Broad-Based Capital Injections

Italy (2008) Capital Injections

Purpose

“To restore stability of the financial system and to remedy a serious disturbance in the economy of Italy”

Key Terms

-

Announcement DateOctober 9, 2008

-

Operational DateJuly 31, 2009

-

Wind-down DatesDecember 31, 2009

-

Program SizeInitially, available funds were up to €15 billion–€20 billion. In February 2009, up to €12 billion

-

Peak Utilization€4.05 billion

-

Notable Features“Tremonti bonds,” code of ethics, commitments to lend to SMEs

In response to the 2007–09 Global Financial Crisis, in October 2008, the Italian government announced urgent measures to guarantee financial stability and the flow of credit. The Italian government targeted three areas of support: (1) bank recapitalizations, (2) liquidity access, and (3) expansion of guarantees on bank deposits. This case study exclusively examines the Italian bank recapitalization scheme introduced in December 2008 in line with European Union State Aid rules.

The four Italian banks recapitalized in 2009 under the scheme were Banco Popolare (€1.45 billion), Banca Popolare di Milano (€500 million), Credito Valtellinese (€200 million), and Banca Montepaschi di Siena (€1.9 billion), for an overall amount of €4.05 billion. The government purchased special bonds issued by banks. These bonds became known as “Tremonti bonds,” and Italian regulators agreed to treat them as core Tier 1 regulatory capital.

|

Italy Context 2008–2009 |

|

|

GDP |

$2,410.9 billion in 2008 |

|

GDP per capita |

$2,196.8 billion in 2009 |

|

Sovereign credit rating (five-year senior debt) |

$40,778 in 2008 $37,080 in 2009 |

|

Size of banking system |

Data for 2008: Fitch: AA- Moody’s: Aa2 S&P: A+

Data for 2009: Fitch: AA- Moody’s: Aa2 S&P: A+ |

|

Size of banking system as a percentage of GDP |

107.3% in 2008 114.2% in 2009 |

|

Size of banking system as a percentage of financial system |

100% in 2008 100% in 2009 |

|

Five-bank concentration of banking system |

62.5% of total banking assets in 2008 |

|

Foreign involvement in banking system |

6% of total banking assets in 2008 6% of total banking assets in 2009 |

|

Government ownership of banking system |

None |

|

Existence of deposit insurance |

Yes in 2008 |

|

Source: Bloomberg. |

The 2007–2009 Global Financial Crisis prompted governments around the world to take unprecedented actions. On October 9, 2008, the Italian government issued Decree-Law N. 155, on urgent measures to guarantee the stability of the financial system and the continued flow of credit. It targeted three areas of support: bank recapitalizations, greater access to liquidity, and expanded guarantees on bank deposits. Decree-Law N. 185/2008 became the legal basis of the Italian bank recapitalization scheme.

The Italian Ministry of Economy and Finance recapitalized four banks in 2009 by the purchase of special bonds, known as “Tremonti bonds,” to strengthen the banks’ balance sheets. Despite speculations, the two largest Italian banks, Intesa Sanpaolo and UniCredit, did not participate in the scheme.

Italian regulators deemed the Tremonti bonds as core Tier 1 regulatory capital because they were perpetual, noncumulative, and convertible into common shares after three years. Participating banks had to adhere to a “code of ethics” regarding policies on executive compensation. They had to commit to increase lending to small and medium-sized enterprises (SMEs), contribute to the guarantee fund for loans granted to SMEs, suspend up to 12 months of mortgage payments for homeowners, and ensure appropriate liquidity levels to creditors of public administrations.

Italian authorities expressed that the Italian recapitalization scheme “exhibited satisfactory performance in its implementation, providing a safety net that corresponds well to market needs and ensuring the provision of lending to the real economy” (EC 2010b). In February 2010, Bank of Italy Governor Mario Draghi expressed that Italian banks were “well placed to cope with the international environment” (Draghi 2010a). Draghi noted that their capital bases were strengthened by the issue of shares, disposal of noncore assets, the ploughing back of profits and, in some cases, government interventions. With regard to the design of Tremonti bonds, a representative from the Bank of Italy pointed out that, in principle, instruments with standard, noncomplex features were preferable as they allowed for greater comparability, better pricing, and clearer loss-absorption mechanisms.

