Broad-Based Asset Management Programs

Bank Assets Management Company (BAMC)

Purpose

Sell or restructure assets acquired from banks to maximize their value, such that the BAMC can repay its bonds and minimize taxpayer burden

Key Terms

-

Launch DatesAnnounced: October 2012; Operational: March 20, 2013; First Transfer: December 20, 2013

-

Wind-down DatesInitial: December 31, 2017; Amended: December 31, 2022

-

Size and Type of NPL Problem13% of all loans and 38.3% of all loans to corporates were non-performing as of August 2013. These were concentrated among large non-financial corporates

-

Program SizeNot specified, but limited by €4 billion cap on guaranteed debt issuance

-

Eligible InstitutionsBanks that could not meet capital adequacy requirements for the next year with a credible business plan

-

UsagePurchased assets with a face value of €5.8 billion for €2.0 billion

-

Ownership StructurePublic

-

Outcomes24.7% estimated EROE by 2018 €81 million in net profits (€172 million in net profits for the government) by the end of 2017

-

Notable FeaturesStrategy modeled on NAMA and SAREB Significant intervention from the European Commission

Slovenia weathered the initial shock of the Global Financial Crisis (GFC) of 2008 well enough to return to growth in 2010. However, non-performing loans continued mounting, banks experienced significant losses, and credit growth turned negative in a credit crunch. Slovenia entered a recession in 2011, experiencing the second largest GDP decline in the euro area. It was not certain whether Slovenia had the fiscal space to resolve these problems without requesting a Troika bailout from the European Commission (EC), European Central Bank (ECB), and International Monetary Fund (IMF). In late 2012 the government tried to prevent such a program by combining capital injections with a public asset management company (AMC) called the Bank Assets Management Company (BAMC). The BAMC did not start purchasing assets until December 2013. The EC believed that BAMC’s asset valuation process did not fit their standards and delayed approval for the purchases accordingly. However, the BAMC eventually purchased assets (largely related to Slovenia’s large corporate sector) with a face value of €5.8 billion for €2.0 billion. The European Commission was highly involved in the BAMC’s implementation. The organization’s design left it vulnerable to government interference. Management was initially dominated by a group of international experts who were extremely unpopular with the public and the government, and the organization did not have sufficient powers to demand collection from well-connected corporate debtors, many of them state-owned.

|

Economic Context: Slovenia, 2012-13 |

|

|

GDP

|

$46.607 billion in 2012 $48.416 billion in 2013 |

|

GDP per capita

|

$22,674.49 in 2012 $ 23,516.53 in 2013 |

|

Sovereign credit rating (five-year senior debt)

|

As of Q4, 2012: Fitch: A- Moody’s: Baa2 (negative outlook) S&P: A (negative outlook)

As of Q4, 2013: Fitch: BBB+ Moody’s: Ba1 S&P: A- |

|

Size of banking system

|

$4.46 trillion in total assets in 2012 $4.35 trillion in total assets in 2013 |

|

Size of banking system as a percentage of GDP |

97.0% in 2012 90.8% in 2013

|

|

Size of banking system as a percentage of financial system |

100% (No data for nonbank financial institutions’ assets to GDP) (%)

|

|

Five-bank concentration of banking system |

65.8% of total banking assets in 2012 66.9% of total banking assets in 2013

|

|

Foreign involvement in banking system |

26.0% of total banking assets in 2012 25.0% of total banking assets in 2013 |

|

Government ownership of banking system |

8.87% of the Slovenian banking system’s assets were in banks that were government-controlled (e.g., where government owned 50% or more equity) at the end of 2012

52.77% of the Slovenian banking system’s assets were in banks that were government-controlled (e.g., where government owned 50% or more equity) at the end of 2013 |

|

Existence of deposit insurance |

100% insurance on deposits up to $128,205 (€100,000) in 2012 (Using 0.78 € per $ period average for 2012, using the IMF’s IFS dataset)

100% insurance on deposits up to $133,333 (€100,000) in 2013 (Using 0.78 € per $ period average for 2013, using the IMF’s IFS dataset) |

|

Sources: IMF World Economic Outlook; Bloomberg; World Bank Deposit Insurance Dataset; IMF International Financial Statistics; World Bank Bank Regulation and Supervision Survey; World Bank Global Financial Development Database. |

In late 2008, less than a year after Slovenia adopted the euro, uncertainty stemming from the Global Financial Crisis (GFC) stopped the flow of foreign capital into the small country. This burst a bubble in lending to Slovenia’s corporate sector. Although government and European Commission (EC) actions brought back modest growth in 2010, uncertainty abroad and a credit crunch associated with growing non-performing loans (NPLs) at home forced Slovenia back into recession in 2011. The uncertainty surrounding the NPLs began to threaten Slovenia’s sovereign credit rating, and some observers speculated that the growing crisis would force the government to request a Troika bailout from the EC, ECB, and IMF. To head off those concerns, the government announced a public asset management company called the Bank Assets Management Company (BAMC or DUTB) in late 2012. The AMC would take over and manage banks’ NPLs for five years, after which it would transfer any remaining assets to a Slovenian government holding company. The asset transfers would be coordinated with €3.2 billion in capital injections at the participating banks. An additional €190 million in capital was injected in 2014.

The government established the BAMC on March 20, 2013, but the organization did not begin taking assets off the balance sheets of Slovenia’s large government-controlled banks until December 20, 2013. This was because the BAMC had to delay its purchases until the European Banking Authority (EBA) released Slovenia’s stress-test results in December 2013. The BAMC went on to purchase assets with a total face value of €5.8 billion for €2.0 billion by the end of 2016. Slovenia ultimately did not need a program from the Troika, but did have to extend the BAMC’s lifetime to 2022 to complete the disposal of its assets.

The BAMC paid back €1.28 billion of its €1.97 billion in government-guaranteed debts by the end of 2018, contributed €172 million in profits to the government and state-owned banks by the end of 2017, had an equity position of €56.2 million by the end of 2018, and had €830.1 million in remaining assets by the end of 2018. The BAMC, in combination with €3.39 billion of government capital injections, is seen as having helped Slovenia avoid an IMF-EU bailout. The government argued that the BAMC contributed to Slovenia being one of the most successful countries in the euro area at resolving non-performing assets. But the organization was very unpopular with the public and political class. It was also subject to significant government intervention that limited its independence, and was dogged by corruption investigations. These governance problems were aggravated by the fact that the BAMC was charged not just with managing bad assets, but also with restructuring distressed corporate borrowers.

Key Design Decisions

Part of a Package

1

The BAMC was created as part of the ZUKSB law, which was meant to provide for asset purchases as well as bank capital injections (Bancni vestnik 63[11). Slovenia coordinated the passage of the ZUKSB with the ZSHD law, which set up a new holding company for state-owned assets.FThe passage of these two laws nearly coincided with the €100 million December 20, 2012, government capital injection for NKBM. This injection sought to bring NKBM into compliance with EBA recommendations on solvency levels after the bank failed to raise enough capital from the private sector and took the form of contingent convertible instruments (CoCos) (EC DG COMP 2013a). In response to a challenge from the parliamentary opposition, the constitutional court concluded that the ZUKSB law was constitutional because Slovenia “will have no choice but to request for international financial assistance” if the law were not passed. The troika, if it provided such assistance, would then monitor Slovenia’s compliance, and this would “infringe upon Slovenia’s sovereignty which is a constitutional principle” (Bardutzky 2016).

The BAMC’s legislation allowed it to conduct up to €1 billion worth of capital injections (Slovene Press Agency 2012-09-20). The BAMC would fund these injections from the same €4 billion in state-guaranteed borrowing as its asset transfers (Slovene Press Agency 2012-09-20; ECB 2012). The newly formed Slovenian government decided in May 2013 not to allow the BAMC to exercise this power. While the government did not state its reasoning publicly, former non-executive director of the BAMC Lars Nygaard offered a potential explanation. Recapitalization would leave the BAMC as a “major owner of the big banks on top of all other assets transferred to it, including some big corporates,” which “would have been too much, politically if not economically” (Bancni vestnik 63[11]).

Legal Authority

1

The BAMC’s domestic legal authority came from the Act Defining the Measures of the Republic of Slovenia to Strengthen Bank Stability (“ZUKSB”), which the government passed in October 2012. ZUKSB created a process for banks to apply to participate in the BAMC (Bancni vestnik 63[11]).

