Resolution and Restructuring in Europe: Pre- and Post-BRRD

Luxembourg: Kaupthing Bank Luxembourg Restructuring, 2008

Purpose

To provide an orderly exit from the suspension of payments, ensuring maximum recovery for creditors and maintaining system-wide confidence

Key Terms

-

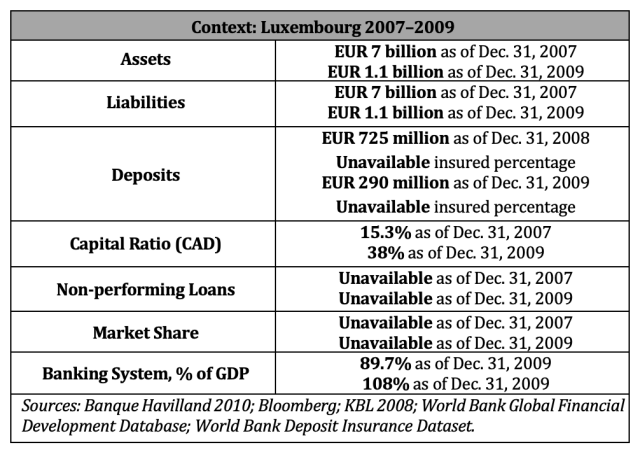

Size and Nature of InstitutionSmall subsidiary of Kaupthing Bank hf, with EUR 2 billion in deposits and EUR 7 billion in assets at the end of 2007

-

Source of FailureThe failure of Kaupthing Bank hf in Iceland led to a cross-default at KBL, entitling creditors to request immediate execution of their claims

-

Start DateOctober 9, 2008

-

End DateJuly 10, 2009

-

Approach to Resolution and RestructuringGovernments provided EUR 320 million to back the transfer of Belgian deposits to Crédit Agricole; London-based Blackfish Capital created a new bank for Luxembourgish depositors; and a special purpose vehicle was created for bad assets

-

OutcomesEUR 320 million debt obligation to state, EUR 55 million in public losses for Belgium and Luxembourg, and creation of new private bank by Blackfish Capital

-

Notable FeaturesThis was the first use of the suspension of payments framework in Luxembourg. The government immediately received burden-sharing SPV debt as repayment for the loan

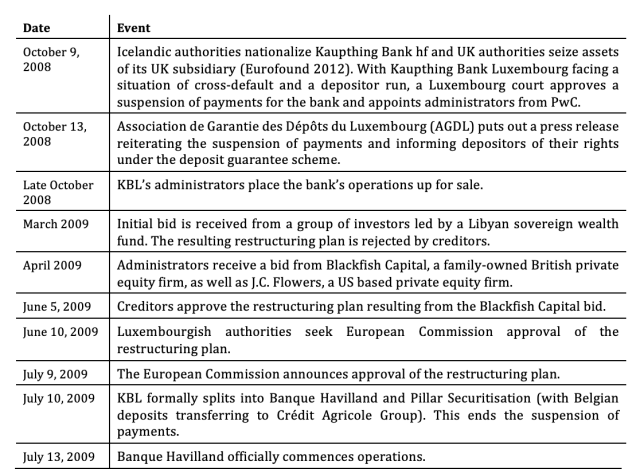

The nationalization of Iceland’s Kaupthing Bank hf on October 9, 2008, caused a situation of cross-default and a depositor run at its subsidiary, Kaupthing Bank Luxembourg S.A. (KBL). A cross-default entitles creditors to request immediate execution of their claims. KBL responded on the same day by requesting and receiving a suspension of payments regime (including depositors) from a Luxembourg court, which also appointed administrators. The administrators placed KBL’s operations for sale later that month, receiving a bid from a private fund, Blackfish Capital, which crafted a restructuring plan that creditors approved on June 5, 2009. The restructuring plan, carried out on July 10, 2009, resulted in the transfer of domestic deposits to Blackfish Capital’s Banque Havilland, the transfer of Belgian deposits to Crédit Agricole Group, and the transfer of remaining assets to a special purpose vehicle (SPV) called Pillar Securitisation. Luxembourg and Belgium each lent EUR 160 million (USD 222 million) to KBL as part of the restructuring. Banque Havilland administered the SPV on behalf of creditors, including the two governments. All prior KBL depositors were 100% protected. Creditors with claims in the SPV, including the Luxembourg and Belgian states, had recovered 50% as of mid-2012.

This module describes the restructuring of Kaupthing Bank Luxembourg S.A. (KBL). KBL was a subsidiary of Icelandic bank Kaupthing Bank hf, and the capital injections and resolution processes provided to the Icelandic banking system are discussed in corresponding cases (George 2024).

