Broad-Based Emergency Liquidity

European Central Bank: Term Refinancing Operations

Purpose

“To enhance the flow of credit above and beyond what could be achieved through policy interest rate reductions alone” (Trichet 2009)

Key Terms

-

Launch DatesAnnouncement: August 22, 2007; First settlement: August 24, 2007

-

Expiration DateLast announcement: March 29, 2010; Last maturity: December 23, 2010

-

Legal AuthorityStatute of ESCB, article 18.1

-

Peak OutstandingEUR 729 billion in June and July 2009

-

ParticipantsEuro-area monetary and financial institutions subject to reserve requirements

-

RateMulti-rate auction until October 2008; fixed-rate scheduled offerings after October 2008

-

CollateralSchedule of marketable and non-marketable debt (see Appendix A)

-

Loan Duration1-, 3-, 6-month; 1-year

-

Notable FeaturesOffered same rate for one-week and one-year operations

-

OutcomesSupport repaid 100%; No fiscal costs

During the Global Financial Crisis (GFC), the European Central Bank (ECB) expanded the frequency, maturities, size, and set of eligible collateral for several of its standing term refinancing operations (TROs). Changes started in August 2007, when the European interbank market tightened, and the ECB supplemented its monthly longer-term refinancing operations (LTROs) with another three-month-maturity tender each month. Another encounter with market turbulence in March 2008 brought six-month LTROs. The largest expansion came after the collapse of Lehman Brothers in September 2008: the ECB enlarged its set of eligible collateral, added 12-month LTROs, and added special-term refinancing operations (STROs) that matured at the end of the reserve maintenance period. In a first, the ECB also said it would satisfy all demands for liquidity in a TRO at a fixed rate, abandoning the auctions that it had long used to determine the interest rates it charged. This demand-driven, “full-allotment” policy combined with the longer maturities to ease interbank rates from their panicked highs. At its peak in summer 2009, more than EUR 729 billion was outstanding. The ECB recouped all loans on this program.

On August 9, 2007, spreads between secured and unsecured overnight funding spiked, stressing Europe’s interbank funding market. Underregulated and opaque financial relationships obscured the immediate cause for this spike, and the ECB used four large fine-tuning operations (FTO)—which could be announced and settled within the day—to support eurozone banks through the week (Trichet 2010). See Runkel (2022a) for a study of these operations. However, this jolt of financial distress proved to be only the first of many during the Global Financial Crisis (GFC), and the FTOs only a stopgap.

Two weeks later, on August 22, the ECB announced the first supplementary longer-term refinancing operation (SLTRO; ECB 2020). Since 1999, the EurosystemFThe Eurosystem consisted of the ECB and the central banks of countries that used the euro. In August 2007, it consisted of national central banks of Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Spain, Greece, and Slovenia. Cyprus, Malta, and Slovakia joined during the GFC. It is not to be confused with the European System of Central Banks, which also included central banks of EU states that did not use the euro. had provided liquidity to banks through longer-term refinancing operations (LTROs) in the last week of each month (ECB 2021). The terms on SLTROs were no different from the terms on the earlier monthly LTROs. Both operations offered sound banks, subject to ECB reserve requirements, secured funding for maturities of three months (ECB 2006). Accepted collateral—which included marketable securities rated at least A- and nonmarketable debt from highly rated issuers—was denominated in euros and took haircuts according to several factors (see the Appendix). Successful banks paid the interest rates that they bid. The ECB used this variable-rate, fixed allotment regime for almost every longer-term refinancing operation.

SLTROs simply offered banks a chance to access long-term funding earlier in the month. Interbank funding spreads stabilized after the ECB introduced the SLTROs, but they did not fall. In March 2008, a new spike in spreads prompted the ECB to conduct more FTOs. Again, the ECB followed the overnight operations with enhancements to its LTROs, this time introducing six-month maturities. Again, interbank funding markets calmed, but did not cool, inching their way upward in fall 2008 (Bank of France 2021).

The ECB took unprecedented action in October 2008 when interest-rate cuts and FTOs failed to soothe markets following the collapse of Lehman Brothers, a large US investment bank. The Eurosystem shifted from conducting open-market operations using a variable-rate, fixed allotment to using what it termed fixed-rate, “full-allotment” operations (ECB 2008a). The fixed rate was the Main Refinancing Rate, which the Governing Council set for weekly Main Refinancing Operations (MROs), used to steer interest rates, and signal monetary policy (ECB 2021; ECB 2006). “Full allotment” meant that banks received as much as they requested (Trichet 2010). In other words, the ECB was on the hook for as much funding as counterparties were willing to collateralize. The Eurosystem had previously conducted fixed-rate, full-allotment FTOs, but never LTROs (ECB 2021).

The ECB also expanded the collateral it would accept, adding lower-rated securities (including those denominated in currencies other than euros), fixed-term deposits, and subordinated debt instruments (ECB 2008a). Last, it added special-term refinancing operations (STROs). These operations varied in maturity along with the length of the reserve maintenance period, a four- to five-week period over which the ECB averaged bank reserves to enforce its reserve requirements (ECB 2007). They were matched with liquidity-absorbing FTOs that siphoned excess liquidity from the European banking system on the last day of the maintenance period. All of these changes worked to strengthen banks’ liquidity without adding net liquidity to the system (Borio and Nelson 2008).

The price of interbank lending fell after the October 2008 changes, dragged lower by the below-market rate charged on the new SLTROs (ECB 2021). But ECB president Jean-Claude Trichet (2009) emphasized the new programs and new structure rather than their interest rates, noting that these expansions to longer-term refinancing supported “the flow of credit above and beyond what could be achieved through policy interest rate reductions alone.”

