Broad-Based Capital Injections

Malaysia: Danamodal Nasional Berhad (Danamodal)

Purpose

To recapitalize and strengthen the Malaysian banking industry, while acting as an active shareholder and Board representative to instigate mergers and revamp corporate governance among beneficiaries

Key Terms

-

Announcement DateJuly 13, 1998

-

Operational DateAugust 10, 1998

-

Wind-down DatesDecember 31, 2003

-

Program SizeRM16 billion authorized

-

Peak UtilizationRM7.59 billion by 10 institutions

-

OutcomesRisk-weighted capital ratio (RWCR) for beneficiaries increased from 9.9% in September 1998 to 12.3% by the end of December 1999

-

Notable FeaturesInjections were initially in the form of Exchangeable Subordinated Capital Loans and then were converted to other types of capital after further due diligence; part of a coordinated government package to address the financial crisis.

The Malaysian economy was relatively well positioned at the beginning of the Asian Financial Crisis. However, the government’s response of tight fiscal and monetary policy, along with contagion from surrounding countries, had severe negative consequences. The banking industry became particularly vulnerable due to substantial loan growth preceding the crisis and exposure to volatile sectors, leading to an increase in NPLs and capital deterioration. As part of its approach to assist the ailing banking sector, the Bank Negara Malaysia created Danamodal Nasional Berhad (Danamodal) on August 10, 1998, as a wholly owned subsidiary aimed at recapitalizing banking institutions. Funding for Danamodal came from RM3 billion in central bank seed capital and RM7.7 billion of five-year zero-coupon bonds. Beneficiaries submitted a recapitalization strategy to Danamodal, which performed assessments in conjunction with external advisors to determine the viability of the institution and required injection amounts. The first phase of injections consisted of interim Tier 2 Capital; beneficiaries then negotiated and signed Definitive Agreements that converted the temporary capital into various types of permanent capital and outlined a long-term relationship with Danamodal. Danamodal appointed two nominees to the beneficiary’s board of directors with additional appointments dependent on the amount of Tier 1 capital injected. Through its Board presence, Danamodal facilitated mergers and implemented behavioral reforms. Injections through Danamodal totaled approximately RM7.6 billion into 10 banking institutions and all funds were repaid by 2007 resulting in a final pre-tax profit of RM200 million.

|

Malaysia Context 1997–1998 |

|

|

GDP (SAAR, Nominal GDP in LCU |

$101.4 billion in 1997 |

|

GDP per capita (SAAR, Nominal GDP in LCU |

$4,638 in 1997 $3,263 in 1998 |

|

Sovereign credit rating

|

Data not available for 1997 |

|

Size of banking system

|

$137.9 billion in 1997 |

|

Size of banking system |

100% in 1997 |

|

Size of banking system |

100% in 1997 100% in 1998 |

|

Five-bank concentration of banking system |

64.8% in 1997 61.5% in 1998 |

|

Foreign involvement in banking system |

18% in 2001 |

|

Government ownership of banking system |

0% in 2001 |

|

Existence of deposit insurance |

Yes in 2008 Yes in 2009 |

|

Sources: Bloomberg; World Bank Global Financial Development Database; World Bank Deposit Insurance Dataset; Cull, Martinez Peria, and Verrier 2018. |

As the Asian Financial Crisis began spilling over into the Malaysian economy, its banking industry quickly began to struggle. Substantial loan growth preceding the crisis and exposure to volatile sectors had led to an increase in non-performing loans (NPLs) and deterioration of capital. As part of a larger plan, on August 10, 1998 the Bank Negara Malaysia (BNM) created Danamodal Nasional Berhad (Danamodal), a wholly owned subsidiary aimed at recapitalizing banking institutions. The BNM funded this Special Purpose Vehicle (SPV) with RM3 billion in BNM seed capital and RM7.7 billion of five-year zero-coupon bonds.