Kaupthing Bank Luxembourg was the Luxembourg subsidiary of Kaupthing Bank hf, one of three large multinational banks in Iceland. Due to a nationwide banking crisis, Icelandic authorities nationalized Kaupthing Bank on October 9, 2008. Media coverage of the events in Iceland led to a run by KBL depositors (CSSF 2009a; Eurofound 2012; EC 2009a). Authorities in the United Kingdom immediately seized the assets of Kaupthing Bank’s UK subsidiary, thereby freezing its operationsFFor more information, see the YPFS case study on the restructuring of Iceland’s three largest banks (George 2024).. The resulting inability to refinance placed KBL in a situation of cross-default, which entitled its creditors to immediately demand repayment of their bonds. In order to prevent this, KBL’s board of directors sought and received a suspension of payments from the Luxembourg District Court, preventing all bank payouts including payments to depositors (CSSF 2008; Eurofound 2012).

The court appointed administrators from PricewaterhouseCoopers (PwC) to oversee the bank during the suspension of payments. Authorities stated that an orderly solution for exit from the suspension of payments was necessary to ensure maximum recovery for creditors and to maintain system-wide confidence. The administrators explored avenues to exit the suspension of payments by placing KBL’s operations up for sale. In April 2009, KBL received a bid from Blackfish Capital, which resulted in KBL’s administrators drafting a restructuring plan that creditors approved on June 5, 2009 (CSSF 2008; Eurofound 2012; EC 2009a).

The restructuring plan consisted of three measures that separated various activities of KBL. The private and online deposits of Belgian customers, which constituted the bulk of KBL’s deposit base, were transferred to Crédit Agricole Group along with the necessary funds to reimburse depositors as necessary. The private and deposit-taking activities of Luxembourg customers were taken over by Blackfish Capital, which transferred them to a newly created entity called Banque Havilland. All of KBL’s unsold assets, mostly consisting of commercial lending operations, were transferred to a special purpose vehicle (SPV) called Pillar Securitisation. The restructuring plan also called for Luxembourg to cover the shortfall between KBL’s total assets and liabilities, which amounted to EUR 310 million as of December 31, 2008. The intention of this state contribution was to cover potential withdrawals by depositors when the suspension of payments period ended. To cover 100% of deposits transferred to Crédit Agricole Group, Luxembourg and Belgium each loaned EUR 160 million (USD 222 million)FAccording to the Bank for International Settlements (BIS), EUR 1 = USD 1.39 on July 10, 2009.. The Association for the Guarantee of Deposits Luxembourg (AGDL) covered the difference between the loan amount and the value of transferred Belgian deposits (EC 2009a; PwC 2009; Global Banking News 2009).

The official split of KBL into Banque Havilland and Pillar Securitisation on July 10, 2009, ended the suspension of payments. The Belgian deposits were transferred to Crédit Agricole Group prior to the split. The deposits of all customers were 100% maintained after restructuringFAGDL began providing payments for claims in December 2008 (AgeFI Luxembourg 2008b).. Banque Havilland commenced operations on July 13, 2009. As a result of the restructuring, interbank creditors of KBL received notes from the SPV. As of most recent data (mid-2012), creditors with claims in the SPV had recovered 50% of their exposures (Banque Havilland 2009; Coe Smith 2009; CSSF 2011; EC 2009a; EC 2009b; Eurofound 2012). The timeline of restructuring events is shown in Figure 1.

Figure 1: Timeline of Events Related to the Restructuring of KBL

Sources: AGDL 2008; Banque Havilland 2009; EC 2009a; EC 2009b; Eurofound 2012.

The restructuring of KBL was the first usage of the suspension of payments framework by Luxembourgish authorities. The use of this framework allowed the bank to be restructured without a liquidation. Authorities needed to be flexible because the framework had not been previously tested. A result of this adaptability was the decision by the Luxembourg Court of Appeal that interbank creditors “for whom the restructuring plan does not provide for full and immediate compensation” had to approve the restructuring plan (Coe Smith 2009).

The restructuring was deemed successful in that no depositors took losses. A European Union (EU) agency report also discusses the fact that KBL’s application for a suspension of payments isolated the subsidiary from its Icelandic parent, which complicated the restructuring process by preventing intragroup debt scheduling (Eurofound 2012). Further discussion regarding the efficacy of the restructuring is limited due to its status as a subsidiary of Kaupthing Bank hf. Context regarding the restructuring of Kaupthing and its two peer banks in the Icelandic banking sector can be found in the YPFS case study on the restructuring of Iceland’s three largest banks (George 2024).

In 2020, Banque Havilland faced criminal scrutiny from Luxembourg over its dealings with leaders from Azerbaijan and Abu Dhabi (Finch and Wilson 2020).

