Account Guarantee Programs

Belgium: Protection Fund/Special Protection Fund

Purpose

To guarantee the protection of Belgian bank customers and savers, the continuity of the activity of financial companies, the preservation of employment, and the protection of economic life (BFPS 2008a)

Key Terms

-

Launch DatesAnnouncement: Oct. 10, 2008; Authorization: Nov. 17, 2008; Operation: EUR 50,000 effective Oct. 7, 2008; EUR 100,000 effective Nov. 17, 2008

-

End DateOriginally set to last one year, later adopted as permanent

-

Eligible InstitutionsCredit institutions, investment firms, and insurance companies

-

Eligible AccountsDeposit accounts, financial instruments, and life insurance products

-

FeesProportion of covered deposits, financial instruments, and gross income

-

Size of GuaranteeFDP: up to EUR 50,000; SPF: EUR 50,000 to EUR 100,000

-

CoverageUnknown

-

OutcomesEUR 522.4 million collected in fees; no payouts

-

Notable FeaturesFast implementation; Two-tranche funding; Coverage of class 21 life insurance products; Payouts offset by outstanding liabilities; Large institutions’ deposits not covered

At the height of the Global Financial Crisis (GFC) in fall 2008, the Belgian government increased the coverage limits of its deposit guarantee to restore faith in its banking system, protect savers and depositors, and safeguard financial stability. Belgium joined the European Union’s (EU) efforts to strengthen deposit guarantee systems. The measures complemented the Belgian government’s other efforts to secure domestic banks. The government implemented the emergency measures in October and November 2008 through royal decrees, which Parliament later incorporated into law. In a five-week span, Belgian authorities increased the deposit guarantee from EUR 20,000 to EUR 100,000 (USD 26,820 to USD 134,100). They also expanded coverage to include deposit-like life insurance products. Two public institutions administered the guarantees for credit institutions and investment firms: the existing Protection Fund for Deposits and Financial Instruments (FDP) guaranteed deposit balances up to EUR 50,000, and the newly created Special Protection Fund for Deposits and Life Insurance (SPF) guaranteed balances between EUR 50,000 and EUR 100,000. Separately, the SPF guaranteed “class 21” life insurance products up to EUR 100,000. The FDP and SPF collected contributions from members. The FDP could also use assets collected by legacy insurance funds prior to the FDP’s establishment in 1998. FDP and SPF protection was compulsory for both credit institutions and investment firms. SPF protection was originally voluntary for life insurers and later became compulsory; life insurers were not members of the FDP. Annually, FDP and SPF members contributed a proportion of their income and assets eligible for protection to the funds. Fees were initially uniform and later became risk based. Protected assets included a range of deposit accounts, financial instruments, and “class 21” life insurance products that offered a fixed return. In 2010, authorities lowered payment timelines from three months to 20 working days, in line with EU guidance. The government initially set a timeline of one year for the higher deposit guarantee limits but later made them permanent. The FDP held collective assets of more than EUR 800 million by year-end 2008. Both the FDP and SPF went unused from 2008 through 2011. External evaluations about the intervention are positive, with scholars arguing that it helped to restore stability to the Belgian banking system during the GFC.

During September and October 2008, Belgian banks avoided systemic runs, yet several large Belgian credit institutions faced liquidity issues after interbank liquidity evaporated and institutional investors withdrew their deposits in large quantities (CBFA 2009). Belgian authorities responded with targeted emergency measures, including capital injections and blanket guarantees, meant to assist six financial institutions, the first four of which were systemic credit institutions: Fortis, Dexia, KBC, ING, bancassurer Ethias, and the Belgian branch of Icelandic bank Kaupthing (CBFA 2009). The Belgian government coordinated with other European Union (EU) member states to partially nationalize Dexia (Luxembourg, France) and Fortis (Luxembourg, Netherlands) (WTM 2019a; WTM 2019b). In light of the extraordinary rescue measures aimed at individual banks, the Belgian state also enacted broad-based interventions by issuing state guarantees on bank debt and deposits (CBFA 2009; Petrovic and Tutsch 2009).

The European Council’s Economic and Financial Committee (ECOFIN) convened on October 7, 2008, to discuss the EU’s crisis response, including a plan to harmonize deposit insurance limits across member states (EC 2008). Among other measures, member states agreed to guarantee deposits up to at least EUR 50,000 (EC 2008). Finance ministers belonging to the Group of Seven (G-7) released a similar press release on October 10, 2008, announcing their agreement to ensure that G-7 deposit insurance and guarantee programs were “robust and consistent” (G-7 2008). On October 10, 2008, Belgian authorities announced the forthcoming increase of deposit insurance coverage from EUR 20,000 to EUR 100,000 (USD 26,820 to USD 134,100),FEUR 1 = USD 1.341 on October 10, 2008 (Bloomberg). exceeding the EU’s guidance (BFPS 2008a). Emergency legislation followed on October 15 and November 17, 2008 (King of Belgium 2008; Parliament 2008a). The former permitted the king to issue new regulations to combat financial stability, and the latter retroactively raised the deposit insurance limit to EUR 50,000 for deposits dated October 7, 2008, and later and to EUR 100,000 beginning November 17, 2008 (King of Belgium 2008; Parliament 2008a). The moves were meant to preserve confidence in the financial system and strengthen the protection of depositors (King of Belgium 2008).

The Belgian system operated with two tiers. The primary Belgian deposit insurance authority was the Protection Fund for Deposits and Financial Instruments (Fonds de Protection des Dépôts et des Instruments Financiers, hereinafter FDP), which guaranteed the first EUR 50,000 of deposits and up to EUR 20,000 of financial instruments (King of Belgium 2008). By royal decree, the Belgian King established a separate Special Protection Fund for Deposits and Life Insurance (Fonds Spécial de Protection des Dépôts et des Assurances sur la Vie, hereinafter SPF), which guaranteed deposit balances between EUR 50,000 and EUR 100,000 and extended coverage to specific life insurance products that previously lacked coverage (King of Belgium 2008).