Key Design Decisions

Part of a Package

1

On October 9, 2008, Italy issued Decree-Law N. 155, “Urgent Measures to Guarantee the Stability of the Credit System and the Continued Flow of Credit to Firms and Consumers in the Current State of Crisis in World Financial Markets.” The decree envisaged a government support package focused on three areas: (1) recapitalizations, (2) access to liquidity, and (3) expanded guarantees on bank deposits (Bank of Italy 2008). The €80 billion Italian economic stimulus plan announced on November 15, 2008, was considered low at an estimated 0.6% of GDP (Bank of Italy 2009d, 5; Financial Times 2008).

Legal Authority

2

The legal basis for the Italian recapitalization scheme for sound banks was Article 12 of Decree-Law N. 185 of November 29, 2009, converted into Law N. 2/2009 on January 28, 2009 (Bank of Italy 2009c).

On December 18, 2008, Italy notified the European Commission of its recapitalization scheme. The EC approved it on December 23, 2008, after intensive exchanges with Italian officials. The scheme was in line with EU State Aid rules, as a temporary measure and compatible with Article 87 (3)(b) “intended to stabilize the markets as a response to the global financial crisis” (EC 2008d; EC 2008e).

The government expected the scheme to have its first operations by January 2009. However, with no use of the scheme, on February 16, 2009, Italy notified the EC of an amendment, which was approved on February 20, 2009. The amendment became operational on February 25, 2009, with an Italian ministerial decree. On July 31, 2009, Italy requested that the EC prolong its recapitalization scheme until December 31, 2009, which was approved in October 2009 (EC 2009c). Ten months after its expiration, the scheme was reintroduced, on October 23, 2010, and ran until December 31, 2010 (EC 2010b).

Communication

1

In October 2008, in a period of 10 days, multiple high-level government meetings took place intended to coordinate an international response and establish common measures to combat the crisis. The meetings included the ECOFIN on October 7, 2008; the G7 summit in Washington, DC, on October 10; an emergency euro area summit of heads of state on October 12; and the European Council meeting on October 15–16.

The euro area heads of state released the “Declaration on a Concerted European Action Plan of the Euro Area Countries,” which committed efforts to reestablish confidence and promote the sound functioning of the financial system. In agreement with the EC and the European Central Bank, the plan outlined support to financial institutions by facilitating: (a) appropriate liquidity conditions, (b) funding of banks, (c) additional capital resources, (d) recapitalizations of distressed banks, (e) flexibility in the implementation of accounting rules, and (f) cooperation among European countries (Euro Summit 2008). A few days later, the European Council endorsed the plan of action and extended it to all countries part of the European Union (European Council 2008).

By September 2009, the core Tier 1 capital ratio of the largest Italian banks reached 7.3% and by March 2010, 7.6% (Draghi 2010a; Draghi 2010b; see Figure 3). It was generally lower than the ratios of other major European banks. However, Bank of Italy Governor Mario Draghi explained that the differences laid in the substantial public recapitalizations abroad and the more stringent criteria used in Italy to classify regulatory capital. Governor Draghi emphasized that the largest Italian banks held high-quality capital and were less leveraged compared to other major European banks. Nonetheless, through 2009 and 2010, Draghi continued to stress the importance of strengthening capital ratios. In a speech in July 2009, he expressed:

I have said, and I say again, that a strengthening is nonetheless necessary. It is not just a question of maintaining strong safeguards for stability; we must compete on an equal footing with the foreign banks which have had to resort to massive injections of public money in recent months; we must be prepared, as of now, to operate with a capital endowment that future regulations will require to be larger than at present. Above all, capital strengthening is indispensable in order to face the deterioration in the macroeconomic situation without neglecting to give firms, households and the economy the support they need” (Draghi 2009).

Administration

1

The Ministry of Economy and Finance was empowered to inject capital in eligible institutions until December 31, 2009. The Bank of Italy assessed each bank’s solvency, capital adequacy, and risk profile.

Program Size

1

The total available funds for the Italian recapitalization scheme was unspecified but expected to be between €15 billion and €20 billion (EC 2008d). Italian authorities made clear that support would be available “as needed” (Bank of Italy 2009d). In February 2009, when the scheme was amended, the size of the scheme was reported to be up to €12 billion (Reuters 2009a).