Danamodal, along with international advisors, reviewed submissions and performed analyses on banking institutions to determine their viability and required injection amounts. Initially, Danamodal injected Exchangeable Subordinated Capital Loans (ESCL), a form of Tier 2 Capital, as a temporary injection to allow for further due diligence and negotiation. During this interim period, beneficiaries signed Definitive Agreements that converted ESCL into permanent capital and outlined a long-term relationship with Danamodal. The three primary forms of permanent capital included Common Shares, Irredeemable Non-Cumulative Convertible Preference Shares (INCEPS), and Subordinated Loans. The different instruments provided a range of expected returns, control, and subordination. Following the injection of capital, Danamodal appointed nominees to the beneficiary’s Board of Directors based on the amount of Tier 1 Capital injected. Through its Board presence, Danamodal facilitated mergers and implemented behavioral reforms. In addition, Danamodal worked with beneficiaries to create performance targets and closely monitored their progress. Over its lifetime, Danamodal injected approximately RM7.6 billion into 10 banking institutions, resulting in an increase of risk-weighted capital ratio (RWCR) for beneficiaries from 9.9% at end of September 1998 to 12.3% at end of December 1999.

All beneficiaries exited the scheme by 2007 resulting in a final pre-tax profit of RM200 million. Although Danamodal has been credited as an essential part of the banking industry’s recovery from the Asian Financial Crisis, the IMF raised issues regarding its strategy to spur lending and enhance beneficiaries’ leadership and corporate governance.

Key Design Decisions

Part of a Package

1

The Malaysian government instituted a three-pronged approach to assist its ailing banking sector during the AFC. The three interventions dealt with purchasing Non-Performing Loans (NPLs), recapitalization, and debt restructuring. It included:

- Pengurusan Danaharta Nasional Berhad (Danaharta): an asset management company that purchased and managed NPLs from banking institutions;

- Danamodal Nasional Berhad (Danamodal): a special purpose vehicle (SPV) that injected capital into banking institutions;

- Corporate Debt Restructuring Committee (CDRC): a debt restructuring agency that allowed borrowers and creditors to negotiate agreements and avoid legal proceedings (BNM 1998a).

Each individual program interacted with one another in various ways. For example, banks sold their NPLs to Danaharta at fair market value, resulting in substantial losses. In a healthy economic environment, these banks would be able to raise capital to make up for this shortfall through shareholders. However, due to uncertain financial conditions, there was insufficient appetite from investors. Therefore, Danamodal stepped in to recapitalize these institutions and restore capital levels. In fact, Danamodal required beneficiaries to sell their NPLs to Danaharta in order to receive capital injections, resulting in existing shareholders bearing the losses associated with these sales. Additionally, if negotiations undertaken by the CDRC could not reach a consensus, Danaharta purchased the NPLs from the dissenting institutions, which assisted the restructuring process (BNM 1998a).

Due to the overlap between programs, shown in Figure 3, the Malaysian government created a Steering Committee that coordinated the interventions of Danaharta, Danamodal, and CDRC. The Governor of the BNM chaired the Steering Committee, which met every two weeks. Its primary responsibilities included ensuring “operations of these institutions are well coordinated and complement each other, and to keep track of their progress” as well as properly sequencing interventions (BNM 1998a).

Figure 3: Malaysia’s Multi-Pronged Approach

Source: Author’s analysis based on BNM 1998a.

Source: Author’s analysis based on BNM 1998a.

Legal Authority

1

Danamodal was legally categorized as a limited liability company and incorporated on August 10, 1998 as a wholly owned subsidiary of BNM (BNM 1998a; Danamodal 1998a). Its governance structure reflected this ownership as its board of directors had BNM representatives as Chairman, Managing Director, and other additional members. The board also consisted of a nominee from the Ministry of Finance and private sector appointees (Danamodal 1998a).

Communication

1

On July 13, 1998, BNM announced the creation of an SPV to recapitalize the banking system. The press release occurred two months after the creation of Danaharta and it references the SPV as a complement to it; “as Danaharta was set up to help remove NPLs from the banking system, there is a need for us to explore other pre-emptive alternatives to recapitalise the banking system.” The approach to recapitalization included a dual objective:

- To inject government capital, both in “core” banking institutions and in weaker institutions that BNM identified as viable;

- To merge core and weaker banking institutions, taking advantage of its role as a strategic shareholder (BNM 1998b).