Both funds were financed by members’ annual contributions and other fees; the FDP could also fund guarantees with assets collected by legacy insurance funds prior to the FDP’s establishment in 1998 (King of Belgium 2008, chap. I, art. 7; FDP 2009b). FDP and SPF protection was compulsory for both credit institutions and investment firms (FDP 2009b; FDP 2011). Insurance companies, which did not issue deposits and were not members of the FDP, could volunteer to insure deposit-like “class 21” products with the SPF for a fee; this coverage became compulsory in 2011 (FDP 2009b; FDP 2011). Assets eligible for the FDP’s deposit protection included deposit funds (demand, savings, and term accounts), debt securities (vouchers, bonds, and certificates of deposit) representing deposits, and funds of any currency held by credit institutions and stock exchange companies awaiting return or allocation of financial instruments (FDP 2009b). FDP member institutions paid annual fees based on eligible deposits, income, and financial instruments (FDP 2009b). SPF coverage required annual contributions separate from those paid to the FDP (King of Belgium 2008, art. 7). Insurance companies paid fees based on eligible deposits and inventory reserves (King of Belgium 2008, chap. I, art. 8).

Following the European Central Bank’s (ECB’s) recommendations, Belgium designed the new SPF’s reimbursement rules, conditions, and limitations to align those with the existing FDP (ECB 2008). The FDP and SPF payout processes shared three triggers: a member institution declared bankruptcy, a member institution suspended payments, or the Belgian financial market supervisor determined that the member could not reimburse its clients’ claims (King of Belgium 2008, chap. I, art. 6; FDP 2009a, sec. 2, para. 8). Initially, the FDP had to reimburse depositors within three months of an institution’s failure, which was later shortened to 20 working days beginning in January 2011, in line with EU guidance (FDP 2011; FPSCPM 2010, chap. 7).

As of July 2010, the Belgian deposit guarantee system covered about 95% of eligible deposits (Van Nieuwenhuyze and Zachary 2010). The FDP did not pay out on any guarantees through year-end 2011 (FDP 2009b, 20; FDP 2010, 8; FDP 2011, 20; FDP 2012c, 22). After its promulgation, the November 14 Royal Decree would have expired unless it was confirmed by the Belgian Parliament within 12 months of declaration (ECB 2008; Parliament 2002; Parliament 2008a). On December 22, 2008, the Belgian Parliament confirmed the November 14 Royal Decree through a corresponding program law, making permanent the crisis-time expansion of depositor guarantees (Parliament 2008b). Though the government initially specified a one-year duration on the emergency increase, Belgian deposit insurance remains at EUR 100,000 per depositor as of June 2022 (BFPS 2008b; FSMA 2022c).

Overall, evaluations of Belgium’s increase in deposit insurance limits are positive. The Belgian Banking, Finance, and Insurance Commission (Commission Bancaire, Financière et des Assurances, hereinafter CBFA)—the financial market supervisor in 2008—argues that the combination of capital injections and guarantees stabilized market confidence in domestic financial institutions and preempted a systemic run on banks (CBFA 2009; FSMA 2022b).

Scholars have documented similar effects and explained the transmission mechanisms of changes to Belgian deposit insurance by using proprietary micro data from more than 300,000 Belgian depositors (Atmaca et al. 2020). Atmaca et al. (2020) argue that the increase in deposit insurance restored depositors’ trust in banks during the crisis. The study also posits that a higher trust in government enhances the effectiveness of higher deposit insurance coverage limits on limiting depositor withdrawals. The scholars document “depositor bunching” near the EUR 20,000 limit in the run-up to the Global Financial Crisis (GFC) and near EUR 100,000 after the limit was increased. The latter effect was stronger during the period of reprivatization than nationalization, which may be related to depositors’ belief in an implicit blanket guarantee of state-owned banks (Atmaca et al. 2020).

Key Design Decisions

Purpose

1

Noting turmoil in financial markets, the Belgian government took measures to preserve confidence in the financial system and strengthen the protection of depositors (King of Belgium 2008). The government increased the coverage of its deposit guarantee to safeguard the stability of the financial system, protect customers and savers of Belgian banks, and preserve their confidence in the banking system (BFPS 2008b).

Belgium also increased its deposit guarantee to EUR 100,000 to help uphold EU-wide financial stability (FDP 2009b). During the crisis, unharmonized deposit guarantees caused some cross-border tensions among EU members (IMF 2009). On October 7, 2008, European finance ministers convened to plan a pan-EU response to the GFC (EC 2008). They later proposed measures meant to harmonize depositor protection across the EU, which the European Parliament adopted on December 18, 2008 (European Parliament 2008). Directive 2009/14/ECFDirective 2009/14/EC amended Directive 94/19/EC, which standardized—among other features—the minimum coverage levels between EU member states’ deposit guarantee systems (EC/EP 2009). went into force on March 11, 2009, and the five major provisions were:

- Increasing the minimum guarantee to EUR 50,000 immediately and to EUR 100,000 by December 31, 2010;

- Reducing the maximum payment period from three months to 20 working days;

- Abolishing coinsurance;

- Informing depositors of new guarantee arrangements and notifying those account holders not protected by the guarantee schemes; and

- Committing to reviews by the European Commission (EC/EP 2009).

Belgian officials raised their minimum guarantee two years ahead of the time frame adopted by the European Commission and Parliament (FDP 2009b).

