Market Support Programs

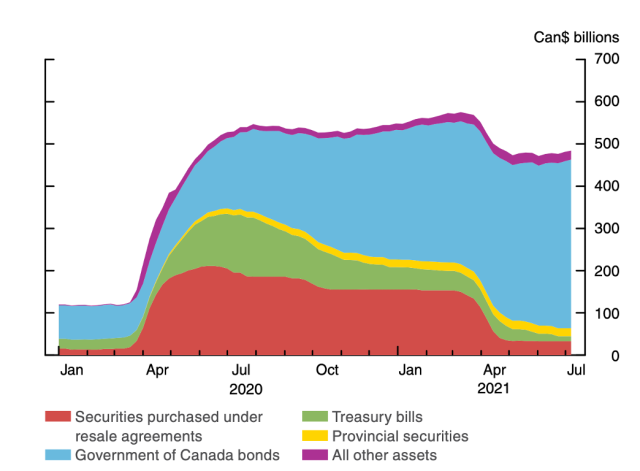

Canada: Provincial Bond Purchase Program

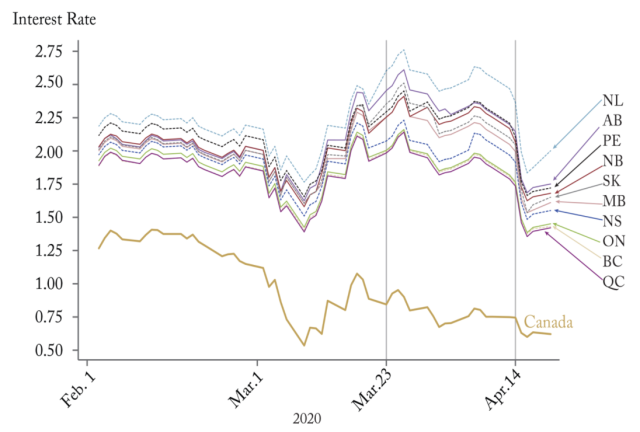

Purpose

To “support the liquidity and efficiency of provincial government funding markets” by purchasing bonds in the secondary market (BoC 2020b).

Key Terms

-

Launch DatesAuthorized: 1991 Announced: April 15, 2020

-

Operational DateMay 7, 2020

-

End DateMay 7, 2021

-

Legal AuthoritySection 18(c) of the Bank of Canada Act

-

Source(s) of FundingSettlement balances

-

AdministratorBMO Global Asset Management

-

Overall SizeCAD 50 billion

-

Eligible Collateral (or Purchased Assets)CAD-denominated bonds issued by or guaranteed by a provincial or territorial government

-

Peak UtilizationCAD 17.558 billion on May 6, 2021

Key Design Decisions

Purpose

Part of a Package

Governance

Administration

Communication

Disclosure

SPV Involvement

Program Size

Source(s) of Funding

Eligible Institutions

Auction or Standing Facility

Loan or Purchase

Eligible Collateral or Assets

Loan Amounts (or Purchase Price)

Other Conditions

Haircuts

Interest Rate

Fees

Term

Regulatory Relief

International Cooperation

Duration

Key Program Documents

Taxonomy

Intervention Categories:

- Market Support Programs

Countries and Regions:

- Canada

Crises:

- COVID-19