Key Design Decisions

Purpose

1

On October 9, 2008, the Icelandic state took over Kaupthing Bank hf, as a consequence of a major banking crisis taking place in Iceland. Media coverage of the events in Iceland led to a depositor run on Kaupthing Bank Luxembourg. In addition, rating agency downgrades of banks headquartered in Iceland led to massive asset devaluations as foreign investors rushed to sell. The seizure of assets of Kaupthing’s British subsidiary by UK authorities placed KBL in a situation of cross-default. As such, the bank’s creditors held the right to immediately demand the repayment of their bonds. As of 2007, KBL had EUR 4.5 billion in non-deposit liabilities on its balance sheet. To prevent this, KBL’s board of directors applied for a suspension of payments by order of the Luxembourg District Court. The court immediately granted the suspension of payments and appointed administrators from PricewaterhouseCoopers to oversee the bank (CSSF 2008; CSSF 2009b; EC 2009a; Eurofound 2012; KBL 2008).

Authorities from Belgium and Luxembourg considered creating a joint fund for the protection of depositors in the two countries. Cross-border cooperation was especially important for Luxembourg to maintain its status as a financial center (See Key Design Decision No. 13, Cross-border Cooperation). Authorities remained open to all scenarios, and both governments ultimately received burden-sharing SPV debt as a result of the restructuring (AFX Asia 2008; EC 2009a; Reuters 2009a).

In its application for State Aid, Luxembourgish authorities stated that an orderly solution for exit from the cessation of payments was necessary to ensure maximum recovery for creditors and to maintain system-wide confidence (EC 2009a).

Part of a Package

1

On October 13, 2008, the Financial Sector Surveillance Commission (CSSF), the financial supervisory agency of Luxembourg, announced that the deposit guarantee scheme administered by the Association de Garantie des Dépôts du Luxembourg had been triggered. The guarantee scheme provided reimbursement up to EUR 20,000, which the government increased to EUR 100,000 in order to further calm depositors (AGDL 2008; AgeFI Luxembourg 2008a; Mayer Brown 2009). For an in-depth discussion of the Luxembourg deposit guarantee, see “Association for the Guarantee of Deposits Luxembourg” Vergara (2022a).

Of the EUR 1.3 billion starting balance of Banque Havilland, EUR 750 billion–EUR 800 million represented existing commitments to the Central Bank of Luxembourg from prior refinancing operations (EC 2009a).

Legal Authority

1

As an alternative to bankruptcy, the leadership of Kaupthing Bank Luxembourg applied for a suspension of payments from the Luxembourg District Court on October 9, 2008 (Eurofound 2012). Article 60 of the Law of 5 April 1993 on financial institutions established the jurisdiction and powers of the CSSF and outlines the steps of the suspension of payments process. The law deems a suspension of payments appropriate in the following situations (Luxembourg Government 1993):

- When the credit of the institution in question is shaken or when it is in a liquidity impasse, whether or not there is a cessation of payment;

- When full performance of the institution’s commitments is compromised; or

- When the legal authorization of the establishment has been withdrawn and this decision is not yet final.

The law also stipulates that the judgment approving the suspension of payments must also include the appointment of one or more administrators who undertake all acts and decisions for the bank in question (See Key Design Decision No. 4, Administration).

The Law of 19 March 2004 stipulates that only the CSSF has the power to formally apply to the Luxembourg District Court for dissolution of an establishment, which was the legal rationale used to split KBL (Luxembourg Government 1993).

Luxembourg law dictates that there are two avenues for ending a suspension of payments period. Either (1) the institution restores levels of liquidity and solvency to satisfy all claims immediately or in acceptable instalments or (2) the placement of the bank into judicial liquidation (EC 2009a).

The loans provided by Luxembourg and Belgium were also subject to European Commission (EC) approval as State Aid given the definitions outlined in Article 87 of the EC Treaty (EU 2002).

Administration

1

Following the suspension of payments, a Luxembourg court appointed PwC as the administrators of KBL on October 9, 2008. In this role, PwC administrators were charged with actualizing the restructuring plan, and held the rights to negotiate and finalize the structure of the special purpose vehicle and the allocation of assets in the restructuring plan (EC 2009b; Eurofound 2012).

The SPV was overseen by a committee appointed by interbank creditors with stakes in the SPV and the government. Banque Havilland ran the SPV on behalf of the creditors committee and the government (Eurofound 2012; Owen 2011).

Governance

1

In order to initiate the restructuring of the bank (formally called dissolution in Luxembourg legislation), the administrators of KBL were legally required to notify the CSSF, which in turn submitted a request to the Luxembourg District Court. The CSSF was also legally required to inform the EC and authorities in all impacted member states of any restructuring measures (Luxembourg Government 1993).