Part of a Package

1

The GFC threatened several systemically important Belgian banks in the second half of 2008. Domestic political authorities took several actions to safeguard the banks’ health, including capital injections and state guarantees on interbank and wholesale credit (CBFA 2009). The Belgian government also implemented a broad credit guarantee scheme with opt-in eligibility, though no banks applied for or used the program (Lawson 2020). In relation to Fortis’s sale to BNP Paribas, the Belgian government also guaranteed the minimum value of certain impaired assets and risk positions (Petrovic and Tutsch 2009). With respect to both quantity and size of rescue measures, most of Belgium’s interventions occurred between September 2008 and April 2009 (Petrovic and Tutsch 2009).

Legal Authority

1

To increase deposit insurance coverage, Belgium relied on four statutes: the Law of 15 October 2008 on Measures to Promote Financial Stability, the Royal DecreeFAccording to one external reviewer, royal decrees are symbolically the king’s decisions, but in practice, they are decisions made by the kern, which is an inner cabinet consisting of the prime minister and deputy prime ministers. The kern can legislate without parliamentary approval, and the Belgian Parliament rarely disagrees with the kern’s decisions. Royal decrees may take two forms:

The king delegates new executive responsibilities to one or more of his ministers; the minister(s) must implement the regulation and assume political responsibility; or the king exercises already vested power by modifying, replacing, supplementing, or repealing laws (Justice en Ligne 2008). of 14 November 2008, Law of 22 December 2008, and Royal Decree of 16 March 2009 (FDP 2009b).

On October 15, 2008, the Belgian Parliament passed a lawFThe Belgian Parliament implemented the new framework by amending the existing Law of August 2, 2002, on the Supervision of the Financial Sector and on Financial Services—Article 117bis of the August 2002 Law describes measures related to financial stability (Parliament 2002; Parliament 2008a, title 2). establishing a supervisory framework for financial stability and granting the Belgian king broad authority to respond to a financial crisis (Parliament 2008a, title 2). The October 15 law allowed the king of Belgium, on the advice of the Financial Stability Committee, to limit the scale or effects of a systemic financial crisis by:

- Adding or changing legislation related to the supervision of insurance companies, credit institutions, investment firms, and the financial sector; and

- Creating a guarantee system for commitments made by the aforementioned regulated institutions (Parliament 2008a, title 2).

Exercising his emergency authority on November 14, 2008, Belgian King Albert II issued a royal decree raising the existing deposit insurance coverage vis-à-vis the FDP from EUR 20,000 to EUR 50,000 and establishing a new Special Protection Fund for Deposits and Life Insurance for balances between EUR 50,000 and EUR 100,000 (King of Belgium 2008, arts. 1, 6). The EUR 50,000 limit took retroactive effect beginning October 7, 2008, and the EUR 100,000 limit began on November 17, 2008 (King of Belgium 2008).

The king’s November 14 Royal Decree also identified mandatory participants for the SPF, including credit institutions, investment firms, branches of European Economic Area (EEA)FThe EEA is an international agreement between the EU member states and three European Free Trade Association states (Iceland, Liechtenstein, and Norway) that allows the latter to fully participate in the EU’s single market, enabling the “four freedoms” of goods, capital, services, and persons, plus competition and State Aid rules and horizontal areas related to the four freedoms (EEA 2013). financial institutions operating in Belgium, and other investment management companies (King of Belgium 2008, art. 4, sec. 1). Insurance companies could opt to guarantee life insurance policies designated as class 21, which was a savings product in the form of a life insurance contract (FSMA 2022a; King of Belgium 2008, art. 4, sec. 2).

After its promulgation, the November 14 Royal Decree would have expired unless it was confirmed by the Belgian Parliament within 12 months of declaration (ECB 2008; Parliament 2002; Parliament 2008a). On December 22, 2008, the Belgian Parliament confirmed the November 14 Royal Decree through a corresponding program law, making permanent the crisis-time expansion of depositor guarantees (Parliament 2008b, chap. 6, art. 199). On March 16, 2009, the king issued another royal decree specifying the conditions under which the government paid out deposits and payment parameters such as timing (King of Belgium 2009).

Administration

1

Belgium legislators established the FDP as a public organization in 1998 and tasked it with maintaining the domestic deposit insurance system, calculating fees, collecting contributions, and managing assets (FDP 2009b). The FDP's mission was to compensate holders of cash or securities accounts who faced potential damage when their financial institutions could not reimburse cash or return securities. By providing guarantees, the FDP attempted to maintain confidence in the financial system (FDP 2009b). The FDP was responsible for onboarding member institutions, executing intervention files, monitoring regulations, reporting on regulatory developments, and planning for the protection of deposits and financial instruments in collaboration with other European authorities (FDP 2009b).

The FDP Secretariat was responsible for managing the financial resources needed to conduct interventions, and two committees managed the FDP’s day-to-day operations (FDP 2009b). The Management Committee set the FDP's general investment policy according to asset class, country of origin, and duration; the Investment Committee executed investment directives (FDP 2009b).

While the Royal Decree of November 14, 2008, raised the FDP’s protection from EUR 20,000 to EUR 50,000, it also established a separate SPF within the Caisse des Dépôts et Consignations, which was a special departmentFThe Caisse des Dépôts et Consignations was the public financial institution responsible for managing deposits across public and private institutions by using national register numbers (for individuals) and company numbers (for institutions) (FPSF n.d.a). The Caisse mobilized funds between any entities contractually obligated to deposit money as collateral with one another (FPSF n.d.a). of the Ministry of Finance (“Federal Public Service Finance”), under the immediate authority of the minister of finance (King of Belgium 2008, art. 3). The General Administration of the Treasury served as the head of the SPF (King of Belgium 2008, art. 3). The SPF funded any claims in excess of EUR 50,000, up to EUR 100,000 (FDP 2009a, chap. 2, sec. 4, para. 14).