As the BAMC entailed state aid, its operations needed to be authorized by the European Commission’s Directorate-General for Competition (EC DG Comp). Even in the absence of a troika program, the EC retained the authority to approve or disapprove all government decisions on asset transfers and capital injections under European rules governing state aid (Bancni vestnik 63[11]; FinSAC 2016).

The EC DG Comp refused to approve asset transfers and capital injections until the Slovenian government (as well as the Bank of Slovenia) coordinated with the EU AQR/ST (EIU 2013-10-07; IMF 2012; BAMC 2014). The EC DG Comp also excluded the BAMC from its asset selection and valuation process, going as far as having the EC DG Comp’s “experts doing independent valuations of all assets suggested by the banks and the supervisor (the Bank of Slovenia) for transfer to BAMC” (Bancni vestnik 63[11]). This delayed the first asset transfers until the end of 2013 (IMF 2012; BAMC 2014). This need for EC DG Comp approvals also delayed asset transfers from Abanka until late 2014 (Slovenian Press Agency 2015-10-06; BAMC 2015; EC DG Comp 2014).

Special Powers

1

The ZUKSB gave the BAMC and the government a number of broad powers over banks. The most significant of these was the power to establish a Bank Stability Fund, which would then conduct capital injections. The BAMC could use its assets to acquire bank shares and other instruments counted in a bank’s capital, but only “if financial stability in the Republic of Slovenia cannot be achieved by other measures or in a more economical manner” (Unofficial ZUKSB translation 2015). The ZUKSB initially devoted up to €1 billion of the €4 billion in state guaranteed borrowing by the BAMC for such capital injections (Slovene Press Agency 2012-09-20). The Slovenian government could heavily circumscribe the use of this power, though the capital injection powers were never used and appear to have been taken away from the organization in 2015 (BAMC 2014). In December 2015, an amendment to the ZUKSB appeared to take away any reference to how much the government was willing to guarantee BAMC lending that would be used for recapitalizing banks (Slovene Press Agency 2012-09-20; Havrylchyk 2013; EC Staff 2013-04-10; Unofficial ZUKSB translation 2015). By this point, the Slovenian government had already used other maneuvers to recapitalize its banks (Sila 2015; BoS 2015).

The law also allowed the BAMC to order a participating bank to convert bad debt into equity in a company before transferring the exposure. The law also allowed the government to control bank dividend policy, operating costs, and staff remuneration (Havrylchyk 2013). However, the BAMC initially lacked a number of powers possessed by contemporary AMCs in Ireland and Spain, which included the ability to provide loans to borrowers and to ensure the AMC acquired a majority position in borrowers (BoS 2014; Sila 2015).

The government largely solved these problems with the previously mentioned December 2015 amendments to the ZUKSB. These amendments gave the BAMC a number of new powers and responsibilities related to restructuring debtors (BAMC Strategy 2016; IMF 2017). For example, it extended the period in which the BAMC was allowed to have voting rights in a participating borrower if the BAMC would have to dispose of the related assets from two to five years (Unofficial ZUKSB translation 2015).

The BAMC was not fully fleshed out when the legislature passed the ZUKSB. The BAMC and Slovenia’s strategy for using the BAMC evolved over time, sometimes dramatically changing with the economic and political situation (Bancni vestnik 63[11]; ENP Newswire 2013). Slovenia went through four ruling coalitions and prime ministers between early 2012 and late 2014. The ZUKSB did not envision the BAMC playing a role in activities like facilitating bank mergers and resolution, though the government eventually asked the BAMC to perform these activities in late 2015 with the Abanka-Bank Celje merger and throughout 2016 when the BAMC absorbed Factor Banka and Probanka (the ZUKSB-A saw the BAMC conducting some of these activities). This required BAMC staff to be extremely flexible (BAMC 2015; Bancni vestnik 63[11]; Havrylchyk 2013; BAMC Strategy 2016).

Mandate

1

The BAMC was set up to be a comprehensive restructuring agency for the Slovenian banking sector, performing capital injections, asset purchases, and corporate restructuring (EC Staff 2013-04-10). However, the BAMC was predominantly focused on the asset-purchase function. Within the ambit of its asset purchase operations, the BAMC aimed to minimize the taxpayers’ burden while repaying BAMC bondholders. The BAMC would do this by maximizing the value of its assets (BAMC 2014; BAMC 2014a). The government also intended to use the BAMC as a tool to eventually conduct restructurings throughout the Slovenian economy (Slovenia NRP 2013). The government understood that the BAMC’s operations could provide support for individual companies with promising business models though mechanisms like exchanging a company’s loan for an equity stake (BAMC Strategy 2016).

Communication

1

The government referred to the BAMC as a bad bank and had trouble getting the Slovenian public to understand what an AMC was. One early BAMC administrator attributed this lack of understanding to the intense debate surrounding the passage of the ZUKSB (Bancni vestnik 63[11]; Slovene Press Agency 2012n). The BAMC began its operations with a straightforward “From Bad to Good” communications policy that aimed to shift the media’s focus from anticipating the consequences of the BAMC’s actions to evaluating the BAMC’s performance (BAMC 2014).

This was unsuccessful at creating support for the BAMC among politicians and the media. The BAMC developed an adversarial relationship with the government and the Bank of Slovenia in the run-up to its asset transfers (BAMC Press Release 2014-10-30; Bancni vestnik 63[11], 101-112; BAMC Press Release 2014-12-18). Executives at the BAMC had an even less positive relationship with the press. They produced long and sometimes sarcastic statements that attempted to refute negative coverage (BAMC Press Release 2014-12-18a; BAMC Press Release 2015-07-13).

In response to the critical reports by the CPC and the Court of Auditors, the BAMC pursued an anti-corruption certification program from private anti-bribery and corruption certification agency ETHIC Intelligence in late March 2015 (BAMC PR 2015b).

The BAMC’s relationship with the government and press apparently became less strained once Nyberg and Månsson left the BAMC (Slovenian Press Agency 2018-07-05; Slovenian Press Agency 2015-10-06; Balogh 2018). The new management adopted a more generic communications strategy around 2016 (BAMC Strategy 2016), which revolved around five principles:

- supporting BAMC’s strategic goals by promoting understanding of the role of BAMC and benefits BAMC brings to the Republic of Slovenia and the taxpayers, in key audiences;

- obtaining the support of key audiences in implementation of measures;

- managing media relations, that will, as far as possible, support the achievement of BAMC’s objectives;

- ensuring the “one company one voice” communication effect; and

- changing BAMC’s communication from being reactive to being proactive (BAMC Stakeholder Strategies).

With this new strategy came a less blunt slogan: “Creating Good with Excellence” (BAMC 2018a).

Ownership Structure

1

The BAMC was organized as a publicly owned joint-stock company because of an interaction between the 2009 changes in Eurostat’s rules and the characteristics of Slovenia’s banking sector at the time. In 2009, as Ireland was developing its own AMC, Eurostat decided that “AMCs with less than 51 percent private ownership would not be classified as contingent liabilities” and would be immediately counted “against public debts and deficits.” While Ireland, and later Spain, found workarounds that allowed them to comply with this rule, the state-dominated structure of Slovenia’s banking sector made it virtually impossible to create an AMC with less-than-majority state ownership. The government thus had no choice but to structure the BAMC as a publicly owned AMC. Professors Gandrud and Hallerberg hypothesized that the Slovenian government had the BAMC acquire its assets at “large haircuts relative to those applied at AMCs in other EU countries” because it wanted to “partially offset the cost of public AMC ownership” by maximizing profits passed on to the government (Gandrud and Hallerberg 2016).

Governance/Administration

2

The BAMC had a “one-tier governance system,” in which the organization was governed by a Board of Directors containing four non-executive directors (appointed by the government) and three executive directors (appointed by the non-executive directors) (BAMC 2014). The OECD said that this structure “allows for greater influence of the single shareholder —the government—on operations” (Sila 2015). The CPC questioned the wisdom of this structure, arguing in late 2014 that “a two-tier governance system would contribute to reducing corruption and other risks which the company was exposed to in the course of its operations and warned about potential conflict[s] of interest” (BAMC 2015). Because the government was the sole shareholder, the BAMC’s “purchases and business plans are [were] approved by the Slovenian government” (IMF 2014).

In response to corruption allegations and management changes, the BAMC modified its governance system in late 2015 (BAMC PR 2015f; BAMC PR 2015H; BAMC Strategy 2016). From this point, the non-executive directors were restricted to having a supervisory (as opposed to a management) role within the organization. These modifications also shortened the mandate of board members appointed before the passage of the 2015 amendment to the ZUKSB to December 31, 2017, at the latest (BAMC Strategy 2016).