The ECB introduced one-year LTROs in May 2009 (ECB 2009c). Later that year, the central bank announced that it would revert to variable-rate tenders in 2010 (Trichet 2010). However, it conducted only one such operation before Greece’s debt problems flared up, marking the beginning of Europe’s Sovereign Debt Crisis and the end of this case’s focus (ECB 2021; Trichet 2010). The ECB resumed fixed-rate, full-allotment tenders and added three-year LTROs in 2011 (see Lawson 2020). The central bank continued to conduct an expanded range of LTRO maturities through 2011, when one-year LTROs were phased out (ECB 2021).

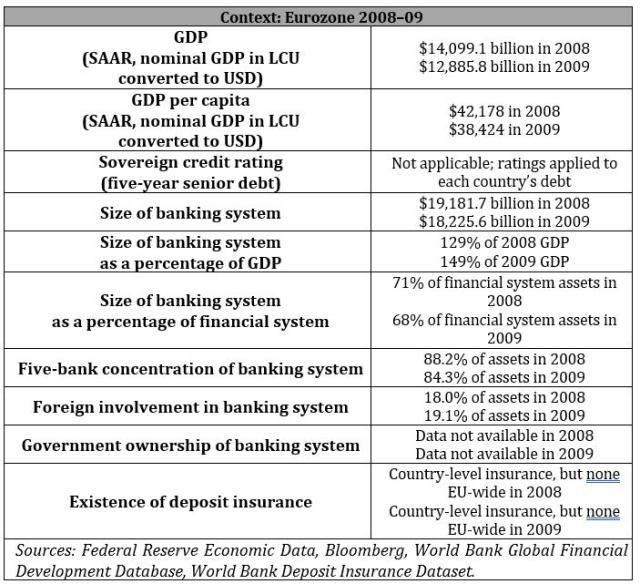

Figure 1: Outstanding Refinancing Operations Settled between August 9, 2007, and April 1, 2010

Note: The shaded area represents the period during which the ECB operations carried a fixed rate and full allotment.

Source: ECB 2021.

Little has been written on the impact of TROs relative to the three-year SLTROs tendered during the EU’s Sovereign Debt Crisis (see Lawson 2020 for a treatment of those operations). A member of the ECB’s executive board termed the fixed-rate, full-allotment policy “the most significant non-standard measure” implemented by the central bank (Manuel González-Páramo 2011). By setting a fixed interest rate, he said, banks with high demand were not penalized by higher borrowing prices. And by setting that rate equal to the ECB’s policy rate, more demand for TROs meant more borrowing at that policy rate, which pulled market rates toward the ECB’s target (Kaminska 2011). An internal Federal Reserve memo written during the Sovereign Debt Crisis noted: “As soon as the ECB switched to a full allotment system in October 2008, the EONIA [Euro Overnight Index Average] rate . . . began trading below the center of the ECB’s policy rate corridor” (Bowman 2010). To fend off critics who argued that the programs would lead to high inflation, the ECB introduced the “separation principle,” under which it held that liquidity management and monetary policy were separate and distinct and required separate tools (ECB 2019, 13). The Federal Reserve memo also cited the ECB’s expanded set of collateral as a lubricant of credit provision. However, the same memo also noted that some euro-area officials had complained that the ECB’s counterparties had held TROs as reserves with the ECB rather than using them to stabilize or increase their provision of credit (Bowman 2010). This made EONIA “highly volatile as a result of constant fluctuations in the amount of excess liquidity in the system” (ECB 2010a). Outside the interbank funding market, researchers from the IMF found strong evidence that SLTROs raised equity prices and slightly decreased sovereign debt yields in the euro area and in other advanced economies (Fratzscher, Duca, and Straub 2016).

Key Design Decisions

Purpose

1

From its announcement of the first SLTRO on August 22, 2007, the ECB maintained that the operations supported the “normalization of the functioning of the euro money market” (ECB 2020). In a speech the following month, ECB president Jean-Claude Trichet noted that such liquidity-driven measures were separate and distinct from the ECB’s monetary policy (Trichet 2007, 4). The idea behind this “separation principle” was to use tools such as refinancing operations to ensure that the interbank market functioned and that the ECB could always use its traditional monetary tools—namely, interest rates—to rein in medium-term rates if signs of inflation appeared (Trichet 2007; ECB 2019, 13). For TROs, the ECB only looked “to keep short-term rates close to the interest rate on the main refinancing operation” (ECB 2008a).

Legal Authority

1

The 1992 Treaty on European Union included several annexes related to the functioning of the Union. Member States that adopted the euro as their official currency devolved many powers of financial regulation to the EU through these annexes. In the realm of monetary policy, the EU permitted the ECB and the national central banks to:

- “operate in the financial markets by buying and selling outright (spot and forward) or under repurchase agreement and by lending or borrowing claims and marketable instruments, whether in Community or in non-Community currencies, as well as precious metals;

- “conduct credit operations with credit institutions and other market participants, with lending being based on adequate collateral” (European Union 1992).

The Statute of the ESCB also vested in the ECB Governing Council the responsibility to formulate monetary policy and guidelines for the Bank’s functioning (European Union 1992). In turn, the Governing Council allowed itself to “change the instruments, conditions, criteria and procedures for the execution of Eurosystem monetary policy operations” (ECB 2006). The power to change such instruments and conditions became important as the ECB enhanced its refinancing operations.

Part of a Package

1

A 2009 speech by ECB President Jean-Claude Trichet christened the central bank’s approach to the crisis as Enhanced Credit Support, referring to the liquidity outcomes that required other tools than interest-rate reductions. ECS was conceived one tool at a time—at least until fall 2008, when the ECB expanded eligible collateral and adopted a fixed-rate, full-allotment regime (ECB 2008a). First came large, liquidity-providing fine-tuning operations (FTOs). These were “the first line of defence,” with the ability to be announced and implemented within a day and provide tens of billions to the large banks ready to transact that quickly. FTOs, when they were conducted at a fixed rate, also used the same benchmark rate as fixed-rate, full-allotment TROs (ECB 2021). Then came the expansions in collateral, which also applied to the MROs that rolled over every two weeks.

