Broad-Based Emergency Liquidity

Hungary: Liquidity Scheme

Purpose

To “. . . improve the overall liquidity position of the Hungarian banking system so as to maintain lending to the real economy” (EC 2010a, 2).

Key Terms

-

Launch DatesMarch 10, 2009

-

Expiration DateOriginal: June 30, 2010; Extended: June 30, 2013

-

Legal AuthorityAmendment to Law IV of 2009/Law CXCIV of 2011

-

Peak OutstandingHUF 690 billion (USD 3 billion) loaned to three domestic financial institutions

-

ParticipantsHungarian-based financial institutions and subsidiaries of foreign banks

-

RateMultiple yield competitive auction for a fixed CAD amount

-

CollateralUnsecured

-

Loan DurationThree-year maximum; one-third of each loan allowed a maximum maturity of four years

-

Notable FeaturesUnsecured lending by the Hungarian state

-

OutcomesHUF 400 billion repaid early by OTP; HUF 290 billion repaid by MFB and FHB in November 2012

Amid the global credit crunch in late 2008, foreign investors dumped Hungarian assets, the Hungarian forint (HUF) depreciated, and liquidity deteriorated in the Hungarian banking sector due to the prevalence of short-term, foreign currency-denominated liabilities. On March 10, 2009, the Hungarian government established a scheme to provide up to HUF 1.1 trillion (USD 4.9 billion) in foreign exchange liquidity to domestic credit institutions and subsidiaries of foreign banks. The government used funds provided by the International Monetary Fund (IMF) and European Union (EU) in October 2008, a USD 25.1 billion package to provide Hungary with sufficient foreign exchange reserves to meet broad external, foreign-currency obligations. Earlier efforts to establish voluntary guarantees and recapitalizations for Hungarian banks using the IMF-EU funds were unsuccessful, and markets remained concerned about the liquidity of Hungary’s banks. By January 2010, the liquidity scheme had lent HUF 690 billion (USD 3 billion) to three domestic banks. Over the next four years, the EC repeatedly reapproved the scheme for six-month extensions, although the facility did not originate any further loans. The scheme was finally allowed to expire on June 30, 2013.

As turmoil spread in global markets, during the Global Financial Crisis, international investors dumped Hungarian government bonds and other assets. The sharp exchange rate depreciation created liquidity pressures for banks (IMF 2011, 4). At the request of the Hungarian government, the International Monetary Fund (IMF), European Union (EU), and World Bank (WB) agreed in October 2008 to a USD 25.1 billionFThis case study uses six currencies. Per Yahoo Finance and the IMF, USD 1.000 = EUR 0.742 = HUF 222.750 = CHF 1.130 = JPY 98.307 = GBP 0.680 = SDR 0.664 on March 25, 2009. package to provide Hungary with sufficient reserves to meet its external obligations, even in extreme market conditions (IMF 2008b, 1).

The Hungarian government (the State) drew down USD 18.9 billion of funds from the IMF and EU,FThe State agreed in principle to World Bank funding on September 22, 2009, but did not conclude the loan agreement (MNB n.d.). The State did not draw on any portion of the multilateral loan package after September 29, 2009. This case refers to the October 2008 package as IMF-EU funding (IMF 2011, 8). mostly to restore the central bank’s currency reserves (IMF 2011, 9, 32; Kerényi 2011, 44). The State allocated USD 2.7 billion evenly between a recapitalization programFFor more information on Hungary’s 2008 Recapitalization Scheme, see Buchholtz (2021). Hungary also implemented a recapitalization scheme alongside a loan consolidation program in response to a recession in 1992; for more information, see Dreyer 2021. to bolster capital ratios at Hungarian banks and a voluntary program to guaranteeFFor more information on Hungary’s 2008 Guarantee Scheme, see Buchholtz 2021. interbank loans issued by Hungarian banks and wholesale debt contracts with foreign counterparties (Gárdos 2008; Buchholtz 2021; 2020; IMF 2011, 8). Both were undersubscribed by eligible banks: only one bank requested capital, and none applied for the guarantee (Buchholtz 2021; 2020).

As a result of minimal participation in these two programs and lingering liquidity pressures, the State allocated the IMF-EU funds to a new liquidity program (IMF 2011, 38). In March 2009, the Hungarian Parliament passed a law authorizing the State to promote the return of the Hungarian financial system to normal functioning (EC 2010a, 3).

Hungary set aside up to HUF 1.1 trillion (USD 4.9 billion) from the IMF-EU funds to lend under commercial terms to Hungarian credit institutions in the form of uncollateralized medium-term foreign-currency loans (EC 2010a, 2; IMF 2011, 21). The Hungarian central bank, the Magyar Nemzeti Bank (MNB), and the Hungarian Financial Supervisory Authority evaluated banks’ systemic importance and liquidity and then made their recommendations for the Minister of Finance to execute. Loans had a maximum maturity of three years, but one-third of each loan could receive a four-year maturity. To ensure adequate repayment, loan interest rates were subject to a fee based on the greater of 1) an IMF weekly rate or 2) the one-year benchmark rate, plus a penalty rate (EC 2010a, 3).

Although Hungary was not part of the Eurozone, it was part of the European Union (EU) and was obligated to notify the European Commission (EC) of any state aid, including this liquidity scheme (Gárdos 2008; EC 2010a, 5; TFEU 2012). However, Hungary did not notify the EC until late 2009, after the EC became aware of the program from press reports (EC 2010a, 1). The EC did not approve the liquidity scheme until January 2010 (EC 2010a). By that point, the State had already lent HUF 400 billion to OTP Bank, the largest Hungarian domestic bank (March 2009); HUF 120 billion to FHB Mortgage Bank plc, a mortgage lender (March 2009); and HUF 170 billion to MFB, a state-owned development bank (April 2009) (EC 2010a, 3). The State made no further loans through the liquidity scheme.