All members of the board were exempt from legislative limits on executive pay, which the BAMC’s creators thought would “sweeten the deal” (Slovene Press Agency 2012-09-20). Dovetailing with this explanation, the majority of its initial board was dominated by foreign experts “with links to the key European crisis management actors” (Piroska and Podvrsic 2019; IMF 2014).FAs of July 31, 2014, there were three foreign non-executive directors, and there was one foreign executive director. The three non-executive directors included the former “President of the ECB Task Force for Crisis Management,” the leader of the IMF’s response to the Asian banking crisis of the late ’90s, and a member who served on the troika in Spain. The single foreign executive director happened to be the former CEO of Reverta, Latvia’s bad bank (BAMC 2014; Lehmann 2017). Former non-executive director of the BAMC Nyberg further elaborated on the BAMC’s focus on international expertise, reflecting that “Since the international credibility of the Slovenian banking sector was very low, the bank needed international consultancies in order to get the green light from Brussels” (The Slovenia Times 2014).

When the government modified the ZUKSB in late 2015, members of the board remained exempt from legislative limits on executive pay, but the government (as the sole shareholder) halved salaries on the board (The Slovenia Times 2015).

The BAMC also had a “performance-based remuneration system” for employees, though it was not the target of widespread public criticism, unlike the performance-based bonuses given to NAMA employees in Ireland (Balogh 2018).

Program Size

1

It is not clear why the Slovenian government chose to limit its guarantees to this size.

Funding Source

1

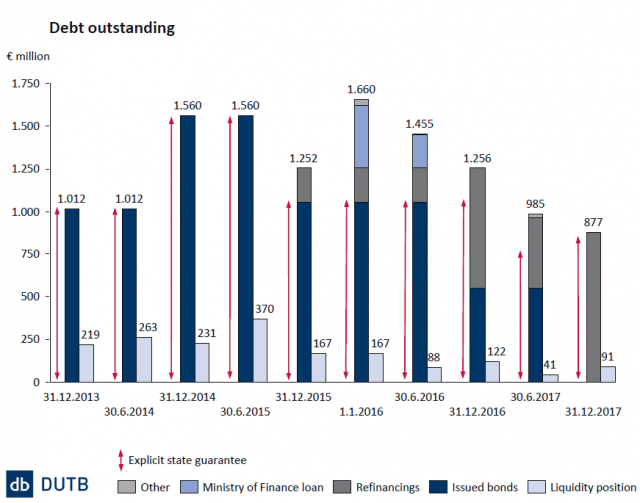

The BAMC funded its asset purchases with government guaranteed bonds with two- and three-year terms, but gradually shifted its financing structure to “Exclusively amortizing low-cost debt” (Balogh 2018). (See Figure 6.) It is also not clear why the Slovenian government charged the BAMC a fee for guaranteeing its bonds, which ranged from 1.00% to 1.25% annually (BAMC 2014; BAMC 2019).

Figure 7: The BAMC gradually shifted the structure of its debt

Source: Balogh 2018, PDF Page 15.

Source: Balogh 2018, PDF Page 15.

Eligible Institutions

1

In late 2013, the Bank of Slovenia described these three banks as those having unresolved measures requiring a capital increase and being in the process of having state aid approved (Bank of Slovenia 2013).

Determining whether a bank was eligible to participate in the BAMC involved two steps. First, the government’s Inter-Ministerial Committee had to establish “that the bank does not have, or will not have within the following 12 months, sufficient capital to meet capital adequacy requirements and, as a result, the stability of the financial system is threatened” (ECB 2013; Bancni vestnik 63[11]). Second, each bank had to submit a business plan to convince the government that the bank was adequately capitalized, that it had an adequate liquidity position, that the bank (as well as the bank’s equity holders) would share the costs of recapitalization during the restructuring,FAs the BAMC ultimately never conducted recapitalizations, this was probably not relevant to the government (BAMC 2014). and that the bank would implement measures to “prevent or mitigate any possible distortion of competition” (ECB 2013). However, other banks did eventually participate in the BAMC. BAMC followed the same procedures in acquiring assets from Banka Celje (Sila 2015). It followed different procedures in acquiring assets from Probanka and Factor Banka. Probanka and Factor Banka first had some of their corporate assets acquired “in arm’s length transactions at negotiated prices”. The BAMC said that it acquired these assets to get enough leverage over a given debtor to execute its plans (Sila 2015; BAMC 2017). Later, the remaining assets of these two banks, which constituted a large number of small exposures, were merged into the BAMC (Balogh 2018). The Bank of Slovenia offered an explanation for the merger, stating that the Slovenian government “economically merited” from the transaction because the government was already the sole owner of all three parties. It elaborated that the merger would allow for “operational rationalization and, most importantly, […][allow] more time for disposing the assets of the acquired companies, consequently increasing the proceeds, and reducing the likelihood of a need” to prop up the two banks with any more capital (BAMC 2017).

Eligible Assets

1

The ZUKSB articulated the process for determining what the BAMC would eventually purchase (Uradni List 2012; Uradni List 2013). While the banks and the Bank of Slovenia prepared an application that would outline the assets the relevant bank wanted to sell, the Inter-Ministerial Committee was responsible for all decisions on what assets would be eligible under the ZUKSB (Nyberg 2014; Uradni List 2012). This committee has not released a methodology for determining which assets should be transferred. The ZUKSB said the Inter-Ministerial Committee would have eight members, all appointed by the Bank of Slovenia and the government (Havrylchyk 2013; Slovenian Press Agency 2019-11-04). However, the Inter-Ministerial Committee would contain members representing the Bank of Slovenia, the Ministry of Finance, the Ministry of Economic Development and Technology, and the Office of the Prime Minister. However, the EC DG Comp, in consultation with the ECB and EBA, ultimately decided which assets would be purchased (BAMC 2014; Bancni vestnik 63[11]; FAQ 2013). As the roots of Slovenia’s problems came from its corporate sector (IMF 2014a), the BAMC mostly acquired large complex corporate exposures from participating banks (Lehmann 2017).

The BAMC’s early management wanted two principles to guide the organization’s asset purchase process. First, it wanted to transfer a bank’s entire exposure to a borrower if the exposure contained both performing and non-performing loans. Second, if the BAMC took over a non-performing loan from a bank, it wanted the BAMC to acquire all of the other exposures (including performing ones) to that borrower from other banks. Management thought that this approach would make it easier to restructure the BAMC’s assets, thus making it easier to increase asset values (Nyberg 2014). However, poor coordination between the BAMC and the Bank of Slovenia meant that these principles were often not practiced, at least for the late 2013 asset transfers (Bancni vestnik 63[11]).

Acquisition - Mechanics

1

All assets would be paid for using government guaranteed bonds with two- and three-year terms issued by the BAMC (Balogh 2018).

The Slovenian government initially thought that “it is sensible to structure assets into groups, so that individual groups with regard to the characteristics of debtors or characteristics of assets which are considered as insurance present a homogenous whole to the creditor in terms of management and realization” (Slovenia NRP 2018).

For its late 2013 asset purchases from NLB and NKBM (as well as its later purchases from Abanka), the BAMC planned for a six-month transfer “in a series of transactions grouped into tranches,” but documentation and time issues forced it to abandon this policy early on (Bancni vestnik 63[11]). In the discussions leading up to these purchases, the government and the Bank of Slovenia wanted the first tranche to be “substantial in size,” but banks favored a smaller transfer, as they were presumably aware of the scale of the documentation problems (BAMC 2014). A 2013 document states that the government planned for the first package to contain “claims against clients in bankruptcy procedures,” for the second package to contain “claims against non-payers insured with real property,” and for the third package to contain “other claims (against restructuring companies, including financial holdings)” (Slovenia NRP 2013).

In actuality, these asset transfers happened at one time and the banks transferred the associated documentation to the BAMC over the next six months. In the meantime, the banks would “act as BAMC’s trustee or asset manager” for the relevant loans (BAMC 2014).

The Slovenian government’s 100% ownership of many companies whose exposures were transferred to the BAMC, as well as its 100% ownership of the participating banks, proved to complicate the asset transfer process. The BAMC’s legislation required the BAMC to recognize asset transfers related to these companies as transactions “between undertakings under [the] common control” of the Slovenian government (BAMC 2019; BAMC 2014). The BAMC revalued these assets upon transfer after they saw that some assets had transfer values that were higher than the values calculated in the AQR. They referred to this €92.6 underpayment as the “day-one” losses associated with revaluing transferred assets, recognizing them as a reduction in the BAMC’s equity (BAMC 2014).

