Broad-Based Asset Management Programs

Indonesia: IBRA’s Asset Management Unit/ Asset Management of Credits

Purpose

Managing the most severe nonperforming loans from banks involved with IBRA

Key Terms

-

Launch DatesAnnouncement date: January 27, 1998 Operational date: Fall 1998

-

Wind-down DatesDisposal: February 27, 2004

-

Size and Type of NPL Problem75% of total loans in 1998 Commercial; corporate

-

Program SizeNot specified at outset

-

Eligible InstitutionsBanks participating in the country’s recapitalization program Closed- and open-bank

-

UsageApproximately IDR 400 trillion in face value of loans by April 2003

-

OutcomesAverage recovery rate for assets between 1999 and 2004 was approximately 25%

-

Ownership StructureGovernment-owned

-

Notable FeaturesIndonesian officials vested IBRA with extrajudicial powers to seize assets of uncooperative debtors

In 1998, Indonesia’s banking sector was undercapitalized, under regulated, and suffering from an excess of nonperforming loans (NPLs). In response, the Indonesian government devised the Indonesian Bank Restructuring Agency (IBRA) and its Asset Management Unit/Asset Management of Credits (AMU/AMC) as part of a three-pronged government emergency plan, along with a blanket guarantee of the debts of all domestic banks and a framework for corporate restructuring. The AMU/AMC acquired and managed nonperforming loans from a variety of Indonesian banks and attempted to dispose of them. The AMU/AMC had acquired nearly IDR 400 trillion (approximately $86 billion) in face value of loans by April 2003. Throughout its history, the organization encountered political interference, transfer issues, documentation problems, and problems with legal authority that impeded its effective operation. Although the AMU/AMC was wound down on its initially scheduled end date of February 27, 2004, its functions and many unresolved legal cases were simply shifted to a new asset management company under the Ministry of Finance.

|

GDP per capita (SAAR, Nominal GDP in LCU converted to USD) |

$1,064 in 1997 $464 in 1998 |

|

Sovereign credit rating (5-year senior debt)

|

As of Q4, 1997: Fitch Rating: BB+ |

|

Size of banking system

|

$105.50 billion in 1997 $44.96 billion in 1998 |

|

Size of banking system as a percentage of GDP

|

46.60% in 1997 45.77% in 1998 |

|

Size of banking system as a percentage of financial system

|

100% in 1997 100% in 1998 |

|

5-bank concentration of banking system

|

48.98% in 1997 60.27% in 1998 |

|

Foreign involvement in banking system |

Data not available for 1997 or 1998 |

|

Government ownership of banking system

|

Data not available for 1997 or 1998 |

|

Existence of deposit insurance |

Yes |

|

Sources: Bloomberg; World Bank Global Financial Development Database; World Bank Deposit Insurance Dataset. |

In the years leading up to the Asian Financial Crisis of 1997, Indonesian firms became increasingly reliant on short-term funding denominated in foreign currencies. Indonesia’s banks, moreover, were undercapitalized, poorly supervised, and engaged in heavy lending to affiliated companies and politically favored enterprises. Following the collapse of the Indonesian rupiah in mid-1997, the country’s banking system was in crisis.

In early 1998, the government devised the Indonesian Bank Restructuring Agency (IBRA) and subsequently its Asset Management Unit/Asset Management of Credits (AMU/AMC) as part of a three-pronged emergency plan, along with a blanket guarantee of the debts of all domestic banks and a framework for corporate restructuring, to deal with problems in the Indonesian banking sector. Banks that came under IBRA’s umbrella would transfer nonperforming loans to the AMU/AMC at zero value, with any proceeds ultimately returned to the banks to be used in repaying government assistance. The organization disposed of loan assets according to size. AMU/AMC was belatedly empowered after creation with expanded legal powers and the ability to escalate actions taken against the largest defaulting borrowers, which included regularly publishing the names of recalcitrant debtors.

The AMU/AMC ultimately acquired almost IDR 400 trillion (approximately $86 billion) in face value of loans. It wound down on its initially scheduled end date of February 27, 2004, but the organization’s functions and its many unresolved legal cases were simply shifted to a new asset management company under the Ministry of Finance.

IBRA has been criticized for not being as effective at managing and recovering assets as it might have been due to a combination of factors, including political interference, transfer issues, documentation problems, and problems with legal authority. The average recovery rate for assets between 1999 and 2004 was approximately 25%.

Key Design Decisions

Part of a Package

1

The emergency plan introduced by the government on January 27, 1998, in response to worsening conditions in the Indonesian banking sector and pressure from the IMF, entailed a blanket guarantee of the debts of all domestic banks, a framework for corporate restructuring, and the establishment (for a five-year period) of IBRA, which would function as a new regulatory agency for the banking industry under the auspices of the Ministry of Finance (Sharma 2001). IBRA also took on assets from banks slated for liquidation and from institutions requesting recapitalization.