Because Hungary issued loans prior to notifying the EC, the EC considered the program “non-notified aid.” In its approval, the EC wrote: “The European Commission regrets that Hungary put the aid scheme into effect, in breach of Article 108(3) TFEU” (EC 2010a, 10). Nevertheless, the EC determined the scheme was in accordance with regulations governing state aid in the Treaty on the Functioning of the European Union (TFEU). It said it agreed with the Hungarian government that “if the issues of lack of liquidity and lack of confidence are not properly dealt with, it can result not only in difficulties for the banking sector but could also have a serious effect on the Hungarian economy as a whole” (EC 2010a, 7).

Summary Evaluation

In 2008, 69% of household debt and 48% of nonfinancial corporate debt in Hungary was denominated in foreign currency—particularly Swiss francs—exposing households and firms to exchange rate risk (Verner and Gyöngyösi 2020, 10, 36). Verner and Gyöngyösi (2020) found that the 30% depreciation in the Hungarian forint observed in late 2008 caused a significant increase in household financial distress and a decline in local demand, precipitating a local recession (Verner and Gyöngyösi 2020, 6). This debt revaluation had negative spillovers to other households, including those without foreign currency debt. The authors also found the overall contractionary effects of debt revaluation on the local economy were more severe when foreign currency debt was concentrated in the household sector, rather than the corporate sector, as it was in Hungary in 2008 (Verner and Gyöngyösi 2020, 6).

Kerényi observed that Hungary’s low level of foreign exchange reserves compared to neighboring economies meant it was uniquely unprepared for the dual financial and economic crises of 2008–2009 (Kerényi 2011, 46). Banai noted that Hungarian banks financed their FX-denominated assets using on- and off-balance sheet short-term FX funding, which the central bank was unprepared to replace in a stressed environment (Banai 2022). With more foreign reserves, the MNB could have intervened in currency markets earlier to arrest the forint’s decline. Because of this delay in providing foreign currency liquidity, Kerényi stated that the MNB only partially fulfilled its role as lender-of-last-resort (Kerényi 2011, 45–46).

The IMF determined that the program’s design posed risks to public finances and was insufficiently transparent, particularly about which banks were eligible (IMF 2011, 21–22).

After the State adjusted the loan pricing at the EC’s request and satisfied the IMF’s recommendations, the State sought and the EC granted extensions to the liquidity scheme due to concerns about financial stability and because market conditions “did not allow for a termination” of the program (EC 2013, 3–4; IMF 2011, 21–22).

In its review of the assistance provided to Hungary, the IMF claimed that the liquidity scheme achieved its goal to “support the real economy by requiring recipient banks to maintain certain credit exposures, notably to SMEs” (IMF 2011, 21). The IMF believed that the liquidity scheme served its purpose “of supplying affordable credit to domestic enterprises . . . under commercial terms” and adequately addressed the need “to maintain liquidity and lending exposures” in the banking sector (IMF 2011, 38).

In 2008, 69% of household debt and 48% of nonfinancial corporate debt in Hungary was denominated in foreign currency—particularly Swiss francs—exposing households and firms to exchange rate risk (Verner and Gyöngyösi 2020, 10, 36). Verner and Gyöngyösi (2020) found that the 30% depreciation in the Hungarian forint observed in late 2008 caused a significant increase in household financial distress and a decline in local demand, precipitating a local recession (Verner and Gyöngyösi 2020, 6). This debt revaluation had negative spillovers to other households, including those without foreign currency debt. The authors also found the overall contractionary effects of debt revaluation on the local economy were more severe when foreign currency debt was concentrated in the household sector, rather than the corporate sector, as it was in Hungary in 2008 (Verner and Gyöngyösi 2020, 6).

Kerényi observed that Hungary’s low level of foreign exchange reserves compared to neighboring economies meant it was uniquely unprepared for the dual financial and economic crises of 2008–2009 (Kerényi 2011, 46). Banai noted that Hungarian banks financed their FX-denominated assets using on- and off-balance sheet short-term FX funding, which the central bank was unprepared to replace in a stressed environment (Banai 2022). With more foreign reserves, the MNB could have intervened in currency markets earlier to arrest the forint’s decline. Because of this delay in providing foreign currency liquidity, Kerényi stated that the MNB only partially fulfilled its role as lender-of-last-resort (Kerényi 2011, 45–46).

The IMF determined that the program’s design posed risks to public finances and was insufficiently transparent, particularly about which banks were eligible (IMF 2011, 21–22).

After the State adjusted the loan pricing at the EC’s request and satisfied the IMF’s recommendations, the State sought and the EC granted extensions to the liquidity scheme due to concerns about financial stability and because market conditions “did not allow for a termination” of the program (EC 2013, 3–4; IMF 2011, 21–22).

In its review of the assistance provided to Hungary, the IMF claimed that the liquidity scheme achieved its goal to “support the real economy by requiring recipient banks to maintain certain credit exposures, notably to SMEs” (IMF 2011, 21). The IMF believed that the liquidity scheme served its purpose “of supplying affordable credit to domestic enterprises . . . under commercial terms” and adequately addressed the need “to maintain liquidity and lending exposures” in the banking sector (IMF 2011, 38).

Key Design Decisions

Purpose

1

The purpose of the liquidity scheme was to “improve the overall liquidity position of the Hungarian banking system so as to maintain lending to the real economy” (EC 2010a, 2). The State said it expected that resolving the shortage of liquidity in the banking sector would improve market confidence and prevent a crisis from affecting the real economy (EC 2010a, 4). The government expected participants in the liquidity scheme to maintain their credit exposure to small- and medium-size enterprises (EC 2010a, 2; IMF 2011, 21).