The press release outlined a number of characteristics of the SPV including structure, lifespan, financing requirements, and operation and financing arrangements. It explains that the SPV would receive seed capital from BNM, with additional funding through bond issuances, and have a finite lifespan with the goal of selling its holdings once it achieved its objectives. The maximum expected budget was RM16 billion, which would maintain a risk-weighted capital ratio (RWCR) above 9% across the banking system. In addition, BNM would leverage international consultants to construct the operating details and financing arrangements of the SPV (BNM 1998b).

Danamodal was transparent in disclosing changes in management, operations, and selection criteria. A significant number of these announcements occurred through press releases. It also issued financial statements that aligned with international accounting standards (BNM 1998a). Deloitte Touche Tomatsu, an independent and external vendor, audited these annual financial statements.

Capital Characteristics

2

Under the “first-loss” principle, “existing shareholders were required to bear all losses prior to recapitalization.” In practice, the application of this principle required banks to mark down the value of existing shareholders investments to accurately reveal net tangible assets and sell their NPLs to Danaharta prior to receiving capital injections from Danamodal. This forced shareholders to realize the losses stemming from declining investments and NPL sales. In addition, it resulted in “equitable burden sharing” and reduced the use of public funds (BNM 1998a).

The “first-loss” principle also played an integral role in the negotiation of Definitive Agreements (DAs), which specified the terms and types of capital used in capital injections (Danamodal 1999a).

Danamodal would first inject Tier 2 subordinated debt, in the form of Exchangeable Subordinated Capital Loans (ESCL), which was converted into equity, debt, or hybrid capital through Definitive Agreements (DAs) (BNM 1998a; IMF 1999). ESCL bore an interest of 7.5% annually and had a three-month maturity, with the option for beneficiaries to extend. The temporary funds allowed for additional due diligence and negotiations prior to conversion (Danamodal 1999a).

Following this interim period, stakeholders signed DAs that outlined recapitalization amount and instruments used (including the decision whether to convert the ESCL into permanent Tier 1 and/or Tier 2 capital), pricing of instruments, investment protection, exit option, shareholder’s call option (Danamodal n.d.a). It is important to note that Danamodal used market-based valuation methods in making investment decisions (Danamodal n.d.b). The DAs varied across institutions due to the unique situation of each individual beneficiary, and time constraints required an accommodating and practical approach. Six main principles guided Danamodal’s structuring of investments: safety (application of first-loss principle), control, return, capital base, exit potential, and monitoring requirements (Danamodal n.d.a).

The three primary instruments used for capital injections by Danamodal and their characteristics are outlined in Figure 6. The different instruments allowed Danamodal to tailor injections to the issues faced by the at-risk institution. The composition of the capital injection depended “primarily on the cash flow characteristics of the instruments and the unique circumstances of the banking institutions concerned” (BNM 1998a).

Figure 6: Characteristics of Capital Used by Danamodal

Sources: Danamodal Nasional Berhad n.d.a; Danamodal 1998a, BNM 1998a.

Sources: Danamodal Nasional Berhad n.d.a; Danamodal 1998a, BNM 1998a.

Program Size

1

The worst-case scenario estimated by BNM dictated a budget of RM16 billion. This funding amount would guarantee that the RWCR across all banking institutions would be at least 9% (BNM 1998a). To estimate a maximum budget the BNM conducted a preliminary, industry-wide stress test in May 1998 that examined how banking institutions performed based on a variety of parameters and assumptions. The analysis looked at institution-specific characteristics such as projected NPLs, specific provisions (property and shares), investments, and off-balance-sheet items. In addition, it included environmental factors such as interest rates (three-month Kuala Lumpur Interbank Offered Rate or KLIBOR), foreign exchange (USD/MYR exchange rate), real estate (property prices), equity markets (Kuala Lumpur Composite Index), and contagion risk from exposure to Indonesia, Thailand, Korea (Danamodal n.d.a).