Governance

1

A board of directors, consisting of equal representatives of the financial sector and the government, administered the FDP (Van Nieuwenhuyze and Zachary 2010). The FDP's Management Committee was responsible for designing, implementing, and monitoring internal controls over annual accounts and reports (FDP 2009b). The FDP published information for member institutions and the Belgian public through annual reports, press releases, and pages on its website (FDP 2012a). The FDP had to publish information for depositors and investors, including the names of member institutions whose coverage had ended under the Belgian system, in the event of default, the terms and conditions of compensation to any related party, and the deadlines for payment (FDP 2009a, chap. 5, paras. 64-66).

The Royal Decree of November 14, 2008, established a separate SPF within the Belgian Ministry of Finance under the immediate authority of the minister of finance (King of Belgium 2008, art. 3). The Belgian king had the power to regulate the SPF’s organization and operation (King of Belgium 2008, art. 3). The Belgian king set the conditions, terms, and limitations of reimbursement of the SPF, which maintained the same triggers for default as the FDP (King of Belgium 2008, chap. I, art. 6). In its review of the emergency legislation passed on October 15, 2008, the ECB encouraged the Belgian king to align the SPF’s reimbursement conditions, terms, and limitations with those of the existing FDP (ECB 2008). The Ministry of Finance broadly described the SPF’s activities in its annual reports to Parliament, under sections also describing the Caisse des Dépôts et Consignations’ activities (King of Belgium 2008, chap. I, art. 10).

Communication

1

The Belgian government first announced the guarantee on October 10, 2008 (BFPS 2008a). A follow-up press release on October 12 framed the measure as part of larger efforts to protect domestic bank customers and savers (BFPS 2008b). Observing turbulence in financial markets, the government described the need to preserve confidence in the financial system and strengthen the protection of depositors (King of Belgium 2008).

On October 14, Belgian Prime Minister Yves Leterme presented to Parliament an emergency bill enabling a state guarantee meant to restore confidence (Leterme 2008). Leterme also stressed the need for European member states to cooperate with their neighbors to resolve the international financial crisis (Leterme 2008). He publicly requested that Luxembourgish Prime Minister Jean-Claude Juncker raise Luxembourg’s guarantee to EUR 50,000 and alluded to the thousands of Belgian customers of the Luxembourgish branch of an Icelandic bank, Kaupthing, which had entered bankruptcy the week prior (BFPS 2008b; Leterme 2008; Wintersteller 2013). On October 17, 2008, Luxembourg Minister of the Treasury Budget Luc Frieden announced his government’s plans to increase deposit insurance coverage to EUR 100,000, which took effect on January 1, 2009 (Chamber of Deputies 2010; Frieden 2008).

Size of Guarantee

1

On November 14, 2008, Belgian authorities raised the coverage level of deposit guarantees to EUR 100,000 per depositor for one year, with the option to extend the policy if necessary (BFPS 2008b). Belgian authorities implemented this change by increasing the FDP’s guarantee from EUR 20,000 to EUR 50,000 and creating the SPF to cover deposit balances between EUR 50,000 and EUR 100,000 (FDP 2009b). The two-tranche financing regime made no functional difference to depositors, but member institutions paid additional contributions to fund the higher coverage (FDP 2009b). The FDP’s expendable funds topped EUR 800 million by year-end 2008. Neither the FDP nor the SPF made payouts from 2008 through 2011, as no further Belgian banks failed (FDP 2009b; FDP 2010; FDP 2011; FDP 2012c). By year-end 2008, the total number of guaranteed institutions was 112, including 59 credit institutions, 23 stock exchange companies, 26 asset managers/investment advisors, and four collective investment companies (FDP 2009b).

Source and Size of Funding

1

The FDP Secretariat was responsible for managing the financial resources needed to conduct interventions (FDP 2009b). FDP resources included contributions from financial institutions after its creation in 1998, investment proceeds, and holdover assets from previous protection systems (FDP 2009b).

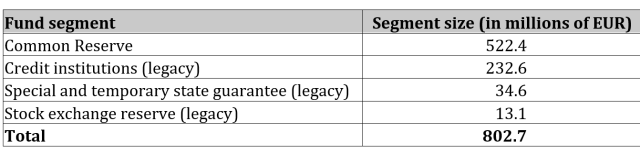

The FDP's pool of funds for intervening in member institutions was known as the “intervention reserve” (FDP 2009b). The intervention reserve contained a “common reserve” of contributions paid since 1999 and legacy funds’ contributions prior to 1999; the legacy funds were organized according to the type of member institution (for example, credit institutions and stock exchanges) (FDP 2009b). To pay out a guarantee from the intervention reserve, the FDP drew down assets first from the corresponding legacy fund, then the common reserve, and later other legacy funds within the intervention reserve (FDP 2009b). In 2007, the European Commission estimated Belgium’s deposit funding ratio—available deposit insurance funds relative to outstanding liabilities—at 0.33 percent (Van Nieuwenhuyze and Zachary 2010). As of December 31, 2008, the intervention reserve contained a total of EUR 802.7 million (FDP 2009b). Figure 1 captures the breakdown between common and legacy funds:

Figure 1: Intervention Reserve Breakdown at Year-end 2008

Source: FDP 2009a, 30.

Source: FDP 2009a, 30.

Prior to the passage of Belgium’s emergency law on October 15, 2008, ECB officials suggested that Belgium follow three funding principles for deposit guarantee schemes to create the SPF:

- The costs of financing are borne, in principle, by credit institutions themselves;

- The financing capacity of the scheme is in proportion to credit institutions’ liabilities; and

- The stability of the banking system of the member state is not jeopardized (ECB 2008).

