Market Support Programs

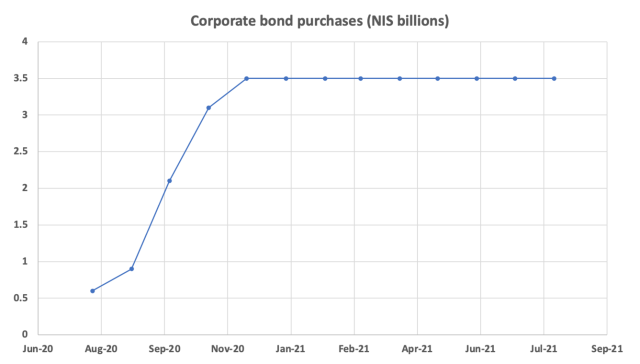

Israel: Corporate Bond Purchase Program

Purpose

To “ensure the continued orderly functioning of the corporate bond market, and to strengthen the passthrough from monetary policy to the credit market, by reducing the interest rate at which companies issue credit in the capital market, and making additional sources of credit available for all industries” (BoI 2020h).

Key Terms

-

Launch DatesAuthorized: July 6, 2020 Announced: July 6, 2020

-

Operational DateJuly 31, 2020

-

End DateDecember 2021

-

Legal AuthorityBank of Israel Law of 2010, Section 36

-

Source(s) of FundingBoI balance sheet

-

AdministratorBank of Israel Markets Department/Trading Desk

-

Overall SizeNIS 15 billion

-

Eligible Collateral (or Purchased Assets)NIL-issued nonconvertible Israeli corporate bonds rated A- or above

-

Peak UtilizationNIS 3.5 billion (USD 1.1 billion)

Key Design Decisions

Purpose

Part of a Package

Governance

Administration

Communication

Disclosure

SPV Involvement

Program Size

Source(s) of Funding

Eligible Institutions

Auction or Standing Facility

Loan or Purchase

Eligible Collateral or Assets

Loan Amounts (or Purchase Price)

Haircuts

Interest Rate

Fees

Term

Other Conditions

Regulatory Relief

International Cooperation

Duration

Key Program Documents

Taxonomy

Intervention Categories:

- Market Support Programs

Countries and Regions:

- Israel

Crises:

- COVID-19