Upon commencing operations in July 2009, Banque Havilland came under the supervision of CSSF as a bank with operations in Luxembourg. Its management of the assets in the SPV came under the supervision of a steering committee comprising representatives of the creditors and the government (Owen 2011).

Communication

1

Following the collapse of the three major Icelandic banks, the governments of Luxembourg and Belgium made clear their intent to protect depositors and creditors in Kaupthing Bank Luxembourg, in order to preserve Luxembourg’s status as a financial center. The CSSF immediately communicated the suspension of payments at KBL to the public on October 9, 2008. The AGDL issued its own press release communicating the suspension of payments on October 13, 2008, providing instructions for depositors on their rights relating to Luxembourg’s deposit guarantee. The press release urged affected clients to complete the necessary paperwork as soon as possible (For more information, see Key Design Decision No. 10, Treatment of Clients) (AFX Asia 2008; AGDL 2008; CSSF 2008).

Regarding the rejection of the initial bid from a coalition of Middle Eastern investors, one of KBL’s administrators stated that the cash offer for the SPV was too low (Reuters 2009b).

The CSSF issued a press release announcing the restructuring plan on July 10, 2009. The press release outlined the various facets of the restructuring plan (See Key Design Decision No. 8, Approach to Resolution/Restructuring) and stated that Banque Havilland would commence activities on July 13, 2009. CSSF annual reports provided context on the restructuring measures, with the 2010 report announcing that all depositors had been fully repaid (CSSF 2009a; CSSF 2009b; CSSF 2010; CSSF 2011).

KBL’s administrators conferred with all relevant stakeholders, including the Luxembourg state, Belgian state, AGDL, and interbank creditors, in order to establish that the restructuring plan based on the bid from private equity fund Blackfish Capital was the best path forward (Eurofound 2012).

Source and Size of Funding

1

In the initial call for tenders, authorities made clear to potential buyers that they were willing to provide the funds necessary to account for the difference between KBL’s assets and liabilities. The restructuring plan stated that as of December 31, 2008, the difference between the bank’s total current liabilities and total assets was EUR 310 million. Luxembourg covered that difference by providing the bank with a EUR 320 millionFThis total represented the EUR 310 million liquidity shortfall plus a margin of EUR 10 million (EC 2009a, 4). (USD 445 million) loan that did not bear interest. Authorities paid this loan out in two tranches, a super-senior tranche of EUR 210 million and a senior tranche of EUR 110 million. The loan from the Luxembourg state was paid back immediately with bonds issued by the SPV. The super-senior tranche received first priority on repayment, while the senior tranche was treated pari passu with interbank creditors. Luxembourgish authorities expected the orderly sale of assets held by the SPV to pay off the bondholders by 2016 or 2017 when it was to be wound up. The EC expected that the orderly sale of assets within the SPV would allow for all creditors to be repaid (EC 2009a).

The Belgian deposits were transferred to the Crédit Agricole Group prior to the split of KBL. At the time, there was a difference between the EUR 320 million loan and the transferred deposits, which totaled EUR 350 million–EUR 400 million. This EUR 30 million–EUR 80 million amount was covered by the AGDL. This coverage corresponded to the compensation depositors would have received had the bank entered into liquidation. The AGDL also received senior SPV bonds as repayment of the funds (EC 2009a).

Due to the large presence of Belgian depositors in KBL, Belgian authorities participated by extending a EUR 160 million loan to Luxembourg (See Key Design Decision No. 13, Cross-border Cooperation). The loan was granted on the condition that Luxembourgish authorities used the funds to finance the aforementioned loan to KBL. The Belgian state’s loan was also divided into two tranches—EUR 105 million and EUR 55 million. These two tranches represented 50% of the two tranches of the loan extended to the bank, and their repayment conditions were aligned. Luxembourgish authorities therefore committed to repay the loan when it received payments from the SPV. As such, this tranche shared the losses of SPV compensation, which totaled 50% as of 2012 (EC 2009a; Eurofound 2012).

Approach to Resolution and Restructuring

1

Following the nationalization of Kaupthing in Iceland, the CSSF announced a Luxembourg court’s appointment of administrators for the Luxembourg subsidiary on October 9, 2008. KBL had approached the court for approval of a suspension of payments regime on that same day. Luxembourg law dictated that the suspension of payments could end either in (1) the institution restoring levels of liquidity and solvency to satisfy all claims immediately or in acceptable instalments or (2) the placement of the bank into judicial liquidation (CSSF 2008; EC 2009a).