The State extended liquidity through foreign exchange (FX) loans to address the risk that banks would sell Hungarian forint (HUF) to meet their FX needs, which would have placed even more pressure on the depreciating exchange rate (IMF 2011, 21). Both foreign and domestic banks had provided extensive foreign currency loans (largely in Swiss francs) to domestic borrowers using forint funds; they had hedged those long foreign currency positions by shorting foreign currencies through FX swaps. This exposed them to exchange rate and maturity risks and, in October 2008, the forint—used to collateralize the swaps— rapidly depreciated. Banks felt FX liquidity pressure amid margin calls and a frozen swap market in which short-term contracts were no longer being rolled over (IMF 2011, 5).

Legal Authority

2

On March 10, 2009, the Hungarian Parliament amended Law IV of 2009—which is also known as the Act on Public Finances, and is based on Law XXXVIII of 1992—to authorize the State to extend nonrecourse medium-term FX loans under commercial terms to credit institutions in Hungary, including subsidiaries of foreign banks (EC 2010a, 2; IMF 2011, 21).

Following a re-codification of its legal documentation in 2011, the law authorizing the State’s liquidity scheme fell under Article 44 (Chapter VII) of Act CXCIV of 2011, known as the Act on the Economic Stability of Hungary (henceforth “the Act”), which was published in the Official Gazette No. 2011/64 on December 30, 2011 (EC 2013, 2). Article 44 of the Act states, “In a situation that may endanger the stability of the financial intermediation system, the state, within the framework of the management of its free funds. . . b) may grant a loan to a credit institution established in the territory of Hungary” (National Assembly 2011, Chapter VII).

Although Hungary was not part of the Eurozone, it was part of the European Union (EU) and was thus obligated to inform the EC of any “State aid”—including its liquidity scheme—prior to granting it. Under Article 107 of the Treaty on the Functioning of the European Union (TFEU), an EU Member State can offer aid to “remedy a serious disturbance in [its] economy” (TFEU 2012). The State determined—and the EC agreed—that the liquidity scheme qualified as state aid under Article 107(1) (EC 2013, 3–4).

However, because state subsidies can confer an unfair economic advantage to a state’s market participants, the EC generally requires EU states to abide by Article 108 of the TFEU. Article 108 calls for the EC to monitor state aid to ensure it is “compatible with the internal market,” as defined by Article 107, and does not distort, or threaten to distort, competition (TFEU 2012). Article 108 also allows the EC to refer states that do not comply with Article 107 to the Court of Justice of the European Union (EC 2010a, 1). In the case of Hungary, the State launched its liquidity scheme in March 2009 but did not notify the EC until November 2009. The EC referred to this as “non notified aid,” and the State acknowledged this was a breach of Article 108(3)FTFEU Article 108 states, inter alia, the EC will review all aid extended by member states and ensure its compliance with Article 107 (TFEU 2012). Article 107(3)(b) states that “3. The following may be considered to be compatible with the internal market: . . . (b) aid to promote the execution of an important project of common European interest or to remedy a serious disturbance in the economy of a Member State” (TFEU 2012). N.B. Prior to December 1, 2009, Articles 107 and 108 are referred to as Articles 87 and 88; the two sets of provisions are functionally identical. of the TFEU (EC 2010a, 4).

The EC did not formal authorize the liquidity scheme until January 2010 (EC 2010a, 2). At that point, the EC judged that, given the ongoing financial market difficulties in Hungary, the scope of the liquidity scheme and its duration were adequate in terms of achieving the State’s objective of boosting lending to the real economy, as well as addressing a “serious disturbance in the entire economy,” under Article 107(3)(b) TFEU (EC 2010a, 6). Moreover, the EC determined that a liquidity scheme could help Hungarian banks overcome their current difficulties in raising funds, and that such a program could be “compatible” with recapitalization and guarantee schemes (EC 2010a, 8).

The EC believed that remuneration fees on loans were sufficientFOn March 31, 2009, shortly after originating a HUF 120 billion loan to FHB, the State injected HUF 30 billion of capital into the bank through the State’s Capital Base Enhancement Fund—again, without notifying the EC (IMF 2011, 22). The EC subsequently declared that the FHB’s rate of remuneration on state capital did not comply with EU state aid rules (IMF 2011, 22). For more information on that recapitalization, see Buchholtz 2018. to repay the State, while the availability of the measure to banks of all sizes and subsidiaries of foreign institutions offset any possible “distortions of competition” amongst Hungarian banks (EC 2010a, 5).

The State was required to inform the EC when it extended a loan within three months of its origination (EC 2013, 3). The State also committed to updating the EC on the liquidity scheme every six months, including the support provided and under what conditions, as well as any other, non-State liquidity support sought by individual borrowers and the volume, nature, and currency of comparable funding (IMF 2011, 5; EC 2010a, 5; EC 2013, 4).

Part of a Package

1

In November 2008, the IMF, EU, and World Bank agreed to a USD 25.1 billion financing package, maturing in four years (EC n.d.). The IMF agreed to contribute USD 15.7 billion as part of a Stand-By Arrangement; the EU agreed to USD 8.1 billion; and the World Bank agreed to USD 1.3 billion (EC n.d.). Ultimately, the IMF provided SDR 7.6 billion (about USD 11 billion) and the EU provided EUR 5.5 billion (USD 7.4 billion). Hungary never drew upon the World Bank’s contribution (see footnote 2 for details) (World Bank 2009; Kerényi 2011; EC n.d.).