Two other building blocks were US dollar liquidity provided by swap lines from the Federal Reserve and purchases of European covered bonds (Trichet 2009). For US dollar liquidity, the Federal Reserve originally swapped dollars for euros only on the days that the Federal Reserve’s Term Auction Facility offered dollars domestically to banks (see Runkel 2022c). The Federal Reserve eventually committed to providing unlimited dollars to the ECB, and the swap lines provided $293 billion at their peak in December 2008 (ECB 2021). Covered bonds were a significant source of liquidity for European banks (Trichet 2010). The ECB purchased more than EUR 60 billion of covered bonds during its Covered Bond Purchase Programme (see Smith 2020).

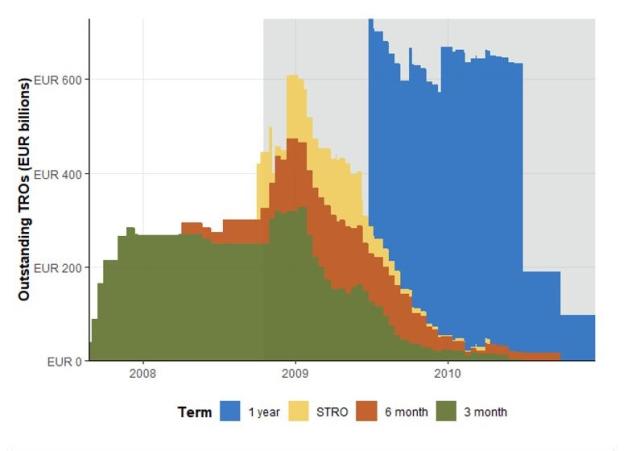

After October 2008, liquidity-providing FTOs were no longer used as crisis-fighting tools, and were instead used exclusively as a cushion on days when large LTROs matured and new LTROs took their place (Atkins 2010). FTOs provided a bridge between these LTROs and MROs. All six liquidity-providing FTOs are shown in Figure 2, alongside the LTROs that matured or were allotted and settled that same week. This is detailed in Key Design Decision No. 11, Eligible Collateral.

Figure 2: Maturing LTROs, Allotted LTROs, and Liquidity-Providing FTOs

Source: ECB 2021.

Source: ECB 2021.

Management

1

The Statute of the ESCB gave to the ECB Executive Board—composed of its President, Vice-President, and four appointees—the responsibility to implement the monetary policy decided by the Governing Council. To the extent that the Governing Council deliberated and adopted new policies and interest rates during the Global Financial Crisis (GFC), it also managed the EU’s SLTROs. The Governing Council consisted of the Executive Board and the governor of each national central bank (European Union 1992). It met twice a month, with monetary policy decisions made every second meeting. Additionally, each national central bank had several rights related to tender procedures including the right to impose sanctions on, refuse the collateral of, and call more collateral from counterparties (ECB 2006).

Administration

1

Under both allotment regimes, counterparties submitted bids through their respective national central bank (or banks if the counterparty had branches in multiple ESCB countries; ECB 2006). During the GFC, the ECB used 44 press releases to announce operations as early as months before a tender, and as late as the same week, with an official invitation to submit bid schedules on the day before a tender (ECB 2020; ECB 2008a; ECB 2006, chart 1). Under the variable-rate regime in place before the collapse of Lehman Brothers, requesting banks submitted up to 10 bids. A bid requested a particular amount of liquidity and offered an interest rate that the counterparty would pay for that amount. The ECB then compiled the bids received by all national central banks. The ECB decided the total liquidity to be allocated and satisfied bids starting at the highest interest rate offered until bids exhausted the allotment. SLTROs settled the day after the bid deadline and allotment (ECB 2006).

After the October 2008 announcement, the ECB stopped conducting auctions. Instead, it fulfilled all bids at a rate equal to the Main Refinancing Rate (MRR). The ECB used the MRR for Main Refinancing Operations and to steer interest rates (ECB 2021; ECB 2006). No other aspects of the bid submission and settlement process changed: The ECB still received bids through the national central banks, still formally announced tenders the day before (informally at irregular intervals), and still settled the day after the bid deadline. A member of the ECB’s Executive Board termed this policy, of fixed-rate and full-allotment, the “most significant non-standard measure” the ECB implemented during the GFC (Manuel González-Páramo 2011).

Eligible Participants

1

To be eligible, institutions must have been:

- Subject to minimum reserve requirements; this requirement effectively limited participation to those banks located in the eurozone (European Union 1992, art. 19),

- Subject to national supervisory standards,

- In good standing with the regulations of the ECB and the institution’s national central bank.

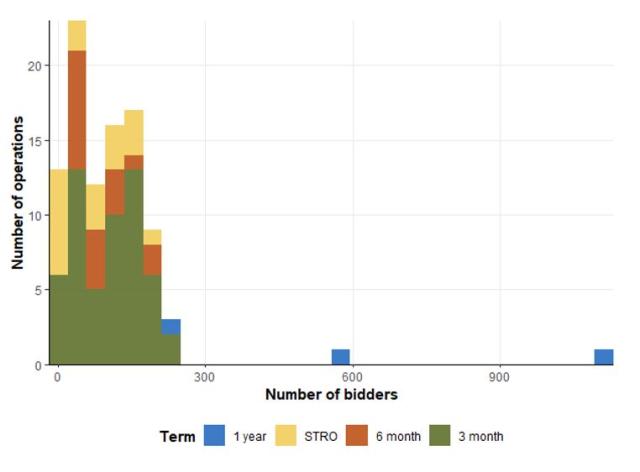

The ECB allowed any banks that fulfilled these criteria to participate in open-market operations based on standard tenders (ECB 2006). Figure 3 shows that 10 to 250 bidders participated in most tenders, though the one-year LTROs in 2009 and 2010 received significantly more. The longer the term of credit, the more space it afforded banks to reconfigure its balance sheet to accommodate higher demand.

