Broad-Based Capital Injections

Korea: Bank Recapitalization Fund

Purpose

To strengthen the capital base of banks in order to encourage lending to nonfinancial institutions, particularly SMEs, through the purchase of preferred shares, hybrid securities, or subordinated debt from Korean commercial banks.

Key Terms

-

Announcement DateDecember 18, 2008

-

Operational DateFebruary 15, 2009

-

Wind-down DatesAugust 2016

-

Program SizeKRW 4.0 trillion by eight private banks and financial institutions

Key Design Decisions

Part of a Package

Governance

Program Size

Source of Injections

Eligible Institutions

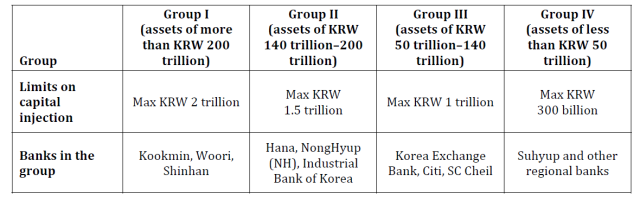

Individual Participation Limits

Capital Characteristics

Restructuring Plan

Exit Strategy

Key Program Documents

Taxonomy

Intervention Categories:

- Broad-Based Capital Injections

Countries and Regions:

- Korea

Crises:

- Global Financial Crisis