In practice, the SPF’s designs reflected the ECB’s suggestions. The SPF was financed by annual contributions and entry fees paid by member institutions (King of Belgium 2008, chap. I, art. 7). If the assets contained in the SPF were insufficient to reimburse depositors of a failing credit institution, the Caisse des Dépôts et Consignations advanced the funds (King of Belgium 2008, chap. I, art. 9, sec. 2). Thereafter, the government’s advance was reimbursed by either half of subsequent contributions from mandatory participantsFAdditionally, if the failing institution was an asset manager, investment advisor, or collective investment company, then the Caisse des Dépôts et Consignations demanded additional contributions from each institution: an initial EUR 4,000 plus 0.5% of annual income until the payout was cleared (King of Belgium 2008, chap. I, art. 9, sec. 3). or a special contribution to be paid by participating insurance companiesFIf the failing company was an insurance company, then each covered insurance company paid 0.01% until the payout was cleared (King of Belgium 2008, chap. I, art. 9, sec. 4).—depending on whether the failed institution belonged to the first or second category (ECB 2008; King of Belgium 2008, chap. I, art. 9, sec. 3).

Eligible Institutions

1

FDP membership was compulsory for credit institutions and investment firms, and the Banking, Finance, and Insurance Commission required financial institutions to obtain membership prior to operating in Belgium (FDP 2009b). Insurance companies were not members of the FDP (FDP 2009a, chap. 1). The FDP protected assets held by: (1) a credit institution governed by Belgian law, (2) a bank branch established in Belgium whose host country was outside the EEA and whose coverage was lower than Belgian coverage, and (3) Belgian investment firms authorized to conduct individual portfolio management, including stock exchange companies, portfolio management companies, investment advisors, and collective investment managers (FDP 2009b). FDP membership was optional for EEA-originated bank branches established in Belgium, and they had to first rely on their home countries for protection before receiving supplementary FDP support (FDP 2009a, chap. 3, para. 54).

When Belgian legislators created the SPF, they offered optional membership to insurers of “class 21” life insurance contracts as part of a larger effort to preserve confidence in the financial system (FDP 2012b). Otherwise, SPF membership eligibility was the same as that of the FDP (FDP 2009a, chaps. 1-2; King of Belgium 2008, chap. I, art. 4). Beginning in 2011, SPF membership became compulsory for insurance companies offering class 21 policies, following the passage of a law on December 23, 2009 (FDP 2011).

Eligible Accounts

1

Clients eligible for FDP protection included natural persons, associations, or small or medium-sized enterprises that had cash deposits with a financial institution (FDP 2009b). Professional investors, large companies,FThe deposit guarantee applied to institutions able to draw up abridged balance sheets, excluding large companies that had to file full-format balance sheets (Van Nieuwenhuyze and Zachary 2010). “Large” typically referred to firms employing more than 100 workers annually or companies exceeding more than one of the following conditions: A balance sheet totaling EUR ~3.7 million; annual turnover (excluding VAT) of EUR 7.3 million; or

average number of employees totaling 50 workers (Van Nieuwenhuyze and Zachary 2010). public authorities, and persons and parties related to the failed institution were not eligible beneficiaries under the program because the protection system was meant for ordinary savers (FDP 2009b).

Protected clients were entitled to EUR 100,000, regardless of the number of accounts that they had with an institution, and clients’ claims were offsetFThe author was not able to confirm that the Belgian government continued its offset policy from 2008 through June 2022. However, one external reviewer noted that the government would benefit from discontinuing such a policy. The same reviewer argued that the offset policy might incentivize depositors to seek deposit and loan services from separate banks, creating inefficiencies in the payout framework. by outstanding debt with the same institution (FDP 2009b). Assets covered under deposit protection included deposit funds (demand, savings, and term accounts), debt securities (vouchers, bonds, and certificates of deposit) representing deposits,FRepresentative deposits included debt securities denominated in euros, monetary units of an EU member state, or the Norwegian kroner or Icelandic kronur (FDP 2009b). Debt securities also had to be nonsubordinated, registered, or held in an account or overdrawn deposit with the issuing institution (FDP 2009b). and funds of any currency held by credit institutions and stock exchange companies awaiting return or allocation of financial instruments (FDP 2009b). Besides deposits, the FDP also insured a variety of financial instruments.FProtected financial instruments included any securities (shares, bonds, special investment funds issued by a third party) held on behalf of clients by a credit institution or stock exchange company (FDP 2009b). The FDP exercised a guarantee on financial instruments when depositors could not recover their assets due to the financial institution's failure (FDP 2009b). Central depositories registered financial instruments to both the credit institution and the depositor, with the latter receiving a direct right of claim, so neither owners nor their assets belonged to any common estate resulting from the financial institution’s insolvency (FDP 2009b). Given the protective measures available to owners of financial instruments, the guaranteed amount was not increased and was maintained at EUR 20,000 (FDP 2009b).

Belgian authorities offered to insure specific life insurance products that attracted the same depositors who used traditional savings products offered by credit institutions, up to EUR 100,000 (FDP 2009b). The SPF could guarantee life insurance contracts subject to Belgian law and designated “class 21,” including those with a fixed yield on the premiums paid, if the issuer opted for protection (FDP 2009b). When a company joined the scheme, its customers benefited from a guarantee up to the surrender value of their life insurance contract (with a maximum payout of EUR 100,000) dated the day prior to the insurer's default (FDP 2009b). The SPF’s coverage of class 21 life insurance products became compulsory in 2011, following the passage of the law on December 23, 2009 (FDP 2011).