Figure 3: Number of Bidders by Maturity

Source: ECB 2021.

Funding Source

1

TROs appeared as an asset on the Eurosystem’s consolidated balance sheet as longer-term refinancing operations. This meant that national central banks or the ECB itself held TROs. It is clear from annual reports of Germany, France, and Slovenia that national central banks held TROs, but it not clear from the ECB annual reports whether the ECB did (ECB 2009b; ECB 2010a). The allocation of holdings across national central banks was not dictated by the ECB’s capital key, by which the ECB apportions profits and losses, and according to which it purchased securities under its Asset Purchase Program. National central banks likely held TROs simply as a result of successful bids submitted to their bank.

Program Size

1

Before the GFC, the ECB aimed to inject 25% of the total liquidity offered by the Eurosystem through LTROs. After August 2007, when the ECB still conducted refinancing operations by variable-rate tenders, it fixed allotment amounts between EUR 25 billion and EUR 75 billion, and offered them every two weeks, increasing the proportion of Eurosystem liquidity injected by TRO (ECB 2021).

After switching to fixed-rate tenders in October 2008, the size of allotments varied greatly, driven entirely by participant demand. One-year operations commanded hundreds of billions of euros, while some one- and three-month LTROs received less than EUR 10 billion in bids. After the introduction of fixed-rate tenders, the operations averaged EUR 40 billion (ECB 2021).

Individual Participation Limits

1

The ECB’s guidelines noted that it reserved the power to impose individual-debtor participation limits as a risk control measure after the adoption of fixed-rate, full-allotment refinancing operations (ECB 2009a). However, no documents suggest that the ECB did so during the GFC.

Rate Charged

1

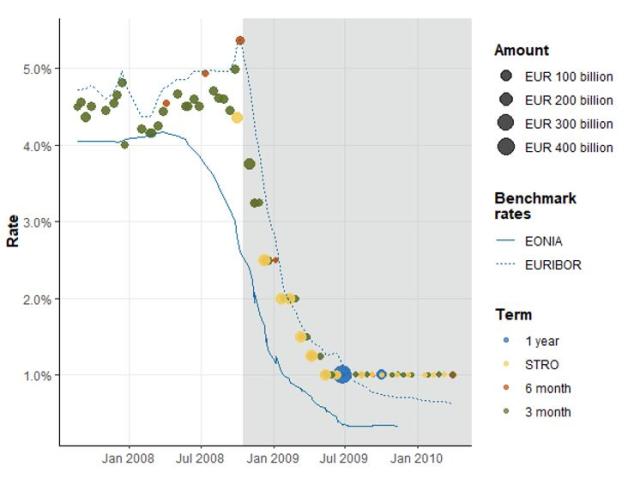

As a rule, the ECB did not use TROs to send signals to the market and therefore normally acted as a rate taker before fall 2008, when the collapse of Lehman Brothers caused a spike in already-high interbank lending rates. To act as a rate taker, the Eurosystem allocated liquidity by auction: bids offering the highest interest rates received their requested amount at the rate bid, until requested amounts exhausted the allotment (ECB 2006). Since the ECB did not set a fixed—or even minimum—interest rate at which it provided liquidity, the rates at which banks received liquidity cannot be classified as penalty rates. Moreover, it is difficult to compare the auction rates to those found in the private market since there is no benchmark rate for secured, euro-denominated interbank lending. The unsecured EURIBOR provides the closest comparison. If the lowest accepted rate at an auction matched the EURIBOR, then that operation was priced at a penalty rate, since there always existed the opportunity cost of committing collateral for three months. Only in a few instances at the end of 2007, and once during the collapse of Lehman Brothers, was the marginal three-month LTRO rate equal, or nearly equal, to the EURIBOR (Bank of France 2021; ECB 2021). See Figure 4 for a graphical depiction of this dynamic.

On October 15, 2008, the ECB departed from this framework in favor of a fixed-rate, full-allotment regime (ECB 2008a). The rate on TROs was fixed to the MRR. By fixing TROs to the MRR, which was used to steer interest rates, rates on TROs subsequently fell from a high marginal rate of 5.36% for last variable rate operation to 3.75% for the first fixed-rate, full-allotment operation (ECB 2021).

ECB decisions pushed the main refinancing rate still lower until May 2009, where the rate would remain at 1.00% through the end of the GFC. The three-month EURIBOR fell below 1% in July 2009 (see Figure 4; ECB 2021; Bank of France 2021), meaning that three-month LTROs and SLTROs effectively required a penalty rate for liquidity through the end of the GFC.

Figure 4: Enhanced Credit Support Operations and Interbank Funding Rates

Note: The shaded area represents the period during which the ECB operations carried a fixed rate and full allotment.

Source: Bank of France 2021; ECB 2021.

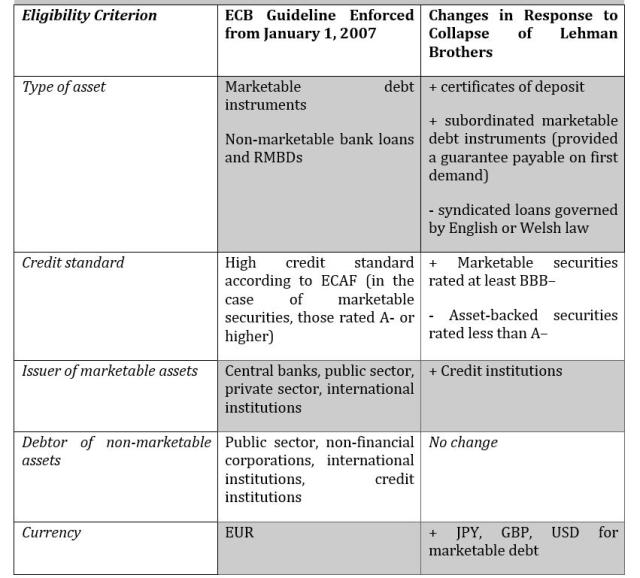

Eligible Collateral or Assets

1

Before the GFC, the ECB adopted a unified framework for Eurosystem open-market operations. Under this framework, the ECB accepted marketable debt instruments, such as ECB debt certificates, rated at least A-. It also accepted two standard non-marketable assets: bank loans, including syndicated loans, and retail mortgage-backed debt (RMBD; ECB 2006, table 4; ECB 2008c). To reduce the complexity of collateral operations, the ECB limited the number of laws governing any eligible syndicated loan to two sets of laws. Many criteria governed the settlement, size, and type of debtor, but all collateral was denominated in euros. Additionally, banks borrowing from a central bank in one EU country could post collateral through a branch in a different EU country (ECB 2006, table 4).