Eligible Institutions

1

Eligible institutions included fundamentally sound Italian banks (including subsidiaries of foreign banks) with shares listed in the regulated markets. The Bank of Italy determined if a bank was fundamentally sound by considering available risk indicators. These included: spreads on credit default swaps on subordinated debt (median value not to exceed 100 basis points in the period from January 2007 to August 2008), credit ratings of at least A-, and a complementary assessment by the Bank of Italy (Bank of Italy 2009b; EC 2008c).

In late 2009, when the scheme was prolonged, Italy made additional commitments:

- To inform the EC, at the moment of the recapitalization, of a bank’s risk profile to enable the EC to evaluate its viability and assess whether the bank was fundamentally sound or required restructuring. The material included a review from the Bank of Italy on the soundness and viability of the bank. The EC was provided with any additional information for its assessment of the bank’s viability. Italy committed to submit within six months the relevant information for each bank recapitalized to enable the EC to review the bank’s risk profile and viability so that it could assess if it could still be considered fundamentally sound.

- When a bank applied for a second recapitalization, Italy submitted an individual notification. The EC assessed whether the bank was still considered fundamentally sound or if it required restructuring (EC 2009c).

Capital Characteristics

2

The Italian government, through the MEF, acquired special bonds known as Tremonti bonds, to support banks’ balance sheets. For some commentators, the fact that banks paid interest on the bonds gave the scheme a more market-orientated feel compared to other European schemes in which banks were nationalized (Markit 2009). The Tremonti bonds were designed to have the same characteristics as common shares in order to qualify as core Tier 1 capital. They had the same degree of subordination and same ability to absorb losses, both in case of insolvency or when losses reduced total capital ratios below the regulatory minimum of 8%.

Tremonti bonds were perpetual and convertible into common shares after three years. Interest was noncumulative and paid only if there were distributable earnings, provided the total capital ratio was at least 8%. Public bank recapitalizations were limited to 2% of a bank’s risk-weighted assets, without surpassing an 8% Tier 1 capital ratio (Bank of Italy 2009b).

Banks could redeem the Tremonti bonds, given authorization by the Bank of Italy, by paying a premium on the face value, which could increase over time in relation to the market value of the bank’s shares. The conversion ratio of Tremonti bonds into shares was fixed based on the average share price of the last 10 trading days before the issue (Bank of Italy 2009b).

The remuneration conditions were designed in line with EU State Aid rules to be temporary, to encourage an early exit. The EC recommended an indicative range based on the type of instrument. For subordinated debt, such as preferred shares, the EC recommended an average required rate of return of 7%. For common shares, the EC recommended an average required rate of return of 9.3% (EC 2008c).

The conditions aimed to ensure an adequate remuneration for the government and protect the interests of taxpayers. Additionally, to minimize distortive effects of recapitalizations, remuneration included an initial coupon with fixed step-up clauses, increases in remuneration associated with dividend payments and the government’s financing costs, and a redemption price premium that increased over the years. To encourage early redemption by banks once the crisis was over, the redemption price was set higher than the nominal value and increased over time (see Figure 4) (Bank of Italy 2009b; EC 2008d; EC 2008e).

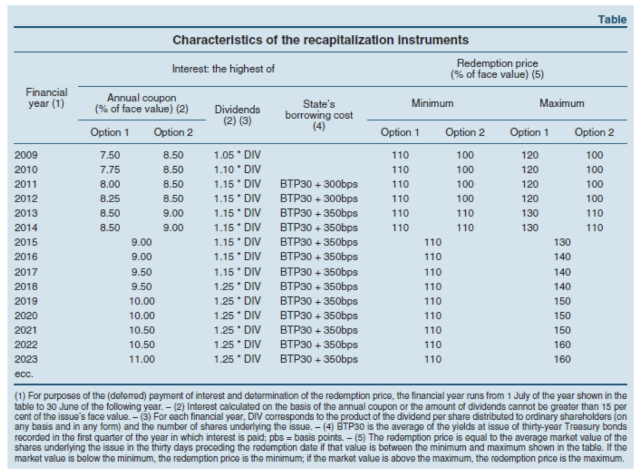

When the recapitalization scheme was introduced in December 2008, the Italian government set the annual rate of return on the bonds at 7.5% for the first six months. Thereafter, it was the highest of these three options:

- A predetermined annual coupon, increasing over time: 7.5% in 2009, 7.75% in 2010, 8% in 2011, 8.25% in 2012, and 8.5% in 2013–2014. Then, it rose in increments of 0.5% every two years (9% in 2015–2016, 9.5% in 2017–2018, etc.), up to 15% in 2039;

- An amount equal to the product of the dividend per share distributed to common shareholders and the number of shares. This amount rose by an increasing percentage over time: 105% of dividends—in whatever capacity and in any form paid—in relation to 2009 profits, 110% for 2010, 115% for 2011–2017, and 125% for 2018 and following years; or

- The average yield on 30-year Italian Treasury bonds (buoni del Tesoro poliennali, or BTPs) increased by a spread. Starting in 2011, the yield at the issuance of the 30-year BTP increased by 300 basis points, then, starting in 2013, the 30-year BTP yield increased by 350 basis points (EC 2008e).

For the second option introduced in February 2009, the interest rate was higher, starting at 8.5%. Thereafter, the interest rate was the highest of the following three elements:

- A predetermined annual coupon, increasing over time: 8.5% in 2009–2012, 9% in 2013–2016, and then rising in increments of 0.5% every two years (9.5% for 2017–2018 and so forth, up to 15% for 2039);

- An amount equal to the product of the dividend per share distributed to common shareholders and the number of shares. This amount rose by an increasing percentage over time: 105% of the dividend—in any capacity and in any form paid—in relation to 2009 profits, 110% in 2010, 115% for 2011–2017, and 125% for 2018 and following years, with a maximum limit of 15% of the nominal value; or

- The average yield on 30-year BTPs increased by a spread. Starting in 2011, the issuing yield of the 30-year BTPs increased by 300 basis points, then, starting in 2013 and for the following years, the 30-year BTP yield increased by 350 basis points (EC 2009b).

Additionally, provisions were in place whereby the government could accept a lesser remuneration, but only in cases where at least 30% of the bank’s issuance was subscribed by private investors (at least two-thirds other than shareholders owning 2% or more of the share capital) on equal terms with the Italian government. In any case, the yield had to be at least 200 basis points above the average yield of 30-year BTPs (Bank of Italy 2009b; EC 2009a).

For the first option, the redemption price was the higher of 110% of the nominal value at issuance or the market value of the bank shares in circulation. The redemption price was set within a percentage value of the nominal value equal to 120% in the event of redemption by June 30, 2013; 130% between July 1, 2013, and June 30, 2016; 140% between July 1, 2016, and June 30, 2019; 150% between July 1, 2019, and June 30, 2022; and 160% in case of redemption from July 1, 2022, onwards (EC 2008e).

For the second option, the redemption price was set within a percentage value of the nominal value equal to 100% in the event of redemption by June 30, 2013, and 110% in the event of redemption between July 1, 2013, and June 30, 2015. For the following years, the redemption price was set as the higher of: 110% of the nominal value of the Tremonti bonds at issuance or the market value of the bank shares in circulation, with a maximum limited to a percentage of the nominal value equal to 130% in the event of redemption between July 1, 2015, and June 30, 2016; 140% between July 1, 2016, and June 30, 2019; 150% between July 1, 2019, and June 30, 2022; and 160% from July 1, 2022, onwards (EC 2009b).

EC Competition Commissioner Neelie Kroes mentioned that “The Italian authorities have asked permission to modify the design of their scheme to make it more attractive to sound banks that are willing to use the state capital only for a very short period of time” (EC 2009a). The first option of remuneration consisted of lower coupon payments and higher redemption prices up to 2014, while the second option consisted of an alternative remuneration option with a higher initial coupon and a higher annual level of the coupon until 2014. Starting in 2015, the two schemes had identical characteristics (see Figure 4).

Figure 4: Tremonti Bonds—the Two Options for Remuneration

Source: Bank of Italy 2009b.

Source: Bank of Italy 2009b.