The blanket guarantee was an attempt to stem the bank runs that were then destabilizing the system. It covered deposits and most other creditor claims (excluding subordinated debt) of domestically incorporated banks, whether denominated in rupiah or foreign currencies. The framework for corporate restructuring, meanwhile, called for a voluntary, temporary suspension of payments on corporate external debt. “However, the government made it clear that there would be no use of public financing, guarantee, or subsidy to erase the debt and reimburse unguaranteed creditors looking for financial redress” (Sharma 2001).

The share of corporate debt held by foreign private banks, roughly two-thirds, influenced Indonesia’s corporate restructuring strategy (Iskander et al. 1999). Indonesia officials met with its biggest foreign creditors in Frankfurt, Germany, in June 1998 and reached an agreement to offer foreign exchange cover for Indonesian companies with foreign-currency-denominated debt (after reaching debt restructuring agreements) (Iskander et al. 1999; Sharma 2001). Then, in September 1998, the Indonesian government introduced the Jakarta Initiative and the Jakarta Initiative Task Force to facilitate voluntary negotiations between parties for corporate restructuring and to secure necessary regulatory approval for deals (Sharma 2001). Additionally, changes to bankruptcy law were introduced in August 1998 that improved efficiency, transparency, and, among a variety of over revisions, placed limitations on secured creditors’ ability to foreclose on collateral during proceedings, “thus making reorganizations more likely” (Iskander et al. 1999).

In short, IBRA was in charge of restructuring corporate borrowers’ debt held by state banks and recapitalized banks, while the Jakarta Initiative handled corporate borrowers’ foreign debts (Bank Indonesia 2001).

Legal Authority

1

On January 26, 1998, the Decree of the President of the Republic of Indonesia No. 27 established IBRA for a period of five years under the auspices of the Ministry of Finance (Decree No. 27 1998). The AMU/AMC was in turn established under the auspices of IBRA as a separate asset management entity (Sharma 2001). Despite this authorization, the absence of certain powers hampered IBRA’s effectiveness, particularly when its goals were at odds with entrenched political and business interests.

Specifically, IBRA did not have the necessary ability to transfer assets or to foreclose on collateral. Provisions of the Law No. 10 of 1998 (the Banking Law) passed in October 1998 solidified the legal basis for the organization’s activities (IBRA 1999). These amendments to Section 37A of the Banking Law strengthened the legal powers of both IBRA and the AMU/AMC, empowering them with the ability to transfer assets and foreclose against a nonperforming debtor (Lindgren et al. 1999; IBRA 1999).

IBRA also faced challenges through the court system, “where—even after a challenge to the constitutionality of IBRA's powers was dismissed—IBRA's bankruptcy petitions were rejected by judge after judge” (Enoch et al. 2001). IBRA finally began winning these cases in mid-2000 (Enoch et al. 2001).

Legal and regulatory mechanisms were often unable to make up for powerful political and business interests. An IMF analyst estimated that the top 10 families in Indonesia in the late 1990s controlled corporations worth more than half the country's market capitalization (Iskander et al. 1999). Many of the bank shareholders were prominent individuals with strong political connections who appear to have kept IBRA from enforcing agreements, despite the entity possessing strong enforcement mechanisms (IMF Staff 2004). For example, IBRA took over one of the country’s largest banks, BDNI, and, under the Jakarta Stock Exchange rules, needed a declaration of insolvency for the bank to be able to write down shareholders’ stakes. BDNI’s shareholders were able to utilize technical procedures to prevent the declaration (Enoch 2000). Well-connected businessmen, particularly those in contact with the former president Suharto’s family, were able to delay IBRA’s plans too (Omori 2014).

Last, IBRA was “subject to considerable political interference,” with some restructuring agreements seeming to “focus on meeting employment or national interest concerns, rather than placing the firm on a commercially viable footing” (IMF Staff 2004). The “prospective redistribution of wealth in Indonesia was so substantial that the vested interests that IBRA encountered were pervasive across its operations” (Enoch et al. 2001).

Special Powers

1

Policymakers eventually equipped IBRA with so-called PP17 powers in October 1999 to “drive debt without judicial rulings” (Gooptu et al. 2000). IBRA, like any other creditor, could use the normal bankruptcy process, but the PP17 powers allowed IBRA to seize assets of uncooperative debtors. IBRA initially used these powers two months later in December to seize 14 hectares of property from PT Sinar Slipi Sejahtera, a debtor firm owned by former president Suharto's daughter (Gooptu et al. 2000).

Still, statements made in subsequent years by an IBRA chairman suggested the seizure powers were not used often. During a meeting with a government committee in 2003, then–IBRA chairman Syafruddin A. Temenggung complained that IBRA was generally unable to exercise these powers. Temenggung stated that of 76 attempted seizures, only three were successful, with the country’s courts ruling against the rest (Tempo 2004).

