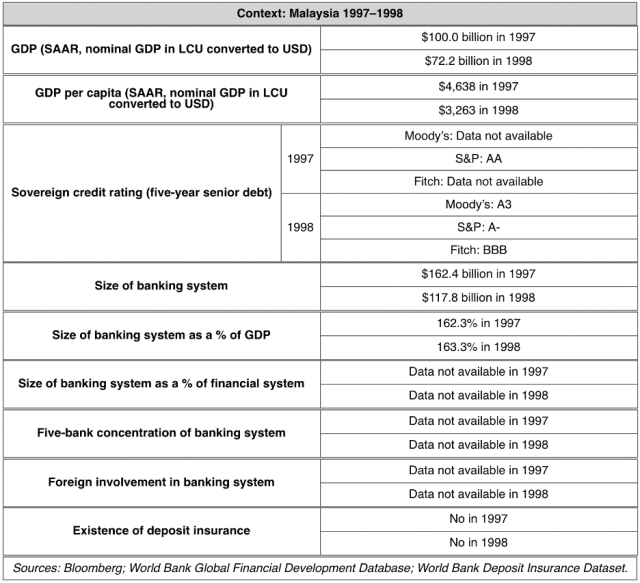

Reserve Requirements

Malaysia: Reserve Requirements, AFC

Purpose

During monetary tightening, to “enhance the efficiency of the intermediation process and not to provide additional liquidity to the system” (BNM 1998a); during monetary easing, to “ease liquidity in the banking system” (BNM 1998h)

Key Terms

-

Range of RR Ratio (RRR) Peak-to-Trough13.5%–4% of eligible liabilities

-

RRR Increase PeriodPre-crisis (set at 13.5% on June 1, 1996)

-

RRR Decrease PeriodFebruary 1998 – September 1998

-

Legal AuthorityCentral Bank of Malaysia Act 1958 (Revised—1994) and Banking and Financial Institutions Act 1989

-

Interest/Remuneration on ReservesUnremunerated

-

Notable FeaturesBNM first cut the SRR during monetary tightening but cut the SRR further as it switched to monetary easing; Malaysia concurrently replaced a longstanding liquid asset requirement with a liquidity management framework

-

OutcomesMYR 22 billion (USD 5.8 billion) injected into the banking system with the initial cuts, offset by decreased direct lending to the interbank market; MYR 15 billion injected with the later cuts

Key Design Decisions

Purpose

Part of a Package

Administration

Governance

Communication

Assets Qualifying as Reserves

Reservable Liabilities

Computation

Eligible Institutions

Timing

Changes in Reserve Requirements

Sources: BNM 1998a; BNM 1998d; BNM 1998e; BNM 1998h; BNM 1998j.

Sources: BNM 1998a; BNM 1998d; BNM 1998e; BNM 1998h; BNM 1998j.

Changes in Interest/Remuneration

Other Restrictions

Impact on Monetary Policy Transmission

Duration

Key Program Documents

Taxonomy

Intervention Categories:

- Reserve Requirements

Countries and Regions:

- Malaysia

Crises:

- Asian Financial Crisis 1997