Other Conditions

1

Banks participating in the government recapitalizations had to adhere to a code of ethics for policies on executive compensation. Additionally, banks had to sign a Memorandum of Understanding, that committed to: (a) increase lending for the next three years to small and medium-sized enterprises; (b) contribute to the guarantee fund for loans granted to SMEs; (c) suspend up to 12 months of mortgage payments for borrowers who lost their jobs or benefited from public income support; and (d) ensure appropriate liquidity levels to creditors of public administrations.

The commitments of the MoU remained valid until the bank redeemed the Tremonti bonds to the government. Banks were required to provide aggregated data on a quarterly basis to enable monitoring of compliance. The Bank of Italy assessed the bank’s compliance with capital requirements (i.e., Tier 1) and its profitability. In line with the EU State Aid guidelines, limits were set on the expansion of a bank’s assets, and additional conditions were set to prevent banks from misusing public support (Bank of Italy 2009a; Bank of Italy 2009b).

In 2010, Italian authorities expressed that the Italian recapitalization scheme “exhibited satisfactory performance in its implementation, providing a safety net that corresponds well to market needs and ensuring the provision of lending to the real economy” (EC 2010b).

The core Tier 1 capital ratio of the largest Italian banks stood at 5.8% by the end of 2008 and increased in the first three months of 2009 (Draghi 2009; Draghi 2010a). Premiums on credit default swaps had risen, but announcements by major Italian banks of their intention to use the recapitalization scheme and increases in profits contributed to reduction of the premiums by more than half (Bank of Italy 2009c).

In February 2010, Italy’s central bank Governor Mario Draghi expressed that Italian banks were “well placed to cope with the international environment.” Draghi noted that their capital bases were strengthened by the issue of shares, disposal of noncore assets, the ploughing back of profits, and in some cases, government interventions (Draghi 2010a).

The scheme expired on December 31, 2009; however, it was reintroduced 10 months later, on October 23, 2010, and ran until December 31, 2010. The Italian government cited protracted effects of the Global Financial Crisis and recent results of stress tests performed by the Committee of European Banking Supervisors (EC 2010a; EC 2010b).

In light of the new regulatory framework applied to all EU member countries in 2014 on capital requirements, as of this writing, it seems very difficult that the Tremonti bonds could be considered eligible as common equity Tier 1 (CET1) and additional Tier 1 (AT1) instruments, due to their remuneration features incentivizing early redemption and usage for only a short period (European Parliament and Council of the European Union 2013). A representative from the Bank of Italy, in discussing the features of the Tremonti bonds, pointed out that, in principle, instruments with standard, noncomplex features were preferable for capital injection as they allowed for greater comparability, better pricing, and clearer loss-absorption mechanisms.

- Banca Montepaschi di Siena (MPS). 2009. “10 Billion Euros to Italian Small and …

- Banca Popolare di Milano (BPM). 2009. “Bipiemme: Tremonti Bond Issue.” Press re…

- ———. 2013. “Bank of Italy Authorises the Full Redemption of Tremonti Bonds and …

- Banco Popolare (BP). 2009a. “Banco Popolare Files a Formal Request for the Issu…

- ———. 2009b. “Clarification on Issue of Financial Instruments under LD 185/08.” …

- ———. 2009c. “Banco Popolare and the Italian Treasury Signed the Memorandum on C…

- ———. 2009d. “Financial Instruments Issued in Favor of the Ministry for Economy …

- ———. 2011. “Tremonti Bonds Fully Redeemed.” News release, March 14, 2011.

- Bank of Italy. 2008. “Economic Bulletin No. 50.” Rome: Banca d’Italia, October …

- ———. 2009a. “Economic Bulletin No. 51.” Rome: Banca d’Italia, January 2009.

- ———. 2009b. “Economic Bulletin No. 52.” Rome: Banca d’Italia, April 2009.