Mandate

1

The AMU/AMC ran the “loan workout on the transferred loans to maximize their return” (Bank Indonesia 1999). Because of the large volume of transferred assets, policymakers also gave the AMU/AMC the ability to subcontract certain loan management to eligible banks. Last, proceeds from loan repayment were used to dilute the size of government stocks in participating financial institutions (Bank Indonesia 1999).

Communication

1

The closure of 16 banks in November 1997 as part of the original IMF agreement contributed to a run on the Indonesian banking system. The Indonesian government later determined not to publicize the early operations of IBRA following its establishment in January 1998. Specifically, a last-minute decision was made not to publicly disclose the February 1998 move to bring 54 banks under IBRA’s umbrella (Enoch 2000). This initial misstep “failed to strengthen market sentiment” (IMF Staff 2004) and caused the public to perceive of IBRA as a nonoperational “paper tiger” during the preliminary stages of its operations (Sharma 2001). The lack of publicity also seems to have undermined the status of IBRA officials working onsite at those banks subject to the operation (Enoch 2000).

Still, Indonesia appointed a new IBRA team in March 1998, which acknowledged the need for “transparency and uniformity of treatment of the banks” and publicity for its decisions (Enoch 2000). This strategy shift included hiring public relations professionals that helped the institution communicate its interventions and decisions (Enoch 2000). In 1999, IBRA officials stated the goal of the agency’s communication strategy was to “maintain support from the public at large for IBRA through providing correct, timely and complete information on IBRA and its activities” (IBRA 1999).

Ownership Structure

1

Omori (2014) writes that despite “the IMF’s suggestion that the IBRA should be an autonomous body, [it] was placed under the MOF’s authority and was thus dependent upon the ministry” (Omori 2014). Still, BI called IBRA “autonomous” in an annual report (Bank Indonesia 1998).

Governance/Administration

1

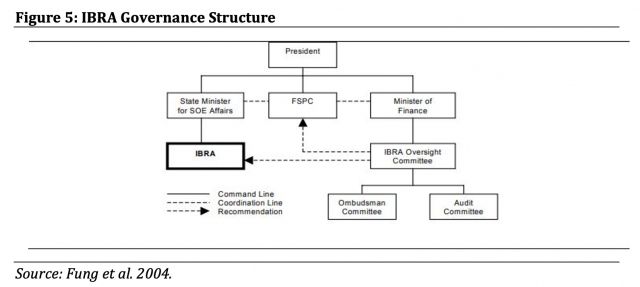

A senior official from the MOF was appointed to head IBRA, and several hundred staff members from the MOF and BI were assigned to it as staff (Enoch 2000).

The state-owned enterprises minister and the Financial Sector Policy Committee (FSPC) oversaw IBRA. The FSPC was a government body chaired by the Coordinating Minister of Economy “to decide and coordinate government policies on the financial system” (Fung et al. 2004). Its members included the ministers of finance and trade and industry and the state ministers of national planning and state-owned enterprise (Fung et al. 2004; IBRA 1999).

The Oversight Committee (OC), which was set up by and reported to the FSPC, met at least weekly and monitored IBRA’s performance and provided independent review of IBRA’s restructuring. The OC made recommendations about matters such as transparency and asset disposals. The body consisted of nine members, including a former minister of finance, the chairman of IBRA, and representatives from the private sector and the academic world (Fung et al. 2004). Officials tasked the OC with independent review of the largest corporate restructuring transactions prior to their submission to the government for final approval. Policymakers gave the OC the new mandate as they strengthened corporate debt restructuring principles in 2001 in response to criticism regarding generous restructuring terms to some of IBRA’s largest debtors. The OC’s recommendations were not binding, but the mere publishing of them “meant that the final restructuring terms agreed by the government would be subjected to somewhat greater public scrutiny” (IMF Staff 2004).

OC reports do not appear to be publicly available, but a September 2001 news report from the Jakarta Post suggests that officials created a public website meant to house the OC’s reviews and activities (Jakarta Post 2001).FThe web address the article gives does not lead to a working website, and web archive searches do not reveal archived versions of the website. This web page may have been part of a larger website that IBRA officials operated that acted as a general information center for the public (IBRA 1999).

Policymakers established the Audit Committee, a standing committee of the OC that included five independent professionals, “to enhance the standard of financial reporting by IBRA and to ensure standards of corporate governance and control” (Fung et al. 2004). Internal audit was formed later in 1998 to ensure transparency. Additionally, IBRA employed independent public accountants to audit its financial statements (Fung et al. 2004). Figure 5 illustrates the governance structure for IBRA.

A number of external, independent parties, including the House of People’s Representatives and the Supreme Audit Agency, possessed the right to conduct reviews and audits of IBRA’s operational activities (IBRA 1999). The extent to which external parties did so is unclear with available documents.

Despite its ostensible independence, IBRA faced regular political interventions, often at the highest levels. At the beginning of the entity’s existence, President Suharto refused to publicize certain IBRA operations and fired a BI governor and the head of IBRA (Sharma 2001). President Suharto’s successor later threatened to reverse the joint recapitalization plan and instead briefly pushed for forced mergers (Lindgren et al. 1999).