When the ECB adopted a fixed-rate, full-allotment regime in October 2008, it also expanded its list of eligible assets. Specifically, it added:

- marketable debt issued in the eurozone but denominated in dollars, pounds, and yen,

- debt instruments issued by credit institutions traded on specific non-regulated markets, subject to a 5% haircut,

- subordinated debt instruments guaranteed by financially sound guarantors,

- syndicated loans governed by three sets of laws, including Welsh or English law,

- fixed-term deposits, if transferred to the Eurosystem, and

- marketable securities rated as low as BBB- except for asset-backed securities (Regulation No 1053 2008).

Figure 5 reprints key eligibility criteria from before and after the collapse of Lehman Brothers.

The ECB imposed haircuts on all collateral posted. It did not change its general haircut policies during the Global Financial Crisis but did tweak their parameters. Its policy before and during the GFC sought to mitigate risk by applying haircuts on the value of collateral posted by counterparties. It used a schedule of haircuts that varied by credit rating, maturity, asset class, and whether the asset offered coupons (ECB 2006). Shortly after the ECB expanded eligible collateral, it ratcheted up haircuts on credit claims and asset-backed securities (ECB 2009a, tables 6-7), and added an additional 8% haircut to the haircuts normally applied for collateral that was denominated in a foreign currency (ECB 2008c). (See Appendix 1 for full pre- and post-October 2008 haircut schedules.)

If on any day the value of collateral fell below that required, national central banks applied margin calls to raise collateral. Counterparty branches in any euro area country could deposit collateral on behalf of the branch that received the liquidity. To enforce these requirements, the ECB had at its disposal an array of possible sanctions, including expulsion from current and future open-market operations (ECB 2006). Crisis-era changes added three possible penalties to this list—initial margins, limits on the amount of collateral from one issuer or debtor, and additional guarantees (ECB 2009a, box 7)—but no documents suggest that such penalties were ever applied.

Figure 5: Eligibility Criteria of Collateral Posted for ECB Monetary Policy Operations

Sources: ECB 2006, table 4; Regulation No 1053 2008.

Sources: ECB 2006, table 4; Regulation No 1053 2008.

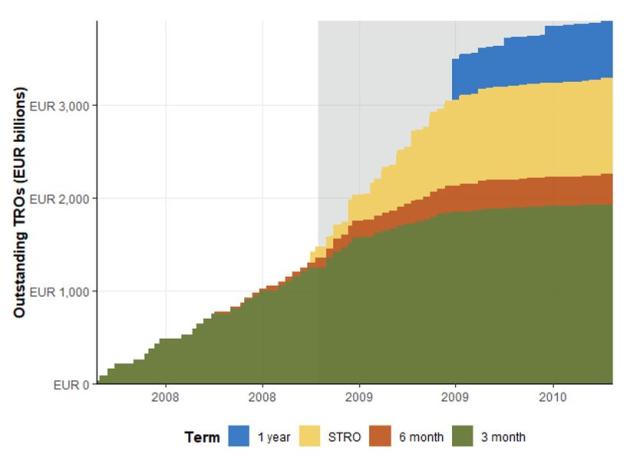

Loan Duration

1

The majority of operations carried three-month maturities, as shown in Figure 6; this was the only longer maturity available before the ECB decided in March 2008 to conduct six-month LTROs (ECB 2020). Following the collapse of Lehman Brothers, the ECB supplemented its long-standing end-of-month LTROs with regular, mid-month special-term refinancing operations (STROs) with maturities matching the supervisory reserve maintenance period, the four-to-five-week period over which banks’ average reserve positions were calculated for regulatory purposes (ECB 2007). It also introduced several six-month LTROs (ECB 2008a). In May 2009, the ECB announced three one-year operations (ECB 2009c). They explained their decision to offer banks year-long funding at the rates equal to the ECB’s one-week facility simply by citing “continuity and consistency with the operations … undertaken since October 2008” (Jones 2009).

Figure 6: Cumulative TROs, by Maturity

Note: The shaded area represents the period during which the ECB operations carried a fixed rate and full allotment.

Source: ECB 2021.

Other Conditions

1

No documents indicate that ECB liquidity support carried conditions besides haircuts, margin calls, and excluding counterparties.

Impact on Monetary Policy Transmission

1

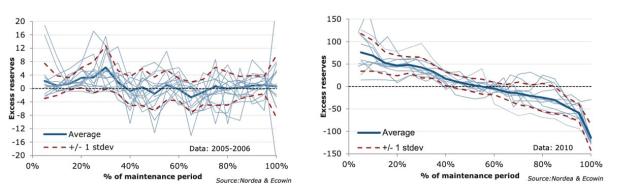

The separation principle, which held that liquidity-focused operations were separate from monetary policy, drove the administration of TROs. Before the crisis, significant liquidity was not provided for long terms or for as much as participants could demand. At the end of the reserve maintenance period, banks sometimes had more liquidity than desired for interest-rate purposes, and sometimes they had less. The ECB used FTOs to “smooth the effects on interest rates caused by unexpected liquidity fluctuations” (ECB 2006). Unlike the main and longer-term refinancing operations, FTOs could be liquidity-providing or liquidity-absorbing. These operations allowed the ECB to reset the liquidity position at the end of the reserve maintenance period. As shown in the left panel of Figure 7, reserve balances were unbiased throughout the maintenance period, and FTOs may therefore have provided or absorbed liquidity at the end of the maintenance period.