- ———. 2009c. 2008 Annual Report. 115th Financial Year. Rome: Banca d’Italia, May…

- ———. 2009d. “An Assessment of Financial Sector Rescue Programmes,” edited by Fa…

- ———. 2010. 2009 Annual Report. 116th Financial Year. Rome: Banca d’Italia, May …

- ———. 2011. 2010 Annual Report. 117th Financial Year. Rome: Banca d’Italia, May …

- Bartiloro, Laura, Luisa Carpinelli, Paolo Finaldi Russo, and Sabrina Pastorelli…

- Council of the European Union (European Council). 2008. “Council of the Europea…

- Credito Valtellinese (Creval). 2009. “Issue of Financial Instruments, Art. 12, …

- ———. 2013. “The Bank of Italy Releases Authorisation for the Early Redemption o…

- Draghi, Mario. 2009. “Address by the Governor of the Bank of Italy, Mario Dragh…

- ———. 2010a. “Speech by the Governor of the Bank of Italy, Mario Draghi.” 16th A…

- ———. 2010b. “Bank of Italy Governor’s Concluding Remarks.” Banca d’Italia Ordin…

- Economist. 2009. “Italy’s Debt Burden.” February 11, 2009.

- Euro Summit. 2008. “Declaration on a Concerted European Action Plan of the Euro…

- European Central Bank (ECB). 2008. “Recommendations of the Governing Council of…

- European Commission (EC). 2008a. “State Aid: Commission Gives Guidance to Membe…

- ———. 2008b. “The Application of State Aid Rules to Measures Taken in Relation t…

- ———. 2008c. “The Recapitalisation of Financial Institutions in the Current Fina…

- ———. 2008d. “State Aid: Commission Approves Italian Recapitalisation Scheme for…

- ———. 2008e. “State Aid N 648/2008 Italy. Italian Bank Recapitalisation Scheme.”…

- ———. 2009a. “State Aid: Commission Authorises Amendment of Italian Scheme to In…

- ———. 2009b. “State Aid N 97/2009 Italy. Amendment of Italian Bank Recapitalisat…

- ———. 2009c. “State Aid N 466/2009 Italy. Prolongation of the Recapitalization S…

- ———. 2010a. “Publication of the Results of the EU-Wide Stress-Testing Exercise…

- ———. 2010b. “State Aid N 425/2010 Italy. Re-Introduction of the Italian Recapit…

- European Economic and Financial Affairs Council (ECOFIN). 2008. “2894th Council…

- European Parliament and Council of the European Union. 2006. “Directive 2006/49…

- ———. 2013. “Regulation (EU) No 575/2013 of the European Parliament and of the C…

- Financial Times. 2008. “Rome’s Fiscal Stimulus Comes under Fire.” November 17, …

- ———. 2009. “Banca Popolare Receives €500m State-Backed Boost,” September 21, 20…

- Group of Seven (G7). 2008. “G7 Finance Ministers and Central Bank Governors Pla…

- Italian News. 2009. “Monte Paschi Receives Green Light to Issue Govt-Backed Bon…

- Markit. 2009. “Italian Government Approves Banking Support Measures.” IHS Marki…

- Mayer Brown. 2009. “Summary of Government Interventions in Financial Markets: I…

- Petrovic, Ana, and Ralf Tutsch. 2009. “National Rescue Measures in Response to …

- Reuters. 2009a. “Italy OKs Bonds Measure to Boost Bank Capital.” February 25, 2…

- ———. 2009b. “Italy Bank Recapitalisation Uptake Too ‘Relaxed.’” May 19, 2009.

- ———. 2009c. “Monte Paschi Wins Approval for $2.8 Bln State Bonds.” December 16,…

Key Program Documents

-

(EC 2008a) Recapitalisation Communication

Communication provided by the European Commission on the recapitalization of financial institutions during the financial crisis: limitation of aid to the minimum necessary and safeguards against undue distortions of competition.

-

(European Commission, October 7, 2008) Press Release of the 2894th The European Economic and Financial Affairs Council (ECOFIN) Meeting

The Council agreed on a coordinated approach in response to the financial crisis.

-

(Petrovic and Tutsch 2009) National Rescue Measures in Response to the Current Financial Crisis

A comprehensive overview of measures introduced by the 27 EU Member States from October 2008 through June 2009.