Additionally, IBRA has been described as “needing to obtain political authority even for its technical operations” (Enoch 2000). This stems partly from the fact that IBRA was subject to the influence of many political entities, from the BI to Parliament and the IMF, because of its broad mandate (Fung et al. 2004). Smaller levels of political and bureaucratic interference can be seen in IBRA’s initial relationship with the BI, whose staff members saw IBRA “as an indictment of their record” and were at times uncooperative (Enoch 2000).

One of IBRA’s biggest errors resulted in part from both political intervention and governance failures. Bank Bali, one of the country’s largest banks, made side payments to a government-connected firm to receive payments under the inter-bank guarantee to close its capital shortfall and gain access to the recapitalization program. The fallout was broad. IBRA and BI officials were fired, and criminal charges were brought against “intermediaries, although no convictions were secured” (Enoch et al. 2001). This scandal led the IMF to suspend its funding to Indonesia in September 1999 (Sharma 2001).

The political storm surrounding the so-called BLBI bonds is another example. These bonds were used as liquidity assistance by BI to provide emergency loans to banks that experienced liquidity problems during the Asian crisis (Fung et al. 2004). Pangestu (2003) writes that there “are many controversies surrounding the issuance of BLBI bonds regarding the size of the liquidity support that could be much larger than the asset[s] of the troubled bank itself; and that the assets pledged by the bank owners and shareholders in return to the support given by Bank Indonesia being significantly less than the amount of liquidity support received by these banks.” An investigative audit by the country’s Supreme Audit Agency found that trillions of rupiah issued in 1997 to 1998 were misused by the recipient banks, “most of which were owned by cronies or relatives of Soeharto [sic]” (Stern 2004). Stern (2004) argues the “issue of whether Bank Indonesia management should have behaved differently . . . will not be easily resolved.” The controversy has continued. In recent years, the government has brought charges against former IBRA chairman Temenggung and others (Hasbullah 2019).

Together, these problems contributed to major turnover among senior staff, including seven different chairmen in a four-year period (Fung et al. 2004).

Program Size

1

Available documentation does not suggest policymakers established size limits for IBRA’s AMU/AMC. The AMU/AMC ultimately acquired almost IDR 400 trillion in face value of loans (Fung et al. 2004; IMF Staff 2004).

Funding Source

1

As of mid-1999, the Indonesian public spent, in total, $85 billion USD on the financial system restructuring efforts, with most of the funds paying for recapitalization and liquidity support (Lindgren et al. 1999). IBRA was financed by a combination of both medium- and long-term government-guaranteed bonds paying an average of 14% annually in interest; some of these bonds were inflation indexed (Sharma 2001).

All cash recovered from IBRA’s operations, after expense deductions, was transferred to reduce the state budget deficit (Fung et al. 2004).

Eligible Institutions

1

The Indonesian government established IBRA in part to oversee the closure of banks that were deemed too insolvent to be eligible for assistance. Indonesian policymakers separated banks into three categories based on independent audits of all state, nationalized, regional, and private banks (Sharma 2001). The categories are detailed in the Program Description section of this study. Banks participating in the recapitalization program were required to transfer some of their bad assets to the AMU/AMC, the selection of which is detailed in Key Design Decision No. 11, on eligible assets (Bank Indonesia 1999). As part of the closure of chosen banks, assets were transferred to the AMU/AMC to manage (Sharma 2001).

Eligible Assets

1

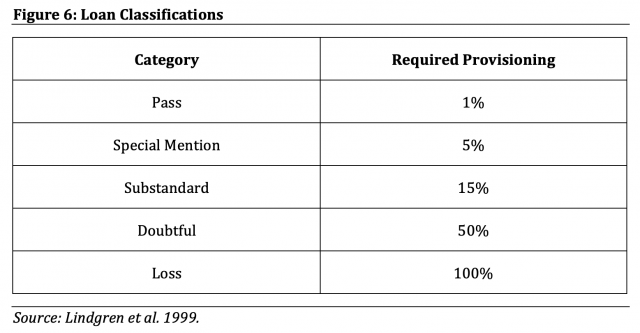

New regulations passed in December 1998 established five categories for the classification of loans, as shown in Figure 6.

The AMU/AMC managed loans in all categories from the banks IBRA closed. Banks participating in IBRA’s joint recapitalization program had to transfer Category 5 loans to the AMU/AMC. The banks could also opt to transfer their Category 4 loans (Bank Indonesia 1999).

Corporate loans made up approximately 84% of IBRA’s loan portfolio, which also included retail and SME debt at about 8% and commercial loans at about 8% (IMF Staff 2002).

Acquisition - Mechanics

1

There were limitations on the size of the loans the AMU/AMC handled directly. The AMU/AMC subcontracted management of bad loans valued between IDR 5 billion and IDR 25 billion back to the individual banks and supervised their efforts. Individual banks remained responsible for handling loans of less than IDR 5 billion. The AMU/AMC directly handled only those loans of greater than IDR 25 billion (Sharma 2001).