However, the role of end-of-maintenance-period FTOs evolved. In 2008, the ECB developed a practice called “frontloading” whereby it provided large amounts of liquidity through TROs early in the reserve maintenance period before siphoning it from the system at the end of the period. This practice biased excess reserves to the start of the maintenance period and biased reserve deficits to the end of the maintenance period, as shown in the right panel of Figure 7. Since reserve requirements were calculated as average reserves over the course of the maintenance period, it did not matter for the purposes of regulations how banks achieved that average.

Just before the ECB expanded collateral and adopted a fixed-rate, full-allotment regime, it expanded the eligible participants in FTOs to include all banks eligible for open-market operations (ECB 2008b). This expansion allowed all banks subject to the reserve requirement to front-load their supervisory requirements and not worry about holding excess reserves later in the month (Svendsen and Wojt 2014). Front-loading remained a legacy of the GFC after the crisis passed, though mostly for a different reason. To prevent the deflationary risks posed by the Sovereign Debt and Euro crises, as well as the differing risks to eurozone economies posed by the COVID-19 pandemic, the Eurosystem purchased trillions of euros worth of securities from banks and conducted similarly large three-year LTROs, see Runkel (2022b) for a detailed study of that intervention (Lawson 2020). Like the TROs, these operations produced excess liquidity in the eurozone. As a result, the ECB had not—as of August 2021—conducted a liquidity-providing FTO at the end of a maintenance period since March 11, 2008. The shift from MRO liquidity to TROs was paralleled by the shift “from stable FTOs to FTOs centered around -10% of the [minimum reserve requirement] on the last day of the period” (Cassola and Huetl 2010). Front-loading, paired with these last-day FTOs kept medium-term rates stable in the face of the ECB’s enormous liquidity injections (Cassola and Huetl 2010).

The ECB also conducted six liquidity-providing FTOs at various points earlier in maintenance periods to cushion the interbank market around the rollovers of its large LTROs. These were not used to offset excess liquidity and are detailed in Figure 2.

Figure 7: Evolution of Front-loading from 2007 (left) to 2010 (right)

Source: Svendsen and Wojt 2014.

Other Options

1

The central bank relied on large, liquidity-providing FTOs as the first line of defense against tumultuous markets (Borio and Nelson 2008). After four large FTOs, it announced the first SLTRO. In April 2008, after a second burst of liquidity-providing FTOs, it announced six-month LTROs. In October 2008, after five FTOs failed to quell markets, it announced STROs; fixed-rate, full-allotment; and expansions to its set of eligible collateral (Runkel 2022a). Since October 2008, the ECB has only used liquidity-providing FTOs to cushion LTRO rollovers as detailed in KDD 3.

During the GFC, TROs became the ECB’s main channel of liquidity, accounting for 72% of the bank’s main refinancing volume. Before the crisis, one- and two-week MROs provided most liquidity. The bank wrote that:

the ECB increased the maturity of its operations by increasing the amounts allotted in longer-term refinancing operations at the expense of main refinancing operations with a view to smoothing out conditions in the term money markets and conducted fine-tuning operations at the end of maintenance periods in order to offset liquidity imbalances (ECB 2009b).

Similar Programs in Other Countries

1

Many central banks scaled up their repurchase operations during the Global Financial Crisis. The Bank of England’s Extended Long-Term Refinancing operations (ELTRs) and the Bank of Canada’s Term Purchase and Resale Agreements (PRAs) most closely resembled TROs. In the English version, the central bank expanded the size and eligible set of collateral for the three-month tenders and continued offering 6-, 9-, and 12-month maturities (Bank of England 2007). In the Canadian version, the central bank introduced 1-, 3-, 6-, 9-, and 12-month repos (Zorn, Wilkins, and Engert 2009, appendix 1). Both accepted a wide range of collateral, including sovereign debt, corporate bonds, and asset-backed instruments (Bank of England 2007; Zorn, Wilkins, and Engert 2009, appendix 1).

Communication

1

Most communication from the ECB came through a series of 47 notices released between August 22, 2007, and March 29, 2010. Forty-four of these press releases announced new tenders of SLTROs, STROs, or regular, monthly LTROs. These tender announcements occasionally reiterated ECB policies, like on August 22, 2007, when the measure aimed “to support a normalization of the functioning of the euro money market” (ECB 2020). ECB officials supplemented this communication with speeches and press conferences in which they articulated the separation principle (Trichet 2007; Manuel González-Páramo 2011). This guideline split monetary policy—the maintenance of medium-term price stability—from liquidity management—the negotiation of short-term conditions with crisis tools—and gave the ECB space to inject large amounts of reserves without confronting critics who charged it with fostering inflation (ECB 2019, 13, 148).

Starting in 2009, tender announcements carried the proviso that TROs could begin to be offered at a spread over the main refinancing rate (ECB 2009c). However, the ECB never took this option (ECB 2021). The ECB also formally announced tenders over wire service the day before it accepted bids, in keeping with its standard-tender policies (ECB 2006). Eleven STROs were announced alongside SLTROs during the GFC, all following the collapse of Lehman Brothers (ECB 2020).

Three other press releases announced the expansion of collateral and adoption of fixed-rate, full-allotment; the schedule of one-year LTROs; and the phase-out of fixed-rate, full-allotment (ECB 2010b). Key Design Decision 20 discusses this last change, which the ECB abandoned with the onset of the Sovereign Debt Crisis.

Disclosure

1

ECB reporting guidelines did not change throughout the crisis. Since the nature of tenders changed from variable-rate to fixed-rate, full-allotment, reports changed accordingly. On the day of allotment, the day before tenders were settled (ECB 2006, chart 1), the ECB reported the total amount bid by counterparties (potential counterparties in the case of tenders without full allotment), the total amount allotted, and, in the case of variable-rate tenders, the marginal and maximum bid rates (ECB 2006). The ECB did not report which counterparties bid for a tender, nor did the Governing Council report minutes of its meetings.