The results of the stress test, shown in Figure 4, prescribed a maximum funding requirement of RM16 billion, approximately 12% of Malaysia GDP. This was broken down into two phases; the first phase would recapitalize 14 banking institutions that the BNM deemed very likely to experience solvency issues and required a total of RM12.8 billion to bolster their RWCR to greater than 9%. The second phase involved 11 institutions that the BNM felt had a lower likelihood of experiencing solvency issues. Therefore, the BNM allocated RM1.6 billion to ensure that the RWCR of these lower-risk institutions stayed above 9%. In addition, the BNM added a precautionary 10% buffer, totaling RM1.6 billion (Danamodal n.d.a). Only 10 of the 14 institutions identified in the phase-one analysis received injections, as “Bank Bumiputra Malaysia Berhad, Bank of Commerce Berhad, Perwira Affin Bank Berhad and Utama Merchant Bank Berhad…opted for their own solutions to address their capitalisation issues” (Danamodal 1999c). Improved market conditions made injections for the institutions associated with phase two unnecessary (IMF 1999).

Figure 4: Stress Test Results

Source: Danamodal n.d.a.

Source: Danamodal n.d.a.

Source of Injections

1

In order to fund itself, Danamodal received RM3 billion in seed capital from BNM (Danamodal n.d.a). It then raised an additional RM7.7 billion on October 21, 1998, through the issuance of zero-coupon bonds (Danamodal n.d.c). The BNM decreased its statutory reserve requirement from 6% to 4% in conjunction with this issuance (Cook 2008; IMF 1999). It also required banks to use the additional liquid capital from the lowered requirement to buy Danamodal bonds (Cook 2008). The bonds had a nominal value of RM11 billion, five-year maturity, yield to maturity (YTM) of 7.25%, and qualified as a class-one liquid asset with zero risk-weighting for capital requirements. Additionally, Danamodal had the ability to extend the duration of the bonds, either partially or fully, by a minimum of one year and maximum of five years. The new YTM, if Danamodal triggered the maturity extension, would equal the “sum of the average YTMs of Malaysian Government Securities (MGS) of similar or closest tenor to the extension period and 50 basis points (Danamodal n.d.c). Unlike Danaharta, Danamodal’s bonds did not carry an explicit government guarantee (BNM 1998a). However, the bonds carried an implied government guarantee since Danamodal was wholly owned by BNM (IMF 1999).

Initially, 57 banking institutions subscribed to the Danamodal bond issuance and future pricing and liquidity were determined by the secondary market for Malaysian government securities, where Danamodal’s bonds regularly traded (Danamodal n.d.a; IMF 1999). On October 21, 2003, Danamodal redeemed its bonds at maturity at a nominal value of RM11 billion (BNM 2003).

Governance

1

Danamodal leveraged the expertise of “reputable, international financial advisors,” Goldman Sachs and Salomon Smith Barney (BNM 1998a; Danamodal n.d.a). They were selected due to their ability to:

- Immediately provide highly trained resources, bridging the learning curve gap;

- Supplement Danamodal’s resources needed to meet performance expectations;

- Provide a third party objective and independent viewpoint;

- Provide expert advice skills and methodologies to ensure an effective recapitalization process (Danamodal n.d.a).

The advisors had a number of functions, such as performing assessments and due diligence reviews (BNM 1998a). These reviews were a prerequisite to receive funds and aimed to gauge the overall health of the beneficiary as well as determine the amount of capital required (BNM 1998a; IMF 1999). Other responsibilities included the construction of an operational infrastructure along with overall policies and procedures governing capital injections (Danamodal n.d.a).