Lawmakers expressed the need to protect class 21 life insurance contracts to preserve confidence in the Belgian financial system (FDP 2012b). According to an official close to the matter, the Belgian government guaranteed class 21 life insurance products in exchange for cooperation by bancassurer Ethias, a large Belgian insurance company, during the rescue of Dexia, a systemically important Franco-Belgian financial institution. On September 30, 2008, Ethias increased its capital stake in Dexia by EUR 150 million on September 30, 2008, as part of a multinational effortFThe Belgian, French, and Luxembourgish governments, along with other key shareholders, injected EUR 6.4 billion in total (Reuters Staff 2008). See Wiggins, Tente, and Metrick (2019b) for more information. to stabilize the latter (Reuters Staff 2008). In return for Ethias’ additional share subscription, the Belgian government guaranteed the class of life insurance that included Ethias’ “FIRST” accounts, which functioned as both life insurance and a savings product. Though the inclusion of class 21 life insurance was mainly meant to secure Ethias in its support of Dexia, the guarantee also benefitted other bancassurers.

Fees

1

Initially, the FDP required members to contribute annually 0.0175% of deposits eligible for compensation, and the SPF required them to pay an additional 0.031% (FDP 2009b). Insurance companies that opted into SPF coverage contributed annually 0.05% of inventory reserves related to protected contracts, plus a one-time entry fee of 0.25% (King of Belgium 2008, chap. I, art. 8).

Following the law passed on December 23, 2009, all FDP and SPF members had to pay a one-time fee of 0.10% and an annual contribution of 0.15% of protected funds, beginning in 2011—the new fees replaced the previous contribution system (FDP 2011). The FDP Management Committee decided not to collect contributions in 2010 (FDP 2011).

A credit institution contested the new contribution system in Belgium’s Constitutional Court and argued that the primary component of the contribution (outstanding eligible deposits) did not indicate risk, so the contribution calculation unfairly targeted credit institutions that financed themselves via deposits rather than capital markets (FDP 2012c). The Court ruled on June 23, 2011, that the single contribution calculation was unconstitutional, so authorities passed legislation on December 28, 2011, that installed risk-based calculations based on solvency, liquidity, and asset quality, beginning in 2012 (FDP 2012c). The SPF’s new contribution was set at 0.10%, adjusted for the contributor's individual risk profile, and increased to 0.245% and 0.15% for the years 2012 and 2013, respectively (FDP 2012c).

Process for Exercising Guarantee

1

The FDP’s payout process had three triggers:

- A member institution declared bankruptcy,

- A member institution suspended payments,FBelgian documentation uses the term “concordat judicare” (“judicial composition”), referring to a special legal process by which a financial institution imposes a moratorium on payments up to two years to save itself (Cornil 2001). Either the institution or a public prosecutor can initiate judicial composition, and the process presumes that the institution is salvageable once it drafts and follows a recovery plan (Cornil 2001). or

- The CBFA determined that the member could not reimburse its clients’ claims (FDP 2009b).

The FDP had to publish the default and prospective payment timetables (FDP 2009a, chap. 2, para. 37). To receive the FDP’s payout, depository institutions had to apply for assistance within two months of default (FDP 2009a, chap. 2, para. 38). The FDP had to complete payouts within three months of default, and the CBFA could extend this timeline by up to three three-month periods for deposits (FDP 2009a, chap. 2, paras. 41-42). The FDP could withhold payments if the member had committed fraud, made false claims about its guarantee, or failed to share information with the FDP (FDP 2009a, chap. 2, paras. 43-44).

The third trigger required the CBFA to proactively declare the member institution’s failure and take preventative measures, including guaranteeing its deposits or securities, to assist in its liquidation, reorganization, or takeover—subject to financial availability and other requirements (FDP 2009b). Authorities could take preventative action only if they believed that doing so would be less expensive than allowing default or if default threatened Belgian monetary, credit, or financial systems (FDP 2009b). In these circumstances, each depositor, investor, or client of the failing institution had the right to compensation for the loss that they would have incurred had the institution failed on its own (FDP 2009b).

Following the passage of a law on December 29, 2010, the Belgian deposit guarantee scheme shortened its payout timeline, beginning 2011, from three months to 20 working days, in line with the EU directives on deposit guarantees (FDP 2011; FPSCPM 2010, chap. 7). The prudential supervisor could extend the payment period by 10 days only under exceptional circumstances (FDP 2011). To better meet the shortened payout timeline, the Belgian government created tools allowing for rapid payment to depositors and designed procedures for the prompt transmission of data about the covered assets eligible for assistance (FDP 2011). The December 2010 law also required the managers of Belgian investor protection systems to regularly test their systems for depositor payout (FPSCPM 2010, art. 59).

The Belgian king set the conditions, terms, and limitations of reimbursement of the SPF, which maintained the same triggers for default as the FDP (King of Belgium 2008, chap. I, art. 6).

Other Restrictions

1

SPF members were not permitted to mention protection in their advertising (King of Belgium 2008, chap. I, art. 6). Members who either failed to fulfill obligations to the SPF or transgressed the ban on advertising could lose deposit insurance coverage (King of Belgium 2009, art. 4).

Duration

1

On November 14, 2008, the Belgian king issued a royal decree to raise the coverage level of deposit guarantees to EUR 100,000 per depositor for one year, with the option to extend the policy as needed (BFPS 2008b; King of Belgium 2008). After its promulgation, the November 14 Royal Decree would have expired unless it was confirmed by the Belgian Parliament within 12 months of declaration (ECB 2008; Parliament 2002; Parliament 2008a). On December 22, 2008, the Belgian Parliament confirmed the November 14 Royal Decree through a corresponding program law, making permanent the crisis-time expansion of depositor guarantees (Parliament 2008b). The coverage remains at EUR 100,000 as of June 2022 (FPSF n.d.b).