Acquisition - Pricing

1

The ZUKSB said that participating banks (in collaboration with the Bank of Slovenia) would propose initial valuations and transfer prices for the assets, which would then then be finalized (or recalculated entirely) by the Inter-Ministerial Committee (ECB 2013; Bancni vestnik 63[11]; Havrylchyk 2013).

However, final approval ultimately fell to the EC DG Comp, which repeatedly rejected the valuations proposed by the participating banks and the BoS for being too high (BAMC 2014). The EC also argued that these high valuations entailed “an inappropriate amount of state aid” after conducting its own valuation of a sample of loans from the two largest banks. Before approving the valuations and transfer prices, the EC DG Comp required that the Slovenian government hire a team of independent experts to calculate them as part of the larger AQR/ST. While we do not know the haircuts on these assets under the original valuations, the valuation from the team of independent experts were eventually approved by the EC DG Comp and resulted in a 71% haircut (EIU 2013-07-05; Bancni vestnik 63[11]).

When the transfers eventually happened, the Bank of Slovenia evidently refused to share its methodology for calculating these figures with the BAMC. This frustrated the BAMC, which then had to use “consultants to get hold of data from banks, asset by asset, and prepare separate valuations” (Bancni vestnik 63[11]).

Although the valuations eventually approved by the EC apparently did not include this feature, the EC noted that the BAMC’s bylaws provided for transfer values being “reduced by up to 3% of the asset value to cover the administrative and operational costs of the BAMC for managing the assets” (EC 2013-04-10). The BAMC was frustrated with this non-inclusion. It argued that “reducing the value of the transferred assets by the cost of financing and operational costs” was a “fundamental precondition for the financial sustainability of the BAMC” (BAMC 2014).

Management and Disposal

2

The BAMC disposed of assets (equity, debt, and real estate) on a case-by-case basis following the “principal of an economic and transparent use of public funds and their highest possible recovery,” though this sometimes involved transfer to the SSH (presumably at a discount) (Nyberg 2014). Once the BAMC acquired assets, it would revalue them according to their fair value and use the valuation to determine whether a recovery (involving enforcement and liquidation or value improvement) or restructuring (collaboration with BAMC to maximize the going concern value of the asset) asset management strategy would maximize the value of the relevant collateral. This valuation involved comparing BAMC’s cash flows under each strategy using “a probability-weighted average of present values of cash flows of both scenarios discounted at a discount rate” representing the BAMC’s costs. For the restructuring scenario, the BAMC calculated the present value of cash flows by looking at the “debtor’s cash flow forecast and the debt servicing capability,” while the BAMC calculated the figure by looking at “the realistic outcome of realizing collateral” in the recovery scenario (BAMC 2014a).

Although the BAMC did not say why they created these particular strategies, it did state that it tended to favor the recovery strategy because of the generally “poor quality of the claims” (BAMC 2016). Sometimes, even after the 2015 changes to the AMC’s corporate governance, the government ordered the BAMC to transfer certain exposures to larger corporates to the SSH (BAMC 2019; IMF 2017).

The BAMC’s initial exit strategy was to sell ten percent of its assets each year until the end of its approximately five-year lifetime, at which point it would transfer any remaining assets to the SSH. This strategy was imposed on the organization (IMF 2014; Bancni vestnik 63[11]). However, the feature was in tension with the BAMC’s goal of maximizing returns to minimize the taxpayers’ burden while repaying the BAMC’s bonds (Bardutzky 2016; BAMC 2014; IMF 2014).

Timeframe

1

The BAMC initially had a five-year lifetime (where the BAMC would wind down by December 13, 2017) (Bancni vestnik 63[11]). Amendments to the ZUKSB eventually extended the lifetime to 2022 to decrease the risk of a fire sale (BAMC Strategy 2016). As of early 2021 there are questions about where the BAMC will have its lifetime extended again (Slovenian Press Agency 2019-12-20; Slovenian Press Agency 2019-12-23).

A number of commentators say that the BAMC and its related capital injections prevented an IMF-EU bailout (IMF 2014a; Slovenian Press Agency 2019; EBRD 2018). Slovenia’s submission to the 2018 European Semester praised the BAMC, saying Slovenia was one of the better euro-area countries at dealing with bad debts (Slovenia NRP 2018). However, some scholars and Slovenian commentators say that it resulted in Slovenia losing its economic sovereignty and “undermining public trust in national institutions” (Guardiancich 2016; Slovenian Press Agency 2019). Some go as far as saying that the ZUKSB’s passage may not have been constitutional. The rejection of the referendum challenging the ZUKSB seemed to be rooted in a “necessity defense,” in that the measure was necessary to prevent the loss of sovereignty associated with an IMF bailout (Bardutzky 2016).

Lars Nyberg had some early reflections on the BAMC’s performance in 2014. He thought the BAMC was able to address the economy’s NPL problems “at arm’s length from the political system” in a way that was not possible for Slovenia’s bad bank in the 1990s. However, the asset valuation and transfer process was “a mess.” Nyberg also lamented the lack of cooperation between the BAMC and other Slovenian government institutions. Like many others, he was concerned with the requirement that the BAMC sell ten percent of its assets each year, noting that it could “hardly be done without ‘forced sales’ and unnecessary losses” (Bancni vestnik 63[11]; Slovene Press Agency 10-10-2012; Sila 2015).

Other Slovenian government institutions generally took a negative view. The Bank of Slovenia described the BAMC as “unable to take the lead in many important restructuring cases as the claims transferred to them are not sufficiently big to put them in a majority position vis-à-vis other creditors” (BoS 2014). Slovenia’s two main government watchdogs took an even more unfavorable view. The BAMC was in operation for less than three months before the CPC started investigating it (Slovenian Press Agency 2014-02-01). The BAMC had a poor record of implementing measures like maintaining safeguards against debtors buying back their assets from the BAMC at a discount (Slovenian Press Agency 2014-02-01; Sila 2015; Slovenian Press Agency 2018-07-05). The Court of Audit also criticized the BAMC for operating in an “inefficient and non-economic way” (Novak 2015-03-04). An investigation followed the late-2015 management changes, which fueled years of suspicion targeting some of the former executives as well as a parliamentary inquiry. However, none of these executives went to prison (Slovenian Press Agency 2019-10-07; Slovenian Press Agency 2018-07-10). Pressure on the BAMC appeared to die down once the new management accepted the criticisms of the Court of Audit and revised the BAMC’s organizational bylaws to address the Court’s concerns (BAMC PR 2015H). Even after the ZUKSB was amended to make the BAMC more independent and the government reshuffled the BAMC’s board, the Slovenian government institutions (and civil society) continued to criticize the BAMC’s governance (The Slovenia Times 2019; IMF 2017). For a period, criticism ignored the BAMC’s current practices, instead focusing on the days when “Swedish financial experts Lars Nyberg and Torbjörn Månsson” sat on the board (Slovenian Press Agency 2018-07-05; Slovenian Press Agency 2019-06-13). The BAMC’s board was largely stable during this time (BAMC PR 2015g; The Slovenia Times 2019). However, these problems reemerged in late 2018, when the chair of the board and the CEO both resigned (BAMC PR 2015g; Slovenian Press Agency 2019-04-04).FSpecifically, it was alleged that the CEO and head of the board had circumvented executive compensation restrictions (in addition to having previous conflicts of interest) (Slovenian Press Agency 2015-10-06; BAMC 2015; Slovenian Press Agency 2015-10-06; EIU 2015; Slovenian Press Agency 2015-10-01).

Benoît Cœuré of the ECB had a largely positive impression of the BAMC when asked about it in February 2014. He described it as having had a good start and noted that it built up the necessary expertise. Although he did not directly comment on whether the BAMC was independent enough, he said that the BAMC “should keep resisting vested interests” and “continue building up the institution itself so that it is credible and independent” (BIS 2014).