The central bank would use most of the IMF and EU funds to restore its currency reserves (IMF 2011, 32; Kerényi 2011, 44). The IMF and EU also provided Hungary with HUF 600 billion (USD 2.7 billion) for a bank support program to be split evenly between two schemes—a guarantee scheme and a recapitalization scheme—designed to strengthen capital positions and increase the liquidity of domestic banks, with the ultimate goal of stabilizing the Hungarian financial system (IMF 2008c; IMF 2007, 17; EC 2009). No banks participated in the guarantee scheme, and only one institution, FHB Mortgage Bank plc, drew down HUF 30 billion in the recapitalization scheme (Buchholtz 2021; 2020). The liquidity scheme was implemented after the State’s guarantee and recapitalization schemes saw little use.

In addition to multilateral financing, the ECB and Swiss National Bank offered the State swap lines. On October 16, 2008, the ECB extended a EUR 5 billion repo facility to the MNB “to support MNB’s newly introduced euro-liquidity operations,” but Hungary was ineligible for the facility until it was converted to a swap facility several months later (Gárdos 2008; ECB 2008). In February 2009, the Swiss National Bank also announced a temporary swap line with the MNB, whereby the Swiss National Bank lent Swiss francs to Hungary against euros (rather than Hungarian forint) (SNB n.d.).

Because the ECB’s repo line was not immediately accessible, the swap agreements offered by the ECB and Swiss National Bank in October 2008 followed the worst period of Hungary’s liquidity crisis. By late October 2008, liquidity in the FX market was eight standard deviations below its long-term average before the crisis (Banai, et al. 2014, 40). To meet the pressing euro and forint liquidity needs of Hungarian banks in late 2008, the MNB intermediated a two-way EUR/HUF swap tender facility beginning on October 10, and on October 16 the MNB established a standing swap facility offering euros (MNB 2008b; MNB 2008a; Banai, et al. 2014, 41–42).

Although foreign banks were more exposed than domestic banks to foreign currency loans to Hungarian borrowers, they also had better access to foreign currency through their parent companies. Foreign banks increased exposures by over 35% (about USD 5 billion) in the period between September 2008 and March 2009 to provide additional liquidity to their Hungarian subsidiaries (IMF 2011, 21).

In January 2009, the Austrian Ministry of Finance convened the European Bank Coordination Process, or Vienna Initiative, with the objective of coordinating a response to bank funding needs among emerging European countries (EBRD 2009b). In September 2009, Hungary, acting on the recommendation of the IMF and EC, committed its systemically important parent banks to maintain 100% rollover rates for individual institutions and recapitalize their subsidiaries as needed (EBRD 2009a).

Management

1

Hungary’s Finance Minister,FIn 2012, the MNB informed the EC that the Ministry of Finance would henceforth be known as the Ministry for National Economy (EC 2012b, 2). This case refers to the office as the Ministry of Finance for the duration of the liquidity scheme. acting through the Államadósság Kezelő Központ Zrt. (ÁKK Zrt.), the Hungarian government’s debt management agency, completed loan contracts with borrowers on behalf of the State (National Assembly 2011, Chapter VII).

The State tasked the MNB and Pénzügyi Szervezetek Állami Felügyelete (PSZÁF), Hungary’s Financial Supervisory Authority, with determining eligibility for the liquidity scheme, but the IMF found that this process lacked transparency (IMF 2011, 21–22).

Citing concerns over the program’s terms, its risk to public finances, and uncertainy over whether banks would comply with the use of fund requirement, the IMF requested that the State place a government representative on the board of each bank borrower. A new Financial Stability Subcommittee—comprised of the Ministry of Finance, the MNB, and the PSZÁF—monitored the financial stability of borrowers. In response to calls from the IMF to improve ongoing supervision of financial institutions, the State turned PSZÁF into an independent institution and empowered the Financial Stability Subcommittee and the MNB to propose legislation or regulation under a “comply or explain” mechanism—though this right was rescinded after April 2010 (IMF 2011, 22–23).

The State committed to extending loans “only to solvent financial institutions” in compliance with capital requirements (EC 2013, 3). However, the State provided limited oversight of the borrowers, despite the IMF’s recommendations to reorganize and improve bank supervision: on-site bank examinations began in April 2009 and concluded in March 2010, a full year after the State originated the loans. Additionally, the State objected to the IMF’s recommendation to hire non-Hungarian external auditors, and audits of Hungarian financial institutions were delayed (IMF 2011, 22). For example, on-site examinations were supposed to include an external audit of OTP’s foreign operations, but this did not begin until 2011, by which point OTP had already repaid its loan (IMF 2011, 22; EC 2010b, 2). In 2010, the EC required the State to evaluate the “solidity of the funding capacity” of borrowers and, upon request, conduct a liquidity stress test (EC 2010b, 2).

Administration

1

Hungarian-based financial institutions or subsidiaries of foreign banks submitted applications to the MNB and PSZÁF (EC 2010a, 2). The MNB evaluated applications on the basis of the institution’s importance to Hungary’s financial system and its short-term liquidity position in the context of the amount of liquidity available in the market, the same process used for the MNB’s Emergency Liquidity Assistance (Banai 2022). PSZÁF assessed the funds available to the institution and its mid-term and long-term liquidity position. For large holding companies, PSZÁF also considered the funds and liquidity positions of the institutions affiliates (EC 2010a, 2).

With the recommendation of both the MNB and PSZÁF, the Finance Minister then finalized the terms of the loan and acted through the ÁKK Zrt., the State’s debtmanagement agency, to extend credit to Hungarian financial institutions (EC 2010a, 2).

Eligible Participants

1

The liquidity scheme was open to all Hungarian-based credit institutions,FIn 2008, there were 36 banks operating in Hungary, roughly 30 of which were foreign-owned and one was a State-owned development bank—MFB, one of the three borrowers in the liquidity scheme (IMF 2008c; Cull, Peria, and Verrier 2018, 47). Foreign-owned banks were thought to perform more efficiently than other types of banks (Cull, Peria, and Verrier 2018, 11). including subsidiaries of foreign banks, but excluded banks operating in the form of branch offices. These participants could request loans, and their applications would be reviewed by several agencies (EC 2010a). Ultimately, only three domestic borrowers participated in the program; parent companies of foreign bank subsidiaries located in Hungary likely had access to alternative funding sources (Banai 2022).