Key Program Documents

-

(FDP 2012a) Protection Fund for Deposits and Financial Instruments (FDP). 2012a. “Protection Fund Home Page.”

Describes the Belgian Protection Fund’s activities and purpose.

-

(FPSF n.d.a) Federal Public Service Finance (FPSF). n.d.a. “The Deposit and Consignment Fund in a Nutshell.” (In French).

Describes the function and purpose of the Deposit and Consignment Fund.

-

(Van Nieuwenhuyze and Zachary 2010) Van Nieuwenhuyze, Ch., and M. D. Zachary. 2010. “The Belgian Deposit Guarantee Scheme in a European Perspective.” National Bank of Belgium Economic Review, December, 91–106.

Describes the changes to Belgian deposit insurance in the year 2008, and the authors place the Belgian changes within the larger EU-wide transition to harmonizing deposit guarantee schemes.

-

(FPSCPM 2010) Federal Public Service Chancellery of the Prime Minister (FPSCPM). 2010. Law Containing Miscellaneous Provisions (I) (1). Public law number 2010/021133.

Shortened the Belgian depositor payout time to 20 working days.

-

(FSMA 2022a) Financial Services and Markets Authority (FSMA). 2022a. “Class 21 Life Insurance.”

Defines class 21 life insurance.

-

(FPSF n.d.b) Federal Public Service Finance (FPSF). n.d.b. “Protection Systems.” Accessed March 13, 2022.

Describes the deposit protection features available to Belgian depositors.

-

(Chamber of Deputies 2010) Chamber of Deputies. 2010. “Extraits de La Loi Du 19 Décembre 2008 Concernant Le Budget Des Recettes et Des Dépenses de l’Etat Pour l’Exercice 2009. (Mémorial A – N° 200 Du 23 Décembre 2008: Pages 2793 et 2794 Articles 44-2 et 46).” (In French).

Describes the law increasing Luxembourg’s depositor coverage.

-

(Cornil 2001) Cornil, Pierre. 2001. “Judicial Composition.” codeca.be (blog).

Describes the meaning of “judicial composition” and what the process requires from both banks and regulators.

-

(ECB 2008) European Central Bank (ECB). 2008. “Opinion of the European Central Bank of 28 October 2008 at the Request of the Belgian Minister for Finance on a Draft Royal Decree Implementing the Law of 15 October 2008 on Measures Promoting Financial Stability.” Report no. CON/2008/61.

Reviews Belgium’s draft emergency legislation, which was passed October 15, 2008. The ECB welcomed the approach and encouraged officials to specify more payment parameters in future legislation.

-

(EC/EP 2009) European Council and European Parliament (EC/EP). 2009. “Directive 2009/14/EC of the European Parliament and of the Council of 11 March 2009 Amending Directive 94/19/EC on Deposit-Guarantee Schemes as Regards the Coverage Level and the Payout Delay.” Official Journal of the European Union 68/3, March.

Requires EU member states to update their deposit-guarantee systems, in accordance with principles established by the ministers of finance.

-

(European Parliament 2008) European Parliament. 2008. “Position of the European Parliament Adopted at First Reading on 18 December 2008 with a View to the Adoption of Directive 2009/.../EC of the European Parliament and of the Council Amending Directive 94/19/EC on Deposit Guarantee Schemes.”

Describes the proposed measures meant to harmonize depositor protection across the EU, adopted by the European Parliament on December 18, 2008.

-

(FDP 2009a) Protection Fund for Deposits and Financial Instruments (FDP). 2009a. Regulations for Intervention of the Protection Fund.

Describes the Protection Fund’s organizational purpose and function. The regulations are located on pages 48–54 of the FDP Annual Report 2008.

-

(FSMA 2022b) Financial Services and Markets Authority (FSMA). 2022b. “Organization.”

Describes the history of the Belgian macroprudential supervisors.

-

(FSMA 2022c) Financial Services and Markets Authority (FSMA). 2022c. “Protection of Deposits.”

Describes the distinct services offered by the FDP and the SPF.

-

(Justice en Ligne 2008) Justice en Ligne. 2008. “Glossary: Royal Decree.”

Blog describing the function of a Royal Decree within the Belgian legislative system.

-

(King of Belgium 2008) King of Belgium. 2008. Royal Decree Implementing the Law of 15 October 2008 on Measures Aimed at Promoting Financial Stability and in Particular Establishing a State Guarantee Relating to Loans Granted and Other Operations Carried out in the Context of Financial Stability, with Regard to the Protection of Deposits and Life Insurance, and Amending the Law of 2 August 2002 on the Supervision of the Financial Sector and Financial Services. Code 4088. Public law no. 2008/03450.

Establishes the Special Protection Fund, which set Belgian deposit insurance at EUR 100,000.

-

(King of Belgium 2009) King of Belgium. 2009. Royal Decree on the Protection of Deposits and Life Insurance by the Special Fund for the Protection of Deposits and Life Insurance. Public law no. 2009/03114.

Outlines reimbursement procedures for the Special Protection Fund.

-

(Parliament 2002) Parliament of Belgium (Parliament). 2002. Law of August 2, 2002, on the Supervision of the Financial Sector and on Financial Services. Code 3058. Public law no. 2002/03392.

Establishes a system of supervision for the financial sector and services.

-

(Parliament 2008a) Parliament of Belgium (Parliament). 2008a. Law Introducing Measures to Promote Financial Stability and Establishing, in Particular, a State Guarantee for Credits Granted and Other Operations Carried out in the Context of Financial Stability. Code 3690. Public law no. 2008/03425.

Authorizes the King of Belgium to enact a state guarantee for the sake of maintaining financial stability.

-

(Parliament 2008b) Parliament of Belgium (Parliament). 2008b. Program Law (1). Public law no. 2008/21120.