Acquisition - Pricing

1

Banks transferred nonperforming loans to the AMU/AMC at no cost, but any proceeds realized were transferred to the banks to be used to buy back the preference shares issued to the Indonesian government in connection with the joint recapitalization. This approach provided the government with the prospect of an early return on its recapitalization investment and reduced the amount the legacy shareholders would have to pay to regain full control of the bank (Lindgren et al. 1999).

Management and Disposal

1

The AMU/AMC disposed of loan assets in three ways: through corporate loan sales via open auction, by outsourcing for commercial loans through a selected third party (servicing agent), and by dealing with small and medium enterprise (SME) and retail loans, which it sold through open tender auction and “crash” programs that allowed the debtor to settle debts by providing a 100% discount on interest and penalty as well as 25% discount on principal for productive loans only (Fung et al. 2004). Loans that did not enter these retail and SME mechanisms were offered for sale through loan auctions (IMF Staff 2002).

Policymakers utilized the outsourcing strategy to allow IBRA to deploy its resources to restructure corporate loans, which made up most of IBRA’s loan portfolio. Between May and August 2000, IBRA engaged four banks to service separate tranches of commercial loans, with a total face value of roughly IDR 13.5 trillion. These servicing agents were paid a management fee for handling the assets and following up on debt servicing issues (IMF Staff 2002). Further details about servicing arrangements are unclear from the available documentation.

IBRA also introduced several new asset programs that the AMU/AMC used to speed up the loan sale process. These included the asset to bond swap program for corporate loans (introduced in late 2001), by which eligible investors were able to use government recapitalization bonds as payment for IBRA assets; the collateralized debt obligation (CDO), through which IBRA securitized a diversified portfolio of restructured loans and loans in the MOU stage in late 2002; and the loans that were not restructured, through which IBRA sold many unrestructured corporate, commercial, and retail loans in 2002 (Fung et al. 2004).

This last change was “fundamental” and “based on the realization that the restructuring progress had stagnated and had put at risk IBRA’s ability to complete the asset recovery process before the expiry of its mandate” (IMF Staff 2004). BI stated in its 2000 annual report that restructuring progress was hindered by difficulties related to the size of haircuts on debt principal owed to lending syndicates made up of foreign banks, state banks, and private domestic banks. The central bank also mentioned the then-volatile exchange rate and the imposition of income taxes on debtors on the haircuts (Bank Indonesia 2001).

IBRA officials thought “shifting the restructuring responsibility to the private sector would increase asset recovery, as investors would place value on the added flexibility to restructure the assets in accordance with their own financial and strategic considerations” (IMF Staff 2004). This strategy shift suggested political influence, powerful interests, and IBRA’s lack of stronger powers frustrated IBRA staffers, leading them to “slowly [surrender] its battle of attrition with the country's richest, most powerful people” and to begin selling loans “one by one, unrestructured—loans that many bankers and former IBRA officials say are virtually worthless to anyone but the borrowers” (Arnold 2003).

IBRA’s initial restructuring aims centered on so-called Top 21 obligors, named as such because of their roughly one-third share of total IBRA loans. Officials utilized an “obligor” concept to manage loan assets, which involved handling debtor companies belonging to the same conglomerate, or obligor, together (IMF Staff 2002). The restructuring itself entailed an assessment of the debtor company’s financial situation with a subsequent determination of a “sustainable” amount of debt, which would be sold. The unsustainable portion was converted into equity or quasi-equity with an eye toward eventual sale (IMF Staff 2002). Policymakers initially attempted to restructure loans prior to sale for three reasons:

- to aid real sector recovery through improvement of the financial position of indebted firms, thus allowing them to regain access to credit markets;

- to improve corporate governance and managerial control (as IBRA was usually the primary creditor and could install new management); and

- to strengthen the banking system prior to the return of a large amount of nonperforming loans (IMF Staff 2002).

Timeframe

1

IBRA’s stated rationale for having a pre-defined lifespan of five years was that its existence was a reminder that the country was in crisis such that ceasing operations as soon as possible would be beneficial (Fung et al. 2004). IBRA formally wound down on its initially scheduled end date of February 27, 2004 (Omori 2014). Yet at the time it still held billions in assets, which were shifted in part to a new asset management company under the MOF and in part to an oversight committee of cabinet ministers.

The AMU/AMC took over assets from a variety of institutions during the financial sector restructuring to deal with the “unprecedented” amount of nonperforming loans in the banking system (Sharma 2001). Still, one criticism of IBRA is that the levels of nonperforming loans in the system remained high even after the asset transfers (Pangestu 2003). Nonperforming loans declined to 6% of total loans in September 2003 from 75% at the height of the country’s crisis (IMF Staff 2004).