KBL’s administrator, PwC, immediately began seeking routes to bring Kaupthing out of the cessation of payments by placing all parts of the bank up for sale. Authorities made all potential buyers aware that the state was willing to provide public funding to make up the difference between the bank’s assets and liabilities (EC 2009a).

The first bid for the private banking operations in Luxembourg came from a Libyan investment fund, and PwC prepared an initial restructuring plan. However, Kaupthing’s creditors rejected this bid on March 16, 2009, citing insufficient valuation of the institution. Two further bids came from J.C. Flowers and Blackfish Capital in April 2009. Creditors approved the restructuring plan associated with Blackfish Capital’s bid, and authorities announced the acceptance of the bid on June 5, 2009. Authorities sought European Commission approval on June 10, and the EC announced its approval on July 9, 2009 (EC 2009a; Eurofound 2012; Reuters 2009b).

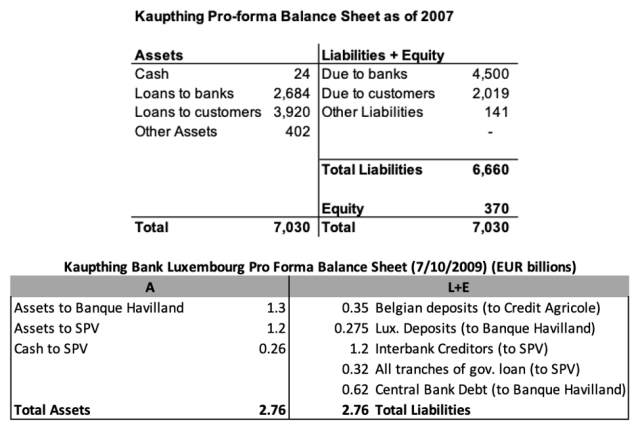

The restructuring plan based on the Blackfish Capital bid involved the takeover of the private and deposit banking activities of KBL in Luxembourg as of March 13, 2009. Blackfish transferred the deposits to a newly registered credit institution called Banque Havilland. This institution had a starting balance of EUR 1.3 billion, of which EUR 750 million–EUR 800 million were existing commitments to the Central Bank of Luxembourg. Blackfish contributed EUR 50 million of capital and EUR 25 million–EUR 75 million of deposits. In total, Banque Havilland received approximately EUR 208 million in cash. The bank’s other assets, most of which consisted of commercial lending operations, were transferred to an SPV called Pillar Securitisation. These were balanced with liabilities that consisted largely of the bonds issued by the SPV to the state, the deposit guarantee association, and existing debts to interbank creditors. The SPV received EUR 260 million in cash. As such, CSSF split the formerly Kaupthing Bank Luxembourg into two entities, Banque Havilland and the SPV (EC 2009a; Reuters 2009b; Total Securitization 2009).

Regarding foreign activities, Kaupthing’s Belgian deposits were transferred to Crédit Agricole Group. The deposits were incorporated into the existing banking operations of the two subsidiaries, Crédit Agricole Belgique and Keytrade BankFCrédit Agricole Group also received some assets as part of the restructuring plan, though research has not revealed any details (AgeFI Luxembourg 2009)..The Swiss branch of the bank was closed, with all depositors being reimbursed by the Swiss deposit guarantee schemeFSee YPFS case study “Swiss Banks’ and Securities Dealers’ Depositor Protection Association” for a detailed description of the Swiss deposit guarantee scheme Vergara (2022b).(EC 2009a). Figure 2 depicts the KBL balance sheet at year-end 2007 and the balance sheet just prior to restructuring in July 2009.

Figure 2: Kaupthing Balance Sheets 2007–2009 (EUR millions)

NOTE: The European Commission offered only ranges for the total amount of Belgian and Luxembourgish deposits. To make the assets and liabilities equal in our pro forma balance sheet, we rounded up both.

Sources: Banque Havilland 2010; EC 2009a; KBL 2008.

Treatment of Creditors and Equity Holders

1

The Luxembourg Court of Appeal decided that the approval of interbank creditors—“for whom the restructuring plan does not provide for full and immediate compensation”— was necessary for the approval of the restructuring plan (Coe Smith 2009). Depositors and trade creditors were to be repaid in full upon the successful completion of the restructuring and did not have to approve the plan.

KBL’s commercial lending operations were transferred to an SPV called Pillar Securitisation. Interbank creditors received EUR 585 million in notes of various classes from the SPV. The restructuring plan stated that the orderly sale of the SPV’s assets should allow creditors to be repaid. As of mid-2012, the creditors had collected 50% of their initial exposure (Coe Smith 2009; EC 2009a; Eurofound 2012).