The European Commission and the Council of the European Union, on the other hand, had more mixed opinions on the BAMC. In April 2013, the European Commission published a paper criticizing the BAMC’s relatively short lifetime. This paper argued that the five-year lifetime forces a choice between “actively running off the portfolio, even at the cost of realising losses” and transferring a sizeable amount of assets to the SSH, which was not designed to facilitate the kinds of restructuring required by the BAMC’s assets (EC Occasional Paper 2013). The Council of the European Union’s 2016 recommendation responding to the 2016 National Reform Programme of Slovenia stated that the BAMC made significant progress on restructuring its loans, but remained “a significant risk to the sustainability of public finances” (Council of the European Union 2016). The Council continued, complaining that “Oversight of the activities of the BAMC appears to be insufficient as the authorities had considerably underestimated the deficit of the BAMC in 2015 by 0.7% of GDP and appeared unaware of the level of write-offs performed by the BAMC” (Council of the European Union 2016). By 2019, the Commission had a more positive view of the BAMC, complimenting it for helping reduce NPLs and beginning to make a profit in 2017. However, it also worried about the fact that the government set a “cost efficiency ratio” for the organization, which “will become more and more difficult as residual assets are more costly to manage” (EC 2019).

Reports from the World Bank mostly look at the Slovenian response as a whole, which they deemed generally successful (FINSAC 2016). One World Bank report mentioned that the BAMC had independence issues, but stated that the late-2015 amendments responded to these issues (World Bank 2019). It also acknowledged that the BAMC, with its complex mix of assets tied up in a powerful corporate sector (Lehmann 2017), had a more challenging mix of assets than its contemporaries in Ireland and Spain (World Bank 2019).

The EIU’s coverage of the BAMC tended to point out the BAMC’s negative media attention in Slovenia. They commented that the “BAMC is perceived as a foreign entity in the Slovenian institutional structure, something imposed by the EU that has to be implemented as part of the anti-crisis measures.” Although they note that the attention was focused on the BAMC’s executive pay policies, they acknowledged that the pay was “very high by the standards of government-owned companies in Slovenia,” but “relatively low compared with other similar institutions around the world.” The EIU also thought that the organization did not have necessary powers to “act decisively and push through restructuring” (EIU 2014a). Later on, its opinion of the BAMC slightly improved, with the EIU publishing articles describing the BAMC as “relatively successful.” However, it also believed that the small size of the BAMC contributed to the still stunted credit supply in Slovenia, as the corporate sector remained “highly leveraged” and the banking sector still had problems dealing with NPAs (EIU 2015a).

The IMF generally approved of the BAMC, but even it alluded to the BAMC not being large enough and that the BAMC had governance problems. They welcomed the asset transfers as “key milestones” on the way to recovery. Similar to the EIU in 2015, the IMF thought that the small size of the BAMC, which did not “include most of the loans to corporates that have been restructured by rolling over principal and a portion of interest due,” meant that NPLs would remain high (IMF 2014). It thought that the BAMC still should transfer more assets, even if such transfers “will likely result in a higher public debt in the short run” (IMF 2015).FThe government disagreed (IMF 2015). As for the BAMC’s governance problems, the IMF issued statements emphasizing the need to safeguard the BAMC’s independence, implying that there was some threat to its independence. Along this line, it claimed that the BAMC’s effectiveness hinges on “abstaining from frequent changes in senior management,” which evidently continued to be a problem even after the foreign executives left (IMF 2017). It also criticized the institution for failing to improve its governance and risk management practices between 2013 and 2014 (IMF 2015). The IMF disapproved of the practice of transferring claims to the SSH, which it appeared to connect to the independence issue. The IMF was still concerned about the independence of the BAMC in the months after the removal of the Swedes, but the government partially allayed these concerns with various amendments to the ZUKSB. Among other things (which were discussed in the section addressing the BAMC’s asset management policies), late-2015 amendments clarified that the Ministry of Finance cannot “not issue instructions to the BAMC for action on individual cases” and that “responsibility for management of the BAMC rests with its executive directors” (IMF 2017).

Reports from various other think tanks had mixed reviews of the BAMC as well. A report from Bruegel theorized that the “BAMC […] had a sound governance structure, though it did not have full political support for controversial restructurings of large distressed companies” (Lehmann 2017). The OECD had a more detailed perspective on the BAMC. Like the Court of Audit, it has problems with the BAMC’s governance framework. The OECD argued that the one-tier structure governed by a board largely appointed by the government gave the government undue influence on the BAMC’s operations (Novak 2015-03-04; Sila 2015). It argued that the “BAMC should have kept the ability to set its own remuneration policy “to attract adequate talent.” Additionally, they thought the BAMC should have had the power to lend money to borrowers (Sila 2015). It complimented the government for extended the BAMC’s mandate through 2015 and for strengthening the organization’s independence (OECD 2017). Another OECD report was concerned that the ZUKSB did not specify what would happen to “losses or profits of the BAMC at the end of its mandate” and that the BAMC’s “absence of capital buffers will also deter private investors who could be interested in buying BAMC bonds” in spite of said debt being guaranteed by the state. It goes on to assert that large capital buffers were necessary because “The Swedish experience demonstrates that asset management companies require sufficient funding and even have to be overcapitalised in order to be autonomous and free from political interference” (Havrylchyk 2013).

Reflecting on his time with the BAMC, CEO and Executive Director Imre Balogh wrote that he had several takeaways. The most notable of these are as follows, though Balogh did not provide explanations for them (Balogh 2018):

- The BAMC’s early operations could have been much more efficient if there had been “careful preparation”

- Organizational frameworks and management systems are extremely important

- One should never call an AMC a bad bank

- AMCs should establish “quick wins” and avoid highly visible expenses to gain public support

- AMCs need to start with viable anti-corruption mechanisms

- There should not be disclosure of “on-going transactions”

- Majority private ownership can be desirable

- The AMC should not intervene in individual business decisions and employ prudential oversight of banks

- One should minimize the AMC’s “cash-burn period”

- Banks should share profits and losses of the AMC over time as an alternative to upfront haircuts

- The AMC should be able to lend to participating debtors as a way to help them successfully progress through their business plans to viability

- AMCs should have “capital cover or pre-defined wind-up mechanism for [the] loss making tail period of AMC,” but should also avoid fire-sale dynamics

- Only purchase “high impact, high volume, relatively homogenous asset classes”

- There should be pre-defined selection and dismissal procedures for executives

- Agence France Presse (AFP). 2012. “Recession-plagued Slovenia can still avoid b…

- Agence France Presse (AFP). 2012. “Slovenia approves ‘bad bank’, backs with 4 b…

- Agence France Presse (AFP). 2012. “Slovenian opposition pushes for referendum o…

- Balogh, Imre. 2017. September 18. “Slovenia’s Experience with NPL Resolution.”

- Balogh, Imre. 2018. May 15. “Lessons Learned from the Work of DUTB.”

- Bardutzky, Samo. 2016. “Constitutional Transformations at the Edge of a Bail-Ou…

- Bank Assets Management Company (BAMC). n.d. “BAMC ETHIC Intelligence Certificat…

- Bank Assets Management Company (BAMC). n.d. “History.” Accessed November 2, 201…

- Bank Assets Management Company (BAMC). n.d. “Stakeholder strategies.” Accessed …

- Bank Assets Management Company (BAMC). 2014. Annual Report 2013.

- Bank Assets Management Company (BAMC). 2014. The 2014 Unaudited Half-Year Repor…

- Bank Assets Management Company (BAMC). 2014. February 6. “BAMC funding in 2013…

- Bank Assets Management Company (BAMC). 2014. February 10. “Committee on Finance…

- Bank Assets Management Company (BAMC). 2014. October 30. “BAMC is surprised tha…

- Bank Assets Management Company (BAMC). 2014. December 18. “BAMC to pay € 127 mi…

- Bank Assets Management Company (BAMC). 2014. December 18. “Time to take a look …

- Bank Assets Management Company (BAMC). 2015. BAMC Annual Report for 2014.

- Bank Assets Management Company (BAMC). 2016. BAMC 2015 Operations Report to the…

- Bank Assets Management Company (BAMC). 2015. February 11. “BAMC launches intern…

- Bank Assets Management Company (BAMC). 2015. July 13. “Higher court acknowledge…

- Bank Assets Management Company (BAMC). 2015. September 24. “BAMC obtains intern…

- Bank Assets Management Company (BAMC). 2015. September 28. “There have been no …

- Bank Assets Management Company (BAMC). 2015. October 6. “Letter of the Chairman…

- Bank Assets Management Company (BAMC). 2015. October 7. “Introductory speech fr…

- Bank Assets Management Company (BAMC). 2015. October 12. “A letter from Metod D…

- Bank Assets Management Company (BAMC). 2015. October 12. “Marko Simoneti and Im…

- Bank Assets Management Company (BAMC). 2015. October 23. “BAMC submits two amen…

- Bank Assets Management Company (BAMC). 2016. BAMC Annual Report 2015.