Eligible Institutions

1

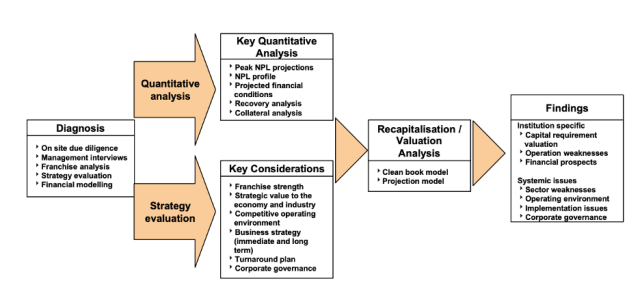

Along with BNM, Goldman Sachs, and Salomon Smith Barney, Danamodal worked to assess the long-term prospects for each institution (Danamodal n.d.b; IMF 1999). The selection process included an in-depth analysis of competitive position and financial standing of each banking institution, quantification of potential synergies to be realized through consolidation, and CAMEL (capital, assets, management, earnings, and liquidity) analysis (Danamodal 1998a). The banks that were selected as beneficiaries were identified in the first phase of stress tests and defined as very likely to experience solvency issues (Danamodal 1999c). The risk profiles of these banks were determined through the stress tests outlined in KDD 5 (Danamodal n.d.a). Of the original 14 banks identified in phase one, 10 received capital injections, while Bank Bumiputra, Bank of Commerce, Perwira Affin Bank, and Utama Merchant Bank secured alternative solutions (Danamodal 1999c). Bank Bumiputra Malaysia and Bank of Commerce were merged with government assistance outside of Danamodal; Perwira Affin Bank acquired BSN Commercial and did not require a further injection of capital; and Utama Merchant Bank was recapitalized by its shareholders. It is important to note that none of the banks identified as lower-risk institutions in the second phase received injections (IMF 1999).

Figure 5: Danamodal Recapitalization Assessment Process

Source: Danamodal n.d.a.

Source: Danamodal n.d.a.

Restructuring Plan

1

Danamodal appointed a minimum of two nominees to serve as Executive Director and either Chairman or Deputy Chairman on the Board of Directors of beneficiary institutions. The amount of Tier 1 Capital injected dictated additional Board representation beyond the minimum two appointees. Through its Board presence, Danamodal facilitated mergers and implemented behavioral reforms such as “sound risk management practices and credit culture, good corporate governance and higher operational efficiencies” (BNM 1998a).

The restructuring process employed by Danamodal encompassed improvements in financial analysis and capital frameworks, operations, IT, organizational structure, human resources, and the beneficiary’s business portfolio. The initial phase consisted of an internal and external situation assessment, followed by the development of a strategic plan (strategic position, operational design, IT design, etc.) and implementation plan (changes in restructuring, governance, consolidation, etc.) (Danamodal n.d.a).

Other Conditions

1

Prior to receiving capital injections, beneficiaries were required to provide a comprehensive business plan and establish, in conjunction with Danamodal, “a list of comprehensive performance targets, monthly reporting, and swift and firm remedial actions against the banks in the event of material shortfalls in performance relative to such targets” (Danamodal n.d.b). Danamodal closely monitored these performance targets, tightening its overall approach to banking supervision. This included requiring financial statement reporting to the BNM on a quarterly, semi-annual, and yearly basis, along with weekly and monthly balance sheet disclosure. The BNM also deployed CAMEL-based supervision, which focused on capital adequacy, asset quality, and management, regarding both in-person assessments, which were increased to a minimum of once per year for all banks, and external monitoring. Additional supervisory changes included BNM approval of financial statements prior to public disclosure and creation of “prompt corrective measures” which created pre-agreed responses by bank managers and owners to breaches of regulatory levels (IMF 1999).

Many of the indicators that were assessed are outlined in Figure 7.

Figure 7: Major Performance Indicators

Source: Danamodal n.d.a.

Source: Danamodal n.d.a.