The Luxembourg government and AGDL also held super-senior and senior claims in the SPV (see Key Design Decision No. 7, Source and Size of Funding). The restructuring plan stated that the super-senior bonds received priority, and senior bonds were to be repaid pari passu with the SPV’s other debts (EC 2009a).

Holders of “non-convertible bonds” in Pillar Securitisation were subject to an Equalization ProvisionFThe annual report classified the vast majority of creditors as holders of non-convertible bonds (Pillar Securitisation 2010).. This provision stated that in the event that assets were not sufficient to compensate noteholders in full, their claims would be reduced in accordance with the shortfall. As of 2022, the SPV reported a loss of EUR 6 million (Pillar Securitisation 2010; Pillar Securitisation 2023).

Treatment of Clients

1

A press release issued by the AGDL on October 13, 2008, alerted depositors to their rights under the deposit insurance scheme. The deposit guarantee scheme covered customer deposits up to EUR 20,000, eventually increasing to EUR 100,000 in October 2008. At the time of KBL’s split, EUR 175 million–EUR 225 million had been paid out to depositors by the AGDL under the existing deposit insurance scheme (AGDL 2008; AgeFI Luxembourg 2008a; EC 2009a).

Upon commencing operations in July 2009, Banque Havilland took over the deposits of all domestic customers. The restructuring plan transferred the deposits of online and private banking customers of the Belgian branch to Crédit Agricole Group. Swiss depositors fell under the purview of Swiss law (CSSF 2010; EC 2009a).

The CSSF 2010 annual report stated that all depositors in KBL were repaid in full (CSSF 2011).

Treatment of Assets

1

The restructuring plan stated that all of the remaining assets not taken by Banque Havilland were to be transferred to an SPV called Pillar Securitisation. These assets amounted to EUR 1.2 billion and consisted primarily of KBL’s commercial lending operations. The liabilities side of Pillar Securitisation’s balance sheet consisted of the bank’s debts to the Luxembourg state, AGDL, and the bank’s interbank creditors (EC 2009a; Global Banking News 2009).

A committee of interbank creditors with stakes in the SPV managed its operations. The restructuring plan stipulated that the orderly sale of all transferred assets should allow for creditors to be repaid (EC 2009a).

Treatment of Board and Management

1

The suspension of payments on October 9, 2008, resulted in the appointment of administrators from PwC. While KBL’s management and internal organization remained in place, all activities were supervised by the appointed administrators. Upon the creation of Banque Havilland, Jonathan RowlandFJonathan Rowland was the son of David Rowland, the new shareholder and honorary president of Banque Havilland (Banque Havilland 2009; Banque Havilland 2010). served as chairman of the board and Magnus Gudmundsson served as the chief executive officer (Banque Havilland 2009; CSSF 2008; Eurofound 2012; PwC 2009).

Cross-Border Cooperation

1

When Icelandic authorities nationalized the country’s three largest banks, including Kaupthing, the existing deposit insurance scheme did not have enough funds to compensate all depositors. Meanwhile the assorted foreign subsidiaries were subject to individual oversight and deposit insurance schemes. Given the lack of adequate funds in Iceland to compensate claimants in the various subsidiaries, regulators in host countries such as Luxembourg took individual actions to protect depositors and creditors. Other host countries included the United Kingdom, Germany, Finland, Switzerland, and Norway (IADI 2011).

At the onset of the crisis, Belgian and the Luxembourgish authorities immediately began discussing measures to protect depositors (AFX Asia 2008; Reuters 2009a). Luxembourg’s prime minister stated that Luxembourg had a duty to protect Belgian savers: “If people in Belgium got the impression that the Luxembourg government only supports banks that manage the savings of Luxembourgers, that would be a death blow to Luxembourg as a financial centre” (AFX Asia 2008).

The bulk of KBL’s deposit base stemmed from its Belgian operations. As a result, Belgian authorities provided Luxembourg with a EUR 160 million loan. Luxembourgish authorities used these funds to provide the loan that was necessary for the completion of KBL’s restructuring (See Key Design Decision No. 7, Source and Size of Funding) (EC 2009a).

When Luxembourgish authorities placed KBL under a suspension of payments, Swiss authorities immediately initiated liquidation proceedings of the Swiss branch. Small deposits totaling less than 5,000 Swiss francs (CHF; USD 4,400)FAccording to the BIS, USD 1 = EUR 0.73 on October 09, 2008.were repaid in full on October 16 and 17, 2008. All other depositors were repaid up to the CHF 30,000 limit by the end of November 2008 (IADI 2011).

Other Conditions

1

The suspension of payments regime within which KBL underwent restructuring prohibited all payments and activities other than precautionary and protective measures, as authorized by the court-appointed administrators (CSSF 2008).