- Bank Assets Management Company (BAMC). 2016. December. BAMC Business Strategy 2…

- Bank Assets Management Company (BAMC). 2016. February 17. “Merger of Factor Ban…

- Bank Assets Management Company (BAMC). 2017. April. BAMC Annual Report 2016.

- Bank Assets Management Company (BAMC). 2018. April. BAMC Annual Report 2017.

- Bank Assets Management Company (BAMC). 2018. September. BAMC Half-Year Report 2…

- Bank Assets Management Company (BAMC). 2019. February. BAMC Business Strategy 2…

- Bank Assets Management Company (BAMC). 2019. July. BAMC Annual Report 2018.

- Bank for International Settlements (BIS). 2014. February 15. “Benoît Cœuré: Int…

- Bank of Slovenia. 2013. “Clarification of the Bank of Slovenia’s role in drafti…

- Bank of Slovenia. 2013. “Frequently asked questions and answers regarding the r…

- Bank of Slovenia. 2013. “Full Report on the Comprehensive Review of the Banking…

- Bank of Slovenia. 2014. July 17. “Policy Strategy Paper for Slovenia.”

- Bank of Slovenia. 2015. March. “Report of the Bank of Slovenia on the causes of…

- Bank of Slovenia. 2019. October. Economic and Financial Developments No.: Octob…

- Brierley, David. 2012. “Slovenia hops on the bad bank bandwagon.” SNL European …

- Carney, Sean. 2012. “Slovenian Cabinet OKs Plan to Create Fund for Bad Bank Ass…

- Cerne, Alenka, Sanja Borkovic, and Peter Tabak. 2018. Slovenia Diagnostics: Ass…

- Cerruti, Caroline Marie Cecile; et al. 2019. Distressed Asset Recovery Program …

- Communication from the Commission on the treatment of impaired assets in the Co…

- Council of the European Union. 2016. August 18. Official Journal of the Europea…

- Damijan, Jože P. 2012. October 8. “What went wrong in Slovenia and how to get o…

- conomic Intelligence Unit (EIU). 2013. July 5. “Transfer of bad loans delayed.”

- Economic Intelligence Unit (EIU). 2013. October 7. “Is Slovenia another Spain?”

- Economic Intelligence Unit (EIU). 2013. November 5. “Government reforms enter c…

- Economic Intelligence Unit (EIU). 2014. January 2. “Bad loan transfers begin.”

- Economic Intelligence Unit (EIU). 2014. July 30. “BAMC: from bad to good?”

- Economic Intelligence Unit (EIU). 2015. October 9. “Government ousts chairman a…

- Economic Intelligence Unit (EIU). 2015. November 19. “Banking sector remains a …

- European Central Bank (ECB). 2012. September 19. OPINION OF THE EUROPEAN CENTRA…

- European Central Bank (ECB). 2013. August 13. OPINION OF THE EUROPEAN CENTRAL B…

- European Central Bank (ECB). 2013. March 22. OPINION OF THE EUROPEAN CENTRAL BA…

- European Central Bank (ECB). 2015. “The fiscal impact of financial sector suppo…

- European Commission. 2011. March 7. “State aid: Commission temporarily clears s…

- European Commission. 2012. May 30. COMMISSION STAFF WORKING DOCUMENT: Assessmen…

- European Commission. 2013. April 10. COMMISSION STAFF WORKING DOCUMENT: In-dept…

- European Commission. 2013. April. Macroeconomic Imbalances Slovenia 2013. Europ…

- European Commission. 2013. May 29. COMMISSION STAFF WORKING DOCUMENT: Assessmen…

- European Commission. 2014. “Graph of the Week: The Net International Investment…

- European Commission. 2019. February 27. COMMISSION STAFF WORKING DOCUMENT: Coun…

- European Commission. Directorate-General for Competition (DG Comp). State Aid G…

- European Commission. Directorate-General for Competition (DG Comp). State Aid G…

- European Commission. EUROSTAT. Directorate D: Government Finance Statistics (GF…

- Gandrud, Christopher, and Mark Hallerberg. 2016. “Statistical Agencies and Resp…

- Georgiev, Georgi. 2013. “UPDATE 1 - Slovenian lenders face 4.78 bln euro capita…

- Gillet, Kit. 2019. “The Caution Behind Slovenia’s Optimism.” The Banker, Decemb…

- Government of The Republic of Slovenia. 2013. May. “National Reform Programme 2…

- Government of The Republic of Slovenia. 2018. April. “National Reform Programme…

- Guardiancich, Igor. 2016. “Slovenia: The End of a Success Story? When a Partial…

- Havrylchyk, Olena. 2013. “Banks’ Restructuring and Smooth Deleveraging of the P…

- Heinz, Frigyes F, and Yan Sun. 2014. “Sovereign CDS Spreads in Europe: The Role…

- International Monetary Fund. 2009. Republic of Slovenia: 2009 Article IV Consul…

- International Monetary Fund. 2011. Republic of Slovenia: 2011 Article IV Consul…

- International Monetary Fund. 2012. Republic of Slovenia: 2012 Article IV Consul…

- International Monetary Fund. 2014. Republic of Slovenia: 2013 Article IV Consul…

- International Monetary Fund. 2014. January 24. “Transcript of a conference call…

- International Monetary Fund. 2015. Republic of Slovenia: 2014 Article IV Consul…

- International Monetary Fund. 2017. Republic of Slovenia: 2017 Article IV Consul…

- International Monetary Fund. 2019. Republic of Slovenia: 2018 Article IV Consul…

- Iwanicz-Drozdowska, Małgorzata, Jakub Kerlin, Anna Kozłowska, Elżbieta Malinows…

- Krzan, Marko. 2014. “Crisis in Slovenia: Roots, Effects, Prospects.” Middle Eas…

- Lehmann, Alexander. Carving out legacy assets: a successful tool for bank restr…

- Lindstrom, Nicole. 2015. “Wither Diversity of Post-Socialist Welfare Capitalist…

- Markovic-Hribernik, Tanja and Matej Tomec. 2015. January. “Bad Bank And Other P…

- NLB Group (BAMC). 2012. April. NLB Group Annual Report 2011.

- Novak, Marja. 2015. “Slovenian supervisor finds possible criminal activity at s…

- Nyberg, Lars. 2014. “Bank Assets Management Company – Experiences so far.” Banč…

- O’Reilly, Carina. 2012. “Slovenian opposition calls for referendum on economic …

- Organisation for Economic Cooperation and Development (OECD). 2009. July 1. OEC…

- Organisation for Economic Cooperation and Development (OECD). 2012. July 18. “S…

- Piroska, Dóra and Ana Podvršič. 2019. October 1. “New European Banking Governan…

- Premrl, Peter. 2015. June. “Corruption Risks in the Process of Establishing the…

- Republic of Slovenia. 2015. July 12. “ORDINANCE On State Assets Management Stra…

- Sila, Urban. 2015. “Restoring the financial sector and corporate deleveraging i…

- Slovene Press Agency (STA). 2012. “Governor Kranjec Sceptical about Plans for B…

- Slovene Press Agency (STA). 2012. “Coalition to Discuss NLB, State Assets Holdi…

- Slovene Press Agency (STA). 2012. “Pensioners, Unions Oppose Sovereign Holding …

- Slovene Press Agency (STA). 2012. “Unions, Employers Welcome Decision To Postpo…

- Slovene Press Agency (STA). 2012. “Slovenia Likely to Set up Bad Bank.” August …

- Slovene Press Agency (STA). 2012. “Central Bank Advises Caution in Plans for Ba…

- Slovene Press Agency (STA). 2012. “Delo Poll Puts Türk and Pahor in Run-off.” A…

- Slovene Press Agency (STA). 2012. “Bank Association Boss Welcomes Plan to Set u…

- Slovene Press Agency (STA). 2012. “Govt Adopts Bill Establishing a Bad Bank (ad…

- Slovene Press Agency (STA). 2012. “Committee Endorses Bad Bank Bill Despite War…

- Slovene Press Agency (STA). 2012. “Trade Union Referendum Initiative Also Targe…

- Slovene Press Agency (STA). 2012. “National Council Vetoes Bad Bank Act.” Octob…

- Slovene Press Agency (STA). 2012. “Žerjav and Vizjak Warn Against Referenda on …

- Slovene Press Agency (STA). 2012. “Chamber of Commerce Critical of Govt Approac…