An applicant had to be deemed financially sound following an evaluation by the MNB and the PSZÁF. The Act on Economic Stability required the Governor of the MNB to provide the Minister of Finance with an evaluation of the applicant’s systemic importance and liquidity positions, as well as an analysis of current market conditions and available liquidity (National Assembly 2011, Chapter VII). In practice, the MNB evaluated the applicant’s systemic importance and its short-term liquidity position, while PSZÁF assessed the funds available to the institution and its mid-term and long-term liquidity position (EC 2010a, 2).

All three of Hungary’s programs were targeted at systemically important banks (Banai 2022). Systemic importance was based on the institution’s size, its influence on financial markets and the payments and settlement systems, and its lending to the real economy, among other criteria.

For large holding companies, PSZÁF also considered the funds and liquidity positions of the institution’s affiliates (EC 2010a, 2). The IMF called for on-site bank examinations and external audits, but the State delayed or objected to these actions (IMF 2011, 22–23).

Funding Source

1

The State funded the liquidity program by reallocating funds from underutilized facilities. In November 2008, Hungary received HUF 600 billion (USD 2.7 billion) for a bank support program that created two schemes—one for bank guarantees and another for recapitalizing banks—designed to strengthen capital positions and increase the liquidity of domestic banks, with the ultimate goal of stabilizing the Hungarian financial system (IMF 2008c; IMF 2007, 17). No banks participated in the guarantee scheme, and only one institution, FHB Mortgage Bank plc, drew down HUF 30 billion in the recapitalization scheme (Buchholtz 2021; 2020).

The State launched the liquidity scheme on March 10, 2009, when the Hungarian Parliament amended the Act on Public Finances to grant the State the authority to extend nonrecourse medium-term FX loans under commercial terms to credit institutions in Hungary, including subsidiaries of foreign banks. The Ministry of Finance budgeted up to HUF 1.1 trillion (USD 4.9 billion) for the liquidity scheme (EC 2010a; IMF 2011, 21).

Program Size

1

The Ministry of Finance budgeted up to HUF 1.1 trillion (USD 4.9 billion) through the liquidity scheme (EC 2010a; IMF 2011, 21). Ultimately, it lent HUF 690 billion (USD 3 billion) to three institutions (EC 2010a, 3).

Individual Participation Limits

1

The State did not limit how much an individual institution could request for a loan. The State lent HUF 400 billion to OTP Bank, the largest Hungarian domestic bank (March 2009); HUF 120 billion to FHB Mortgage Bank plc, the largest mortgage lender, responsible for issuing mortgage bonds on behalf of other banks (March 2009); and HUF 170 billion to MFB, a state-owned development bank (April 2009) (EC 2010a, 3). FHB Mortgage Bank plc, the only participant in the recapitalization scheme, also benefitted from Hungary’s liquidity scheme, which the EC stated did not comply with TFEU rules on state aid (Buchholtz 2021; IMF 2011, 22).

Rate Charged

1

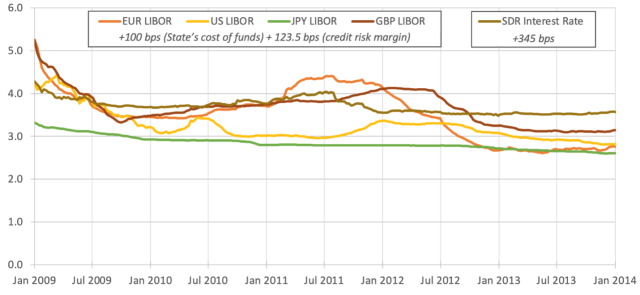

Loans were subject to fees based on the higherFIn March 2009, most of the State’s liquidity loans were offered in euros, and the Euribor-based pricing was the higher of the two rates, by roughly 15 bps (EC 2010a, 9). of:

- IMF’s weekly “Special Drawing Rights Interest Rate Calculation” plus 345 basis points; or

- a twelve-month IBOR plus 100 basis points (addressing the State’s cost of funds) and an additional credit risk margin of 123.5 basis points (EC 2010a, 8). The 12-month IBOR benchmark was determined using the currency the loans were granted in (see Figure 5) (EC 2010a, 3).

Figure 5: Effective Interest Rates on Liquidity Scheme Loans, 2009–2014 (%)

Sources: Bloomberg, IMF.

Sources: Bloomberg, IMF.

The credit risk margin was based on the ECB Recommendations on Government Guarantees on Bank Debt published on October 20, 2008. According to the EC, the penalty add-on to the 12-month IBOR was adequate remuneration for the aid since the liquidity scheme was funded by the IMF’s portion of the original multilateral schemes announced in November 2008 (EC 2010a, 3). Because Hungary lacked adequate CDS data, the risk of loans utilized the lowest CDS rating category, A, which at the time equated to a rate of 73.5 bps plus a mark-up of 50 bps. The EC noted this fee was consistent with the State’s guarantee scheme (EC 2010a, 8–9).

Beginning July 1, 2010, the State adjusted the IBOR-based pricing formula of the loans upwards according to the borrower’s credit ratingFIn 2009, Moody’s had rated OTP at Baa1 and FHB at A3 (Moody’s 2009). Because the State guaranteed most of MFB’s funds, its rating generally tracked that of the State (Banai 2022). on the day of origination (EC 2010b, 2):

- 20 bps for banks with a rating of A+/A1 or A/A2

- 30 bps for banks rated A-/A3

- 40 bps for banks rated below A-

Borrowers without ratings were considered to have a rating of BBB (EC 2010b, 2). In the case of multiple assessments by rating agencies, the higher rating would be used for the calculation of the fee (EC 2010b, 2).