IBRA was also criticized for being slow to mobilize on the disposal of its assets (both the loans it took over and its equity stakes.) Enoch et al. (2001) write that “to some extent, this [criticism] is undoubtedly justified,” but “in mitigation, one should recall the deep intensity of the crisis and the ongoing political transition, freezing investor interest with regard to any involvement in the country” (82). Further, the authors elaborate, due to IBRA’s reliance on special powers, it was unable to operate effectively until the law and the regulations surrounding its operation became effective. “For unexplained reasons, each stage of the passage of the law was protracted, and it was not until February 1999 that IBRA was able to use its powers. As a result, it was, for instance, unable to manage the assets of the banks closed in April 1998 for ten months after the closures: the result was undoubtedly a depletion in the value of the assets, and an increase in the ultimate cost of the banking sector restructuring for the public sector” (111).

During some (unspecified) part of IBRA’s operational period, it retained assets on its books at face value, which kept the organization from negotiating realistic deals. While this reduced moral hazard, any deal negotiated appeared to the public as a loss “rather than a recovery from losses incurred earlier.” This is likely to have contributed to IBRA’s poor public image, because “it led to a perception that it was selling the country ‘cheap’ and, hence, denied IBRA the popular protection that would enable it to better withstand the powerful vested interests set against it” (Enoch et al. 2001).

Additionally, Enoch et al. (2001) elaborate that, due to IBRA’s lack of effective penalties against nonperforming debtors, it struggled to collect loans, “which gave rise to ever-higher needs for provisioning” (97).The state banks were particularly egregious: because these banks expected that their loss loans would be transferred to the AMU/AMC and they would be fully recapitalized, they did not see a compelling reason to go after nonperforming debtors. “Some banks were particularly generous in their deposit rates, while having no evident strategy for enhancing loan recoveries. The overall result was that, even while the nominal interest rate spreads in the banking sector were negative, there was a continued need for banks to make additional provisioning, further worsening the insolvency of the sector” (97).

Further, there was difficulty in setting up the legal framework that enabled IBRA to deal with its assets, and the amount of labor required to document all of the assets and prepare them for sale was enormous (Enoch et al. 2001). There were also major documentation problems, which impeded the transfer of loans from frozen and closed banks to IBRA (Fung et al. 2004).

McLeod (2005) writes that “it is difficult to judge whether IBRA can be regarded as a success. Clearly, the amount of cash it [was] able to return to the government [was] only a small proportion (about 25%) of the value of the bonds the government issued to bail out banks’ creditors . . . but of course most, if not all, of the assets in IBRA’s portfolio were severely compromised at the outset, and there was no realistic expectation that the full book value could be recovered.

“In any case, IBRA’s performance suffered greatly from political interference, as could only have been expected given the vast sums involved. Top management of the institution was changed on numerous occasions as presidents came and went and as each president sought to achieve the outcomes desired” (43). The “prospective redistribution of wealth in Indonesia was so substantial that the vested interests that IBRA encountered were pervasive across its operations” (Enoch et al. 2001). This political interference was a “major problem leading to delays and inconsistencies in the restructuring process” (Pangestu 2003). Some restructuring agreements seemed to “focus on meeting employment or national interest concerns, rather than placing the firm on a commercially viable footing” (IMF Staff 2004). Pangestu (2003) argues “restructuring cannot proceed without the full commitment by Government to support the agencies undertaking the restructuring” (32).

Additionally, efforts were hampered by an implicit guarantee in the financial sector. Indonesian bankers believed the government would bail out their institutions, given only one bank had been allowed to fail in the 1990s and there were cases of government banks and private banks being bailed out (Pangestu 2003).

Fung et. al. (2004) have argued that IBRA’s broad mandate may have hampered its effectiveness, with one organization acting as “an asset management company, an agent to carry out recapitalization, an agent for the blanket guarantee, a manager/supervisor of almost 80% of the banking system, and a restructuring agent of the banking system through, e.g. merging banks” (15).

IBRA's final chairman, Temenggung, summed up what he saw as one of IBRA’s biggest weaknesses: not letting the market play a big enough role. Countries “dealing with nonperforming loan problems should push their banks to dispose of bad assets through the private sector” (Holland 2004).

- Adams, Charles, Robert E. Litan, and Michael Pomerleano. 2000. Managing Financi…

- Arnold, Wayne. 2003. “Indonesian Bank Agency Fading Out.” New York Times, Octob…

- Bank Indonesia. 1998. “Bank Indonesia Report for the Financial Year 1997/98.” B…

- Bank Indonesia. 1999. “Bank Indonesia Report for the Financial Year 1998/99.” B…

- Bank Indonesia. 2001. “Bank Indonesia Annual Report 2000,” 2001. Bank Indonesia.