Stigma Strategy

1

Open-market operations used aggregate disclosures to limit stigma. Aggregate disclosures limited the ability of market observers to identify who borrowed from the facility. ECB press releases do not mention borrowing stigma, and academic literature does not suggest that it was a significant hurdle. ECB officials said that stigma was not usually associated with refinancing operations.

Exit Strategy

1

At the end of 2009, the ECB offered its last SLTRO and reverted back to its pre-crisis status quo offering one tender in the last week of each month (ECB 2021). In March 2010, the ECB (ECB 2010b) announced its intention to phase out fixed-rate, full-allotment LTROs. It settled a three-month LTRO on April 29 using a variable rate and fixed allotment. The next week, Greek debt troubles spilled over into the first episode of Europe’s Sovereign Debt Crisis (Bilefsky and Thomas Jr. 2010). The ECB abandoned its phase-out plans and announced that it would continue offering fixed-rate, full-allotment LTROs (ECB 2010c). As of 2021, the ECB still tendered three-month LTROs by fixed-rate, full-allotment. The central bank phased out six-month LTROs in 2010, one-year operations in 2012, and ended regular STROs in 2014 (ECB 2021). The ECB added three-year LTROs in 2011, which were heavily subscribed (Lawson 2020). By this time, the ECB had also moved away from the separation principle, realizing that its liquidity tools could boost its monetary policy goals by putting downward pressure on rates (ECB 2019, 3).

Key Program Documents

-

(Trichet 2009) Trichet, Jean-Claude. 2009. “The ECB’s Enhanced Credit Support.” Working Paper 2833. Monetary Policy and International Finance. Munich: CESifo.

Speech given by the ECB president describing SLTROs, longer-maturity LTROs, increased collateral, and fixed-rate, full-allotment.

-

(ECB 2007) European Central Bank (ECB). 2007. “Publication of the Indicative Calendar of Reserve Maintenance Periods for 2008.” Press release.

Calendar detailing start and end dates of reserve maintenance periods.

-

(ECB 2008a) European Central Bank (ECB). 2008a. “Measures to Further Expand the Collateral Framework and Enhance the Provision of Liquidity.” European Central Bank.

Crucial announcement of fixed-rate, full-allotment and collateral expansion following the collapse of Lehman Brothers.

-

(ECB 2009a) European Central Bank (ECB). 2009a. “Guideline of the European Central Bank of 23 October 2008 Amending Guideline ECB/2000/7 on Monetary Policy Instruments and Procedures of the Eurosystem.” Official Journal of the European Union 52, no. L 36: 31–45.

Crisis-era revision to ECB’s operating guidelines; full breakdown of collateral expansion, and new possible sanctions.

-

(ECB 2020) European Central Bank (ECB). 2020. “Summary of Ad Hoc Communication.” Internet Archive.

Dataset of each nonperiodic notice issued by the ECB; the primary channel of announcements for new tenders.

-

(ECB 2006) European Central Bank (ECB). 2006. “Guideline of the European Central Bank of 31 August 2006 Amending Guideline ECB/2000/7 on Monetary Policy Instruments and Procedures of the Eurosystem.” Official Journal of the European Union 49, no. L 352: 1–90.

ECB’s precrisis policies and a general primer on how the Eurosystem functions.

-

(Regulation No 1053 2008) Regulation (EC) No. 1053/2008 of the European Central Bank of 23 October 2008 on Temporary Changes to the Rules Relating to Eligibility of Collateral. 2008. 282 OJ L. ECB: 32008R1053.

Official publication of collateral expansion.

-

(European Union 1992) European Union. 1992. “Protocol (No. 18) on the Statute of the European System of Central Banks and of the European Central Bank.” Official Journal of the European Communities. Treaty on European Union. C 191. EUR-Lex.

Protocol annexed to the Treaty on European Union authorizing the ECSB; article 18 authorizes the ECB and national central banks to undertake open-market operations including repurchase agreements and lending.

-

(Atkins 2010) Atkins, Ralph. 2010. “ECB Avoids Disruption as Banks Repay Funds.” Financial Times, July 1, 2010.

Article describing maturity of several hundred billion euros in large term refinancing operations.

-

(Bank of England 2007) Bank of England. 2007. “Central Bank Measures to Address Elevated Pressures in Short-Term Funding Markets.”

Press release explaining the first round of ELTRs.

-

(Bilefsky and Thomas Jr. 2010) Bilefsky, Dan, and Landon Thomas Jr. 2010. “Greece Takes Its Bailout, but Doubts for the Region Persist.” The New York Times, May 3, 2010, sec. Business.

Article describing the start of the Sovereign Debt Crisis.

-

(Jones 2009) Jones, Sam. 2009. “Unconventional Conventions at the ECB.” Financial Times, May 7, 2009, sec. Alphaville.

Article with quotes from ECB President Jean-Claude Trichet about the introduction of one-year LTROs.

-

(Kaminska 2011) Kaminska, Izabella. 2011. “On the ECB’s ‘Most Significant Non-Standard Measure.’” Financial Times, December 8, 2011, sec. Opinion.

Article interpreting the speech by Manuel González-Páramo and SLTRO’s impact on yields.

-

(Bank of France 2021) Bank of France. 2021. “EONIA and EURIBOR.” Daily data. BOF/QS_D_IEUTIO3M; BOF/QS_D_IEUEONIA. Quandl.

Daily EONIA and EURIBOR rates.

-

(ECB 2008b) European Central Bank (ECB). 2008b. “Counterparties for Fine-Tuning Operations.” Press release.

Press release announcing that FTOs will open to all counterparties eligible for standard-tender open-market operations.