Exit Strategy

1

At inception, BNM predicted that the recapitalization process would take no more than five years. This timeframe would allow Danamodal to accomplish its short and medium-term objectives and make significant headway towards the long-term goal of industry consolidation and restructuring (Danamodal n.d.a). It is important to note that Danamodal expected the majority of capital injections to occur during the first two years (Danamodal n.d.b). Danamodal’s exit strategy followed the below principles:

- Seize the earliest chance to exit;

- Achieve objectives of recapitalization or enhance prospects of future achievement;

- Aim for full recovery of investments;

- If the overall economic recovery helps to restore solvency issues among banking institutions, the need for Danamodal’s continued involvement may be reduced;

- Adhere to the overall policies views of the Malaysian government and BNM regarding the timing of the exit (Danamodal n.d.a).

On October 31, 2003, approximately five years after its creation, Danamodal closed its operations (BNM 2003). It exited the scheme through “initial public offering, strategic sales of its holdings, and sales of its holdings directly in the market” (Danamodal n.d.b).

BNM championed the success of the Danamodal program; it found that the speedy creation and implementation of the scheme was an essential part of the banking industry’s recovery from the AFC. The capital injections performed by Danamodal helped struggling but viable banking institutions raise capital and instill enhanced corporate governance (BNM 2003). This resulted in beneficiaries resuming lending activities and led to increased consumer confidence along with a revival of business and economic activities in the domestic real sector (BNM 2003; Danamodal n.d.a). In addition, BNM stated that Danamodal’s strict observance to the “first-loss” principle successfully minimized the total cost of recapitalization (BNM 2003). BNM felt the capital injections were performed “with a strong commercial orientation, focus on speed and outcomes, transparency in [Danamodal’s] policies and operations, sense of public accountability and credibility, and bias for hope and possibilities” (Danamodal n.d.a).

On the other hand, the IMF expressed concerns regarding Danamodal’s attempts to replace ineffective leadership with more capable alternatives. In particular, the IMF feared, even with new senior leadership, the potential for “inadequate, ineffective, or otherwise deficient management teams [to] remain.” This could lead to similar issues occurring in the future. Additionally, the IMF felt that the emphasis on loan growth by BNM and the interventions aimed at sparking growth had the potential to generate poor quality loans (IMF 1999).

Abidin (2000) credits the Malaysian government’s interventions as having “made serious efforts and registered good progress in restructuring its financial and corporate sectors,” specifically citing the success of Danaharta and Danamodal. These two programs were particularly effective “because they were executed efficiently, in a transparent manner and at a cost much lower than that incurred by the other crisis-hit countries” (Abidin 2000).

- Abidin, Mahani Zainal. 2000. “Malaysia’s alternative approach to crisis managem…

- Bank Negara Malaysia (BNM). 1997. “Bank Negara Malaysia Annual Report 1997.”

- ———. 1998a. “Bank Negara Malaysia Annual Report 1998.”

- ———. 1998b. “Recapitalisation and Consolidation of the Banking Sector.” July 13…

- ———. 1999. “Bank Negara Malaysia Annual Report 1999.”

- ———. 2000. “Consolidation of Domestic Banking Institutions.” February 14, 2000.

- ———. 2001a. “Bank Negara Malaysia Annual Report 2001.”

- ———. 2001b. “Best Practices for the Management of Credit Risk.” September 1, 20…

- ———. 2003. “Bank Negara Malaysia Annual Report 2003.”

- ———. 2007. “Financial Stability and Payment Systems Report.”

- Cook, Malcolm. 2008. Banking Reform in Southeast Asia: The region’s decisive de…

- Cull, Robert, Maria Soledad Martinez Peria, and Jeanne Verrier. 2018. “Bank Own…

- Danamodal Nasional Berhad (Danamodal). 1998a. “Details on Establishment of Dana…

- ———. 1998b. “Danamodal Plans to Inject RM1.5 billion into RHB Bank.” October 8,…

- ———. 1998c. “Danamodal to Inject RM50 billion into Perdana Merchant Bankers Ber…

- ———. 1998d. “Danamodal Concludes Capital Injection of RHB Bank Berhad and Buys …

- ———. 1998e. “Khazanah’s Interest in RHB Bank.” December 21, 1998.