Duration

1

Following the suspension of payments, the appointed administrators immediately began exploring options to restore normal operations. Creditors approved the final restructuring plan on June 5, 2009, with the EC approval coming on July 9, 2009. As such, KBL officially split on July 10, 2009, with Banque Havilland commencing legal operations on July 13, 2009 (CSSF 2010; EC 2009a).

According to the restructuring plan, authorities expected the SPV to be wound up by 2016 or 2017 at the latest. As of mid-2012, creditors had recovered 50% of their initial exposure. As of most recent information (2022), Pillar Securitisation still exists as an entity, though information is limited on the nature of its current operations (EC 2009a; Pillar Securitisation 2023).

Key Program Documents

-

(Eurofound 2012) Eurofound. 2012. “Banque Havilland, Luxembourg.,” May 21, 2012.

Web page discussing Banque Havilland and the restructuring process that led to its creation.

-

(Mayer Brown 2009) Mayer Brown. 2009. “Summary of Government Interventions: Luxembourg.” April 21, 2009.

Summary of Luxembourg’s financial interventions in the Global Financial Crisis.

-

(EC 2009a) European Commission (EC). 2009a. “State Aid Decisions N 344/2009— Luxembourg, N 380/2009—Belgium; Restructuring Aid for Kaupthing Bank Luxembourg S.A.,” July 9, 2009.

European Commission decision regarding State Aid for the restructuring of Kaupthing Bank Luxembourg.

-

(EC 2009b) European Commission (EC). 2009b. “Extract from the Decision Concerning Kaupthing Bank Luxembourg S.A.” Notices from Member States, July 22, 2009.

EC decision ratifying the mission of the administrators of Kaupthing Bank Luxembourg.

-

(EU 2002) European Union (EU). 2002. Consolidated Versions of the Treaty on European Union and of the Treaty Establishing the European Community. Section 2, Aids Granted by States, Article 87.

Section of the Treaty Establishing the European Community, defining State Aid.

-

(Luxembourg Government 1993) Luxembourg Government. 1993. Law of 5 April 1993 on the Financial Sector, as Amended.

Law establishing the suspension of payments and restructuring framework, as well as the AGDL’s coverage requirements (Translated by the Luxembourg Chamber of Deputies).

-

(AFX Asia 2008) AFX Asia. 2008. “Update 2-Belgium, Luxembourg to Help Iceland’s Kaupthing.” AFX Asia, October 17, 2008.

News article discussing efforts by the Belgian and Luxembourgish governments to support Kaupthing Bank Luxembourg.

-

(Coe Smith 2009) Coe Smith, Claire. 2009. “Kaupthing Was First to Test Directive.” Financial News, July 13, 2009.

Press article discussing Luxembourg’s use of the suspension of payments for Kaupthing Bank Luxembourg.

-

(Finch and Wilson 2020) Finch, Gavin, and Harry Wilson. 2020. “UAE’s MBZ Was Known as ‘the Boss’ at Banque Havilland.” Al Jazeera, December 21, 2020.

News article discussing special privileges granted to a Banque Havilland client by owner David Rowland.

-

(Global Banking News 2009) Global Banking News. 2009. “Kaupthing Luxembourg Creditors Approve Restructuring.” Global Banking News, June 5, 2009.

News article discussing the approval of the restructuring plan by Kaupthing Bank Luxembourg’s creditors.

-

(Owen 2011) Owen, Glen. 2011. “Probe into Last-Ditch Loans at Icelandic Bank.” This is Money UK, April 10, 2011.

News article discussing the loans offered to KBL.

-

(Reuters 2009a) Reuters. 2009a. “Belgium, Luxembourg Discuss Kaupthing Guarantee Fund.” Reuters, January 6, 2009.

News article reporting discussions around protecting Belgian and Luxembourger depositors at Kaupthing Bank Luxembourg.

-

(Reuters 2009b) Reuters. 2009b. “Update 1-Kaupthing Luxembourg Creditors OK Restructuring.” Reuters, June 5, 2009.

Reuters article reporting the approval of the Blackfish Capital restructuring bid for Kaupthing Bank Luxembourg.

-

(Total Securitization 2009) Total Securitization. 2009. “Blackfish to Acquire Kaupthing Bank Luxembourg.” Total Securitization, July 17, 2009.

News article discussing Blackfish Capital’s role in the restructuring of Kaupthing Bank Luxembourg.

-

(AGDL 2008) Association pour la Garantie des Dépôts Luxembourg (AGDL). 2008. “Kaupthing Bank: Situation of the Bank.” Press release, October 13, 2008.

AGDL announcement regarding the failure of Kaupthing.