In 2012, the IBOR-based pricing scheme was revised again for loans issued until June 30, 2012 (EC 2012a, 3–4). For loans with remaining maturities of one year or more, the State determined the fees would be no less than 40 bps plus a complex risk-based fee.FThe formula for the risk-based fee was 40 bps × 1/2 × (median five-year senior CDS spread over the three years ending one month before the origination date/median level of the iTraxx Europe Senior Financials five-year index over the same period) + 1/2 × (median 5-year senior CDS spread of all EU Member States/median five-year senior CDS spread in Hungary over the same period) (EC 2012a, 3).

For borrowers without CDS data, a credit rating would be used to derive an equivalent CDS spread using the median value of five-year CDS spreads over the same three-year period, based on a representative sample of large banks in the EU (EC 2012a, 3–4).

For loans with remaining maturities of less than one year, the fees would be no less than 50 bps plus a complex risk-based fee.FThe formula for the risk-based fee was 20 bps for ratings A+/A1 or A/A2, 30 bps for banks rated A-/A3, and 40 bps for banks rated below A- (EC 2012a, 3–4).

Eligible Collateral or Assets

1

The State extended credit against a commitment by banks to secure external funding and maintain corporate lending exposures in Hungary (IMF 2011, 21). If an institution defaulted on a loan, the State was required to submit a restructuring plan or liquidation plan to the EC within six months of the default (EC 2010a, 5).

Loan Duration

1

Loans had a maximum maturity of three years, while one-third of each loan could receive a four-year maturity (EC 2010a, 3). All three loans had a final maturity date of November 11, 2012 (see Figure 6).

Figure 6: Hungarian Liquidity Scheme Borrower Amounts and Duration

Source: EC 2010a, 3-4.

Source: EC 2010a, 3-4.

Other Conditions

1

Loans were uncollateralized, and the primary condition on borrowers was a requirement that borrowers used the funds to lend to the real economy, including Hungarian corporations, and especially small and medium-size enterprises (SMEs) (IMF 2011, 21–22). However, research did not uncover a mechanism to enforce this promise.

Additionally, the State forbade institutions from advertising their borrowing through the liquidity scheme or engaging in “aggressive commercial strategies” during the duration of the loan, and dictated that borrowers could not use the funds to finance acquisitions (EC 2010a, 3; EC 2013, 3).

Impact on Monetary Policy Transmission

1

To reduce the risks of volatility in short-term interest rates and of banks incurring losses due to a lack of liquidity, the MNB narrowed the interest rate corridor in October 2008 (MNB 2009, 22). The MNB raised the reference rate by 300 bps, the only central bank in the region to do so (Kerényi 2011, 45). By mid-2009, the MNB observed enough improvement in market conditions to justify reimposing the original interest rate corridor (MNB 2009, 22).

To manage FX volatility, the MNB established a floor on net international reserves (NIR) at a lower level than the baseline projection included in the balance of payments. However, this was constrained by the level of reserves required to ensure an adequate buffer for the MNB’s guarantee, recapitalization, and liquidity schemes (IMF 2011, 15).

With regard to its FX purchases over the same period, the MNB was required to consult with the IMF if the 12-month CPI inflation rate fell outside an inner band of the target rate plus or minus 1%. Had the CPI rate fallen outside plus or minus 2%, the IMF would have required the MNB to cease FX purchases (IMF 2011, 15).

Other Options

1

The liquidity scheme, part of a broad suite of measures to provide liquidity and support the Hungarian economy, was implemented after the State’s guarantee and recapitalization schemes saw little use (Buchholtz 2021; IMF 2011, 38).

Similar Programs in Other Countries

1

Although Hungary’s actions were not coordinated with responses in other countries, its liquidity provisions resembled those undertaken by the Bank of Greece in August 2011. With non-performing assets rising amid broad credit downgrades, the Bank of Greece offered emergency liquidity assistance, a revolving line of credit charging a penalty rate (100–150 basis-point premium to the ECB’s refinancing rate), to all Greek banks, so long as support did not interfere with EU monetary policy. Greece was one of the first countries to use broad emergency liquidity assistance, with Ireland, Portugal, and several other countries offering similar programs in subsequent years (Runkel 2022). Like Greece, Hungary’s central bank, MNB, stepped in as lender-of-last-resort when the traditional lender-of-last-resort failed. However, Hungary’s decision to offer unsecured lending was unlike the Greek emergency liquidity assistance, and unusual among central banks generally.

During the GFC, the Bank of Korea provided USD 26.6 billion in foreign currency liquidity program to banks struggling to raise overseas funding. The Bank of Korea established a USD 10 billion scheme that provided foreign currency loans secured by export bills, but only allocated USD 0.2 billion between December 10, 2008, and February 25, 2009 (Chung 2011, 260).

Communication

1

On March 10, 2009, the Hungarian Parliament amended the Act, which was published in the Official Gazette, “Magyar Közlöny” (No. 2009/28), effectively announcing the liquidity scheme (EC 2010a, 2). We were unable to locate any State communication that described the program’s terms in detail, possibly in an attempt to avoid stigmatizing potential participants (Banai 2022). The IMF determined the liquidity scheme lacked transparency, particularly around borrower eligibility (IMF 2011, 22–23).

The EC published its approval of each request for extension by the State, and the IMF published its own review of Hungary’s response to liquidity shortages (EC 2013; IMF 2009a).

Disclosure

1

In addition to publishing its approval of the scheme, the EC published evaluations of the State’s requests for extensions to the liquidity scheme, including disclosures of borrowers and amounts lent (EC 2009; EC 2013; EC 2010a). Between 2009 and 2011, the IMF published evaluations covering the State’s guarantee, recapitalization, and liquidity schemes (IMF 2009a; IMF 2011).