- ———. 1999a. “Danamodal Nasional Berhad today signed Definitive Agreements with …

- ———. 1999b.“Danamodal Signs Definitive Agreement with Sabah Bank Berhad.” Febru…

- ———. 1999c.“Danamodal Injects RM1.6 billion into MBF Finance Berhad.” March 12,…

- ———. 1999d. “Danamodal Signs Definitive Agreements with Oriental Bank Berhad an…

- ———. 2000a. “Investments in Recapitalised BIs.” February 11, 2000.

- ———. 2000b. “Financial Statements for the Financial Year ended 31st December, 1…

- ———. 2000c. “BSN Commercial Bank (M) Fully Repaid Danamodal's Loan of RM420 Mil…

- ———. 2001a. “Repayment of Danamodal’s Loan of RM700 Million to Oriental Bank Be…

- ———. 2001b. “Danamodal Signed S&P Agreement With Arab-Malaysian Finance Berhad …

- ———. 2001c. “Investments in Recapitalised BIs.” October 11, 2001.

- ———. 2001d. “Investments in Recapitalised BIs.” December 22, 2001.

- ———. 2002. “Financial Statements for the Year ended 31st December, 2001.” Febru…

- ———. n.d.a. “Danamodal Nasional Berhad - the Malaysian approach to bank recapit…

- ———. n.d.b. “Frequently Asked Questions (FAQs) on Danamodal.”

- ———. n.d.c. “Salient Terms and Conditions of the Bonds.”

- International Monetary Fund. 1999. Malaysia: Selected Issues. IMF Staff Country…

- Lindgren, Carl-Johan. Leslie E. Teo, Charles Enoch, Tomás JT Baliño, Anne Marie…

- Sulaiman, Seri Ali Abul Hassan. 1999. “Governor’s Keynote Address at the Nation…

Key Program Documents

-

(BNM 1998a) Bank Negara Malaysia Annual Report 1998

The annual report from the Malaysian central bank outlining the economic conditions and providing an outline of Danamodal.

-

(Danamodal n.d.a) “Danamodal Nasional Berhad - the Malaysian approach to bank recapitalisation, revitalisation and restructuring”

An overview from Danamodal of the recapitalization and restructuring efforts

-

(Danamodal n.d.b) “Frequently Asked Questions (FAQs) on Danamodal.”

An FAQ document from Danamodal providing information on its operations.

-

(Danamodal 1998a) Details on Establishment of Danamodal Nasional Berhad

A notice on the establishment of Danamodal and details surrounding its operations.

-

(BNM 2001b) Best Practices for the Management of Credit Risk

Guidance from the central bank on risk-management practices for banks.

-

(Danamodal n.d.c) Salient Terms and Conditions of the Bonds

The term sheet for the Danamodal bonds.

-

(BNM 1998b) Recapitalisation and Consolidation of the Banking Sector

A press release from the central bank on the plan to recapitalize and consolidate the banking sector.

-

(BNM 2000) Consolidation of Domestic Banking Institutions

A press release on the consolidation of the banking sector in Malaysia.

-

(Danamodal 1998b) Danamodal Plans to Inject RM1.5 billion into RHB Bank

A notice on Danamodal’s plans to inject capital into a bank in 1998.

-

(Danamodal 1998c) Danamodal to Inject RM50 billion into Perdana Merchant Bankers Berhad

A notice on Danamodal’s plans to inject capital into a bank in 1998.

-

(Danamodal 1998d) Danamodal Concludes Capital Injection of RHB Bank Berhad and Buys 30% of the Bank

A notice on Danamodal’s support to RHB Bank and government ownership of the bank.

-

(Danamodal 1998e) Khazanah’s Interest in RHB Bank

A press release on the potential interest in one of the banks receiving support via Danamodal.

-

(Danamodal 1999a) Danamodal Nasional Berhad today signed Definitive Agreements with four banking institution

A press release on Danamodal’s support to four banking institutions in 1999.

-

(Danamodal 1999c) Danamodal Injects RM1.6 billion into MBF Finance Berhad

A press release on Danamodal’s support to MBF Finance Bank in 1999.