-

(ECB 2008c) European Central Bank (ECB). 2008c. “Further Technical Specifications for the Temporary Expansion of the Collateral Framework.” European Central Bank.

Press release clarifying the particulars of collateral expansion.

-

(ECB 2009c) European Central Bank (ECB). 2009c. “Longer-Term Refinancing Operations.” European Central Bank.

Announcement that ECB would offer one-year LTROs.

-

(ECB 2010b) European Central Bank (ECB). 2010b. “ECB Announces Details of Refinancing Operations with Settlement up to 12 October 2010.” European Central Bank.

Announcement that ECB would phase-out GFC policies.

-

(ECB 2010c) European Central Bank (ECB). 2010c. “ECB Decides on Measures to Address Severe Tensions in Financial Markets.” European Central Bank.

Announcement that, in light of the Sovereign Debt Crisis, it would abandon plan to phase-out GFC tender policies.

-

(Bowman 2010) Bowman, David. 2010. “The ECB’s Use of Term Refinancing Operations.” Memo 2. Federal Open Market Committee. Washington, D.C.: Federal Reserve.

Internal Federal Reserve memo summarizing SLTRO activity and impact.

-

(ECB 2009b) European Central Bank (ECB). 2009b. “Annual Report 2008.” Frankfurt am Main.

Annual report describing monetary policy stance and changes of the Eurosystem.

-

(ECB 2010a) European Central Bank (ECB). 2010a. “Annual Report 2009.” Frankfurt am Main.

Annual report describing monetary policy stance and changes of the Eurosystem.

-

(ECB 2019) European Central Bank (ECB). 2019. A Tale of Two Decades: The ECB’s Monetary Policy at 20. Luxembourg: Publications Office.

ECB study reviewing the monetary policy frameworks and their inflection points between 1999 and 2019.

-

(ECB 2021) European Central Bank (ECB). 2021. “History of All ECB Open Market Operations.”

Dataset of open-market operations: rates, dates, volumes, and procedures.

-

(Manuel González-Páramo 2011) Manuel González-Páramo, José. 2011. “The ECB’s Monetary Policy during the Crisis.” Closing speech presented at the Tenth Economic Policy Conference, Málaga, October 21.

Speech by ECB Executive Board member on the impacts of SLTROs and tender procedures.

-

(Svendsen and Wojt 2014) Svendsen, Anders, and Alexander Wojt. 2014. “The Liquidity Management of the ECB.” Explanatory note presented at the Nordea, March.

Consultant presentation describing the ECB’s frontloading policy.

-

(Trichet 2007) Trichet, Jean-Claude. 2007. “Introductory Statement with Q&A.” Frankfurt am Main, September 6.

Press conference articulating the ECB’s separation principle for the first time.

-

(Trichet 2010) Trichet, Jean-Claude. 2010. “State of the Union: The Financial Crisis and the ECB’s Response between 2007 and 2009.” Journal of Common Market Studies 48, no. s1: 7–19.

The ECB president’s account of the central bank’s policies during the Global Financial Crisis.

-

(Zorn, Wilkins, and Engert 2009) Zorn, Lorie, Carolyn Wilkins, and Walter Engert. 2009. “Bank of Canada Liquidity Actions in Response to the Financial Market Turmoil.” Bank of Canada Review, 3–22.

Bank of Canada review on its activities in the autumn quarter of 2009.

-

(Borio and Nelson 2008) Borio, Claudio, and William Nelson. 2008. “Monetary Operations and the Financial Turmoil.” BIS Quarterly Review, International banking and financial market developments, no. March: 31–46.

Study comparing the central bank responses of Australia, Canada, the Eurozone, Japan, Switzerland, and the United States to the Global Financial Crisis.

-

(Cassola and Huetl 2010) Cassola, Nuno, and Michael Huetl. 2010. “The Euro Overnight Interbank Market and ECB’s Liquidity Management Policy During Tranquil and Turbulent Times.” Working Paper 1247. European Central Bank. 1678446. Social Science Research Network (SSRN).

Study examining the efficacy of ECB monetary policy.

-

(Fratzscher, Duca, and Straub 2016) Fratzscher, Marcel, Marco lo Duca, and Roland Straub. 2016. “ECB Unconventional Monetary Policy: Market Impact and International Spillovers.” IMF Economic Review 64, no. 1: 36–74.

IMF research paper evaluating the effect of SLTROs on asset prices.

-

(Lawson 2020) Lawson, Aidan. 2020. “The European Central Bank’s Three-Year Long-Term Refinancing Operations.” Journal of Financial Crises, 2, no. 3: 352–68.

YPFS case study on the so-called “very long-term refinancing operations” (VLTROs) during the Sovereign Debt Crisis.

-

(Runkel 2022a) Runkel, Corey N. 2022a. “European Central Bank: Fine-Tuning Operations.” Journal of Financial Crises 4, no. 2/.

YPFS case describing the Eurosystem's FTOs during the GFC.

-

(Runkel 2022b) Runkel, Corey N. 2022b. “Eurozone: Pandemic Emergency Purchase Programme.” Journal of Financial Crises 4, no. 2.

YPFS case reviewing the eurozone’s PEPP.

-

(Runkel 2022c) Runkel, Corey N. 2022c. “United States: Term Auction Facility.” Journal of Financial Crises 4, no. 2.

YPFS case study reviewing the Federal Reserve’s Term Auction Facility during the Global Financial Crisis.

-

(Smith 2020) Smith, Ariel. 2020. “The European Central Bank’s Covered Bond Purchase Programs I and II.” Journal of Financial Crises 2, no. 3: 382–404.

YPFS case study reviewing the ECB’s CBPP1 and CBPP2.

Figure 8: Pre-October 2008 ECB Haircut Schedule

Figure 9: Post-October 2008 ECB Haircut Schedule

Taxonomy

Intervention Categories:

- Broad-Based Emergency Liquidity

Countries and Regions:

- Euro Zone

Crises:

- Global Financial Crisis