Stigma Strategy

1

The State did not have an explicit strategy for addressing stigma.

Exit Strategy

1

The liquidity scheme was initially slated for expiration in June 2009. Effective July 1, 2010, the State raised its lending rates in accordance with the EC’s stated desire that programs of this type contain “minimum exit incentives” and gradually return to market conditions in order to minimize potential spillover effects on other EU Member States (EC 2010a, 6). The State requested six extensions to the scheme, all of which were approved by the EC (EC 2013). OTP, the largest borrower, repaid its loan in two installments on November 5, 2009, and March 19, 2010, long before the loan’s maturity on November 11, 2011; information on repayment by the other two borrowers was unavailable (EC 2010a, 3-4). The State and the EC allowed the scheme to expire on June 30, 2013 (EC 2013, 1).

Key Program Documents

-

(EC 2010a) European Commission (EC). 2010a. “State Aid NN 68/2009 Hungary Liquidity Scheme for Banks.”

Initial approval for Hungary’s liquidity scheme.

-

(IMF 2011) International Monetary Fund (IMF). 2011. “Hungary: Ex Post Evaluation of Exceptional Access Under the 2008 Stand-By Arrangement.” IMF Staff Country Reports 11, no. 145: i.

An overview of Hungary’s IMF Stand-by Arrangement.

-

(National Assembly 2011) National Assembly of Hungary (National Assembly). 2011. Law CXCIV of 2011 (Act on the Economic Stability of Hungary).

Law CXCIV of 2011—in Hungarian; this act replaced Law IV of 2009 following a recodification of Hungarian Law.

-

(TFEU 2012) European Commission (EC). [1957] 2012. Treaty on the Functioning of the European Union. 326/1 C 37.

Treaty restricting the ECB from, among other activities, monetary financing.

-

(EBRD 2009a) European Bank for Reconstruction and Development (EBRD). 2009a. “European Bank Coordination: PSI Rollover Requirements and Macroeconomic Consequences.”

Details from the “Vienna Initiative” on rollover agreements among countries in Central and Eastern Europe.

-

(EC n.d.) European Commission (EC). n.d. “Financial Assistance to Hungary.” Accessed March 21, 2022.

Information on Hungary’s balance of payments (BoP) program and post-program surveillance.

-

(ECB 2008) European Central Bank (ECB). 2008. “Magyar Nemzeti Bank and European Central Bank Cooperation to Support the MNB’s Euro Liquidity Providing Instruments.”

ECB announcement of its support for the MNB.

-

(MNB 2008a) Magyar Nemzeti Bank (MNB). 2008a. “The MNB’s Two-Way O/N FX Swap Tenders (Providing Euro and Forint Liquidity).”

MNB announcement of initial two-way swap tenders.

-

(MNB 2008b) Magyar Nemzeti Bank (MNB). 2008b. “The MNB’s O/N FX Swap Standing Facility Providing Euro.”

Following the two-way swap tenders, the MNB’s announcement of a euro swap facility.

-

(MNB n.d.) Magyar Nemzeti Bank (MNB). n.d. “IMF / EU Financial Assistance (Archive).” Accessed April 28, 2022.

Details on the agreement with the World Bank, whose funding the Hungarian state never drew upon.

-

(SNB n.d.) Swiss National Bank (SNB). n.d. “Swiss National Bank and Magyar Nemzeti Bank Cooperate to Provide Swiss Franc Liquidity.” Accessed January 6, 2022.

Announcement of Swiss National Bank and MNB swap line.

-

(World Bank 2009) World Bank. 2009. “Hungary: Financial Sector and Macro Stability Development Policy Loan.”

World Bank announcement on the loan to the Hungarian state, which was not drawn.

-

(Chung 2011) Chung, Hee Chun. 2011. “The Bank of Korea’s Policy Response to the Global Financial Crisis,” Bank for International Settlements, no. 54: 10.

Analysis of the Bank of Korea’s GFC liquidity provision, which resembled Hungary’s foreign currency lending.

-

(EC 2009) European Commission (EC). 2009. “State Aid N 664/2008 – Support Measures for the Banking Industry in Hungary.”

EC approval of Hungary’s initial crisis response measures, prior to the launch of the liquidity scheme.

-

(EC 2010b) European Commission (EC). 2010b. “State Aid N 225/2010 Prolongation and Modification of the Hungarian Bank Support Scheme.”

First extension to Hungary’s liquidity scheme.

-

(EC 2012a) European Commission (EC). 2012a. “State Aid SA.34078 (2011/N) Extension of the Hungarian Bank Support Scheme.”

Fourth extension to Hungary’s liquidity scheme.

-

(EC 2012b) European Commission (EC). 2012b. “State Aid SA.35144 (2012/N) Extension of the Hungarian Bank Support Scheme.”

Fifth extension to Hungary’s liquidity scheme.

-

(EC 2013) European Commission (EC). 2013. “State Aid SA.36087 (2013/N)—Hungary—Sixth Prolongation of the Liquidity Scheme for Banks.”

Sixth and final extension to Hungary’s liquidity scheme.

-

(Gárdos 2008) István Gárdos (Gárdos). 2008. “IMF, European Union and World Bank Support Credit Crisis Relief Measures.”

Overview of Hungary’s initial crisis response measures, including the guarantee and recapitalization schemes.

-

(IMF 2007) International Monetary Fund (IMF). 2007. “Hungary: 2007 Article IV Consultation: Staff Report; and Public Information Notice on the Executive Board Discussion.” IMF Staff Country Reports 07, no. 250: 1.

IMF country report on Hungary.

-

(IMF 2008a) International Monetary Fund (IMF). 2008a. “Press Release: IMF Announces Staff-Level Agreement with Hungary on 12.5 Billion Euro Loan (US$15.7 Billion); European Union, World Bank to Lend, Too.”