- “Decree of the President of the Republic of Indonesia No. 27 of 1998.” Indonesi…

- Djiwandono, J. Soedradjad. 2005. Bank Indonesia and the Crisis: An Insider’s Vi…

- Enoch, Charles. 2000. “Interventions in Banks During Banking Crises: The Experi…

- Enoch, Charles, Barbara Baldwin, Olivier Frécaut, and Arto Kovanen. 2001. “Indo…

- Fane, George, and Ross H. McLeod. 2002. “Banking Collapse and Restructuring in …

- Fung, Ben, Jason George, Stefan Hohl, and Guonan Ma. 2004. “Public Asset Manage…

- Gooptu, Sudarshan, Ruth Neyens, Bernard Drum, Sarah Cliffe, and Lant Pritchett…

- Guerin, Bill. 2002. “Indonesia’s Cycle of Subservience to the IMF.” Asia Times,…

- Hasbullah. 2019. “Analysis of Corruption Settlement for Obligor Deviations of B…

- Holland, Tom. 2004. “How to Fix a Bank, Revisited.” Wall Street Journal, May 19…

- IBRA. 1999. “Strategic Plan 1999-2004.” Indonesian Bank Restructuring Agency.

- IMF Staff. 2002. “Staff Country Reports: Indonesia: Selected Items.” IMF Countr…

- IMF Staff. 2004. “Staff Country Reports: Indonesia: Selected Items.” 04/189, Ju…

- Iskander, Magdi, Gerald Meyerman, Dale F. Gray, and Sean Hagan. 1999. “Corporat…

- Jakarta Post. 2001. “JP/IBRA’s OC Launches Website.” Jakarta Post, September 18…

- Lindgren, Carl-Johan, Tomás J.T. Baliño, Charles Enoch, Anne-Marie Gulde, Marc …

- McLeod, Ross H. 2005. “The Economy: High Growth Remains Elusive.” In Budy P. Re…

- Muhammad, Mar’ie, and J. Soedradjad Djiwandono. 1997. “Letter of Intent from th…

- Omori, Sawa. 2014. “The Politics of Financial Reform in Indonesia: The Asian Fi…

- Organization for Economic Co-operation and Development (OECD). 2020. “National …

- Pangestu, Mari. 2003. “The Indonesian Bank Crisis And Restructuring: Lessons An…

- Sharma, Shalendra D. 2001. “The Indonesian Financial Crisis: From Banking Crisi…

- Stern, Joseph J. 2004. “The Impact of the Crisis – Decline and Recovery.” CID W…

- Tempo. 2004. “IBRA’s Journey from Time to Time.” Tempo, May 4, 2004.

Key Program Documents

-

“Decree of the President of the Republic of Indonesia No. 27 of 1998.” 1998. Indonesian Government.

Presidential decree establishing IBRA.

-

Muhammad, Mar’ie, and J. Soedradjad Djiwandono. 1997. “Letter of Intent from the government of Indonesia to the International Monetary Fund,” October 31, 1997.

Letter from Indonesia’s finance minister and central bank governor describing the policies that the country intended to implement in the context of its request for financial support from the IMF.

-

Arnold, Wayne. 2003. “Indonesian Bank Agency Fading Out.” New York Times, October 2, 2003.

News article detailing IBRA officials’ actions at the end of its existence.

-

Guerin, Bill. 2002. “Indonesia’s Cycle of Subservience to the IMF.” Asia Times, September 10, 2002.

Article initially published in the Asia Times detailing the Indonesian government’s relationship with the IMF during the Asian Financial Crisis.

-

Holland, Tom. 2004. “How to Fix a Bank, Revisited.” Wall Street Journal, May 19, 2004.

News article detailing Asian policymakers’ attempts to restructure financial sectors and clean up bad loans in the wake of the Asian Financial Crisis.

-

Jakarta Post. 2001. “JP/IBRA’s OC Launches Website.” Jakarta Post, September 18, 2001.

News article announcing a new government website meant to publicize IBRA’s Oversight Committee reports and activities, though the web address the article gives does not lead to a working website, and web archive searches do not reveal archived versions of the given website.

-

Tempo. 2004. “IBRA’s Journey from Time to Time.” Tempo, May 4, 2004.

News article chronicling IBRA’s history.

-

Adams, Charles, Robert E. Litan, and Michael Pomerleano. 2000. Managing Financial and Corporate Distress: Lessons from Asia. Brookings Institution Press.

Book detailing various lessons learned from financial crises in Asia.

-

Fung, Ben, Jason George, Stefan Hohl, and Guonan Ma. 2004. “Public Asset Management Companies in East Asia.” FSI Occasional Papers, February 26, 2004. Bank for International Settlements – Financial Stability Institute.

Case study examining asset management companies established in Asia.

-

Gooptu, Sudarshan, Ruth Neyens, Bernard Drum, Sarah Cliffe, and Lant Pritchett. 2000. “Indonesia Economic and Social Update.” Brief 51202, January 31, 2000. World Bank.

World Bank report examining various economic and social trends in Indonesia.

-

IMF Staff. 2004. “Staff Country Reports: Indonesia: Selected Items.” 04/189, July 2004. International Monetary Fund.

IMF report outlining various Indonesian economic and governmental updates.