-

(AgeFI Luxembourg 2008a) AgeFI Luxembourg. 2008a. “Luc Frieden: ‘Luxembourg Increases the Guarantee of Bank Deposits to 100,000 Euros.’” Press release, October 20, 2008.

Press release announcing the increase of the Luxembourg deposit insurance scheme.

-

(AgeFI Luxembourg 2008b) AgeFI Luxembourg. 2008b. “À défaut d’une reprise de la banque l’AGDL commencera l’indemnisation des clients de Kaupthing Bank Luxembourg début Décembre 2008.” Press release, December 2008.

Press release detailing the payout timing for depositors from the Luxembourg deposit insurance scheme.

-

(AgeFI Luxembourg 2009) AgeFI Luxembourg. 2009. “Crédit Agricole Takes over the Customers of Kaupthing Bank Belgium.” Press release, February 2009.

Press release discussing the transfer of Belgian deposits in KBL to Crédit Agricole.

-

(Banque Havilland 2009) Banque Havilland. 2009. “Press Release, 30th September 2009, Time: 11AM.” Press release, September 30, 2009.

Press release announcing Banque Havilland’s commencement of operations.

-

(CSSF 2008) Financial Sector Surveillance Commission (CSSF). 2008. “Suspension of Payments: Kaupthing Bank Luxembourg S.A. – Appointment of Administrator.” Press release, October 9, 2008.

Press release announcing the suspension of payments at Kaupthing Bank Luxembourg.

-

(CSSF 2009b) Financial Sector Surveillance Commission (CSSF). 2009a. “Restructuring of Kaupthing Bank Luxembourg S.A.” Press release, July 10, 2009.

Press release announcing the restructuring of Kaupthing Bank Luxembourg.

-

(PwC 2009) PricewaterhouseCoopers (PwC). 2009. “Press Release, July 10, 2009.” Press release, July 10, 2009.

Press release announcing the implementation of the restructuring plan and the lifting of the suspension of payments regime.

-

(Banque Havilland 2010) Banque Havilland. 2010. Annual Report 2009.

Banque Havilland annual report for the year 2009.

-

(CSSF 2009a) Financial Sector Surveillance Commission (CSSF). 2009b. Annual Report 2008.

CSSF annual report for 2008.

-

(CSSF 2010) Financial Sector Surveillance Commission (CSSF). 2010. Annual Report 2009.

CSSF annual report for the year 2009.

-

(CSSF 2011) Financial Sector Surveillance Commission (CSSF). 2011. Annual Report 2010.

CSSF annual report for the year 2010.

-

(KBL 2008) Kaupthing Bank Luxembourg (KBL). 2008. Annual Report 2007.

Kaupthing Bank Luxembourg annual report for year 2007.

-

(Pillar Securitisation 2010) Pillar Securitisation. 2010. Annual Report 2009.

Annual report for Pillar Securitisation for the year 2009.

-

(Pillar Securitisation 2023) Pillar Securitisation. 2023. Annual Report 2022.

Annual Report for Pillar Securitisation for the year 2022.

-

(George 2024) George, Ayodeji. 2024. “Iceland: Landsbanki Restructuring, 2008.” Journal of Financial Crises.

YPFS case study discussing the restructuring of Iceland’s major banks during the GFC.

-

(IADI 2011) International Association of Deposit Insurers (IADI). 2011. “Discussion Paper on Cross Border Deposit Insurance Issues Raised by the Global Financial Crisis,” March 2011.

IADI paper summarizing the cross-border implications of deposit insurance events arising from the Global Financial Crisis of 2007–2009.

-

(McNamara et al. 2024) McNamara, Christian M., Carey K. Mott, Salil Gupta, Greg Feldberg, and Andrew Metrick. 2024. “Survey of Resolution and Restructuring in Europe, Pre- and Post-BRRD.” Journal of Financial Crises 6, no. 1.

Survey of YPFS case studies examining 21st-century bank resolutions and restructurings in Europe before and after the existence of the Bank Recovery and Resolution Directive.

-

(Vergara 2022a) Vergara, Ezekiel. 2022a. “Association for the Guarantee of Deposits Luxembourg.” Journal of Financial Crises 4, no. 2: 444–58.

Case study discussing the deposit guarantee scheme in Luxembourg.

-

(Vergara 2022b) Vergara, Ezekiel. 2022b. “Swiss Banks’ and Securities Dealers’ Depositor Protection Association.” Journal of Financial Crises 4, no. 2: 606–23.

Case study discussing the Swiss deposit guarantee scheme.

Taxonomy

Intervention Categories:

- Resolution and Restructuring in Europe: Pre- and Post-BRRD

Crises:

- Global Financial Crisis