Appendix: Timeline

|

Date |

Event |

Description |

|

Oct./07/2008 |

The European Economic and Financial Affairs Council (ECOFIN) met to plan a response to the global financial crisis |

The ECOFIN approved a set of principles and extraordinary measures for European governments to combat the crisis (ECOFIN 2008). |

|

Oct./09/2008 |

Italy issued Decree-Law N. 155. |

Decree-Law N. 155, “Urgent Measures to Guarantee the Stability of the Credit System and the Continued Flow of Credit to Firms and Consumers in the Current State of Crisis in World Financial Markets.” The decree envisaged a government package focused on three areas of support to the Italian banking sector: (a) bank recapitalizations, (b) access to liquidity, and (c) expanded guarantees on bank deposits (Bank of Italy 2008). |

|

Oct./10/2008 |

Group of Seven (G7) summit convened in Washington DC. |

The G7 finance ministers and central bank governors pledged to take aggressive actions that included: support for systemically important financial institutions, all necessary efforts to ensure credit access to banks, temporary guarantees on short- and medium-term liabilities, expansion of guarantees on bank deposits, bank recapitalization through the use of public funds, and acquisition of illiquid assets (G7 2008). |

|

Oct./12/2008 |

Euro summit of heads of state held in Paris. |

The euro area heads of state released the “Declaration on a Concerted European Action Plan of the Euro Area Countries,” which committed efforts to reestablish confidence and the well-functioning of the financial system. In agreement with the European Commission (EC) and the European Central Bank (ECB), the plan outlined support to financial institutions by facilitating: (a) appropriate liquidity conditions, (b) funding of banks, (c) additional capital resources, (d) recapitalizations of distressed banks, (e) flexibility in the implementation of accounting rules, and (f) cooperation among European countries (Euro Summit 2008). |

|

Oct./13/2008 |

The European Commission released the “Banking Communication.” |

The European Commission provided guidance on the application of State Aid measures for banks in the context of the Global Financial Crisis. It highlighted that recapitalization schemes were important measures member states could take to preserve financial stability and proper functioning of financial markets (EC 2008a; EC 2008b). |

|

Oct./15-16/2008 |

The Council of the European Union (European Council) met in Brussels. |

The European Council endorsed the plan of action and extended it to all countries part of the European Union (European Council 2008). |

|

Nov./20/2008 |

ECB released a recommendation on the pricing of bank recapitalizations. |

See ECB 2008. |

|

Nov./29/2008 |

Italy passes Decree-Law N. 185/2008 |

Article 12 of Decree-Law N. 185 of November 29, 2009 became the legal basis for the Italian recapitalization scheme. It was converted into Law N. 2/2009 on January 28, 2009 (Bank of Italy 2009c). |

|

Dec./02/2008 |

The ECOFIN anticipated the need for further recapitalizations. |

The ECOFIN expressed that it “recognized the need for further guidance for precautionary recapitalizations to sustain credit, and called for its urgent adoption by the European Commission” (EC 2008c). |

|

Dec./05/2008 |

The European Commission released a communication for recapitalization schemes. |

“The Recapitalisation of Financial Institutions in the Current Financial Crisis: Limitation of Aid to the Minimum Necessary and Safeguards against Undue Distortions of Competition” communication provided guidance for new recapitalization schemes and adjustments of existing ones (EC 2008c). |

|

Dec./23/2008 |

The EC approved European Union (EU) State Aid case N 648/2008. |

Recapitalization measures in favor of the Italian banking sector (EC 2008e). |

|

Feb./20/2009 |

The EC approved amendments to EU State Aid, case N 97/2009. |

The European Commission approved amendments to the Italian recapitalization scheme to offer a second offer of remuneration, more attractive for banks that planned to use the government capital for a short period (EC 2009b). |

|

July/31/2009 |

First capital injection and Italy’s request that the EC prolong its recapitalization scheme (EC 2009c). |

Banco Popolare (BP) became the first bank to receive a capital injection for €1.45 billion (EC 2010b). |

|

Oct./06/2009 |

The EC approved a prolongation of the scheme until December 31, 2009. State Aid case N 466/2009. |

See EC 2009c. |

|

Aug./05/2010 |

Italian Decree-Law N. 125, Art. 2.1. Published in the Italian Official Journal 182. |

The passage became the legal basis for the Italian recapitalization scheme (EC 2010b). |

|

Oct./21/2010 |

EC approved the reintroduction of the Italian recapitalization scheme. State Aid case N. 425/2010. |

The scheme expired on December 31, 2009. Italy requested that the EC reintroduce the scheme until December 31, 2010 (EC 2010b). |

Taxonomy

Intervention Categories:

- Broad-Based Capital Injections

Countries and Regions:

- Italy

Crises:

- Global Financial Crisis