Market Support Programs

Corporate Bond Secondary Market Scheme (UK)

Purpose

To improve market liquidity in order to remove obstacles to corporate access to credit.

Key Terms

-

Announcement DateMarch 19, 2009

-

Operational DateMarch 25, 2009

-

Expiration DateAugust 4, 2016

-

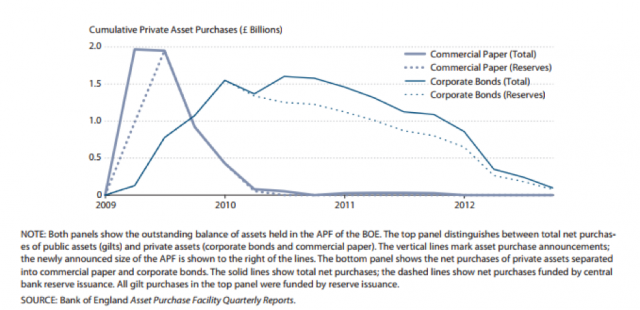

Peak Utilization£1.6 billion

-

ParticipantsHM Treasury, Bank of England

Key Design Decisions

Purpose of MLP

Auction or Standing Facility

Program Size

Program Duration

Prelaunch Public Consultation

Eligible Institutions

Eligible Collateral or Assets

Disclosure

Key Program Documents

Taxonomy

Intervention Categories:

- Market Support Programs

Countries and Regions:

- United Kingdom

Crises:

- Global Financial Crisis