Incorporates Royal Decrees of November 14 into law, formally legalizing the increase in deposit insurance to EUR 100,000; see chapter 6, article 199.

-

(Reuters Staff 2008) Reuters Staff. 2008. “UPDATE 2-FACTBOX-France, Belgium, Luxembourg Invest in Dexia.” Reuters, September 30, 2008.

Describes the joint efforts to recapitalize Dexia by the French, Belgian, and Luxembourgish governments, along with Dexia’s key shareholders.

-

(BFPS 2008a) Belgian Federal Public Services (BFPS). 2008a. “Additional Financial Measures.”

Connects to the original (archived) government website, where Belgium announced an increase to deposit guarantees on October 10, 2008.

-

(BFPS 2008b) Belgian Federal Public Services (BFPS). 2008b. “Financial Crisis: Government Communication.”

Describes the array of measures taken by the Belgian government to combat the Global Financial Crisis in real time.

-

(EC 2008) European Council (EC). 2008. “2894th Council Meeting Economic and Financial Affairs, Luxembourg, 7 October 2008.” Press release, October 7, 2008, no. C/08/279.

Press release summarizing the Council’s coordinated approach in response to the GFC.

-

(FDP 2012b) Protection Fund for Deposits and Financial Instruments (FDP). 2012b. “Protection for Branch 21 Life Insurance.”

Describes the protection of class 21 life insurance.

-

(Frieden 2008) Frieden, Luc. 2008. “Luc Frieden: ‘Le Luxembourg Augmente La Garantie Des Dépôts Bancaires à 100.000 Euros.’” (In French).

Announcement in which Luxembourg pledges to increase its deposit insurance coverage.

-

(G-7 2008) Group of Seven (G-7). 2008. “G-7 Finance Ministers and Central Bank Governors Plan of Action.”

Statement by the Group of Seven countries outlining their response to the GFC.

-

(Leterme 2008) Leterme, Yves. 2008. “Government Statement on Its General Policy.” Belgian Government News.

Describes the Belgian government’s emergency responses to the Global Financial Crisis.

-

(CBFA 2009) Banking, Finance, and Insurance Commission (CBFA). 2009. Annual Report 2008–2009. 2009.

Describes the economic events taking place in Belgium in the run-up to the Global Financial Crisis.

-

(EEA 2013) European Economic Area, Standing Committee of the EFTA States, subcommittee V on Legal and Institutional Questions (EEA). 2013. The Basic Features of the EEA Agreement. European Free Trade Association. July 1, 2013.

Describes the form and function of the EEA.

-

(FDP 2009b) Protection Fund for Deposits and Financial Instruments (FDP). 2009b. FDP Annual Report 2008. April 14, 2009.

Describes the Protection Fund’s activities in the year 2008, including crisis adjustments to the deposit guarantee system.

-

(FDP 2010) Protection Fund for Deposits and Financial Instruments (FDP). 2010. FDP Annual Report 2009. April 26, 2010.

Describes the Protection Fund’s activities in the year 2009, including post-crisis adjustments to the deposit guarantee system.

-

(FDP 2011) Protection Fund for Deposits and Financial Instruments (FDP). 2011. FDP Annual Report 2010. April 18, 2011.

Describes the Protection Fund’s activities in the year 2010.

-

(FDP 2012c) Protection Fund for Deposits and Financial Instruments (FDP). 2012c. FDP Annual Report 2011. March 26, 2012.

Describes the Protection Fund’s activities in the year 2011.

-

(IMF 2009) International Monetary Fund (IMF). 2009. “Euro Area Policies: 2009 Article IV Consultation: Staff Report; Public Information Notice on the Executive Board Discussion; and Statement by the Executive Director for Member Countries.” IMF Country Report No. 09/223.

Examines the euro area in light of the Global Financial Crisis.

-

(Atmaca et al. 2020) Atmaca, Sümeyra, Karolin Kirschenmann, Steven R. G. Ongena, and Koen Schoors. 2020. “Deposit Insurance, Bank Ownership and Depositor Behavior.” SSRN Electronic Journal, December.

Describes the behavior of Belgian depositors in response to the government’s nationalizations and deposit guarantees in 2008.

-

(Lawson 2020) Lawson, Aidan. 2020. “The Belgian Credit Guarantee Scheme (Belgium GFC).” Journal of Financial Crises 2, no. 3: 619–34.

Describes the Belgian Credit Guarantee Scheme launched in response to the Global Financial Crisis.

-

(Petrovic and Tutsch 2009) Petrovic, Ana, and Ralf Tutsch. 2009. “National Rescue Measures in Response to the Current Financial Crisis.” ECB Legal Working Paper Series No. 8, July 2009.

Piece detailing financial responses to the Global Financial Crisis by country.

-

(Wintersteller 2013) Wintersteller, Markus. 2013. “Luxembourg’s Financial Centre and Its Deposits.” ECFIN Country Focus 10, no. 9.

Examines Luxembourg and its deposit insurance system.

-

(WTM 2019a) Wiggins, Rosalind, Natalia Tente, and Andrew Metrick (WTM). 2019a. “European Banking Union C: Cross-Border Resolution–Fortis Group.” Journal of Financial Crises 1, no. 3: 150–71.

Describes the resolution of Fortis Group.

-

(WTM 2019b) Wiggins, Rosalind, Natalia Tente, and Andrew Metrick (WTM). 2019b. “European Banking Union D: Cross-Border Resolution–Dexia Group.” Journal of Financial Crises 1, no. 3: 172–88.

Describes the resolution of Dexia Group.

Taxonomy

Intervention Categories:

- Account Guarantee Programs

Countries and Regions:

- Belgium

Crises:

- Global Financial Crisis