- Slovene Press Agency (STA). 2012. “Minister, Unions Negotiating in Attempt to A…

- Slovene Press Agency (STA). 2012. “National Council Rejects Bad Bank, Sovereign…

- Slovene Press Agency (STA). 2012. “Speaker Sets Deadline for 40,000 Signatures …

- Slovene Press Agency (STA). 2012. “MPs Asks Constitutional Court to Review Bad …

- Slovene Press Agency (STA). 2012. “Top Court Bans Holding, Bad Bank Referendum …

- Slovene Press Agency (STA). 2013. “Bad Bank to Remain in Operation Longer than …

- Slovene Press Agency (STA). 2014. “Corruption Watchdog Investigating Bad Bank D…

- Slovene Press Agency (STA). 2014. “Disclosure Limited to Loans at Bad Bank as T…

- Slovene Press Agency (STA). 2015. “Bad Bank ‘Getting it Done’, Boss Says.” Augu…

- Slovene Press Agency (STA). 2015. “Bad Bank Claims Executive Pay in Line with R…

- Slovene Press Agency (STA). 2015. “Two Turbulent Years of the Bank Asset Manage…

- Slovene Press Agency (STA). 2015. “Večer Sees Bad Bank as Battleground of Lobbi…

- Slovene Press Agency (STA). 2018. “Bad bank gets adverse audit opinion for 2014…

- Slovene Press Agency (STA). 2018. “Prosecution eyes five former bad bank execut…

- Slovene Press Agency (STA). 2019. “Committee discusses possibility to shut down…

- Slovene Press Agency (STA). 2019. “Report: SDS MP no longer among suspects in B…

- Slovene Press Agency (STA). 2019. “Former NLB, NKBM chairman say banks had no i…

- Slovenian Press Agency (STA). 2019. “BAMC inquiry hears first witnesses.” Octob…

- Slovenian Press Agency (STA). 2019. “Bratušek, Čufer defend massive 2013 bank b…

- Slovenian Press Agency (STA). 2019. “Bad bank wants to use its assets to build …

- Slovenian Press Agency (STA). 2019. “Finance says BAMC should be shut down as p…

- The Slovenia Times. 2014. “Bad Bank With “Bad Habits.” February 6, 2014.

- The Slovenia Times. 2015. “Govt Appoints New Directors at BAMC, Cuts Pay.” Marc…

- The Slovenia Times. 2019. “Matej Pirc appointed CEO of BAMC.” April 26, 2019.

- Stevis, Matina. 2012. “DJ UPDATE: Euro Zone Finance Ministers Flesh Out Spain B…

- Uradni List Republike Slovenije. 2012. “Stevilka 105. Oradni list RS, st. 105/2…

- Uradni List Republike Slovenije. 2013. “Stevilka 103. Oradni list RS, st. 103/2…

- Unofficial ZUKSB translation. 2015.

- World Bank. 2016. Bank resolution and bail-in in the EU: selected case studies …

Key Program Documents

-

BAMC Business Strategy 2016-2022

The BAMC’s first published strategy document. It outlines some of the changes that came to the organization after 2015.

-

Bank Assets Management Company –Experiences so far (2014)

This article from one of the BAMC’s early executives outlines the many difficulties associated with getting the BAMC up and running

-

SLOVENIA SEVERAL DOMESTIC BANKS: RESOLUTION VIA PUBLIC RECAPITALIZATION AND BAIL-IN (2013)

Case study on Slovenia’s capital injections and asset transfers during the global financial crisis.

-

Report from the European Commission DG Comp, Subject: State aid n° SA.37690 (2013/N) Rescue aid in favour of Abanka d. d. (December 18, 2013)

This state aid decision did not approve any asset transfers from Abanka to the BAMC, but set down a path for the government to develop a more detailed restructuring plan. It also approved a temporary capital injection by the government, which would be used to keep the institution alive until the EC could approve a more comprehensive plan.

-

Report from the European Commission DG Comp, Subject: State aid n° SA.38228 (2014/N) Restructuring of Abanka Vipa Group - Slovenia (August 13, 2014)

This state aid decision approved asset transfers from Abanka to the BAMC, a number of capital injections, and a more detailed restructuring plan.

-

Report from the European Commission DG Comp, Subject: State aid SA.38522 (2014/N) – Slovenia Restructuring aid for Banka Celje/Abanka (December 16, 2014)

This state aid decision approved a merger of Banka Celje and Abanka, a restructuring of the merged bank, a €190 million recapitalization of the merged bank, and asset transfers from the merged bank to the BAMC.

-

Report from the European Commission DG Comp, Subject: State aid n° SA.37643 (2013/N) – Slovenia Orderly winding down of Factor Banka d. d. (December 18, 2013)

This state aid decision approved the winding down and transfer of Factor Banka’s remaining assets to the BAMC.

-

Report from the European Commission DG Comp, Subject: State aid n° SA.35709 (2013/N) – Slovenia Restructuring of Nova Kreditna Banka Maribor d. d. (NKBM) – Slovenia (December 18, 2013)

This state aid decision approved the first recapitalization of NKBM for €100 million (temporarily approved by the rescue decision on 20 December 2012), the second recapitalization of €870 million, and an asset transfer to the BAMC.

-

Slovenia’s 2013-2014 National Reform Program (2013)

This document that Slovenia submitted to the European Commission outlines the country’s medium-term plan for achieving the EU 2020 Strategy. The BAMC was a major part of the plan’s attempt to induce bank recovery, corporate deleveraging, and restructuring. It also contains some early implementation plans for the BAMC as well as a status report on the BAMC’s asset purchases.

-

Act Amending the Act Defining the Measures of the Republic of Slovenia to Strengthen Bank Stability (In Slovene, Zakon o spremembah in dopolnitvah Zakona o ukrepih Republike Slovenije za krepitev stabilnosti bank (ZUKSB-A)) (Oradni list RS, st. 104/2015 z

Law amending the ZUKSB in several ways. One of the most notable is the extension of its wind-down date to 2022.

-

Act Defining the Measures of the Republic of Slovenia to Strengthen Bank Stability (In Slovene, Zakon o ukrepih Republike Slovenije za krepitev stabilnosti bank (ZUKSB)) (December 27, 2012)

Statute that created the BAMC.

-

CB GUIDING PRINCIPLES FOR BANK ASSET SUPPORT SCHEMES (February 25, 2009)

ECB guidance on the design of asset purchase operations.

-

Regulation Amending the Regulation Implementing Measures to Strengthen Bank Stability (In Slovene, Uredba o spremembah in dopolnitvah Uredbe o izvajanju ukrepov za krepitev stabilnosti bank) (Oradni list RS, st. 51/2013 z dne 14.6.2013) (June 14, 2013)

Amendment of regulation outlining eligibility for participation in the BAMC as well as the details of how the BAMC would operate. There is no overarching theme to the changes, but several pertain to how the BAMC interacts with various European institutions.

-

Regulation Amending the Regulation Implementing Measures to Strengthen Bank Stability (In Slovene, Uredba o spremembah in dopolnitvah Uredbe o izvajanju ukrepov za krepitev stabilnosti bank) (Oradni list RS, st. 22/2016 z dne 25.3.2016) (March 25, 2016)

Amendment to earlier regulations meant to bring them into accord with the December 2015 amendments to the ZUKSB.

-

Regulation Implementing Measures to Strengthen Bank Stability (In Slovene, Uredba o izvajanju ukrepov za krepitev stabilnosti bank) (Oradni list RS, st. 22/2013 z dne 15.3.2013) (March 15, 2013)

Regulation outlining eligibility for participation in the BAMC as well as the details of how the BAMC would operate.

-

Regulation Implementing Measures to Strengthen Bank Stability (In Slovene, Uredba o izvajanju ukrepov za krepitev stabilnosti bank) (Oradni list RS, st. 103/2013 z dne 11.12.2013) (December 11, 2013)

Regulation outlining how the BAMC borrows and pays dividends, the conditions that business plans must fulfill, and several other elements of the BAMC’s operations.

-

Bank Assets Management Company – Experiences so far (2014)

This article from one of the BAMC’s early executives outlines the many difficulties associated with getting the BAMC up and running.

-

Banks’ Restructuring and Smooth Deleveraging of the Private Sector in Slovenia (June 14, 2013) (Olena Havrylchyk)

Working paper accompanying the OECD’s 2013 Economic Review of Slovenia, which summarizes the roots and details of Slovenia’s banking troubles. It also lays out the BAMC’s potential role in solving those problems as well as several obstacles the BAMC will face along the way.