Initial press release announcing the joint IMF-EU-WEB loan to Hungary.

-

(IMF 2008b) International Monetary Fund (IMF). 2008b. “Press Release: IMF Executive Board Approves 12.3 Billion Euro Stand-By Arrangement for Hungary.”

Official IMF announcement of the Stand-By Arrangement.

-

(IMF 2008c) International Monetary Fund (IMF). 2008c. “Hungary: Request for Stand-By Arrangement-Staff Report; Staff Supplement; and Press Release on the Executive Board Discussion” 2008, no. 361.

IMF report on Hungary’s request for a Stand-By Arrangement.

-

(IMF 2009a) International Monetary Fund (IMF). 2009a. “Hungary: Second Review Under the Stand-By Arrangement, Request for Waiver of Nonobservance of Performance Criterion, and Request for Modification of Performance Criteria: Staff Report; and Press Release on the Executive Board Discussion.” IMF Staff Country Reports 09, no. 197: i.

IMF’s second review under the Stand-By Arrangement.

-

(IMF 2009b) International Monetary Fund (IMF). 2009b. “Hungary: Third Review Under the Stand-By Arrangement, Requests for Extension of the Arrangement, Rephasing of Purchases, and Modification of Performance Criterion.” IMF Staff Country Reports 09, no. 304: i.

IMF’s third review under the Stand-By Arrangement.

-

(IMF 2009c) International Monetary Fund (IMF). 2009c. “Hungary: Fourth Review Under the Stand-By Arrangement, and Request for Modification of Performance Criteria (2009).”

IMF’s fourth review under the Stand-By Arrangement.

-

(MNB 2009) Magyar Nemzeti Bank (MNB). 2009. “Annual Report 2009.”

Annual report of the MNB, 2009.

-

(Trading Economics n.d.) Trading Economics. n.d. “Hungary - Credit Rating.” Accessed March 22, 2022.

Hungary’s credit ratings.

-

(Allen and Moessner 2010) William A Allen, and Richhild Moessner (Allen and Moessner). 2010. “Central Bank Co-Operation and International Liquidity in the Financial Crisis of 2008-9.” BIS Working Paper, 310, May 2010.

Overview of central bank responses to the GFC.

-

(Banai, et al. 2014) Ádám Banai, András Kollarik, and András Szabó-Solticzky (Banai, et al.). 2014. “The Network Topology of the Hungarian Short-Term Foreign Exchange Swap Market.” Research in Economics and Business: Central and Eastern Europe 6, no. 2.

Overview of the Hungarian FX swap market and the effects of the GFC on that market.

-

(Banai, Király, and Nagy 2011) Banai, Ádám, Júlia Király, and Márton Nagy. 2011. “The Demise of the Halcyon Days in Hungary: ‘Foreign’ and ‘Local’ Banks—before and after the Crisis,” no. 54: 30.

Analysis of foreign and local banking representation in Hungary.

-

(Buchholtz 2020) Buchholtz, Alec. 2020. “The Hungarian Guarantee Scheme (Hungary GFC).” Journal of Financial Crises 2, no. 3: 18.

YPFS case study on Hungary’s guarantee scheme.

-

(Buchholtz 2021) Buchholtz, Alec. 2021. “Hungary Recapitalization Scheme.” Journal of Financial Crises 3, no. 3: 18.

YPFS case study on Hungary’s Recapitalization Scheme, which only saw one participant.

-

(Cull, Peria, and Verrier 2018) Cull, Robert, Maria Soledad Martinez Peria, and Jeanne Verrier. 2018. “Bank Ownership: Trends and Implications.” IMF Policy Research Working Paper 8297. Development Research Group; Finance and Private Sector Development Team.

IMF Policy Research Working Paper presenting recent trends in government and foreign bank ownership across countries.

-

(EBRD 2009b) Erik Berglof and Piroska M. Nagy (EBRD). 2009b. “Coordinated Policy Response to the Financial Crisis in Emerging Europe.”

Presentation detailing the “Vienna Initiative’s” response to the crisis in Central and Eastern Europe, delivered at an informal seminar in Vienna sponsored by the European Bank for Reconstruction and Development, January 23, 2009.

-

(Kerényi 2011) Ádám Kerényi (Kerényi). 2011. “Financial Assistance for Hungarian Crisis Management – a Case Study.” Studies in International Economics and Finance, 35–61.

Overview of the Hungarian response to the GFC.

-

(Petrovic and Tutsch 2009) Petrovic, Ana, and Ralf Tutsch. 2009. “National Rescue Measures in Response to the Current Financial Crisis.” ECB Legal Working Paper Series, July.

Piece detailing financial responses to the Global Financial Crisis by country.

-

(Runkel 2022) Runkel, Corey N. 2022. “Greece Emergency Liquidity Assistance.” Journal of Financial Crises 4, no. 2.

YPFS case study reviewing the Bank of Greece’s (and the ECB’s) Emergency Liquidity Assistance.

-

(Várhegyi 2008) É. Várhegyi (Várhegyi). 2008. “The Hungarian Banking System 20 Years After Modernization.” Acta Oeconomica 58, no. 4: 351–66.

Analysis of the Hungarian banking sector.

-

(Verner and Gyöngyösi 2020) Verner, Emil, and Győző Gyöngyösi. 2020. “Household Debt Revluation and the Real Economy: Evidence from a Foreign Currency Debt Crisis.” MNB Working Papers, No. 2020/2, March.

Summary of foreign debt borrowing by Hungarian households in the lead-up to the GFC.

European Commission’s Review of Hungary’s Liquidity Scheme

Taxonomy

Intervention Categories:

- Broad-Based Emergency Liquidity

Countries and Regions:

- Hungary

Crises:

- Global Financial Crisis