Broad-Based Emergency Liquidity

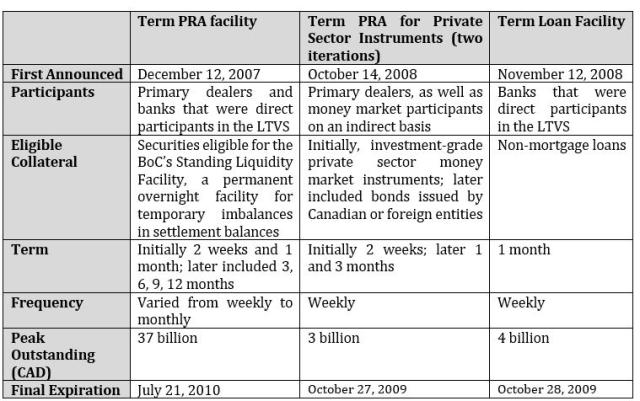

Canada: Term Purchase and Resale Agreement Facility

Purpose

To “provide funding liquidity directly to major market participants to stabilize the financial system and to limit spillover effects to the broader economy” (Longworth 2010)

Key Terms

-

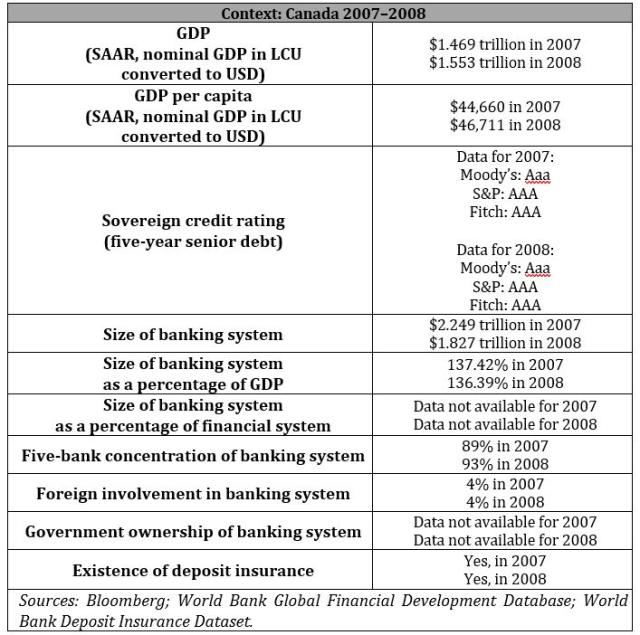

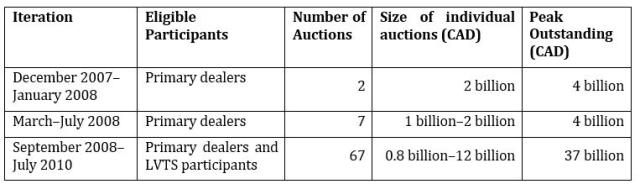

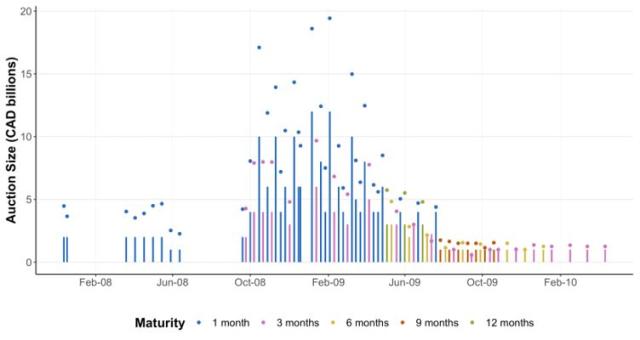

Launch DatesFirst iteration: December 12, 2007; Second iteration: March 11, 2008; Final iteration: September 18, 2008

-

Expiration DateJuly 21, 2010

-

Legal AuthorityBank of Canada Act Section 18

-

Peak OutstandingCAD 37 billion

-

ParticipantsPrimary dealers and banks that participated in the Large Value Transfer System (LVTS)

-

RateMultiple yield competitive auction

-

CollateralInitially narrow range of collateral, but widened to include all collateral accepted in the Standing Liquidity Facility

-

Loan DurationInitially one month; later three months; extended up to 12 months

-

Notable FeaturesCoordinated with actions taken by six other central banks

-

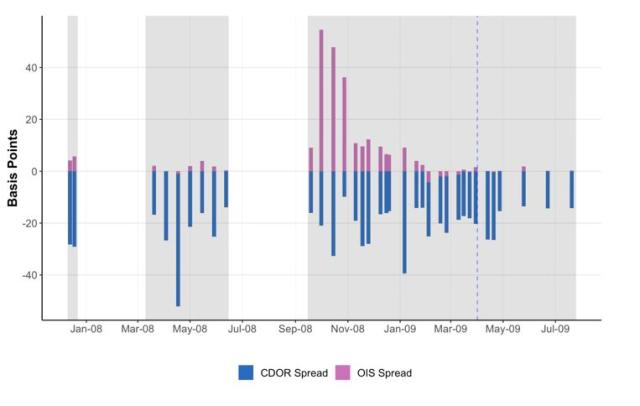

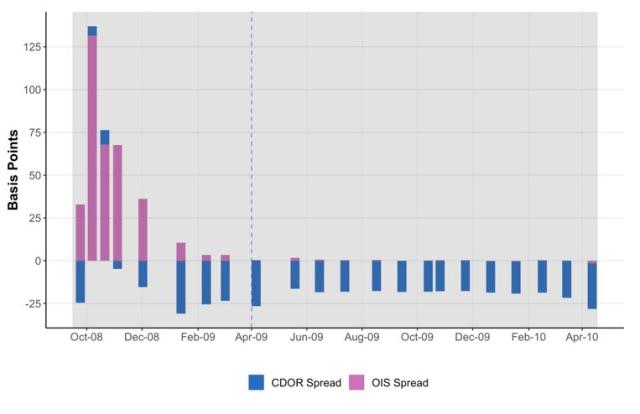

OutcomesWidespread usage of the facility coincided with a reduction in bank financing costs.

Key Design Decisions

Purpose

Part of a Package

Management

Administration

Funding Source

Program Size

Individual Participation Limits

Rate Charged

Eligible Collateral or Assets

Loan Duration

Other Conditions

Impact on Monetary Policy Transmission

Other Options

Similar Programs in Other Countries

Communication

Disclosure

Stigma Strategy

Exit Strategy

Key Program Documents

Taxonomy

Intervention Categories:

- Broad-Based Emergency Liquidity

Countries and Regions:

- Canada

Crises:

- Global Financial Crisis