-

Constitutional Transformations at the Edge of a Bail-Out: The Impact of the Economic Crisis on the Legal and Institutional Structures in Slovenia (2016)

Research paper discussing the progression of Slovenia’s economic crisis and how events during the crisis transformed Slovenia’s constitutional structures. The narrative features the BAMC several times.

-

Restoring the financial sector and corporate deleveraging in Slovenia (2014)

Working paper accompanying the OECD’s 2015 Economic Review of Slovenia that has a particularly good summary of Slovenia’s stress testing, capital injection, and asset management programs.

-

Sovereign CDS Spreads in Europe: The Role of Global Risk Aversion, Economic Fundamentals, Liquidity, and Spillovers (Heinz and Sun)

2014 IMF working paper that spends a significant time discussing the impact of the GFC over time in Central, Eastern, and South-Eastern Europe.

-

A letter from Metod Dragonja, state secretary at the Ministry of Finance (October 2015)

Letter from the Finance Ministry noting that it had officially filled the two vacant board positions at the BAMC with two Slovenians and refuting some of Nyberg’s claims.

-

BAMC submits two amended internal by-laws and signed employment agreements for executive directors to the Court of Audit (October 2015)

A press release following the transition from foreign to Slovenian leadership claiming that the BAMC had taken actions to resolve the Court of Audits concerns.

-

Committee on Finance and Monetary Policy Introduction by Dr Lars Nyberg, chairman of the management board (February 2014)

Speeches by two executives at BAMC that address the progress of the BAMC as well as various allegations and misunderstandings as to the organization’s operations.

-

Frequently asked questions and answers regarding the reorganisation of the Slovenian banking system (published by the Bank of Slovenia in December 2013)

FAQ sheet from the Bank of Slovenia which details the results of stress tests, the government’s short-term response, long-term response, and the question of punishing responsible actors in the economic crisis.

-

Introductory speech from dr. Lars Nyberg at the meeting of the Committee on Financial and Monetary policy (October 2015)

Lars Nyberg’s address upon his leaving the BAMC.

-

Letter of the Chairman of the Board to the Minister of Finance (October 2015)

Letter from one executive at the BAMC (shortly after his departure was announced) that makes a case for his salary and the BAMC’s divergence from a new compensation policy.

-

Marko Simoneti and Imre Balogh take the helm of BAMC (October 2015)

Announcing that two Slovenians would be taking over the leadership of the BAMC after the departure of foreign leadership.

-

Merger of Factor Banka and Probanka to BAMC confirmed by the Government of the Republic of Slovenia (2016)

Press release announcing the merger of Factor Banka and Probanka. It includes statements explaining the rationale for the merger and how it relates to the management of toxic assets.

-

BAMC Annual Report for 2014 (July 2015)

Annual report outlining the BAMC’s financial results and overall performance in 2014.

-

BAMC UNAUDITED HALF-YEAR REPORT 2015 (August 26, 2015)

Overview of the BAMC’s performance in the first half of 2015. Contains details on the BAMC’s conflict with the Court of Audit.

-

BAMC 2015 OPERATIONS REPORT TO THE NATIONAL ASSEMBLY IN ACCORDANCE WITH ARTICLE 15 OF ZUKSB (June 2016)

Extensive review of the BAMC’s operations through 2015. It functions much like a refocused annual report.

-

BAMC Annual Report 2015 (September 2016)

Annual report discussing the year in which there were significant management changes at NAMA.

-

BAMC Annual Report 2016 (April 2017)

Report outlining the BAMC’s financial results and overall performance in 2016.

-

BAMC HALF-YEAR REPORT 2016 (September 2016)

Unaudited report during the period when the merger of Probanka and Factor Banka into BAMC occurred. At this point the organization was hitting all its KPIs but for economic return on equity.

-

BAMC HALF-YEAR REPORT 2017 (September 2017)

Unaudited report during a period where the BAMC has a positive sentiment as to its performance, coming after a year where they significantly reduced their assets under management.

-

BAMC Annual Report 2017 (April 2018)

Report outlining the BAMC’s financial results and overall performance in 2017.

-

BAMC HALF-YEAR REPORT 2018 (September 2018)

Unaudited report during a period where the BAMC is broadly hitting its KPIs.

-

BAMC Annual Report 2018 (July 2019)

Report outlining the BAMC’s financial results and overall performance in 2018.

-

Bank of Slovenia Financial Stability Review, January 2016

Review of Slovenia’s financial position during a year in which the banking system continued its recovery. Overall, it had a positive outlook.

-

Bank of Slovenia Policy Strategy Paper for Slovenia 2016 (December 2016)

Update of the 2015 policy strategy paper. It happens in the shadow of significant structural reforms in Slovenia which were put forward by the EU.

-

Bank of Slovenia Financial Stability Review, May 2009

Financial stability report discussing the immediate impact of the 2008 market turmoil on the Slovenian financial system. It notes that without the return of international funding or significant fiscal policy on the part of the government, the Slovenian banking system would be under extreme stress. It also provides a fairly comprehensive view of Slovenia’s economy during this time.

-

Bank of Slovenia Financial Stability Review, May 2010

Financial stability report that details the coming credit crunch that followed the initial shock of the GFC in Slovenia. It also provides a fairly comprehensive view of Slovenia’s economy during this time.

-

Bank of Slovenia Financial Stability Review, May 2013

Financial stability report that features Slovenia’s dip back into recession.

-

Bank of Slovenia Financial Stability Review, May 2014

Central bank outline of risks to the Slovenian financial system. Most notably, it outlines the beginning economic recovery.

-

Bank of Slovenia Financial Stability Review, May 2015

Review on Slovenia’s improving economic growth accompanied by continuing uncertainties as to the condition of the financial system.

-

Bank of Slovenia Policy Strategy Paper for Slovenia, July 17, 2014

Short paper from the Bank of Slovenia that describes the policy environment and puts forward economic policy recommendations.

-

DUTB (BAMC) Annual Report 2013

The BAMC’s first annual report, which was subject to increased scrutiny from the Slovenian government and chronicled the multiple challenges the team had getting the BAMC running.

-

Full Report on the comprehensive review of the banking, December 16, 2013 (Report by Bank of Slovenia)

June through December 2013 results for the Stress Test and Asset Quality Report.

-

Lessons Learned from the Work of DUTB (2018)

Presentation by the CEO and Executive Director of the BAMC that provides an overview of the BAMC’s performance. There are several slides that note best practices for AMCs.

-

Macroeconomic Development and Projections, April 2014 (Report by Bank of Slovenia)

Central bank outline of economic projections. It is the first relatively optimistic report we see from BoS during this crisis.

-

Presentation in Paris by Peter Premrl of the Commission for the Prevention of Corruption (CPC) on Corruption Risks in the Process of Establishing the Bad Bank in Slovenia (June 2015)

Presentation on the corruption risks and mitigation tools related to the BAMC.

-

Report of the Bank of Slovenia on the causes of the capital shortfalls of banks and the role of the Bank of Slovenia as the banking regulator

Review of Slovenia’s Euro crisis response measures.

-

Report on comprehensive review of the banking system and associated measures, 2013 (Report by Bank of Slovenia)

Document containing results from Slovenia’s Stress Test and Asset Quality Review.

-

Stability of the Slovenian Banking System, December 2010 (Report by Bank of Slovenia)

Overview of risks to financial stability in Slovenia during the first ten months of 2010. It shows increasing pressure on the economy and breaks down financial risks into several categories for discussion.

-

Stability of the Slovenian Banking System, January 2014 (Report by Bank of Slovenia)

Overview of risks to financial stability in Slovenia during 2013. It shows increasing pressure on the economy and breaks down financial risks into several categories for discussion. Its discussion of the BAMC notes that the organization’s operations increased credit quality near the end of 2013.

-

Stability of the Slovenian Banking System, December 2014 (Report by Bank of Slovenia)

Overview of risks to financial stability in Slovenia during 2013. It shows increasing pressure on the economy and breaks down financial risks into several categories for discussion.

-

THE 2014 UNAUDITED HALF-YEAR REPORT OF THE BAMC January – June 2014 (August 27, 2014)

Overview of BAMC operations for the first half of 2014.

Taxonomy

Intervention Categories:

- Broad-Based Asset Management Programs

Countries and Regions:

- Slovenia

Crises:

- Global Financial Crisis