-

Iskander, Magdi, Gerald Meyerman, Dale F. Gray, and Sean Hagan. 1999. “Corporate Restructuring and Governance in East Asia.” Finance and Development/F&D 36 (1).

IMF article examining proper corporate restructuring and governance strategies.

-

Lindgren, Carl-Johan, Tomás J.T. Baliño, Charles Enoch, Anne-Marie Gulde, Marc Quintyn, and Leslie Teo. 1999. “Financial Sector Crisis and Restructuring: Lessons from Asia.” Occasional Papers 188. Occasional Papers, 1999. International Monetary Fund.

IMF paper detailing various Asian financial sector restructuring efforts.

-

McLeod, Ross H. 2005. “The Economy: High Growth Remains Elusive.” In Budy P. Resosudarmo, ed. The Politics and Economics of Indonesia’s Natural Resources, 31–50. ISEAS–Yusof Ishak Institute.

Book chapter examining Indonesia’s macroeconomic performance in the 1990s and early 2000s.

-

Omori, Sawa. 2014. “The Politics of Financial Reform in Indonesia: The Asian Financial Crisis and Its Aftermath.” Asian Survey 54 (5): 987–1008.

Research explaining the politics of financial reforms in Indonesia by applying the theory of veto players.

-

Stern, Joseph J. 2004. “The Impact of the Crisis – Decline and Recovery.” CID Working Paper 103, January 2004. Center for International Development at Harvard University.

Working paper about the Asian financial crisis and related recovery efforts.

-

Bank Indonesia. 1998. “Bank Indonesia Report for the Financial Year 1997/98.” Bank Indonesia.

Bank Indonesia annual report detailing that year’s economic, monetary, and banking developments and policy responses.

-

Bank Indonesia. 1999. “Bank Indonesia Report for the Financial Year 1998/99.” Bank Indonesia.

Bank Indonesia annual report detailing that year’s economic, monetary, and banking developments and policy responses.

-

Bank Indonesia. 2001. “Bank Indonesia Annual Report 2000.” Bank Indonesia.

Bank Indonesia annual report detailing that year’s economic, monetary, and banking developments and policy responses.

-

Djiwandono, J. Soedradjad. 2005. Bank Indonesia and the Crisis: An Insider’s View. ISEAS–Yusof Ishak Institute.

Book written by former Indonesian central bank chair Djiwandono discussing the country’s banking crisis in the 1990s.

-

Enoch, Charles. 2000. “Interventions in Banks During Banking Crises: The Experience of Indonesia,” March 2000. International Monetary Fund.

Discussion paper detailing Indonesia’s banking crisis and related interventions.

-

Enoch, Charles, Barbara Baldwin, Olivier Frécaut, and Arto Kovanen. 2001. “Indonesia: Anatomy of a Banking Crisis Two Years of Living Dangerously 1997-99.” WP/01/52, May 2001. International Monetary Fund.

IMF working paper detailing Indonesia’s banking crisis.

-

Fane, George, and Ross H. McLeod. 2002. “Banking Collapse and Restructuring in Indonesia, 1997-2001.” Cato Journal 22 (2): 277–95.

Article examining Indonesia’s financial crises and related restructuring efforts.

-

Hasbullah. 2019. “Analysis of Corruption Settlement for Obligor Deviations of Bank Indonesia Liquidity Assistance (BLBI).” Indonesian Journal of Criminal Law Studies 4 (1): 15–28.

Journal article analyzing a settlement related to the BLBI.

-

IBRA. 1999. “Strategic Plan 1999-2004.” Indonesian Bank Restructuring Agency.

IBRA report detailing the agency's purpose, history, and strategy.

-

IMF Staff. 2002. “Staff Country Reports: Indonesia: Selected Items.” IMF Country Report 02/154, 2002. International Monetary Fund.

IMF report analyzing a variety of developments in Indonesia, including IBRA and its performance.

-

Organization for Economic Co-operation and Development. 2020. “National Currency to US Dollar Spot Exchange Rate for Indonesia.” FRED, Federal Reserve Bank of St. Louis. FRED, Federal Reserve Bank of St. Louis. 2020.

OECD data showing US dollar exchange rate for Indonesian currency.

-

Pangestu, Mari. 2003. “The Indonesian Bank Crisis And Restructuring: Lessons And Implications For Other Developing Countries.” In G-24 Discussion Papers. G-24 Discussion Paper Series. United Nations.

G-24 discussion paper examining Indonesia’s banking crisis and restructuring efforts.

-

Sharma, Shalendra D. 2001. “The Indonesian Financial Crisis: From Banking Crisis to Financial Sector Reforms, 1997-2000.” Indonesia, No. 71 (April): 79–110.

Journal article detailing the Indonesian financial crisis and related reforms.

Taxonomy

Intervention Categories:

- Broad-Based Asset Management Programs

Countries and Regions:

- Indonesia

Crises:

- Asian Financial Crisis 1997