS case studies examining 21st-century bank resolutions and restructurings in Europe before and after the existence of the Bank Recovery and Resolution Directive.

-

(World Bank 2016) World Bank. 2016. “Bank Resolution and ‘Bail-In’ in the EU: Selected Case Studies Pre and Post BBRD.” Financial Sector Advisory Center, December 12, 2016.

Collection of World Bank case studies about bail-in measures taken in European countries.

-

(EC 2013b) European Commission (EC). 2013b. “State Aid SA.36598 (2013/N) - the Netherlands—Restructuring Plan SNS Reaal 2013.” Letter from the EC to the Netherlands, December 19, 2013.

Letter from the European Commission to Dutch authorities approving their restructuring plan for SNS Reaal.

-

(Netherlands 2013) Kingdom of the Netherlands (Netherlands). 2013. “Statement by Minister Jeroen Dijsselbloem,” February 1, 2013.

Statement by the minister of finance explaining the nationalization of SNS Reaal.

Appendix A: Special Measures Financial Enterprises Act

The Special Measures Financial Enterprises Act (Intervention Act) amended the existing Financial Supervision Act and the Bankruptcy Act, as well as any other laws that were connected with the new powers being granted (Netherlands 2012). Prior to the Intervention Act, the Dutch supervisory framework emphasized prevention (Mondaq 2011). The Global Financial Crisis exposed the insufficiency of the existing framework to respond to institutions that already had major problems (Mondaq 2011). The existing tools focused on an institution’s imminent bankruptcy but did not provide the government with the means to resolve the institution without resorting to bankruptcy (Mondaq 2011).

The Dutch Parliament passed the Intervention Act on February 14, 2012, granting the law a retroactive entry into force date of January 20, 2012 (Netherlands 2012). The passage of the Intervention Act granted new intervention powers to the minister of finance and the Dutch National Bank (DNB) (IR Global 2013). The act grants the minister of finance resolution powers in situations where there is an imminent threat to financial stability. The minister of finance determines “threats to stability” in consultation with the DNB and with the agreement of the prime minister. In these instances, the minister of finance’s major powers are twofold:

- Direct intervention into the institution’s internal management; and

- Expropriation of assets, liabilities, or securities issued by the institution.

The Intervention Act establishes the DNB as the resolution authority for financial institutions that are failing or likely to fail. Using a “transfer order”, the DNB holds the power to execute the following;

- Selling a troubled institution to a private buyer via transfer of shares;

- Transfer of deposits from a troubled institution to private party, with funding from the deposit guarantee scheme (DGS); and

- The transfer of a troubled institution’s assets and liabilities to a private party, allowing the institution to be split into a “good bank” and a “bad bank.”

Before executing any of its powers, the Intervention Act requires the DNB to receive approval of its transfer order from the Amsterdam District Court. The exercise of both bodies’ respective powers are subject to the no creditor worse off than in liquidation (NCWOL) principle.

Appendix B

Figure 4: Types of Compensation 2023

Source: Netherlands n.d.b.

Taxonomy

Intervention Categories:

- Resolution and Restructuring in Europe: Pre- and Post-BRRD

Countries and Regions:

- Netherlands

Crises:

- European Soverign Debt Crisis