-

(Danamodal 1999d) Danamodal Signs Definitive Agreements with Oriental Bank Berhad and United Merchant Finance Berhad

A press release on Danamodal’s support to two banks in 1999.

-

(Danamodal 2000a) Investments in Recapitalised BIs

A summary of the support to banking institutions in Malaysia through February 2000.

-

(Danamodal 2000c) BSN Commercial Bank (M) Fully Repaid Danamodal's Loan of RM420 Million

A press release announcing the repayment of Danamodal’s support by BSN Commercial Bank.

-

(Danamodal 2001a) Repayment of Danamodal’s Loan of RM700 Million to Oriental Bank Berhad

A press release announcing the repayment of Danamodal’s support by Oriental Bank Berhad.

-

(Danamodal 2001b) Danamodal Signed S&P Agreement With Arab-Malaysian Finance Berhad for the Sale of 100% Equity Interest In MBf Finance Berhad

A press release announcing the sale of Danamodal’s interest in a financial institution.

-

(Danamodal 2001c) Investments in Recapitalised Bis

A summary of the support to banking institutions in Malaysia through October 2001.

-

(Danamodal 2001d) Investments in Recapitalised Bis

A summary of the support to banking institutions in Malaysia through December 2001.

-

(Sulaiman 1999) Governor's Keynote Address at the National Credit Management Conference

A transcript from a speech given by the central bank governor in 1999.

-

(Abidin 2000) Malaysia’s alternative approach to crisis management

A journal article outlining the Malaysian government’s response to the Asian financial crisis.

-

(Cook 2008) Banking Reform in Southeast Asia: The region’s decisive decade

A book on the financial sector reform in Southeast Asia after the financial crisis.

-

(BNM 1997) Bank Negara Malaysia Annual Report 1997

The annual report from the Malaysian central bank outlining the economic conditions.

-

(BNM 1999) Bank Negara Malaysia Annual Report 1999

The annual report from the Malaysian central bank outlining the economic conditions.

-

(BNM 2001) Bank Negara Malaysia Annual Report 2001

The annual report from the Malaysian central bank outlining the economic conditions.

-

(BNM 2003) Bank Negara Malaysia Annual Report 2003

The annual report from the Malaysian central bank outlining the economic conditions.

-

(BNM 2007) Financial Stability and Payment Systems Report

The biannual report from the central bank on financial stability in Malaysia.

-

(Danamodal 2000b) Financial Statements for the Financial Year ended 31st December, 1999

The annual financial statement for Danamodal for fiscal year 1999.

-

(Danamodal 2002) Financial Statements for the Financial Year ended 31st December, 2001

The annual financial statement for Danamodal for fiscal year 2001.

-

(IMF 1999) Malaysia: Selected Issues

The 1999 IMF report on economic and financial conditions in Malaysia.

-

(Lindgren et al. 2000) Financial Sector Crisis and Restructuring; Lessons from Asia

An IMF report on financial crisis responses in Asian countries.

Appendix A: Timeline of Interventions

Sources: BNM 1997; BNM 1998a; BNM 1998b; BNM 2001a; BNM 2003; Danamodal 1998c; Danamodal 1998d; Danamodal 1999a; Danamodal 1999b; Danamodal 1999c; Danamodal 1999d; Danamodal n.d.a; Danamodal n.d.c.

Sources: BNM 1997; BNM 1998a; BNM 1998b; BNM 2001a; BNM 2003; Danamodal 1998c; Danamodal 1998d; Danamodal 1999a; Danamodal 1999b; Danamodal 1999c; Danamodal 1999d; Danamodal n.d.a; Danamodal n.d.c.

Appendix B: Breakdown of Injection Process

Source: Danamodal n.d.a.

Source: Danamodal n.d.a.

Taxonomy

Intervention Categories:

- Broad-Based Capital Injections

Countries and Regions:

- Malaysia

Crises:

- Asian Financial Crisis 1997